Atopic Dermatitis Clinical Trials Market Report Scope & Overview:

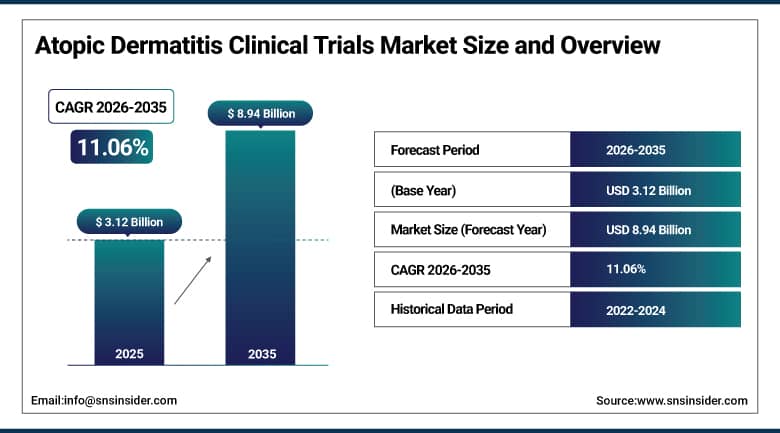

The Atopic Dermatitis Clinical Trials Market was valued at USD 3.12 billion in 2025 and is expected to reach USD 8.94 billion by 2035, growing at a CAGR of 11.06% from 2026 to 2035.

Atopic dermatitis is the most common chronic inflammatory skin disease worldwide. It affects an estimated 230 million people across all age groups and imposes a significant quality-of-life burden characterized by persistent itch, sleep disruption, anxiety, and social impairment. For decades, treatment was dominated by topical corticosteroids that managed symptoms inadequately and carried long-term safety limitations.

More than 70 compounds are currently in active clinical development for moderate to severe atopic dermatitis globally. Pharmaceutical companies are funding interventional trials, real-world evidence studies, and pediatric extension programs at unprecedented scale. The commercial incentive is clear. Dupilumab generated approximately USD 11.6 billion in revenue across all indications in 2024, with roughly 60% attributable to atopic dermatitis. Competing biologics and JAK inhibitors from AbbVie, Eli Lilly, Leo Pharma, and Pfizer have each secured approvals and are building market positions. New entrants are targeting differentiated mechanisms including IL-31 inhibition, IL-33 blockade, and TSLP antagonism to establish clinical and commercial differentiation from the approved agents.

Market Size and Forecast

-

Market Size 2026E: USD 3.48 Billion

-

Market Size 2035: USD 8.94 Billion

-

CAGR: 11.06% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Atopic Dermatitis Clinical Trials Market - Request Free Sample Report

Atopic Dermatitis Clinical Trials Market Trends

-

The FDA's June 2024 extension of dupilumab approval to infants as young as six months has opened a new pediatric trial frontier, with several companies now designing or enrolling Phase III studies in infant and toddler atopic dermatitis populations that were previously underserved by approved therapies.

-

JAK inhibitor oral and topical therapies including upadacitinib, abrocitinib, and ruxolitinib cream are generating Phase IV real-world evidence trials focused on long-term safety and comparative effectiveness that are expanding the post-approval clinical investment footprint.

-

Biomarker-driven patient stratification is being incorporated into advanced clinical trial designs, allowing sponsors to enrich trial populations based on IgE levels, TARC concentrations, and specific comorbidity profiles to improve response rate predictability and regulatory submission strength.

-

China's inclusion of tralokinumab on its national reimbursement drug list in December 2024 has catalyzed Phase III and Phase IV clinical program investment by multiple international and domestic Chinese companies targeting the country's large and commercially underserved atopic dermatitis patient population.

-

Combination therapy trials evaluating biologics alongside topical therapeutics and barrier repair agents are emerging as a scientifically credible strategy for achieving complete skin clearance in patients with severe disease who show incomplete response to biologic monotherapy.

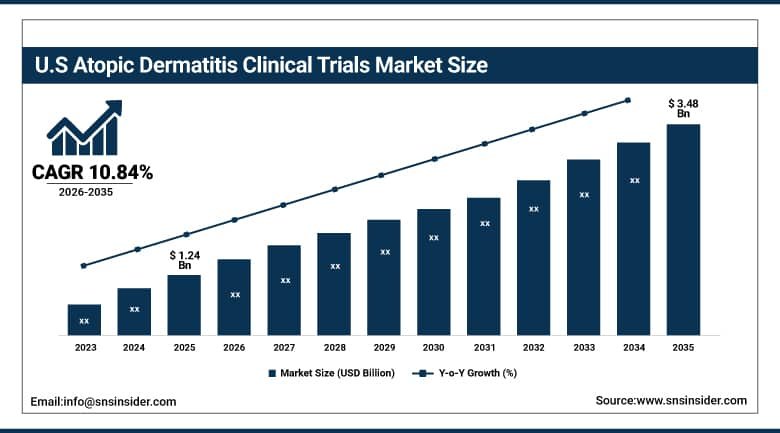

The U.S. Atopic Dermatitis Clinical Trials Market Size Outlook

The U.S. Atopic Dermatitis Clinical Trials Market was valued at USD 1.24 billion in 2025 and is expected to reach around USD 3.48 billion by 2035, growing at a CAGR of 10.84% from 2026 to 2035.

The U.S. leads as the global market in atopic dermatitis clinical trials, based on commercial and clinical activity. It owes this leadership position to numerous strengths. Firstly, the FDA has been a good partner in the regulation of this sector by approving many new mechanism agents from 2017 and giving guidelines on trial designs and patient endpoints. Secondly, the U.S. healthcare system supports wide usage of biologics through its reimbursement framework of private health insurances and Medicare Part D. This creates high patient participation levels during clinical trials, thereby reducing drop-out rates in clinical trials. Thirdly, the presence of academic medical centers with dedicated dermatological and allergic clinics such as Mayo Clinic, Cleveland Clinic, Harvard, and Stanford adds to the strong pool of clinical investigators and patient recruitment channels.

The clinical development program for lebrikizumab by Eli Lilly, which received FDA approval in 2023 for adults with moderate to severe atopic dermatitis, included extensive Phase III trial enrollment at U.S. sites that generated the comparative efficacy and safety data required for regulatory approval and payer reimbursement negotiation. Post-approval Phase IV studies evaluating lebrikizumab in pediatric populations and in combination with topical therapies are continuing to generate clinical data that supports formulary access and label expansion in the U.S. market.

Atopic Dermatitis Clinical Trials Market Segment Analysis

-

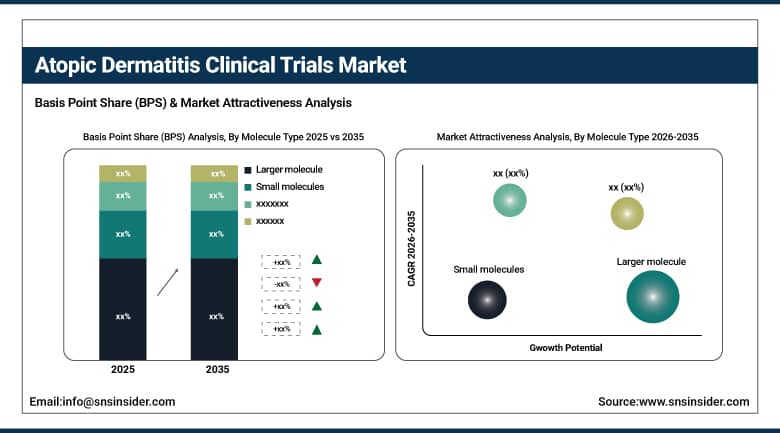

By Molecule Type, the large molecules segment dominated the atopic dermatitis clinical trials market with 56.38% share in 2025, while the small molecules segment is the fastest growing.

-

By Study Phase, the Phase III segment dominated the atopic dermatitis clinical trials market with 47.25% share in 2025, while the Phase II segment is the fastest growing study phase.

-

By Study Design, the interventional trials segment dominated the atopic dermatitis clinical trials market with 63.48% share in 2025, while observational trials are the fastest growing study design.

-

By Sponsor Type, the pharmaceutical and biopharmaceutical companies segment dominated the atopic dermatitis clinical trials market with 58.74% share in 2025, while CROs are the fastest growing sponsor type.

-

By Therapeutic Class, the biologics and monoclonal antibodies segment dominated the atopic dermatitis clinical trials market with 52.63% share in 2025, while JAK inhibitors are the fastest growing therapeutic class.

By Molecule Type, the large molecules segment dominates the market, while the small molecules segment is the fastest-growing.

Larger molecule therapies represented a majority 56.38% share in the revenue generated by the atopic dermatitis clinical trial market in 2025. Commercialization success with dupilumab served as a clear validation of concept, highlighting the efficacy of precision targeting with monoclonal antibodies over generic systemics. The clinical data drove pharmaceutical funding into the development of novel biologics. Tralokinumab, lebrikizumab, and nemolizumab represent three unique biologics that target unique mechanisms in the immune cascade involved in atopic dermatitis. The inherent expense involved in biologic trials is driven by manufacturing complexity, trial site specialization, and duration resulting in maximum per-trial revenue in this category.

Small molecules are growing the fastest. JAK inhibitors in particular have generated intense commercial and clinical interest. Upadacitinib from AbbVie demonstrated head-to-head superiority over dupilumab on some efficacy endpoints in Phase III data presented at major dermatology congresses. This result shifted prescribing and research attention toward oral small molecule options that offer administration convenience advantages over subcutaneous biologic injections. The atopic dermatitis clinical trial pipeline for small molecules includes JAK inhibitors, PDE4 inhibitors, TSLP receptor antagonists, and novel topical agents. Regulatory agencies in the U.S., Europe, and Japan have each issued guidance on JAK inhibitor safety labeling requirements that are shaping trial design for this drug class across the forecast period.

By Study Phase, the Phase III segment dominates the market, while Phase II is the fastest-growing study phase.

Phase III trials generated 47.25% of clinical trial market revenue in 2025. This dominance reflects both the cost structure of Phase III programs and the extraordinary commercial value that pharmaceutical companies assign to confirmatory efficacy data in a therapy area where approved products generate billions of dollars annually. A successful Phase III trial in moderate to severe atopic dermatitis represents one of the most commercially significant clinical milestones in dermatology. Phase III programs in atopic dermatitis typically involve multicenter, double-blind, placebo-controlled designs enrolling several hundred to over a thousand patients across multiple countries. The investigator fees, site costs, patient stipends, clinical operations, and regulatory activities associated with programs of this scale make Phase III the highest absolute revenue contributor within the market.

Phase II is growing fastest because the pipeline entering early clinical evaluation has expanded significantly. Companies that identified differentiated mechanisms following the biologic and JAK inhibitor successes are now advancing their compounds through Phase II dose-finding and efficacy exploration studies. Phase II trials serve the commercial function of establishing proof of concept before major Phase III investment commitments are made. Investors, licensing partners, and acquirers use Phase II data as the primary trigger for transaction decisions. The density of Phase II activity in atopic dermatitis is therefore an early indicator of the Phase III pipeline that will sustain market growth over the next five to seven years. This pipeline richness gives the clinical trials market a durable structural growth outlook.

By Study Design, the interventional trials segment dominates the market, while observational trials are the fastest-growing segment.

Interventional trials held 63.48% of market revenue in 2025. Randomized controlled interventional trials are the regulatory gold standard for drug approval in atopic dermatitis. FDA, EMA, and PMDA all require interventional Phase III data demonstrating superiority or non-inferiority to placebo or active comparators before granting marketing authorization. The regulatory requirement for interventional evidence makes this study design a structural constant within the clinical trial spending profile for any company seeking drug approval. Pharmaceutical companies fund interventional programs as a mandatory component of product development investment rather than as discretionary research expenditure, which creates a stable and predictable revenue base for clinical research organizations and site networks specializing in atopic dermatitis.

Observational studies are growing faster because the approved therapy landscape has matured to the point where real-world evidence has become commercially and medically essential. Payers are using comparative effectiveness data from observational registries to inform coverage decisions and step therapy protocols. Health technology assessment bodies in Europe require real-world evidence submissions for reimbursement recommendations. Prescribing physicians want evidence of how approved therapies perform in patients excluded from pivotal trials, including those with significant comorbidities or long treatment histories. Pharmaceutical companies fund prospective observational cohort studies and retrospective database analyses to generate this evidence in support of market access and label expansion objectives.

By Sponsor Type, pharmaceutical and biopharmaceutical companies dominate the market, while CROs are the fastest-growing sponsor type.

Pharmaceutical and biopharmaceutical companies generated 58.74% of clinical trial market revenue in 2025. Their spending dominance reflects the direct commercial alignment between clinical trial investment and drug approval outcomes. Large pharmaceutical companies with approved or near-approval atopic dermatitis programs fund extensive Phase III programs, global site networks, real-world evidence studies, and pediatric extension programs that collectively represent hundreds of millions of dollars in annual trial expenditure per product. The investment is justified by the commercial return profile of a successful atopic dermatitis drug, where peak annual sales commonly exceed USD 2 billion for agents that establish strong positioning in the moderate to severe patient segment.

CROs are growing fastest as a sponsor type because pharmaceutical companies are increasingly outsourcing the execution of their clinical programs to specialized contract research partners. The complexity of global multicenter atopic dermatitis trials, which span regulatory jurisdictions from the United States to Japan to Brazil, requires sophisticated site management, patient recruitment, data management, and regulatory submission capabilities that many pharmaceutical sponsors prefer to purchase from specialized CRO partners rather than build entirely in-house. CROs including ICON, Covance, Syneos Health, and PRA Health Sciences have developed dedicated dermatology trial practices with established site networks and therapeutic area expertise that accelerate program timelines and reduce sponsor resource requirements.

By Therapeutic Class, the biologics and monoclonal antibodies segment dominates the market, while JAK inhibitors are the fastest-growing therapeutic class.

Biologics and monoclonal antibodies accounted for 52.63% of atopic dermatitis clinical trial market revenue in 2025. The precision targeting capability of monoclonal antibodies against specific cytokines and receptors within the atopic inflammatory pathway has produced the most clinically impactful treatments in the history of atopic dermatitis therapy. Dupilumab demonstrated 75% improvement in EASI scores in pivotal trial populations. Subsequent biologics have demonstrated comparable or differentiated profiles that have collectively expanded the addressable population for effective targeted therapy. The scale of investment required to develop a biologic from candidate selection through Phase III registration and CMC manufacturing development positions large pharmaceutical companies as the primary funders of this therapeutic class.

JAK inhibitors are the fastest-growing therapeutic class in atopic dermatitis clinical trial investment. JAK inhibitors address the intracellular signaling cascades activated by multiple inflammatory cytokines simultaneously. This broad mechanism of action produces rapid and substantial symptom relief, including significant itch reduction within days of treatment initiation. The clinical speed advantage over biologic therapies is a meaningful commercial differentiator for patient populations where itch severity is the primary quality-of-life determinant. Both oral systemic JAK inhibitors and topical JAK inhibitor formulations are advancing through the development pipeline. The topical segment in particular addresses patients with mild to moderate disease who require effective symptom control without systemic immunosuppression, representing a large commercial population not primarily served by injectable biologics.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.72% |

|

Europe |

Germany |

28.46% |

|

Asia Pacific |

China |

36.74% |

|

Middle East & Africa |

Israel |

22.48% |

|

Latin America |

Brazil |

43.74% |

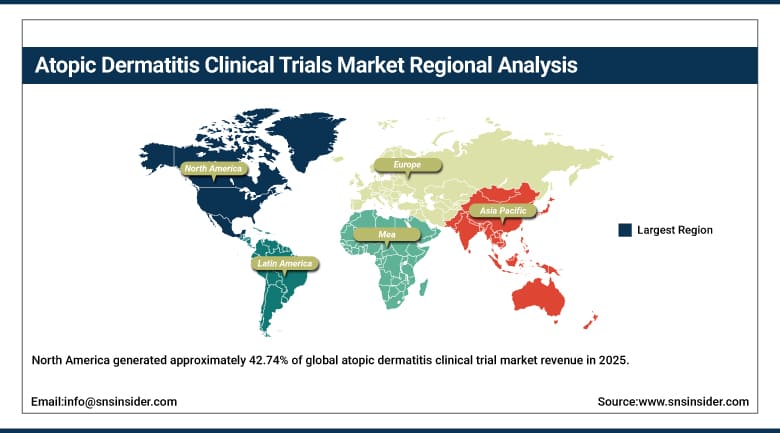

North America Atopic Dermatitis Clinical Trials Market Insights

North America generated approximately 42.74% of global atopic dermatitis clinical trial market revenue in 2025. The United States leads regional demand across every segment. Its combination of sophisticated clinical trial infrastructure, experienced dermatology investigator networks, broad patient access to clinical studies, and FDA regulatory efficiency makes it the preferred primary market for global Phase III program enrollment. Commercial insurance coverage of approved atopic dermatitis biologics has reached approximately 40% of eligible moderate to severe patients in the United States, a penetration rate that simultaneously demonstrates market maturity and the remaining growth opportunity for new entrants. Canada contributes supplementary regional demand through its provincial public health coverage programs and established academic dermatology research centers.

The United States telehealth and teledermatology infrastructure expansion that accelerated during the COVID-19 pandemic has measurably improved patient identification and clinical trial recruitment for atopic dermatitis programs. Patients in geographically remote areas who previously lacked access to specialist dermatology care are now identified, evaluated, and enrolled into clinical trials through virtual screening visits followed by in-person investigational site visits only at study-required timepoints. This model has expanded the effective geographic catchment area of U.S. atopic dermatitis trial sites substantially.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Atopic Dermatitis Clinical Trials Market Insights

Europe accounted for approximately 28.47% of global atopic dermatitis clinical trial market revenue in 2025. Germany, France, the United Kingdom, Denmark, Poland, and the Netherlands are the leading country-level contributors to European clinical trial activity. The EMA's established regulatory framework for biologic drug approval provides a clear development pathway for companies targeting European market authorization. European health technology assessment bodies including G-BA in Germany and NICE in the United Kingdom require robust comparative effectiveness evidence from clinical trials before granting full reimbursement status. This HTA requirement is a structural demand driver for Phase III and Phase IV clinical programs at European sites. Denmark has been a particularly active market for atopic dermatitis research, partly due to Leo Pharma's headquarters location and its extensive clinical research investment in the country.

Leo Pharma's global development program for tralokinumab included extensive Phase III enrollment across European sites, generating the clinical database required for EMA approval and subsequent European country-level HTA submissions. The company's continued Phase IV real-world evidence program across multiple European markets is generating ongoing clinical research economic activity that reinforces Denmark and other Nordic countries as primary European atopic dermatitis clinical trial destinations for both commercial and investigator-initiated studies.

Asia Pacific Atopic Dermatitis Clinical Trials Market Insights

Asia Pacific region is currently seen to be the fastest growing regional market with regard to the atopic dermatitis clinical trials, set to grow at a CAGR of about 13.24% from 2026 to 2035. China is seen as a key contributor to this growth in the region. Domestic firms of pharmaceuticals in China are undertaking the development of native biologics and small molecules in the treatment of atopic dermatitis in the process. For instance, there is CM310, an IL-4Ra inhibitor competitor of dupilumab, being developed in China by a firm called Keymed Biosciences. Japan and South Korea have already made substantial developments regarding clinical research infrastructure, and they are also having regulatory bodies whose policies match those internationally recognized, making them good candidates for registration trials. India is seen becoming an increasingly important venue for Phase I and Phase II clinical research.

China's National Medical Products Administration has substantially accelerated its review timelines for innovative drugs including biologics for dermatological conditions since implementing regulatory reforms in 2018. This regulatory improvement has encouraged multinational pharmaceutical companies to include Chinese patients in global Phase III atopic dermatitis programs, which simultaneously advances NMPA approval applications and contributes to faster global enrollment completion. Domestic Chinese companies including Henlius and Innovent have also initiated clinical development programs for atopic dermatitis biologics targeting market authorization through the domestic regulatory pathway.

Middle East & Africa and Latin America Atopic Dermatitis Clinical Trials Market Insights

The Middle East, Africa, and Latin America regions are smaller contributors to global atopic dermatitis clinical trial revenue but each contain commercially and scientifically important research markets. Israel is the dominant country within MEA, hosting internationally recognized dermatology research centers with established participation in multicenter global clinical programs. Israeli academic dermatologists have contributed meaningfully to registrational trials for approved atopic dermatitis biologics and maintain active relationships with major international pharmaceutical sponsors. Saudi Arabia and the UAE are investing in clinical research infrastructure as part of their broader healthcare modernization programs, creating emerging capacity for trial enrollment that could attract growing program investment during the forecast period. Brazil is the leading Latin American market, hosting the region's most experienced clinical research organizations and an established patient registry infrastructure for chronic dermatological conditions.

Brazil's regulatory agency ANVISA has implemented progressive harmonization with ICH guidelines for clinical trial conduct and drug approval, which has increased the country's attractiveness to multinational pharmaceutical sponsors seeking Latin American enrollment sites for global atopic dermatitis programs. The country's large and ethnically diverse patient population provides scientific value for programs where phenotypic and demographic diversity in trial populations strengthens the generalizability of clinical evidence for regulatory and commercial purposes.

Market Dynamics

Growth Drivers: A rich and rapidly expanding atopic dermatitis therapeutic pipeline and growing global disease prevalence are sustaining exceptional clinical trial market growth across all major regions.

Global atopic dermatitis prevalence is increasing. Environmental factors including urbanization, reduced microbial exposure in early childhood, increased air pollution, and dietary changes are each implicated in the rising incidence observed across high-income and emerging market countries. More patients with moderate to severe disease are being recognized and diagnosed as specialist dermatology services expand globally. More diagnosed patients create larger eligible trial populations. More eligible trial populations attract greater commercial trial investment. This cycle of clinical and commercial reinforcement is structurally self-sustaining throughout the forecast period. The commercial success of approved agents also provides pharmaceutical companies with the revenue confidence to fund aggressive pipeline investment, creating a financial feedback loop that sustains high levels of new trial initiation even as the approved therapy landscape matures.

Restraints: Increasing competition for experienced atopic dermatitis clinical trial investigator sites and patient recruitment challenges in a crowded pipeline are raising per-patient trial costs and extending enrollment timelines.

The density of atopic dermatitis clinical programs now competing for enrollment simultaneously at major academic medical centers and dermatology practices is creating measurable site and patient competition effects. Experienced principal investigators manage multiple competing protocols. Patients who meet eligibility criteria for one trial frequently meet criteria for several others. Site selection and patient recruitment timelines have extended for programs launching in 2024 and 2025 relative to programs initiated five years earlier when the competitive environment was less congested. Per-patient costs have risen accordingly. Sponsors are responding by expanding site networks into less competitive geographies including Eastern Europe, Latin America, and Southeast Asia, which introduces operational complexity and regulatory coordination costs that partially offset the recruitment efficiency gained.

Opportunities: Label expansion into new age groups, disease severity segments, and combination therapy regimens offers substantial incremental commercial and clinical trial revenue potential for established biologic sponsors.

Pediatric extensions of FDA-approved biologics for treating atopic dermatitis constitute one of the biggest upcoming prospects in clinical trials for dermatological diseases. After the recent FDA approval of dupilumab for use in children aged just six months old in June 2024, there has been an intense effort toward developing pediatric indications for competing drugs and JAK inhibitors. There is already a considerable pool of patients with atopic dermatitis requiring treatment who have not been satisfactorily addressed using traditional treatments, leading to immense pressure for developing biologic alternatives. This pressure has culminated in a number of pediatric Phase II and Phase III clinical trials that are expected to yield significant additional income in the clinical trials market during the coming years.

Recent Developments

-

2025: Sanofi and Regeneron presented long-term five-year dupilumab safety and efficacy extension data in adults and adolescents with atopic dermatitis at the American Academy of Dermatology Annual Meeting, supporting commercial positioning against newer competing agents and providing the clinical foundation for formulary negotiation with major insurance payers.

-

2025: AbbVie initiated a new Phase III pediatric atopic dermatitis trial for upadacitinib in patients aged 2 to 11 years, advancing its strategy to secure a broader pediatric label that would extend the commercial lifecycle of its JAK inhibitor franchise into younger patient populations previously not addressed by its existing approved indications.

-

2024: Eli Lilly received FDA approval for lebrikizumab for adults with moderate to severe atopic dermatitis and simultaneously initiated Phase III enrollment for a pediatric development program, establishing a dual-track clinical and commercial strategy that mirrors the approved biologic pathway pioneered by dupilumab in the same indication.

-

2024: Leo Pharma initiated a Phase III study evaluating tralokinumab in combination with topical corticosteroids in patients with inadequate response to biologic monotherapy, addressing a clinically important patient population and generating combination therapy evidence that has direct implications for treatment guideline development and payer formulary positioning.

-

2023: Kyowa Kirin advanced rocatinlimab, its IL-31 receptor A antagonist targeting itch signaling directly, through Phase III enrollment with results anticipated to differentiate its mechanism from IL-4 and IL-13 targeting biologics and provide a novel clinical option for patients whose primary disease burden is pruritus rather than skin inflammation.

Atopic Dermatitis Clinical Trials Market Key Players are:

-

Sanofi S.A. and Regeneron Pharmaceuticals (dupilumab)

-

AbbVie Inc. (upadacitinib)

-

Eli Lilly and Company (lebrikizumab)

-

Leo Pharma (tralokinumab)

-

Pfizer Inc. (abrocitinib and cendakimab)

-

Novartis AG

-

AstraZeneca PLC

-

Kyowa Kirin Co. Ltd. (rocatinlimab)

-

Galderma SA

-

Incyte Corporation

-

Dermira Inc. (Eli Lilly)

-

Arena Pharmaceuticals (AstraZeneca)

-

Almirall SA

-

Boehringer Ingelheim

-

UCB SA

-

GlaxoSmithKline PLC

-

Arcutis Biotherapeutics

-

Novan Inc.

-

Keymed Biosciences (CM310)

-

ICON plc (CRO)

Frequently Asked Questions

North America dominated the Atopic Dermatitis Clinical Trials Market in 2023.

The “Large Molecules” segment dominated the Atopic Dermatitis Clinical Trials Market.

Advancements in Biologic and Molecular Therapies, Enhancing Research, are accelerating the market growth.

The Atopic Dermatitis Clinical Trials Market was USD 2.44 billion in 2023 and is expected to reach USD 6.39 billion by 2032.

The Atopic Dermatitis Clinical Trials Market is expected to grow at a CAGR of 11.21% from 2024-2032.

Get in Touch