Peptide Therapeutics Market Report Scope & Overview:

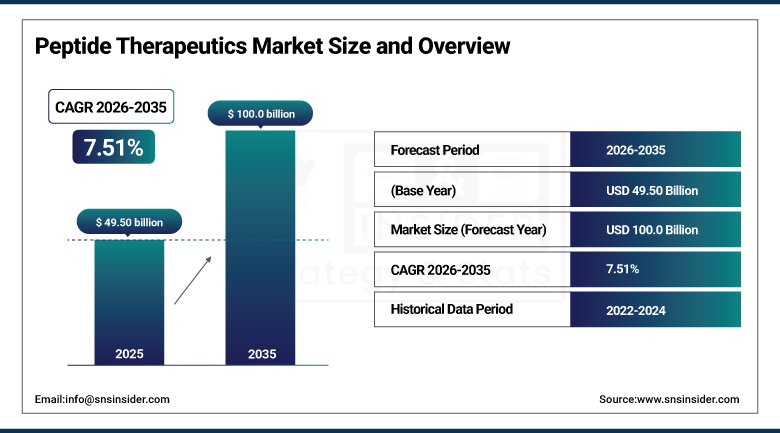

The Peptide Therapeutics Market was valued at USD 49.50 Billion in 2025 and is expected to reach USD 100.0 Billion by 2035, growing at a CAGR of 7.51% from 2026 to 2035.

Peptides occupy a strategically compelling position in modern pharmacotherapy, combining the target specificity of large molecule biologics with a manufacturing complexity and molecular footprint that sits closer to small molecule drugs. This dual advantage has made them the preferred drug modality for an expanding range of clinical indications where conventional small molecules lack adequate selectivity and full biologics carry excessive immunogenicity or manufacturing cost burden. The global peptide therapeutics market has matured from a niche endocrinology segment anchored by insulin and growth hormone into a broad and diversified therapeutic class spanning oncology, metabolic disorders, infectious diseases, cardiovascular conditions, and neurology. Sustained investment in peptide synthesis technology, notably solid phase peptide synthesis and recombinant DNA production platforms, has progressively reduced manufacturing costs while simultaneously enabling the production of more complex, longer chain peptides with enhanced pharmacological profiles. The explosive commercial success of GLP-1 receptor agonists in metabolic disease management has redefined the market's growth trajectory, demonstrating that peptide therapeutics can achieve blockbuster commercial outcomes at a scale that was previously reserved exclusively for monoclonal antibodies.

The remarkable commercial validation delivered by GLP-1 peptide therapies in obesity and type 2 diabetes management has triggered a fundamental reappraisal of the peptide drug class across the global pharmaceutical industry, with leading companies redirecting significant pipeline capital into novel peptide candidates across metabolic, oncological, and cardiovascular indications, while simultaneously investing in next generation oral peptide delivery technology that could unlock patient populations currently inaccessible to injectable peptide administration and expand the addressable market to an extraordinary degree.

Market Size and Forecast

- Market Size in 2025: USD 49.50 Billion

- Market Size by 2035: USD 100.0 Billion

- CAGR: 7.51% from 2026 to 2035

- Base Year: 2025

- Forecast Period: 2026 to 2035

- Historical Data: 2022 to 2024

To Get more information on Peptide Therapeutics Market - Request Free Sample Report

Peptide Therapeutics Market Trends

- Accelerating commercial momentum of GLP-1 receptor agonist peptide therapies in obesity, type 2 diabetes, and emerging cardiometabolic indications driving record revenues for market leaders and stimulating an unprecedented wave of pipeline investment into next generation peptide analogs and combination therapies.

- Rapid advancement of oral peptide delivery technology through permeation enhancers, protease inhibitor co formulations, nanoparticle encapsulation, and novel absorption promoter systems that are progressively overcoming the oral bioavailability limitation that has historically confined most therapeutic peptides to injectable administration.

- Growing adoption of solid phase peptide synthesis automation and continuous flow chemistry platforms enabling higher throughput, lower cost, and more reproducible manufacturing of complex peptide sequences at commercial scale.

- Expanding clinical pipeline of peptide based oncology therapies encompassing tumor targeting peptide drug conjugates, cancer vaccine peptide antigens, and peptide mediated radionuclide delivery systems that are redefining the role of peptides in precision cancer medicine.

- Rising interest in cell penetrating peptides and peptide carrier platforms as delivery vehicles for intracellular therapeutic cargo including nucleic acids, small molecules, and proteins across a broad range of disease areas.

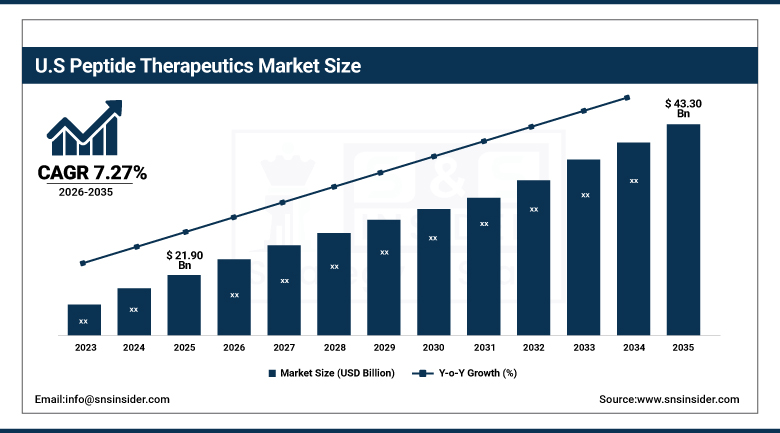

U.S. Peptide Therapeutics Market was valued at USD 21.90 Billion in 2025 and is expected to reach USD 43.30 Billion by 2035, registering a CAGR of 7.27% during 2026 to 2035.

The United States is the undisputed global leader in the peptide therapeutics market, representing well over 40% of worldwide market revenue and hosting the most dynamic research, regulatory, and commercial ecosystem for peptide drug development anywhere in the world. The FDA's established regulatory pathway for peptide therapeutics, encompassing both biological license applications for recombinant peptides and new drug applications for synthetic molecules, provides pharmaceutical developers with a clearly structured route to market approval. The U.S. market benefits from unparalleled private sector R&D investment, a world leading network of academic research institutions generating novel peptide candidates, strong venture capital infrastructure supporting peptide focused biotech startups, and the world's largest private health insurance market enabling premium pricing for innovative peptide therapies that deliver measurable clinical differentiation. The extraordinary commercial success of semaglutide and tirzepatide in the U.S. obesity and diabetes market has attracted every major pharmaceutical company into the GLP-1 and broader metabolic peptide space, generating a competitive intensity that is accelerating the entire field.

The U.S. market's leadership in peptide therapeutics is being further reinforced by the Inflation Reduction Act's impact on drug pricing negotiations, which is creating a strategic incentive for pharmaceutical companies to prioritize first in class peptide innovation over incremental small molecule reformulation, since novel molecular entities with meaningfully differentiated clinical profiles are better positioned to justify premium pricing under the evolving Medicare negotiation framework, driving capital toward genuinely transformative peptide drug development programs.

Peptide Therapeutics Market Segment Analysis

- Based on Type, Innovative peptide therapeutics accounted for the largest market share in 2025; Generic peptides are expected to be the fastest growing type segment through the forecast period.

- Based on Type of Manufacturers, In-house manufacturing accounted for the largest market share of 65.25% in 2025; Outsourced contract manufacturing expected to register the fastest growth through 2035.

- Based on Synthesis Technology, Recombinant DNA Technology accounted for the largest market share of 64.3% in 2025; Liquid Phase Peptide Synthesis expected to register the highest CAGR through the forecast period.

- Based on Route of Administration, Parenteral administration accounted for the largest market share in 2025; Novel delivery routes including transdermal, nasal, and buccal expected to grow fastest.

- Based on Application, Metabolic Disorders accounted for the largest market share in 2025 driven by GLP-1 therapies; Oncology expected to register the fastest growing application CAGR through 2035.

By Type, Innovative dominates, Generic peptides expected to grow fastest

Innovative peptide therapeutics held the dominant share of the market in 2025, reflecting the relatively recent approval timelines of many breakthrough peptide drugs and the substantial portion of the market still protected by active composition of matter and formulation patents. The commercial success of novel GLP-1 receptor agonists, peptide based cancer therapies, and next generation hormone analogs has generated blockbuster revenue streams for originator pharmaceutical companies that continue to invest heavily in lifecycle management strategies, novel indications, and next generation molecular designs to extend their clinical and commercial positions in high value therapeutic categories. The innovation pipeline for peptide therapeutics has never been richer, with several hundred peptide drug candidates in clinical development globally across a wide spectrum of disease areas.

Generic peptide therapeutics are projected to register the fastest CAGR through 2035 as a substantial wave of established peptide drug patents approaches expiration across major markets in the coming decade. Insulin analogs, growth hormone preparations, octreotide analogs, leuprolide acetate formulations, and numerous other commercially significant peptide drugs are either already facing generic competition or will do so within the forecast period, creating large revenue opportunities for manufacturers with validated SPPS and recombinant synthesis capabilities and established regulatory track records in peptide chemistry. India and South Korea are emerging as the leading geographies for generic peptide manufacturing investment.

By Synthesis Technology, Recombinant DNA Technology dominates, LPPS expected to grow fastest

Recombinant DNA technology held a commanding 64.3% market share across synthesis technology in 2025, reflecting its unique suitability for producing complex, longer chain therapeutic peptides and proteins including insulin analogs, growth hormone preparations, and GLP-1 receptor agonists at commercial scale with consistently high purity and biological activity profiles. Recombinant manufacturing platforms offer critical advantages in reproducing the precise molecular folding and post translational modification patterns that determine the pharmacological activity of many high value therapeutic peptides, capabilities that synthetic chemistry approaches cannot always match for larger and more structurally complex peptide molecules.

Liquid phase peptide synthesis is expected to register the highest CAGR during the forecast period, driven by ongoing improvements in reaction efficiency, solvent recovery systems, and continuous flow processing technology that are progressively closing the cost and throughput gap with solid phase methods for certain peptide length ranges and structural classes. LPPS retains inherent advantages in the synthesis of high-volume commodity peptide APIs where process economics are paramount, and its renewed competitiveness is attracting growing investment from contract development and manufacturing organizations seeking to diversify their peptide synthesis technology platforms.

By Route of Administration, Parenteral dominates, Novel delivery routes expected to grow fastest

The parenteral route of administration held the dominant position in 2025, accounting for the substantial majority of peptide therapeutics revenue globally. The injectable administration pathway remains the clinical standard for most therapeutic peptides because the oral bioavailability of unmodified peptides is typically less than 1 percent, owing to their susceptibility to proteolytic degradation in the gastrointestinal tract and poor permeability across intestinal epithelial membranes. Subcutaneous and intramuscular injection via prefilled syringe, autoinjector, and implantable pump platforms have become highly refined delivery systems that optimize patient convenience, dosing accuracy, and pharmacokinetic consistency for the majority of approved therapeutic peptides.

Novel and alternative delivery routes encompassing oral, transdermal, nasal, buccal, and pulmonary administration are expected to grow at the fastest rate from 2026 to 2035. Oral peptide delivery represents the holy grail of the field, with technology platforms from companies including Novo Nordisk, Chiasma, and Enteris BioPharma demonstrating meaningful progress in achieving therapeutically relevant oral bioavailability through permeation enhancers, enteric coating, and novel excipient approaches. The commercial success of oral semaglutide tablets in type 2 diabetes management has conclusively validated the oral peptide delivery concept and catalyzed substantial research investment into expanding this technology platform to additional peptde therapeutic candidates.

Regional Insights:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

44% |

|

Europe |

Germany |

27% |

|

Asia Pacific |

Japan |

38% |

|

Middle East & Africa |

Saudi Arabia |

26% |

|

Latin America |

Brazil |

48% |

North America Peptide Therapeutics Market Insights

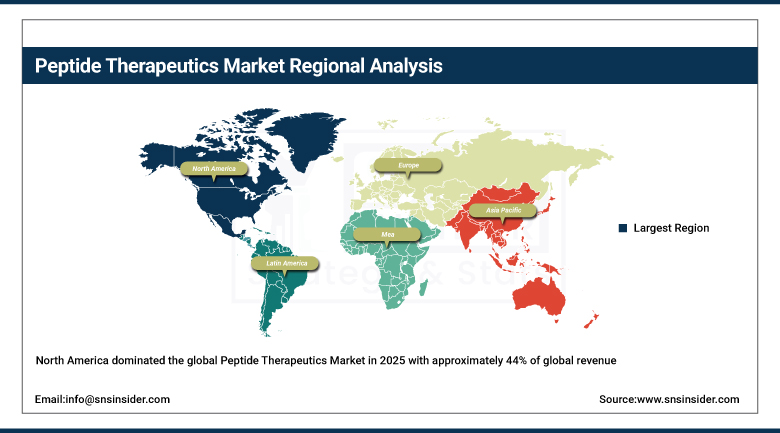

North America dominated the global Peptide Therapeutics Market in 2025 with approximately 44% of global revenue, led overwhelmingly by the United States. The U.S. market was valued at USD 21.90 Billion in 2025 and is projected to reach USD 43.30 Billion by 2035. The region's leadership is underpinned by the world's largest and most commercially dynamic branded pharmaceutical market, an exceptionally productive biopharma R&D ecosystem anchored in Boston, San Francisco, New York, and San Diego, strong FDA regulatory support for peptide drug approvals, and a health insurance landscape that enables premium pricing for clinically differentiated novel therapies. The extraordinary GLP-1 market expansion driven by obesity and type 2 diabetes treatment demand has disproportionately benefited North American revenue given the region's high disease prevalence and insurance coverage infrastructure for these indications.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Peptide Therapeutics Market Insights

Europe maintained a strong second place position in the global Peptide Therapeutics Market in 2025, with Germany, France, the United Kingdom, Switzerland, and Italy leading regional revenue generation. Europe's peptide therapeutics ecosystem benefits from world class academic research institutions, a robust contract research and manufacturing services sector centered in Germany, Switzerland, and Denmark, and a regulatory framework through the European Medicines Agency that provides a well structured pathway for innovative peptide drug approvals. European pharmaceutical companies including Novo Nordisk and Ipsen are globally significant players in the peptide therapeutics space, contributing substantial revenue from their insulin, GLP-1, and oncology peptide portfolios.

Asia Pacific Peptide Therapeutics Market Insights

Asia Pacific is expected to register the fastest regional CAGR during the forecast period of 2026 to 2035, driven by Japan, China, South Korea, and India. Japan leads the regional market with approximately 38% of Asia Pacific revenue, reflecting its well developed pharmaceutical infrastructure, high standards of clinical care, and significant domestic R&D investment in peptide drug development. China is the fastest growing national market in the region, propelled by a rapidly expanding biosimilar peptide manufacturing sector, growing domestic demand for metabolic disease therapies driven by rising obesity and diabetes prevalence, and increasing domestic innovation in peptide chemistry. India's cost competitive SPPS manufacturing capabilities are positioning it as a leading global source of generic peptide APIs and finished dosage forms as key product patents expire.

Middle East & Africa and Latin America Peptide Therapeutics Market Insights

The Middle East and Africa and Latin America represent growing markets for peptide therapeutics, primarily driven by the rising burden of chronic diseases including diabetes, obesity, and cancer across populations with improving healthcare system access and growing pharmaceutical market sophistication. Saudi Arabia leads the MEA region with approximately 26% of regional revenue, supported by Vision 2030 healthcare investment, high disease burden from type 2 diabetes and metabolic syndrome, and growing availability of insulin and GLP-1 therapies through both public and private healthcare channels. Brazil leads Latin America with approximately 48% of regional share, driven by its large insured population, growing oncology care infrastructure, and increasing access to biosimilar peptide therapies through the national health system and expanding private insurance coverage.

Market Dynamics:

Growth Drivers: Rising global burden of chronic diseases and expanding clinical validation of peptide based targeted therapy driving sustained pharmaceutical investment

The most fundamental driver of the Peptide Therapeutics Market is the global escalation in chronic disease burden across oncology, metabolic disorders, and cardiovascular disease, where peptide therapeutics are demonstrating compelling clinical advantages over alternative treatment modalities. The global prevalence of type 2 diabetes is projected to reach 783 million people by 2045, obesity rates continue to climb across virtually every national economy, and cancer incidence is rising in both absolute and age adjusted terms across developed and developing world populations. In each of these therapeutic areas, peptides offer a mechanism of action specificity and tolerability profile that positions them as a preferred treatment option for patients who do not achieve adequate outcomes with conventional small molecule therapies, and as precision medicine thinking becomes more deeply embedded in clinical practice guidelines, the role of highly targeted peptide therapeutics in first line and combination treatment regimens is expanding steadily.

The intellectual property landscape of the peptide therapeutics industry is entering a period of extraordinary richness, with several hundred novel peptide drug candidates in clinical development globally spanning phase one discovery stage assets through phase three pivotal programs, creating a regulatory approval pipeline whose commercial output through 2035 will materially expand the market's revenue base and introduce new therapeutic areas where peptides have not previously been established as standard of care treatments.

Restraints: Limited oral bioavailability, manufacturing complexity, and peptide stability challenges constraining broader therapeutic access

The most persistent technical constraint in the Peptide Therapeutics Market is the inherently poor oral bioavailability of most therapeutic peptides, arising from rapid enzymatic degradation by gastrointestinal proteases, minimal intestinal permeability for large hydrophilic molecules, and first pass hepatic metabolism that dramatically reduces systemic exposure. This limitation confines the majority of approved peptide therapeutics to parenteral administration routes that impose needle burden on patients, require trained administration techniques, and create adherence challenges in chronic disease management settings where long term daily or weekly self injection is required. Manufacturing complexity represents an additional constraint, as peptide synthesis at commercial scale demands highly specialized chemistry expertise, sophisticated chromatographic purification infrastructure, and rigorous quality control systems that translate into capital intensive manufacturing facilities and high cost of goods that can limit accessibility in lower income markets and price sensitive healthcare environments.

Opportunities: Oral peptide delivery breakthroughs, peptide drug conjugates, AI driven discovery, and biosimilar market expansion

The successful commercialization of oral semaglutide has opened a genuinely transformative opportunity frontier for the broader peptide therapeutics industry, demonstrating that meaningful oral bioavailability for therapeutic peptides can be achieved through carefully engineered delivery system design. This proof of concept is catalyzing intensive research investment into oral delivery platforms for additional high value peptide candidates across oncology, cardiovascular, and immunological indications, with the potential to unlock patient populations who decline injectable therapy and dramatically expand treatment penetration in chronic disease management. Peptide drug conjugates, which link potent cytotoxic payloads to tumor targeting peptide homing sequences for precision oncology applications, represent a rapidly advancing technology platform that combines the target selectivity of peptide chemistry with highly concentrated therapeutic action at the disease site. Meanwhile, the expanding biosimilar peptide market offers substantial revenue opportunities for manufacturers with the technical and regulatory capabilities to supply high quality generic peptide APIs and formulations to price sensitive healthcare markets at competitive cost structures.

Recent Developments:

- 2026: Novo Nordisk launched phase III clinical trials for a next generation oral GLP-1 and GIP dual agonist peptide drug which would promise greater glycemic control and weight loss than currently available GLP-1 and GIP agonist peptides available via both oral and injectable formulations, offering a convenient dosage method that would help greatly increase adoption rates amongst those disinclined to use injectable therapies.

- 2025 (March): Eli Lilly extended the use of its tirzepatide clinical trial program beyond metabolic conditions to include heart failure and non-alcoholic steatohepatitis, leveraging the current capabilities of its leading GLP-1 and GIP dual agonist peptide therapy, thereby increasing its commercially addressable market size.

- 2024 (November): AstraZeneca made an important co-development pact with a major biotechnology company focusing on peptide drug conjugates for a portfolio of targeted tumor cytotoxic conjugates for oncology involving solid tumors, bringing together the former's strength in clinical development and commercialization with the latter's innovative peptide conjugate linker/payload technologies.

- 2024 (July): Pfizer released encouraging phase two results on its GLP-1 receptor agonist peptide therapy for obesity, showing considerable weight reduction in obese subjects while overcoming previous problems with gastrointestinal tolerance with earlier oral formulations of peptides as seen by Pfizer's novel absorption enhancement technology.

- 2025 (February): Sun Pharmaceutical Industries increased its capacity for peptide production through commissioning a specialized SPPS peptide API production facility in India, allowing it to provide both local and export markets with a wide array of peptide APIs upon patent expirations for various therapeutic peptides.

Peptide Therapeutics Market Key Players:

-

Novo Nordisk A/S

- Eli Lilly and Company

- Pfizer Inc.

- Sanofi S.A.

- AstraZeneca plc

- Amgen Inc.

- Novartis AG

- Takeda Pharmaceutical Company Limited

- F. Hoffmann La Roche Ltd.

- Ipsen S.A.

- AbbVie Inc.

- Merck & Co. Inc.

- Teva Pharmaceutical Industries Ltd.

- Sun Pharmaceutical Industries Ltd.

- Dr. Reddy's Laboratories Ltd.

- Bachem Holding AG

- PolyPeptide Group AG

- Lonza Group AG

- Fresenius Kabi AG

- Biocon Limited

Peptide Therapeutics Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 49.50 Billion |

| Market Size by 2035 | USD 100.0 Billion |

| CAGR | CAGR of 7.51% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Generic, Innovative) • By Type of Manufacturers (In-house, Outsourced) • By Synthesis Technology (Solid Phase Peptide Synthesis, Liquid Phase Peptide Synthesis, Recombinant DNA Technology) • By Route of Administration (Parenteral, Oral, Pulmonary, Mucosal, Others) • By Application (Oncology, Metabolic Disorders, Cardiovascular, Infectious Diseases, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Novo Nordisk A/S, Eli Lilly and Company, Pfizer Inc., Sanofi S.A., AstraZeneca plc, Amgen Inc., Novartis AG, Takeda Pharmaceutical Company Limited, F. Hoffmann La Roche Ltd., Ipsen S.A., AbbVie Inc., Merck & Co. Inc., Teva Pharmaceutical Industries Ltd., Sun Pharmaceutical Industries Ltd., Dr. Reddy's Laboratories Ltd., Bachem Holding AG, PolyPeptide Group AG, Lonza Group AG, Fresenius Kabi AG, Biocon Limited |

Frequently Asked Questions

Ans: The Peptide Therapeutics Market is expected to grow at a CAGR of 7.51% from 2026 to 2035.

Ans: The Peptide Therapeutics Market was valued at USD 49.50 billion in 2025.

Ans: The rising global burden of chronic diseases particularly metabolic disorders, oncology, and cardiovascular conditions combined with the clinical validation of peptide based targeted therapies, rapid advances in synthesis technology, and the extraordinary commercial momentum of GLP-1 receptor agonist peptide therapies are the primary structural drivers of sustained market growth through 2035.

Ans: The Recombinant DNA Technology segment dominated the Peptide Therapeutics Market in 2025 with approximately 64.3% of global synthesis technology revenue, reflecting its superior suitability for producing complex long chain therapeutic peptides with consistently high purity and biological activity at commercial scale.

Ans: North America dominated the Peptide Therapeutics Market in 2025 with approximately 44% of global market revenue, led by the United States whose combination of world class pharmaceutical R&D infrastructure, FDA regulatory leadership, strong insurance reimbursement frameworks, and extraordinary commercial demand for GLP-1 metabolic peptide therapies positions it as the most valuable single national market in the global peptide therapeutics industry.

Get in Touch