Airway Disease Treatment Market Report Scope & Overview:

Get More Information on Airway Disease Treatment Market - Request Sample Report

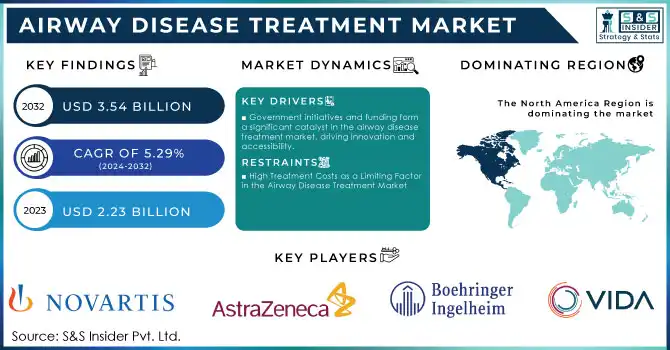

Airway Disease Treatment Market was valued at USD 2.23 billion in 2023 and is expected to reach USD 3.54 billion by 2032, growing at a CAGR of 5.29% from 2024-2032.

The airway disease treatment market is experiencing fast growth due to the increasing prevalence of respiratory diseases worldwide, such as asthma, COPD, and bronchitis. For Instance, in the United States alone, over 150,000 Americans died yearly of chronic obstructive pulmonary disease, a death occurring every four minutes, and 75% of these were due to smoking tobacco. 25% of all patients diagnosed with COPD have never smoked, while other factors such as air pollution and an aging population are taking their toll. It is for these environmental and lifestyle pressures that the demand for effective treatment is increasing. Pharma scientific advancements in terms of biologics and targeted therapies are addressing this need by offering more effective and side-effect-reducing solutions.

Looking forward, the airway disease treatment market presents significant opportunities for growth, driven by rising pollution levels and the increasing prevalence of respiratory diseases. This rising number of cases intensifies the demand for efficient and affordable treatments, and pharmaceutical companies are shifting their focus to more cost-effective therapies. The incorporation of AI and machine learning into drug discovery is crucial for companies meeting the demand and accelerating the creation of new treatments. It is not only speeding up the process of developing drugs but also increasing the accuracy and accessibility of care for the respiratory condition. Therefore, the airway disease treatment market is becoming an increasingly inclusive space, creating growth for the sake of a broader population by ensuring that patients worldwide gain access to the best therapy.

The focus on personalized medicine shapes treatment strategies, increasingly making treatment tailored to specific patients based on genetic testing and disease biomarkers. The advancement in diagnostic tools supports this kind of tailoring of more precise and targeted therapies, even as disease management through digital health technologies, telemedicine, wearable devices, and AI-driven diagnostics evolves in parallel. These innovations enable healthcare professionals to monitor a patient in real-time; treatments can then be adjusted accordingly to optimize outcomes. By encouraging a more data-driven, patient-centric approach, these technologies drive improvements in patient engagement and disease control. Therefore, integrating these digital solutions into contemporary practice will shape the future of airway disease treatment market.

Airway Disease Treatment Market Dynamics

DRIVERS

-

The Growing Influence of the Aging Population on the Airway Disease Treatment Market

The increasing aging population worldwide brings the senior population into ever greater contact with chronic respiratory diseases like COPD and asthma. These trends are expanding the patient base by further instigating demand for more specialized treatments. For instance, diseases like COPD, which affect older individuals more often, are compelling the scientific community to develop more advanced therapies, specifically biologics, and personalized medicine, which are currently driving key trends in the sector. Advances in diagnostic tools and methods of delivery of treatments continue to further enhance the management of airway diseases, with greater precision in therapy now possible. This coincides with an increasing demand for innovative treatments with an aging population, and this creates a significant growth opportunity for pharmaceutical companies specializing in respiratory care as well as customized treatments for this age group.

-

Government initiatives and funding form a significant catalyst in the airway disease treatment market, driving innovation and accessibility.

Public health agencies have strongly supported policy incentives for managing respiratory diseases, leading to increased research investments and advancements in therapies and preventive measures. Global trends in the healthcare industry move toward cost control and better outcomes, where governments are going to give incentives for early diagnosis and proper treatment of diseases related to the airways. This support from regulatory bodies is also broadening access to health care in underdeveloped areas and opens new demand and competition. In this regard, government support not only fuels the market growth but also creates a more vibrant and competitive environment, replete with opportunities for companies investing in innovative airway disease solutions.

RESTRAINTS

-

High Treatment Costs as a Limiting Factor in the Airway Disease Treatment Market

The high cost of treatment is a significant restraint in the airway disease treatment market, as advanced therapies such as biologics and specialized inhalation devices can be cost-prohibitive. This monetary burden restricts access, particularly for patients residing in low-income regions or those who do not have comprehensive insurance coverage. High drug development and production costs, among other economic factors, are significant cost increase sources. As mentioned above, complex regulatory requirements add further expenses that are passed on to consumers. High costs not only reduce the treatment adoption rate but also create inequalities in healthcare access when fewer patients can get to enjoy innovative solutions. Therefore, this might restrain the overall growth of the market as affordability takes on a more prominent role in increasing the scope and effectiveness of treatments for airway diseases.

Airway Disease Treatment Market Segment Analysis

BY TYPE

Asthma Segment dominated the Airway Disease Treatment Market with the highest revenue share of about 54% in 2023 because the disease is prevalent and the treatments are well established. With millions of asthma patients worldwide, there is an ongoing strong demand for preventive and rescue medications- inhaled and biologics. Market leadership will continue, as companies will strive towards improvement in asthma care and patient outcomes.

Chronic Obstructive Pulmonary Disorder Segment is expected to grow at the fastest CAGR of about 6.16% from 2024-2032. The sizeable aging population, along with increased smoking-related diseases, has contributed to this growth. Long-acting bronchodilators and biologics are among the treatments that improve options and lead to further growth in the market. As a result, investment and innovation in COPD therapies may accelerate in manners that alter the competitive dynamics of airway disease treatment.

BY END USE

Hospitals Segment dominated the Airway Disease Treatment Market with the highest revenue share of about 43% in 2023, due to their comprehensive care capabilities and advanced treatment infrastructure. Hospitals are equipped with specialized facilities, such as respiratory therapy units and intensive care, which are essential for managing severe airway diseases. This supremacy is likely to persist, as critical care and complicated treatments are going to remain the preserve of hospitals, with considerable investment in respiratory disease management technologies and services.

Clinics Segment is expected to grow at the fastest CAGR of about 7.03% from 2024-2032 due to the growing demand for outpatient care and specialty clinics dedicated to respiratory diseases. With increasing accessibility and decreasing cost of healthcare, it is aimed to be provided at clinics that will provide personalized treatment with speed service. This shift of healthcare towards outpatient care would demand more investment in clinic-based facilities and available specialized care options leading to a drastic change in the treatment landscape for airway diseases.

BY TREATMENT

Bronchodilators Segment dominated the Airway Disease Treatment Market with the highest revenue share of about 43% in 2023, as these products are commonly used by most patients in managing chronic asthma and other conditions, including COPD. Bronchodilators are critical for the relief of symptoms and improvement in lung function because they are a go-to treatment for many patients. This dominance is expected to continue, as pharmaceutical companies heavily invest in developing more potent and personalized bronchodilator therapies, promoting market growth and competition.

The oxygen Therapy Segment is expected to grow at the fastest CAGR of about 8.33% from 2024-2032, primarily because of increasing the prevalence of chronic respiratory diseases and the aging population. With worsening conditions such as COPD, increasingly, patients have to require supplemental oxygen in daily management, so the demand for oxygen therapy is steadily mounting. This will probably translate to intensified competition and innovation in the oxygen therapy market because companies will look toward offering more portable, efficient, and cost-effective solutions that can reshape patient care and market dynamics.

Airway Disease Treatment Market Regional Outlook

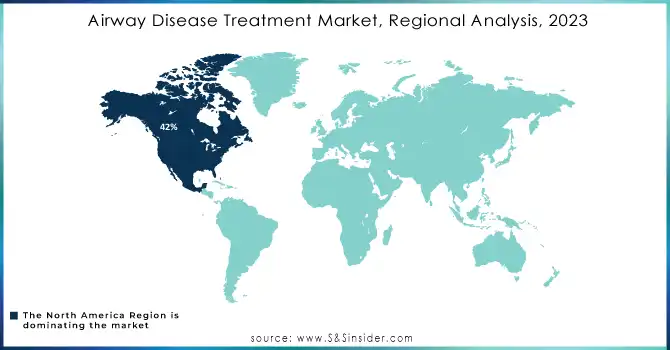

North America dominated the Airway Disease Treatment Market with the highest revenue share of about 42% in 2023, due to a comingling of high healthcare expenditure, well-developed medical infrastructure, and prevalent access to treatments. Strong emphasis on research and development, plus the high prevalence of asthma and COPD, contributes to this demand for innovative therapies and devices in the region. This trend is likely to continue going forward because North American companies will dominate the product development market, which would trigger a large amount of investment globally.

Asia Pacific is expected to grow at the fastest CAGR of about 7.40% from 2024-2032 Driven by Increased Healthcare Access, a Growing Middle Class, and a Higher Prevalence of Respiratory Diseases. As the region's aging population expands and more people shift to urban areas, the demand for airway disease treatments is growing fast. Such rapid growth will likely attract huge amounts of investment, stimulate local market innovation, and shift competition towards cheaper, region-specific treatment solutions, which would altogether reshape the global landscape of the airway disease treatment market.

Need Any Customization Research On Airway Disease Treatment Market - Inquiry Now

LATEST NEWS -

-

In 2024, Boehringer Ingelheim launched a treatment in Qatar for managing three types of interstitial lung diseases, including progressive fibrosing interstitial lung disease (PF-ILD).

-

In 2024, AstraZeneca unveiled new research at ATS 2024, showcasing advancements in treatments for respiratory and immune-mediated diseases, including COPD and asthma.

KEY PLAYERS

-

Holaira, Inc. (Aeris, Holaira’s Bronchial Thermoplasty System)

-

VIDA Diagnostics (VIDA Insight, VIDA Lung AI)

-

Boehringer Ingelheim International GmbH (Spiriva, Striverdi)

-

AstraZeneca (Symbicort, Fasenra)

-

Teva Pharmaceuticals (ProAir HFA, Qvar RediHaler)

-

GlaxoSmithKline (Advair, Breo Ellipta)

-

Novartis (Xolair, Ultibro Breezhaler)

-

Sun Pharmaceutical Industries Ltd. (Breztri Aerosphere, Pulmicort)

-

Pfizer Inc. (Breztri Aerosphere, Xolair)

-

Zydus Group (Duolin, Asthalin)

-

Merck & Co., Inc. (Singulair, Dulera)

-

AbbVie Inc. (Rinvoq, Humira)

-

Bristol-Myers Squibb (Orencia, Breztri Aerosphere)

-

Mylan (Symbicort, EpiPen)

-

Eli Lilly and Company (Emgality, Trulicity)

-

Roche (Xolair, Pulmozyme)

-

Amgen (Tezspire, Kineret)

-

Baxter International Inc. (Bethkis, Altabax)

-

Sandoz (Novartis) (AirFluSal Forspiro, Symbicort)

-

Cipla (Seroflo, Foracort)

-

F. Hoffmann-La Roche Ltd. (Pulmozyme, Xolair)

-

Medtronic (Breathe, CoreValve)

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 2.23 Billion |

| Market Size by 2032 | USD 3.54 Billion |

| CAGR | CAGR of 5.29% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Asthma, Chronic Obstructive Pulmonary Disorder, Bronchiectasis) • By Treatment (Bronchodilators, Corticosteroids, Cytotoxic Drugs, Oxygen Therapy, Antibiotics, Others) • By End Use (Hospitals, Clinics, ASCs, Rehabilitation Centres, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Holaira, Inc., VIDA Diagnostics, Boehringer Ingelheim International GmbH, AstraZeneca, Teva Pharmaceuticals, GlaxoSmithKline, Novartis, Sun Pharmaceutical Industries Ltd., Pfizer Inc., Zydus Group, Merck & Co., Inc., AbbVie Inc., Bristol-Myers Squibb, Mylan, Eli Lilly and Company, Roche, Amgen, Baxter International Inc., Sandoz (Novartis), Cipla, F. Hoffmann-La Roche Ltd., Medtronic. |

| Key Drivers | • The Growing Influence of the Aging Population on the Airway Disease Treatment Market • The Role of Government Initiatives and Funding in Shaping the Airway Disease Treatment Market |

| Restraints | • High Treatment Costs as a Limiting Factor in the Airway Disease Treatment Market |

Frequently Asked Questions

Oxygen therapy is expected to grow at the fastest CAGR of 8.33% due to rising chronic respiratory diseases and the aging population.

North America dominates with the highest revenue share due to high healthcare expenditure and the prevalence of asthma and COPD.

The Asia Pacific region is expected to grow at the fastest CAGR of 7.40% due to increased healthcare access and a growing middle class.

The COPD segment is expected to grow at the fastest CAGR of 6.16% from 2024 to 2032.

Airway Disease Treatment Market was valued at USD 2.23 billion in 2023 and is expected to reach USD 3.54 billion by 2032, growing at a CAGR of 5.29% from 2024-2032.

Get in Touch