Personal and Entry Level Storage Market Report Scope & Overview:

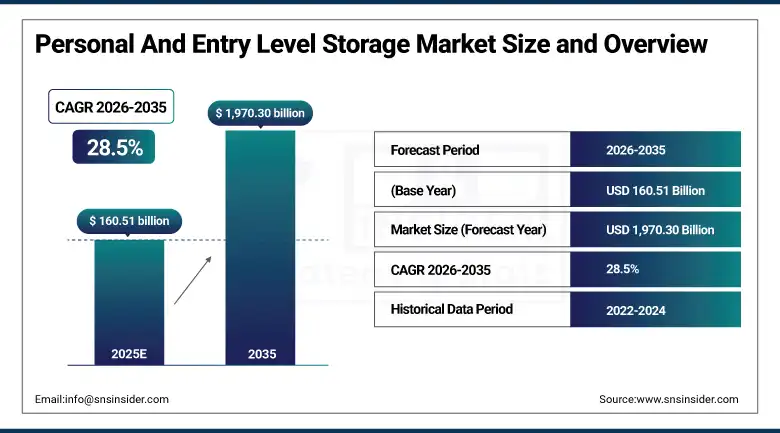

Personal and Entry Level Storage Market was valued at USD 160.51 billion in 2025 and is expected to reach USD 1,970.30 billion by 2035, growing at a CAGR of 28.5% from 2026-2035.

The rapid industrial and personal digital data generation by individuals, small and medium-sized enterprises, and intelligent connected devices is supporting the extraordinary growth of the personal and entry-level storage market. Demand is fueled by increased use of cloud storage, Network-Attached Storage (NAS), and removable storage products driven by the remote working revolution, digital media production explosion, and edge computing adoption. The global data generation is accelerating exponentially — driven by 4K/8K video content creation, gaming, AI model training datasets, IoT sensor data, and digital work file proliferation — creating sustained, growing demand for affordable, scalable, and high-performance personal storage solutions. Notable innovations such as Microsoft's 365 Backup and NetApp's BlueXP hybrid cloud management platform highlight the market's dynamic evolution.

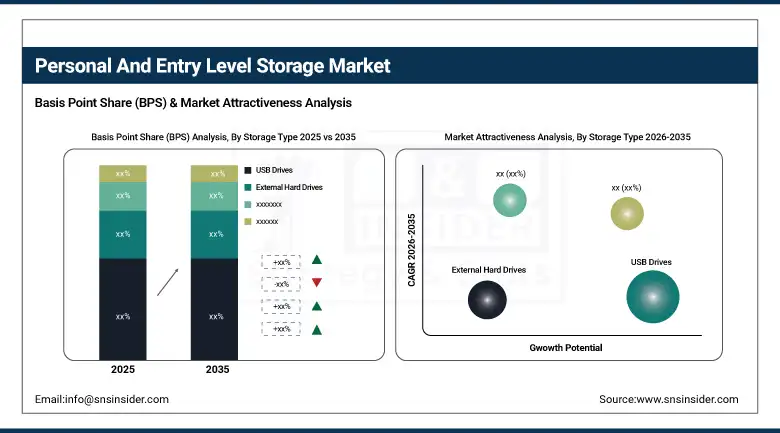

According to industrial statistics, the USB Drives were expected to capture about 47.49% of the market share in the personal and entry-level storage segment, because of their wide applicability and easy plug-and-play technology – whereas the Solid State Drives will show the highest CAGR at about 29.83% on account of performance enhancement, cost reduction, reliability, and usage in high-performance applications like laptops and video editing.

Market Size and Forecast

• Market Size in 2025: USD 160.51 Billion

• Market Size by 2035: USD 1,970.30 Billion

• CAGR: 28.5% from 2026 to 2035

• Base Year: 2025

• Forecast Period: 2026-2035

• Historical Data: 2022-2024

To Get more information On E-Learning Compliance Corporate Training Market - Request Free Sample Report

Personal and Entry Level Storage Market Trends

• Rapid decline in SSD prices driven by 200+ layer NAND flash stacking and QLC architecture advancements making high-performance solid-state storage accessible to mainstream personal and entry-level user segments.

• Growing adoption of multi-bay NAS devices by remote workers, content creators, and small businesses combining on-premise storage speed with cloud synchronization for comprehensive hybrid data management.

• Increasing deployment of AI-powered personal storage platforms providing intelligent auto-categorization, duplicate detection, facial recognition photo organization, and predictive storage management features.

• Rising demand for high-speed Thunderbolt 5 and USB4-compatible external storage solutions delivering workstation-class throughput for professional video editing, 3D rendering, and large dataset management on personal devices.

• Integrating growing smart home systems turning NAS drives to serve as central hubs controlling digital lives from home security camera feeds, smart devices’ activities, multimedia collections, and automated family data backups.

• Growing adoption by enterprises and professional consumers of software-defined storage technology for efficient and flexible data management on diverse personal and basic level storage platforms.

• Growing need for durable portable SSD with military standards of resistance to drops and water, along with built-in hardware encryption.

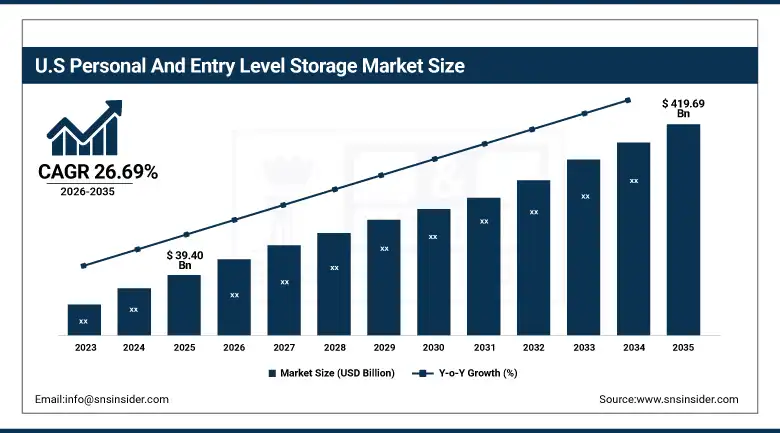

U.S. Personal and Entry Level Storage Market was valued at USD 39.40 billion in 2025 and is expected to reach USD 419.69 billion by 2035, registering a CAGR of 26.69% during 2026-2035.

Domination of the market is achieved by the United States due to the increase in the creation of digital content, increased utilization of smart devices, and the use of cloud and network storage. Growth of the industry is supported by the digital workflow associated with working remotely, the content creator industry, gaming culture that requires fast storage systems, and consumer adoption of technology. The big tech firms include Microsoft, Apple, and Google while the hardware providers include Western Digital, Seagate, and Samsung who are increasing personal storage solutions for consumers.

The recognition of NetApp as the 2024 Company of the Year for hybrid cloud storage management by Frost & Sullivan — alongside Microsoft's launch of Microsoft 365 Backup providing enhanced data protection and recovery — underscores the market's accelerating shift toward intelligent, hybrid storage architectures that bridge personal and cloud storage for comprehensive data management through 2035.

Personal and Entry Level Storage Market Segment Insights

-

Based on Storage Type, USB Drives accounted for the largest market share in 2025; SSDs expected to be the fastest-growing segment.

-

Based on Connectivity, USB segment dominates the market share, Cloud segment is anticipated to have the fastest CAGR

-

Based on End-User, Individual Consumers accounted for the largest market share in 2025; BFSI held share with strong institutional storage demand.

Personal and Entry Level Storage Market Segment Analysis

By Storage Type, USB Drives dominate, SSDs expected to grow fastest

USB Drives emerged as the leading choice in the personal and basic category due to their approximately 47.49% market share in 2025. The universal applicability to almost all types of computing systems, easy connectivity, vast storage ranging from 8GB to 2TB, and very affordable prices from commodity USB sticks to the high-performing metal-bodied USB 3.2 drive ensure that the segment remains the volume leader. USB drives continue to play an indispensable role in moving files, software transfer, and booting of operating systems.

SSDs are expected to grow at the fastest CAGR of approximately 29.83% during 2026-2035, driven by continuously declining prices as 200+ layer NAND stacking and QLC architectures scale, combined with the performance advantages of SSDs over HDDs — including silent operation, shock resistance, faster data transfer speeds exceeding 2,000 MB/s, and superior reliability — making them increasingly preferred for laptops, gaming, and professional video editing workflows where speed and durability are paramount.

By Connectivity, USB segment dominates, Cloud expected to grow rapidly

The market for USB connectivity was the main product category in the Personal and Entry Level Storage Market for the year 2025 owing to its high level of universality, low cost, ease of use, and speed of data transfers. The USB-powered external hard drive, SSDs, and flash drive continue being the storage products of choice for individuals and small businesses because of portability and ease of use. Advances in USB standards such as USB 3.2 and USB-C keep raising the bar.

Cloud connectivity is expected to witness the fastest growth during 2026–2035 owing to rising adoption of personal cloud storage, remote working models, and growing demand for seamless multi-device data access. Increasing integration of AI-driven backup solutions, subscription-based storage platforms, and hybrid cloud ecosystems is accelerating cloud-based storage adoption globally.

By End-User, Individual Consumers lead, SMEs and BFSI growing rapidly

Consumers are set to dominate in the personal and entry-level storage space in 2025 owing to the huge growth in personal digital content generation such as high definition photos and videos, gaming, music collections, and remote working files. The rise in phone photo quality together with the increase in high-quality content production has spurred the need for personal storage due to limited internal storage capacity of devices.

Market share in 2025 for BFSI industry stood at around 17.55% as this industry requires an encryption and compliance based personal as well as entry level storage for storing critical information, customer files, and audit trails. The healthcare sector constitutes another major consumer category that requires HIPPA compliance to store patient data, imaging databases, and clinical documents. Small and medium sized enterprises form a key emerging end user group owing to affordable NAS devices offering professional file sharing capabilities.

Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

38% |

|

Europe |

Germany |

29% |

|

Asia Pacific |

China |

43% |

|

Middle East & Africa |

UAE |

29% |

|

Latin America |

Brazil |

43% |

North America Personal and Entry Level Storage Market Insights

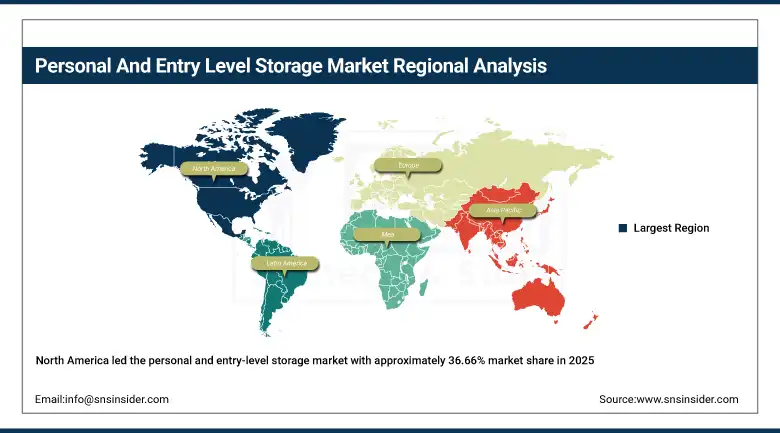

North America led the personal and entry-level storage market with approximately 36.66% market share in 2025, supported by strong consumer demand, cutting-edge digital infrastructure, high content creation activity, and the presence of global technology leaders including Western Digital, Seagate, and Synology. The U.S. continues to dominate, driven by cloud adoption integration with personal storage devices, a booming gaming and content creator economy, and strong enterprise SMB NAS adoption.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Personal and Entry Level Storage Market Insights

Asia Pacific is projected to grow at the fastest CAGR of 30.03% during 2026-2035, with China, India, and South Korea spearheading growth. Rapidly growing smartphone penetration creating digital content management needs, expanding e-commerce and digital economy participation, rising consumer electronics spending, and government digitalization initiatives are combining to create extraordinarily strong storage demand across the region. China's massive consumer electronics market and India's rapidly growing tech-savvy middle class represent the most significant growth opportunities.

Europe Personal and Entry Level Storage Market Insights

Europe plays a significant role in the Personal Storage & Entry Level Storage segments because the need for secure personal storage due to data security measures as per GDPR regulations, along with the presence of strong prosumers and creative professionals, is very prominent. Synology and QNAP have particularly strong European market positions in the NAS segment.

Middle East & Africa and Latin America Personal and Entry Level Storage Market Insights

The Middle East personal and entry-level storage market is growing, driven by increasing digital content creation, improving broadband infrastructure, and growing adoption of personal cloud and NAS storage in UAE and Saudi Arabia. Latin America, led by Brazil, is experiencing rising storage demand driven by expanding smartphone penetration, growing digital content consumption, and increasing remote work adoption requiring personal backup and file management solutions.

Market Growth Drivers:

Exponential growth in digital content creation and hybrid storage adoption accelerating market expansion: The Personal and Entry Level Storage Market is experiencing strong growth due to the rapid increase in personal digital data generated from 4K/8K video creation, gaming, remote work, social media content, and connected IoT devices. Increased use of external SSD, NAS, USB, and personal cloud storage solutions has fueled the demand for inexpensive yet large-capacity storage devices among end-users and SMEs. Ongoing decreases in hardware pricing and developments in the field of USB4, Thunderbolt 5, and cloud syncing are set to drive growth. Moreover, the rise of the creator economy and the increased deployment of AI-enabled backup and data management services along with cloud/local hybrid storage solutions have redefined personal storage by making it intelligent and scalable, fueling long-term market growth through 2035.

Market Restraints:

Rising cybersecurity risks and cloud privacy concerns limiting consumer confidence in connected storage ecosystems: Issues such as ransomware attacks, data breach, cloud storage vulnerabilities, and personal privacy concerns are hindering the acceptance of cloud and connected storage technologies by the consumers and small-medium enterprises. Consumers and SMEs are still hesitant about storing their personal financial, sensitive, or business information on internet-based storage devices because of the growing concerns of cyber attacks, as well as regulatory uncertainties about data ownership and protection. Moreover, problems related to software compatibility with different operating systems, expensive recovery costs from hardware damages, as well as fast obsolescence of the devices are additional barriers facing users. Competition through pricing among competitors is another issue impacting the market participants' revenues.

Market Opportunities:

Rising demand for AI-powered personal cloud storage and edge data management creating new growth opportunities: Due to the proliferation of artificial intelligence-powered storage management, edge computing, and hybrid cloud environments, many opportunities for development in the Personal and Entry-Level Storage market are expected. Customers increasingly require smart storage solutions that offer backup capability, efficient file management, synchronization in real-time, and safe remote access via a number of devices. Besides, the fast growth of content creators, gamers, telecommuters, and professionals working in the field of digital media has led to increased interest in fast SSDs, network attached storage solutions, and personal clouds. Finally, innovative trends such as AI cybersecurity technology, energy-efficient storage architecture, and decentralized data management platforms may become important sources of additional revenues for many years to come.

Recent Developments:

-

2026: Western Digital Corporation introduced next-generation portable SSDs with enhanced AI-assisted backup capabilities and higher transfer speeds targeting content creators and hybrid workforce users.

-

2026: Seagate Technology launched upgraded personal cloud and NAS storage solutions featuring improved cybersecurity, remote access functionality, and scalable backup management for SMEs and home users.

-

2026: Synology Inc. expanded its entry-level NAS portfolio with energy-efficient storage systems optimized for personal cloud applications, multimedia streaming, and remote collaboration environments.

Personal and Entry Level Storage Market Key Players

• Western Digital Corporation

• Seagate Technology Holdings plc

• Samsung Electronics Co., Ltd.

• SanDisk Corporation

• Toshiba Corporation

• Kingston Technology Corporation

• Synology Inc.

• QNAP Systems, Inc.

• NetApp, Inc.

• LaCie

• G-Technology

• Buffalo Technology

• Drobo

• Transcend Information, Inc.

• Silicon Power Computer & Communications Inc.

• iOmega

• Apricorn

• Verbatim

• Lexar

• PNY Technologies

Personal and Entry Level Storage Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 160.51 Billion |

| Market Size by 2035 | USD 1,970.30 Billion |

| CAGR | CAGR of 28.5% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Storage Type (External Hard Drives, SSDs, USB Drives, Network-Attached Storage (NAS), Personal Cloud Storage, Others) • By Connectivity (USB, Ethernet/Wi-Fi, Cloud) • By End-User (Individual Consumers, SMEs, BFSI, Healthcare, IT & Telecom, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Western Digital Corporation, Seagate Technology Holdings plc, Samsung Electronics Co., Ltd., SanDisk Corporation, Toshiba Corporation, Kingston Technology Corporation, Synology Inc., QNAP Systems, Inc., NetApp, Inc., LaCie, G-Technology, Buffalo Technology, Drobo, Transcend Information, Inc., Silicon Power Computer & Communications Inc., iOmega, Apricorn, Verbatim, Lexar, PNY Technologies |

Frequently Asked Questions

Ans: North America dominated the Personal and Entry Level Storage Market in 2025, driven by strong consumer digital content creation demand, cloud-hybrid storage adoption, high gaming and content creator market activity, and the presence of global storage technology leaders including Western Digital and Seagate.

Ans: The SSDs segment is expected to grow at the fastest CAGR of approximately 29.83% during 2026-2035, driven by continuously declining NAND flash prices, superior performance advantages over HDDs, shock resistance, and increasing adoption in laptops, gaming systems, and professional video editing workflows.

Ans: The USB Drives segment dominated the Personal and Entry Level Storage Market in 2025, owing to their ubiquitous compatibility across virtually all computing devices, plug-and-play convenience, educational, and corporate user segments.

Ans: Exponential growth in personal digital data generation from 4K/8K content creation, gaming, remote work digital workflows, and IoT device proliferation — combined with rapidly declining SSD and NAS costs making high-performance storage increasingly accessible — is the primary driver of the market's extraordinary growth through 2035.

Ans: The Personal and Entry Level Storage Market was valued at USD 160.51 billion in 2025.

Ans: The Personal and Entry Level Storage Market is expected to grow at a CAGR of 28.5% from 2026 to 2035.

Get in Touch