Enterprise Generative AI Market Report Scope & Overview:

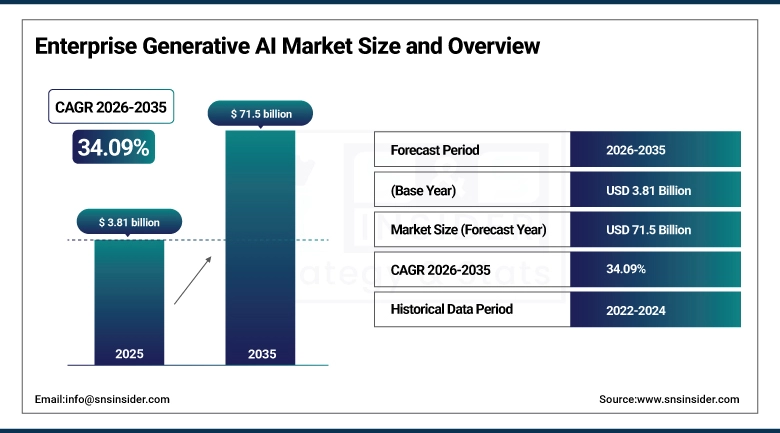

The Enterprise Generative AI Market was valued at USD 3.81 billion in 2025 and is expected to reach USD 71.5 billion by 2035, growing at a CAGR of 34.09% from 2026-2035.

Enterprise Generative AI market is growing as a result of fast digital transformation, increased demand for automation solutions, and AI-driven content creation, programming, and decision-making solutions. The application of generative AI by enterprises helps them improve their efficiency, lower operational costs, and engage more customers. The adoption of cloud computing services, large language models, and integration with business processes is making the global market grow even faster.

Gartner's CIO Agenda Survey documents that enterprise software and AI is now the top technology investment priority for CIOs globally surpassing cybersecurity as the primary budget allocation demonstrating the organizational commitment that is converting AI pilot programs into production enterprise deployments at scale.

Enterprise Generative AI Market Size and Forecast

-

Market Size in 2025: USD 3.81 Billion

-

Market Size by 2035: USD 71.5 Billion

-

CAGR: 34.09% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Enterprise Generative AI Market - Request Free Sample Report

Enterprise Generative AI Market Trends

-

Retrieval-Augmented Generation (RAG) architecture adoption is enabling enterprise AI applications to ground model outputs in enterprise-specific knowledge bases regulatory documents, product catalogs, customer records rather than relying solely on general training data, improving output accuracy for domain-specific enterprise queries.

-

Fine-tuned domain-specific models where foundation models are adapted on proprietary enterprise data to specialize in legal contract analysis, medical diagnosis support, financial risk assessment, or engineering design review are creating enterprise AI applications whose performance exceeds general-purpose model capabilities in specific task categories.

-

AI governance platform adoption is growing as enterprise compliance teams implement model monitoring, output auditing, bias detection, and explainability documentation capabilities that satisfy regulatory AI governance requirements in financial services, healthcare, and government sectors.

-

Multi-agent orchestration where multiple specialized AI agents collaborate on complex enterprise workflows, passing information between reasoning, retrieval, code execution, and communication agents is enabling automation of multi-step business processes that single-model prompting cannot complete reliably.

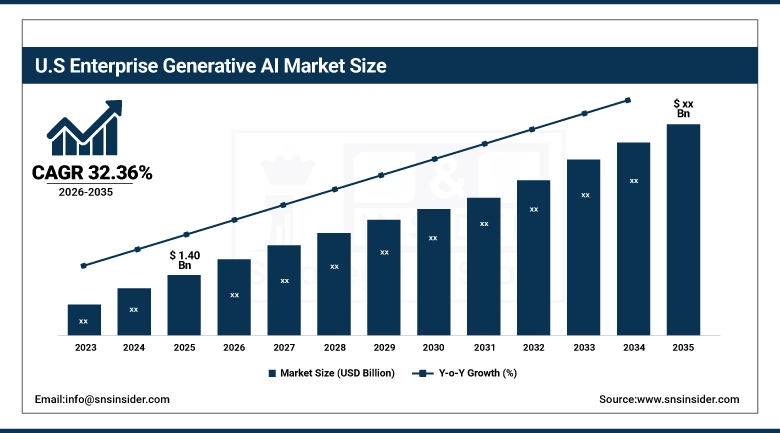

U.S. Enterprise Generative AI Market was valued at approximately USD 1.40 billion in 2025 and is expected to grow at a CAGR of 32.36% from 2026-2035.

The US Enterprise Generative AI market is growing because of highly developed innovation ecosystems in the country, adoption of enterprise cloud services, and application of generative AI in software development, marketing, and customer service. Large-scale investments in the field from tech leaders, new companies, and early adoption in industries such as BFSI, healthcare, and retail are pushing the market forward.

Microsoft's commercial announcement that Microsoft 365 Copilot reached over 400,000 organizations as customers within its first year of commercial availability represents the fastest enterprise software adoption in Microsoft's history demonstrating that enterprise generative AI is converting from innovative product to mainstream business tool faster than any previous enterprise software category.

Enterprise Generative AI Market Segment Analysis

-

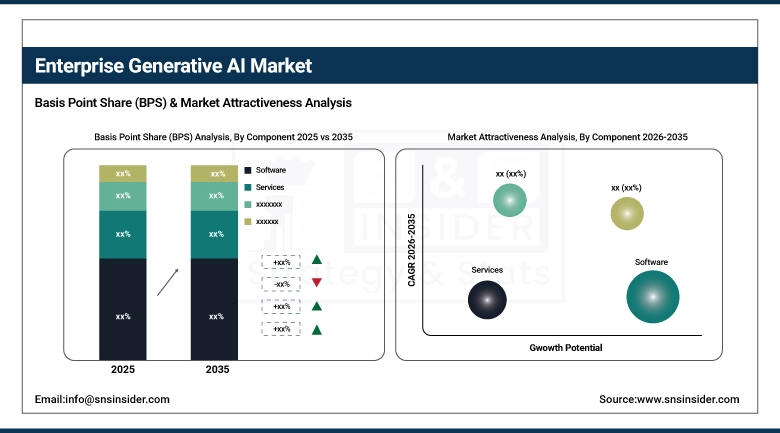

By Component, Software dominated the Enterprise Generative AI Market with the largest share; Services growing at the fastest CAGR.

-

By Deployment, Cloud dominated; On-Premises growing as regulated industries require data sovereignty.

-

By End Use, BFSI, Healthcare, and IT & Telecom hold large shares; Retail & E-Commerce growing at fastest CAGR.

By Component: Software dominant, Services growing fastest

Software held the dominant component position in the Enterprise Generative AI Market in 2025, encompassing the foundation model platforms, API infrastructure, enterprise AI application development environments, and pre-built AI application suites that constitute the primary commercial offering in enterprise generative AI. Foundation model platform licenses from OpenAI (Azure OpenAI Service), Anthropic (Claude for Enterprise), Google (Vertex AI), and Meta (Llama deployment on enterprise infrastructure) represent the highest-value software component whose commercial scale reflects the organizational commitment to generative AI as a platform investment rather than a project-level tool. Services are growing at the fastest CAGR, driven by the professional services market for enterprise AI implementation strategy consulting, model fine-tuning, RAG infrastructure deployment, AI governance framework implementation, and change management whose complexity creates demand for specialist expertise that few organizations maintain internally.

By Deployment: Cloud dominant, On-Premises growing fastest

Cloud has been the dominant player in the Enterprise Generative AI Market in the year 2025 due to its scalability, low-cost infrastructure implementation, and compatibility with the providers of foundation models, including OpenAI, Google Cloud, and Microsoft Azure. The cloud provides easy deployment for enterprise-wide implementations without significant capital expenses. It also enables continuous updates, distribution, and API access to the large language models. The On-Premise deployment segment has witnessed the highest Compound Annual Growth Rate (CAGR) during the forecast period owing to an increase in the number of regulated sectors, including banking, health care, defense, and governments. This is due to the need for data sovereignty and compliance within these sectors for sensitive data management.

By End Use: Multiple verticals significant, Retail fastest CAGR

The BFSI sector holds a large end-use share, reflecting financial services organizations' early and deep adoption of generative AI for credit decision narrative generation, regulatory document analysis, customer service automation, fraud detection narrative, and trading research summarization. The compliance-intensive nature of financial services creates both the governance requirements that enterprise AI must satisfy and the documentation workload that AI automation most compellingly addresses. Healthcare is a major enterprise AI end-use whose adoption is accelerating with FDA's and EMA's progressive framework development for AI-assisted clinical decision tools, medical documentation AI, and drug discovery workflow automation. Retail and E-Commerce is growing at the fastest end-use CAGR — where product description generation, personalized marketing content creation, customer service chatbot automation, and supply chain optimization represent AI applications whose ROI is immediately measurable in conversion rate, customer satisfaction, and operational cost metrics.

Enterprise Generative AI Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

89% |

|

Europe |

United Kingdom |

27% |

|

Asia Pacific |

China |

38% |

|

Middle East & Africa |

UAE |

40% |

|

Latin America |

Brazil |

48% |

North America Enterprise GenAI Market Insights

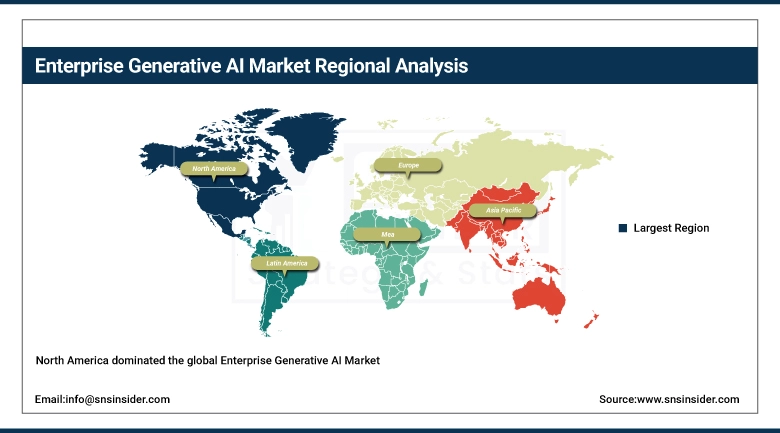

North America dominated the global Enterprise Generative AI Market, sustained by the United States' concentration of the world's most commercially active enterprise AI ecosystem. The U.S. federal government's AI executive orders requiring AI transparency, safety standards, and procurement frameworks for AI-powered government services are sustaining government enterprise AI market development alongside the private sector's commercially motivated adoption. Microsoft's enterprise AI platform dominance where Azure OpenAI Service, Microsoft 365 Copilot, and GitHub Copilot each address distinct enterprise user populations create the broadest single-vendor enterprise AI reach in any national market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Enterprise GenAI Market Insights

Europe's Enterprise Generative AI Market is growing with the EU AI Act's structured approach to AI governance which provides regulatory clarity that sustains enterprise AI investment within defined compliance frameworks and the progressive adoption of AI across European financial services, manufacturing, and healthcare sectors. The EU AI Act's classification of generative AI applications by risk tier creates compliance investment that sustains enterprise AI governance platform demand and specialist implementation service procurement. Germany's industrial enterprise AI adoption where AI-powered engineering design, quality control, and supply chain optimization applications are growing across automotive and mechanical engineering companies creates one of Europe's most commercially active enterprise AI markets.

Asia Pacific Enterprise GenAI Market Insights

Asia Pacific is the fastest-growing regional Enterprise Generative AI Market, driven by China's domestic large language model development where Baidu's ERNIE Bot, Alibaba's Tongyi Qianwen, and Tencent's Hunyuan are competing for Chinese enterprise AI market share against international models whose use Chinese data sovereignty requirements may constrain Japan's enterprise AI adoption acceleration, and India's growing IT services sector whose AI capabilities are being marketed to global enterprise clients. South Korea's semiconductor and electronics enterprises Samsung, SK Hynix, LG Electronics are deploying enterprise AI for chip design optimization, quality control AI, and engineering productivity applications that represent some of Asia Pacific's most technically sophisticated enterprise AI deployments.

MEA and Latin America Enterprise GenAI Market Insights

The UAE's Enterprise Generative AI Market is advancing with the government's ambitious AI National Strategy which targets making the UAE a global AI hub by the end of the decade and the adoption of AI across the Gulf states' banking, energy, and government service sectors whose digital transformation ambitions create substantial enterprise AI procurement. Latin America's enterprise AI market is growing in Brazil's financial services sector where major banks including Itaú Unibanco and Bradesco are deploying AI for credit decision, customer service, and fraud detection applications and Mexico's manufacturing and export-oriented enterprise sector.

Enterprise GenAI Market Growth Drivers:

-

Enterprise automation demand and foundation model cost reduction driving extraordinary enterprise generative AI market growth globally

Increasing demands for enterprise automation and reduced costs of foundation models are leading to high growth rates in the Enterprise Generative AI Market around the world. Businesses are embracing the technology to automate content generation, coding, customer service, and decision-making tasks, thereby enhancing efficiency and productivity. Additionally, the decreasing prices of foundation models and enhanced accessibility through cloud-based API solutions are making it easier for companies of different sizes to adopt the technology.

Enterprise GenAI Market Restraints:

-

Data privacy concerns and AI hallucination risks creating enterprise generative AI market adoption challenges globally

Enterprise generative AI adoption is constrained by the AI hallucination problem where large language models generate plausible-sounding but factually incorrect outputs with a confidence that human review may not reliably catch whose consequences in high-stakes enterprise applications including legal advice, financial analysis, and medical documentation create liability exposure that conservative organizations find commercially unacceptable without robust human oversight processes. Data privacy concerns where enterprise customers who send proprietary data to external AI providers face potential exposure of trade secrets, client information, and competitive intelligence sustain resistance to public cloud AI API adoption among the most security-sensitive enterprise segments.

Enterprise GenAI Market Opportunities:

-

Agentic AI deployment and vertical industry foundation models creating transformative enterprise generative AI growth opportunities globally

Agentic AI where AI systems execute multi-step tasks autonomously, using tools, browsing the web, writing and executing code, and interacting with APIs without continuous human direction represents enterprise generative AI's most commercially transformative emerging capability. An AI agent that autonomously processes a purchase order from receipt through vendor verification, budget approval workflow, ERP entry, and supplier confirmation a workflow that currently requires human handling at each step creates operational cost savings whose scale justifies significant enterprise investment. The emergence of vertical industry foundation models trained specifically on legal documents, medical literature, financial filings, or engineering specifications is enabling AI performance in specialized domains that surpasses general-purpose model performance with smaller model sizes and lower inference costs.

Recent Developments:

-

2026: Anthropic launched Claude Enterprise Ultra a fine-tuned enterprise AI platform combining Claude's constitutional AI safety framework with enterprise-specific capabilities including automated compliance checking, multi-jurisdiction legal reasoning, and document redaction receiving ISO 27001 and SOC 2 Type II certification within 90 days of launch and achieving 500 Fortune 1000 customer deployments in its first six months, reporting 67% customer utilization in legal, compliance, and contract management workflows where accuracy and auditability requirements sustain premium enterprise pricing.

-

2025: Microsoft expanded Microsoft 365 Copilot with Copilot Studio autonomous agents enabling enterprise IT teams to build AI agents that autonomously complete multi-step business processes including HR onboarding, IT service desk resolution, and finance exception handling without continuous human oversight reporting that early access customers deploying autonomous agents achieved 40% reduction in routine process handling time and 28% improvement in employee satisfaction scores from reduced administrative burden on knowledge workers.

Enterprise Generative AI Market Key Players

Some of the Enterprise Generative AI Market Companies

-

Microsoft Corporation (Azure OpenAI, Copilot)

-

Alphabet Inc. (Google Cloud Vertex AI, Gemini)

-

Amazon Web Services Inc. (Amazon Bedrock)

-

OpenAI Inc. (ChatGPT Enterprise, API)

-

Anthropic PBC (Claude for Enterprise)

-

Meta Platforms Inc. (Llama, Meta AI)

-

IBM Corporation (watsonx)

-

Salesforce Inc. (Einstein AI)

-

ServiceNow Inc. (Now Assist)

-

Workday Inc. (Workday AI)

-

Oracle Corporation (Oracle AI)

-

SAP SE (Joule AI)

-

Adobe Inc. (Adobe Firefly, Sensei)

-

Cohere Inc.

-

Mistral AI SAS

-

Inflection AI Inc.

-

Stability AI Ltd.

-

C3.ai Inc.

-

Writer Inc.

-

Jasper AI Inc.

Enterprise Generative AI Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.81 Billion |

| Market Size by 2035 | USD 71.5 Billion |

| CAGR | CAGR of 34.09% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Software, Services) • By Deployment (Cloud, On-Premises) • By Enterprise Size (Large Enterprises, SMEs) • By End Use (BFSI, Healthcare, Retail & E-Commerce, Manufacturing, IT & Telecom, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Microsoft Corporation (Azure OpenAI, Copilot); Alphabet Inc. (Google Cloud Vertex AI, Gemini); Amazon Web Services Inc. (Amazon Bedrock); OpenAI Inc. (ChatGPT Enterprise, API); Anthropic PBC (Claude for Enterprise); Meta Platforms Inc. (Llama, Meta AI); IBM Corporation (watsonx); Salesforce Inc. (Einstein AI); ServiceNow Inc. (Now Assist); Workday Inc. (Workday AI); Oracle Corporation (Oracle AI); SAP SE (Joule AI); Adobe Inc. (Adobe Firefly, Sensei); Cohere Inc.; Mistral AI SAS; Inflection AI Inc.; Stability AI Ltd.; C3.ai Inc.; Writer Inc.; Jasper AI Inc. |

Frequently Asked Questions

The Enterprise Generative AI Market was valued at USD 3.81 billion in 2025.

North America dominated; Asia Pacific is the fastest growing regional market.

Retail & E-Commerce is growing at the fastest CAGR; BFSI, Healthcare, and IT & Telecom hold large shares.

Software dominated; Services are growing at the fastest CAGR.

The Enterprise Generative AI Market is expected to grow at a CAGR of 34.09% from 2026 to 2035.

Get in Touch