Vendor Risk Management Market Report Scope & Overview:

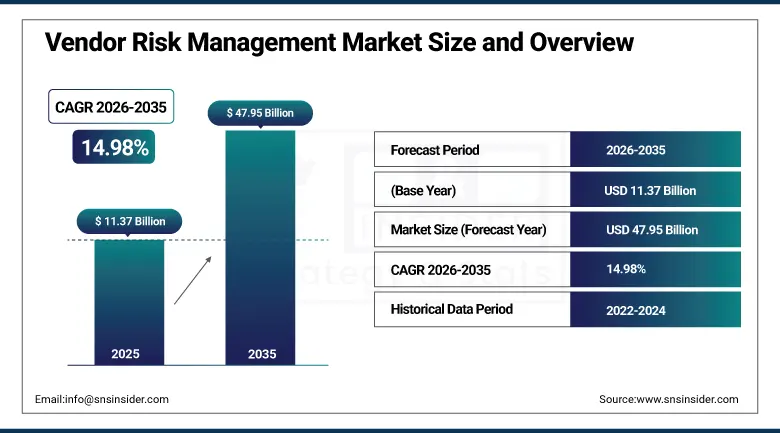

The Vendor Risk Management Market was valued at USD 11.37 Billion in 2025 and is expected to reach USD 47.95 Billion by 2035, growing at a CAGR of 14.98% from 2026 to 2035.

Vendor risk management (VRM) encompasses the software platforms, professional services, and structured frameworks that organisations deploy to identify, assess, monitor, and mitigate the operational, financial, cybersecurity, compliance, and reputational risks arising from their dependence on third-party vendors, suppliers, and business partners. As enterprise operations have grown increasingly dependent on outsourced functions, cloud service providers, and complex multi-tier supply chains, the attack surface and compliance exposure created by third-party relationships has expanded dramatically, transforming vendor risk management from a periodic procurement due-diligence exercise into a continuous, board-level strategic priority. Modern VRM platforms integrate automated vendor onboarding assessments, continuous cybersecurity posture monitoring, financial stability scoring, regulatory compliance tracking, and contract lifecycle management within unified dashboards that provide chief risk officers and procurement leaders with real-time visibility into third-party risk exposure across their entire vendor ecosystem.

In July 2023, AuditBoard launched AuditBoard ITRM, a purpose-built IT risk management solution designed for CISOs and their security teams that streamlines the identification and classification of IT systems, accelerates business impact assessments, and aids remediation of identified vulnerabilities across organisational IT risk programmes. The platform's design to enhance collaboration across IT security and other organisational functions demonstrated the growing commercial importance of integrated risk management platforms whose cross-functional workflow capability addresses the reality that effective vendor and IT risk management requires coordinated input from security, procurement, legal, and business unit stakeholders rather than siloed risk assessment processes.

Market Size and Forecast

-

Market Size in 2026E: USD 13.07 Billion

-

Market Size by 2035: USD 47.95 Billion

-

CAGR: 14.98% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Vendor Risk Management Market - Request Free Sample Report

Vendor Risk Management Market Trends

-

AI-powered continuous vendor monitoring is enabling real-time assessment of cybersecurity, financial, compliance, and operational risks across third-party ecosystems.

-

Integration of vendor risk management with enterprise risk and GRC platforms is providing organizations with unified risk visibility and governance.

-

ESG risk monitoring is becoming a key capability as organizations strengthen supply chain sustainability and regulatory compliance initiatives.

-

Fourth-party and extended supply chain risk visibility is expanding to address risks originating from subcontractors and multi-tier vendor networks.

-

Cloud-based vendor risk management platforms continue to dominate adoption due to their scalability, real-time analytics, automated compliance updates, and lower total cost of ownership.

The U.S. Vendor Risk Management Market Outlook

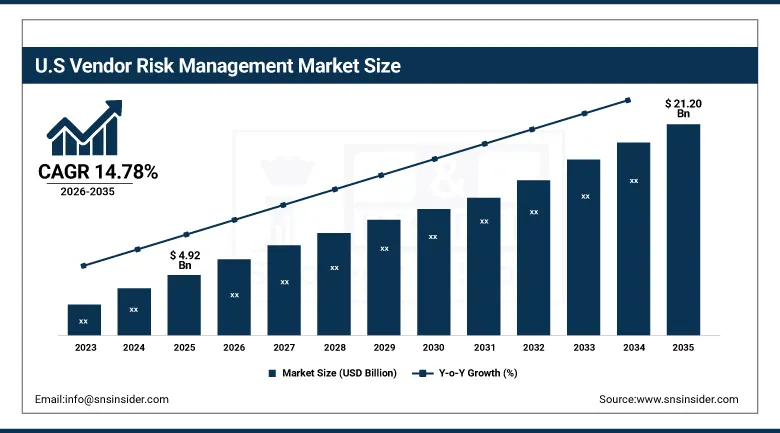

The U.S. Vendor Risk Management Market was valued at approximately USD 4.92 Billion in 2025 and is expected to reach approximately USD 21.20 Billion by 2035, growing at a CAGR of approximately 14.78%.

The United States vendor risk management market is anchored by the nation's tight regulatory landscape spanning GDPR-equivalent state privacy laws, HIPAA healthcare data protection requirements, SOX financial control mandates, and sector-specific regulations from the OCC, CFPB, and HITECH Act that collectively require formal documented third-party risk oversight programmes across virtually every regulated industry. The U.S. financial services sector's extensive vendor dependency for core banking systems, payment processing, and cloud infrastructure creates among the most sophisticated VRM platform adoption globally, driven by both regulatory examination requirements and the catastrophic reputational and financial consequences that major U.S. banks and financial institutions have experienced from third-party data breaches.

In 2025, MetricStream expanded its AI-powered third-party risk management platform with enhanced continuous monitoring capabilities that automatically track vendor cybersecurity posture changes, sanctions list updates, and adverse media signals across the organisation's entire vendor portfolio without requiring manual reassessment cycles. The platform's automated evidence gathering and document parsing capability, designed to reduce the analyst workload burden that comprehensive vendor risk assessment programmes traditionally require, demonstrated the growing commercial importance of AI-assisted risk management workflows whose efficiency gains enable organisations to scale third-party risk oversight across rapidly expanding vendor ecosystems without proportional headcount growth.

Vendor Risk Management Market Segment Analysis

-

By Component, solutions dominated the vendor risk management market with the largest revenue share in 2025, while services are the fastest growing component during 2026 to 2035.

-

By Solution Type, financial control dominated the market in 2025, while compliance management is the fastest growing solution type as enterprises integrate VRM with broader ERM frameworks.

-

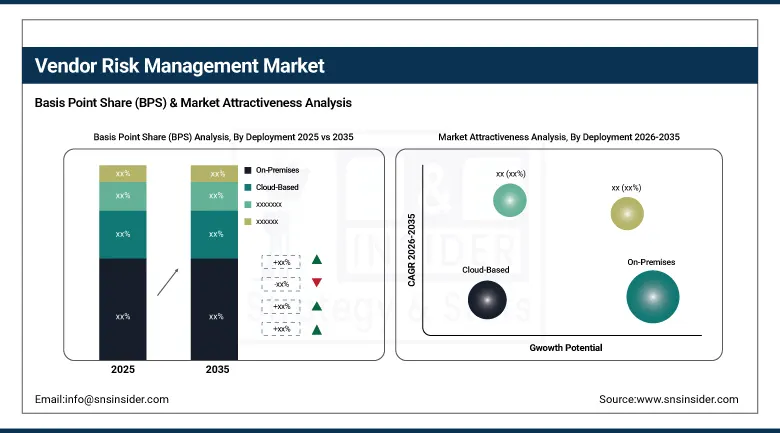

By Deployment, on-premises solutions held over 67% revenue share in 2025, while cloud-based solutions are projected to grow rapidly as companies migrate to SaaS models.

-

By Organization Size, SMEs accounted for over 69% share in 2025 due to affordable SaaS-based VRM tools, while large enterprises are expected to grow fastest given their complex vendor ecosystems.

By Solution Type, financial control dominates, compliance management grows fastest

Financial control generated the dominant solution type revenue share in 2025, reflecting organisations' foundational reliance on financial-risk due diligence to evaluate vendor stability, creditworthiness, and operational viability before establishing or renewing critical vendor relationships. Financial control assessment, which evaluates vendor balance sheet strength, credit ratings, payment history, and business continuity risk indicators, addresses the fundamental commercial risk that vendor financial distress or insolvency poses to organisational supply chain continuity and represents the most universally applicable VRM solution type across every industry vertical regardless of cybersecurity or regulatory complexity considerations. The widespread adoption of financial control assessment as a baseline vendor onboarding requirement escalated the demand.

Compliance management is expected to grow at the fastest CAGR, with documented growth rates of approximately 16.7%, as enterprises increasingly integrate VRM with broader enterprise risk management frameworks that enable unified oversight of multiple risk categories spanning regulatory compliance, operational risk, and strategic risk within a single governance structure. The proliferation of sector-specific and jurisdiction-specific regulatory frameworks, each imposing distinct vendor oversight documentation requirements, has created an increasingly complex compliance landscape that manual compliance tracking processes cannot efficiently manage, driving demand for automated compliance management modules whose regulatory framework mapping and automated evidence collection capabilities directly address this complexity.

By Deployment, on-premises holds historical share, cloud-based grows fastest

On-premises solutions held over 67% revenue share in 2025, reflecting the historical preference of heavily regulated industries including financial services, healthcare, and government for VRM deployments whose data residency, security control, and customisation capability within organisationally controlled infrastructure satisfied strict data governance policies that early-generation cloud platforms could not adequately address. Organisations subject to the most stringent regulatory data sovereignty requirements, particularly in banking and government sectors, have historically favoured on-premises VRM deployment to maintain direct control over sensitive vendor risk data and assessment documentation whose disclosure or breach could create significant regulatory and reputational consequences.

Cloud-based solutions are projected to grow rapidly as companies migrate to SaaS models that require scalable, cost-efficient VRM tools whose real-time analytics, automatic software updates, and lower total cost of ownership increasingly outweigh the data sovereignty advantages that justified historical on-premises preference. Cloud-based VRM platforms' capability for continuous monitoring, automated threat intelligence integration, and rapid deployment without significant IT infrastructure investment has made them the preferred choice for organisations building new VRM programmes, while modern cloud security certifications including SOC 2, ISO 27001, and FedRAMP have progressively addressed the data governance concerns that previously constrained cloud adoption in regulated industries.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.47% |

|

Europe |

Germany |

28.47% |

|

Asia Pacific |

China |

38.47% |

|

Middle East & Africa |

UAE |

22.84% |

|

Latin America |

Brazil |

43.84% |

North America Vendor Risk Management Market Insights

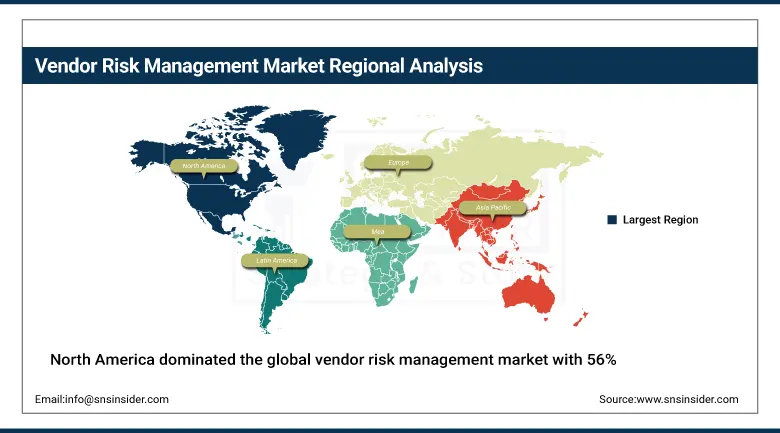

North America dominated the global vendor risk management market with 56% share in 2025, attributable to its advanced compliance ecosystem, high digital adoption, and frequent third-party security incidents that have elevated VRM to a board-level strategic priority across virtually every regulated industry. The United States accounts for approximately 82.47% of regional revenue through the large presence of technology companies, extensive adoption of cloud-based VRM solutions, and increased organisational spending to protect against cyber risks and comply with data privacy and vendor management regulations. The concentration of major VRM platform vendors including MetricStream, LogicManager, Prevalent, and Aravo Solutions headquartered in North America sustains the region's technology leadership position and creates a deep talent and innovation ecosystem that reinforces continued market leadership.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Vendor Risk Management Market Insights

Europe held the second largest share of global vendor risk management revenues in 2025, driven by stringent regulations including GDPR that compel companies across the EU to implement formal vendor risk management practices whose documentation requirements and substantial penalty exposure for non-compliance create non-discretionary VRM platform adoption. Germany accounts for approximately 28.47% of European revenues through its large industrial and financial services sectors whose extensive vendor ecosystems require sophisticated risk oversight, the United Kingdom and France contribute significant additional market share through their developed financial services and technology sectors, and the EU's Digital Operational Resilience Act's financial sector-specific third-party risk requirements are creating substantial new compliance-driven VRM platform demand across European banks and insurers.

Asia Pacific Vendor Risk Management Market Insights

Asia Pacific is the fastest-growing regional vendor risk management market, as massive digital transformation, cloud migration, and IT outsourcing reshape vendor ecosystems in China, India, Japan, and Australia. Growing cyberattacks and compliance modernisation are further accelerating VRM adoption across the region. China accounts for approximately 38.47% of Asia Pacific revenues through its rapidly expanding technology and financial services sectors whose vendor ecosystem complexity is growing with the country's digital economy expansion, while India's large IT outsourcing and business process outsourcing industry creates particularly significant VRM platform demand as both a vendor and a customer of third-party risk management services within the global technology supply chain.

MEA & Latin America Vendor Risk Management Market Insights

Middle East and Latin America are growing vendor risk management markets where digital transformation, expanding financial services regulation, and growing cybersecurity awareness are creating increasing commercial demand. The UAE leads MEA revenues at approximately 22.84% of the regional total through its position as a regional financial and technology hub whose growing fintech sector and cross-border vendor relationships create sophisticated VRM platform requirements. Brazil leads Latin American revenues at approximately 43.84% of the regional total through its large financial services sector, growing data protection regulatory framework under the LGPD, and expanding technology sector whose vendor ecosystem complexity is increasing with digital transformation investment.

Market Dynamics

Growth Driver: Intensifying third-party cybersecurity threats and tightening global regulatory compliance mandates requiring formal vendor risk oversight are the primary structural growth drivers of the vendor risk management market.

The vendor risk management market's exceptional growth trajectory is powered by the convergence of escalating third-party cyber risk, whose documented surge in supply-chain attacks has elevated vendor security posture to a board-level concern, and an expanding global regulatory framework whose GDPR, HIPAA, SOX, and DORA mandates create compliance-driven non-discretionary VRM platform adoption across regulated industries. Each new regulatory framework that explicitly mandates formal third-party risk documentation, evidence collection, and continuous monitoring capability creates proportional VRM platform demand growth whose adoption timeline is compressed by mandatory compliance deadlines rather than discretionary technology investment cycles. The growing complexity of multi-tier vendor ecosystems, where organisations' direct technology and service vendors themselves depend on extensive subcontractor networks, is simultaneously expanding the technical scope and platform sophistication that comprehensive VRM solutions must address.

Restraint: High implementation complexity and the shortage of skilled risk management professionals create adoption barriers that constrain VRM platform deployment speed in resource-constrained organisations.

Comprehensive VRM platform implementation requires substantial organisational change management, including establishing standardised vendor risk assessment methodologies, integrating VRM workflows with existing procurement and legal processes, and training risk management staff in platform usage and risk assessment interpretation, creating implementation timelines and resource requirements that can extend procurement-to-value realisation periods by six to twelve months for comprehensive enterprise deployments. The global shortage of skilled third-party risk management professionals whose specialised expertise spans cybersecurity assessment, regulatory compliance interpretation, and financial risk analysis creates talent acquisition challenges that constrain organisations' capacity to fully leverage advanced VRM platform capabilities, particularly in mid-market organisations whose smaller risk management teams must manage increasingly sophisticated vendor risk programmes with limited specialised headcount.

Opportunity: AI-powered continuous monitoring and ESG risk integration represent transformative commercial frontiers expanding VRM platform value propositions beyond traditional periodic assessment models.

The integration of artificial intelligence and machine learning capabilities into VRM platforms for automated document parsing, continuous cybersecurity posture monitoring, and predictive risk scoring represents a fundamental platform capability evolution whose efficiency gains enable organisations to scale comprehensive third-party risk oversight across rapidly expanding vendor ecosystems without proportional analyst headcount growth. Each AI capability that reduces manual risk assessment workload while improving risk detection accuracy creates demonstrable return on investment that justifies premium platform pricing and accelerates displacement of legacy manual assessment processes. ESG risk monitoring integration, driven by expanding regulatory requirements including the EU Corporate Sustainability Reporting Directive's supply chain disclosure mandates, represents an emerging high-growth VRM capability whose adoption is expanding the addressable market beyond traditional cybersecurity and financial risk assessment.

Recent Developments:

-

2025: MetricStream expanded its AI-powered third-party risk management platform with enhanced continuous monitoring capabilities that automatically track vendor cybersecurity posture, sanctions list updates, and adverse media signals, reducing manual reassessment burden and enabling real-time vendor risk visibility across enterprise portfolios.

-

2023: AuditBoard launched AuditBoard ITRM, a purpose-built IT risk management solution for CISOs designed to enhance collaboration across organisational functions, accelerating identification and classification of IT systems and streamlining business impact assessments for vendor-related technology risk.

-

2023: Multiple leading VRM platform providers including Prevalent and Aravo Solutions expanded their compliance management modules to address the EU Digital Operational Resilience Act's financial sector third-party risk requirements, supporting European banks and insurers in meeting new regulatory third-party oversight mandates.

Vendor Risk Management Market Key Players are:

-

MetricStream Inc.

-

LogicManager Inc.

-

Prevalent Inc.

-

Aravo Solutions Inc.

-

SAP Ariba (SAP SE)

-

Oracle Corporation (GRC)

-

IBM Security

-

RSA Security LLC

-

Genpact Limited

-

LockPath (NAVEX Global)

-

SAI Global

-

Resolver Inc.

-

OneTrust LLC

-

ServiceNow Inc.

-

Diligent Corporation

-

BitSight Technologies Inc.

-

SecurityScorecard Inc.

-

CyberGRX Inc.

-

Panorays Ltd.

-

UpGuard Inc.

Vendor Risk Management Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 11.37 Billion |

| Market Size by 2035 | USD 47.95 Billion |

| CAGR | CAGR of 14.98% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solutions, Services) • By Solution Type (Financial Control, Compliance Management, Vendor Information Management, Contract Management, Audit Management, Quality Assurance Management) • By Deployment (On-Premises, Cloud-Based) • By Organization Size (Small & Medium Enterprises, Large Enterprises) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | MetricStream Inc., LogicManager Inc., Prevalent Inc., Aravo Solutions Inc., SAP Ariba (SAP SE), Oracle Corporation (GRC), IBM Security, RSA Security LLC, Genpact Limited, LockPath (NAVEX Global), SAI Global, Resolver Inc., OneTrust LLC, ServiceNow Inc., Diligent Corporation, BitSight Technologies Inc., SecurityScorecard Inc., CyberGRX Inc., Panorays Ltd., and UpGuard Inc. |

Frequently Asked Questions

The financial control segment dominated the Vendor Risk Management Market in 2025 as organisations rely on financial-risk due diligence to evaluate vendor stability, creditworthiness, and operational viability across their vendor relationships.

North America dominated the Vendor Risk Management Market in 2025, holding 56% of global revenues.

Intensifying third-party cybersecurity threats driving board-level risk priority, tightening global regulatory compliance mandates including GDPR, HIPAA, and DORA requiring formal vendor risk oversight.

The Vendor Risk Management Market was valued at USD 11.37 Billion in 2025.

The Vendor Risk Management Market is expected to grow at a CAGR of 14.98% from 2026 to 2035.

Get in Touch