Personal Loans Market Report Scope & Overview:

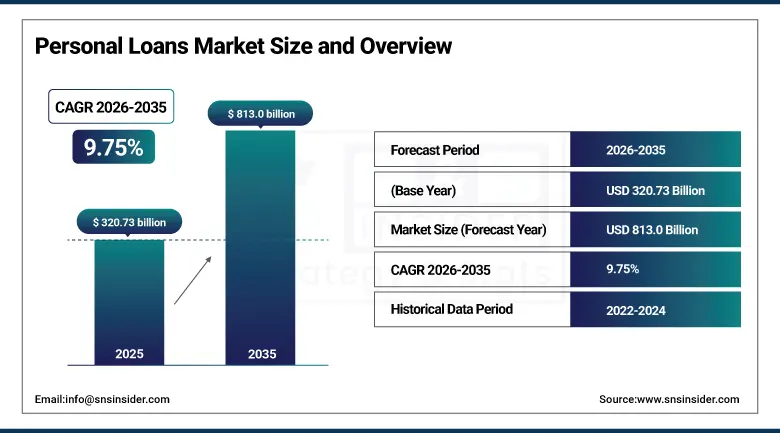

The Personal Loans Market was valued at USD 320.73 billion in 2025 and is expected to reach USD 813.0 billion by 2035, growing at a CAGR of 9.75% from 2026–2035.

Personal loans represent the most flexible and widely accessible category of consumer credit, providing individuals with lump-sum or revolving access to borrowed funds for any personal purpose without the collateral requirements that restrict mortgage and auto loan access, the use-case restrictions that constrain student loan and business financing eligibility, or the revolving high-cost characteristics of credit card debt that make extended credit card balances financially disadvantageous for borrowers who need multi-year repayment horizons. The market encompasses a diverse range of borrowing instruments including unsecured personal instalment loans extended by banks, credit unions, and online lenders based solely on creditworthiness assessment, secured personal loans backed by savings deposits, vehicles, or other personal assets that command lower interest rates through collateral risk mitigation, personal lines of credit providing revolving access to pre-approved credit limits for ongoing or uncertain funding needs, and specialist debt consolidation loan products that combine multiple higher-rate debt obligations into a single lower-rate loan to reduce monthly payment burden and total interest cost.

The Federal Reserve's 2025 Survey of Consumer Finances confirming that personal loan balances reached their highest level in U.S. history in 2024, driven by the combination of persistent inflation-driven household expense inflation, home equity accessibility limitations at elevated mortgage rates, and the proliferation of one-click digital loan application platforms, validates the structural demand drivers that are sustaining personal loan market growth independent of interest rate cycle fluctuations.

Market Size and Forecast

-

Market Size in 2026E: USD 351.97 Billion

-

Market Size by 2035: USD 813.0 Billion

-

CAGR: 9.75% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Personal Loans Market - Request Free Sample Report

Personal Loans Market Trends

-

Accelerating adoption of AI-powered credit assessment models that supplement traditional credit bureau score-based underwriting with alternative data sources including bank account transaction analysis, payroll connectivity, rental payment history, utility bill payment records, and professional credential databases, enabling more accurate creditworthiness prediction and expanding credit access to the estimated 50 million credit-invisible Americans and hundreds of millions of underbanked consumers globally whose lack of traditional credit file history renders them ineligible for conventional personal loan products.

-

Rapid growth of buy-now-pay-later personal credit products that offer interest-free or low-interest instalment payment options at the point of retail purchase through embedded financing platforms, representing a structural evolution of traditional personal lending from bank-originated term loans toward merchant-embedded consumer finance that integrates directly into the digital commerce checkout experience.

-

Growing demand for green personal loans with preferential interest rates for financing environmentally beneficial consumer investments including residential solar panel installation, electric vehicle purchase, home energy efficiency upgrades, and sustainable home renovation projects, as banks and fintech lenders introduce sustainability-linked consumer lending products in response to consumer environmental values and regulatory encouragement of green finance product development.

-

Increasing use of open banking and consumer-permissioned financial data sharing to accelerate loan application processing, where borrowers grant lenders direct digital access to their bank account transaction history through open banking APIs that provide real-time income verification, expense pattern analysis, and cash flow sufficiency assessment without requiring document upload, bank statement mailing, or employment verification phone calls.

-

Rising adoption of income-share agreements and revenue-based personal financing alternatives for education and professional development purposes, where repayment obligations are tied to borrower income outcomes rather than fixed instalment schedules, aligning lender and borrower incentives around successful income generation rather than creating debt obligations that persist regardless of borrower financial circumstances.

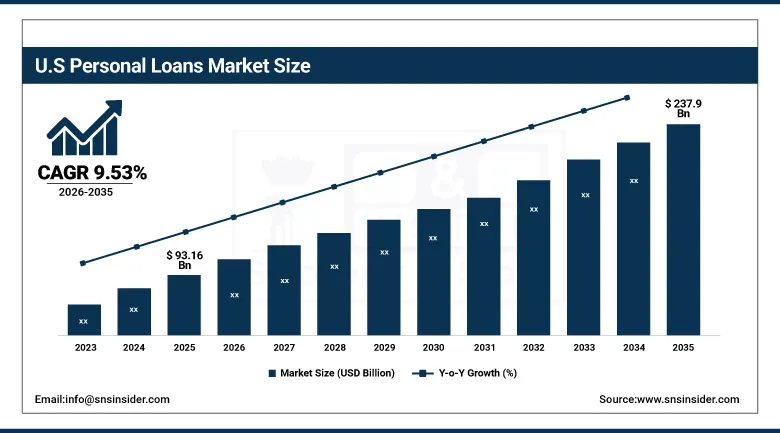

The U.S. Personal Loans Market Outlook

The U.S. Personal Loans Market was valued at approximately USD 93.16 billion in 2025 and is expected to reach approximately USD 237.9 billion by 2035, growing at a CAGR of 9.53%.

The United States is the world's largest and most commercially competitive personal loans market, where the combination of the world's highest consumer credit utilisation rates, an extraordinarily diverse lending landscape encompassing major money-center banks, regional banks, credit unions, specialty finance companies, and a mature fintech lending ecosystem, and sophisticated consumer financial awareness of personal loan products as a debt management and large purchase financing tool collectively create the conditions for sustained market expansion. Total U.S. consumer personal loan balances exceeded USD 225 billion in 2025 across all lender types, with fintech lenders including SoFi, LendingClub, Upstart, and Avant originating approximately 30 to 35% of personal loan volume by count despite their younger market vintage relative to the established bank personal loan portfolios of JPMorgan Chase, Bank of America, Citibank, and Wells Fargo.

The Consumer Financial Protection Bureau's open banking rulemaking under Section 1033 of the Dodd-Frank Act, requiring covered financial institutions to provide consumers with machine-readable digital access to their transaction data through standardized APIs, is creating the regulatory foundation for widespread open banking-enabled personal loan applications that will dramatically reduce the friction and documentation burden of borrower income verification across the U.S. personal loans market.

Personal Loans Market Segment Analysis

-

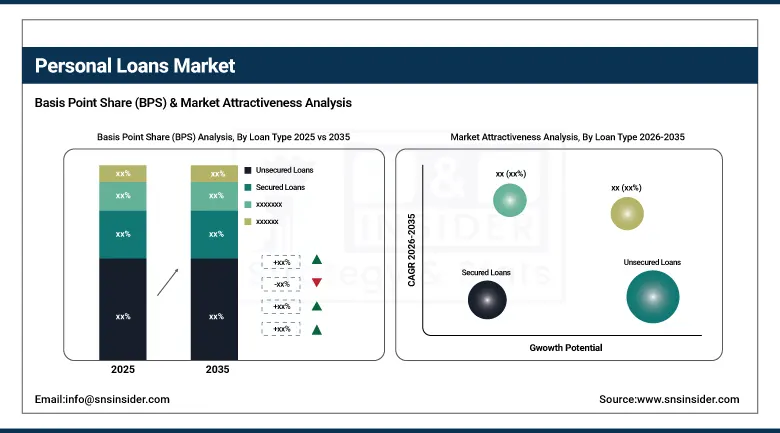

By Loan Type, Unsecured Loans dominated with approximately 44.80% in 2025; Debt Consolidation Loans are the fastest-growing type at a CAGR of 10.40%.

-

By Loan Tenure, Medium-Term Loans led with approximately 51.20% in 2025; Short-Term Loans are the fastest-growing at a CAGR of 11.04%.

-

By Lender Type, Banks led with approximately 50.24% in 2025; Online Lenders are the fastest-growing at a CAGR of 11.20%.

-

By Loan Purpose, Debt Consolidation led with approximately 35.32% in 2025 as the primary use case across all personal loan categories; Home Improvement is the fastest-growing purpose at a CAGR of 10.30%.

By Loan Type, Unsecured Loans dominate, debt consolidation is expected to grow fastest

Unsecured Loans retained the dominant position with approximately 44.80% of the personal loans market in 2025, reflecting their fundamental commercial appeal as the most accessible, fastest-to-fund, and most flexible personal borrowing instrument available to creditworthy consumers without the requirement to pledge personal assets as security for a lender who might exercise repossession rights upon payment default. The unsecured personal loan's combination of fixed interest rate, fixed repayment schedule, and defined loan maturity provides the budgeting certainty that consumers managing multiple financial obligations prefer over the variable minimum payment and revolving utilisation characteristics of credit cards and personal lines of credit when financing known-cost expenditures with predictable repayment timelines.

Debt Consolidation Loans are the fastest-growing loan type at a CAGR of 10.40% through 2035, sustained by the persistent and in several major markets growing aggregate consumer credit card debt that creates ongoing demand for the interest cost reduction achievable through refinancing high-rate revolving credit card balances into lower-rate fixed-term personal loans.

By Lender Type, Banks dominate, Online Lenders are expected to grow fastest

Banks retained the dominant lender type position with approximately 50.24% of personal loans market revenues in 2025, reflecting the advantage that existing customer relationships provide in personal loan origination, where banks can offer pre-approved personal loan offers to existing deposit and checking account holders based on their internal transaction history without requiring any application process beyond acceptance confirmation, creating a frictionless origination pathway that fintech lenders whose customer relationships do not include daily transaction visibility cannot replicate.

Online Lenders are the fastest-growing lender type at a CAGR of 11.20% through 2035, driven by their structural advantages in application speed, underwriting methodology breadth, and digital user experience design that serve the growing proportion of personal loan borrowers who priorities convenience and credit access over brand familiarity and prefer entirely digital loan management through mobile applications rather than bank branch or call center interaction.

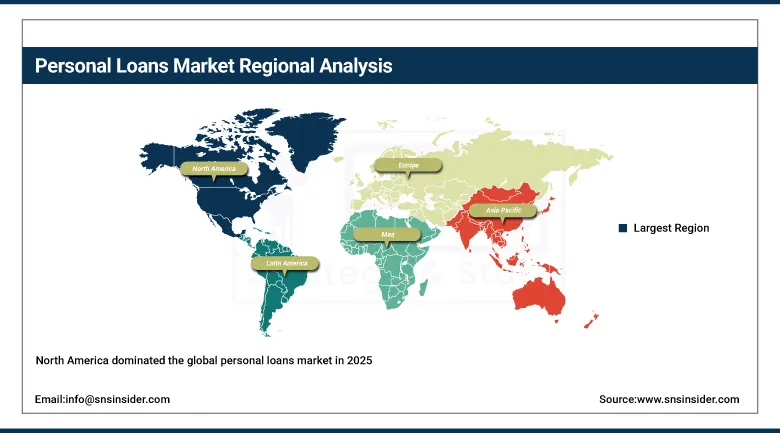

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

85.4% |

|

Europe |

United Kingdom |

26.2% |

|

Asia Pacific |

China |

44.1% |

|

Middle East & Africa |

Saudi Arabia |

29.7% |

|

Latin America |

Brazil |

43.5% |

North America Personal Loans Market Insights

North America dominated the global personal loans market in 2025, with the United States accounting for approximately 85.4% of North American revenues as the world's largest consumer credit market by aggregate outstanding balance. The region's market leadership reflects the highest per-capita consumer debt levels among major economies, the most competitive lending landscape combining traditional bank personal loan programmes with a mature fintech lender ecosystem, high consumer financial literacy regarding personal loan products as credit card debt alternatives, and regulatory frameworks that protect consumer rights in lending transactions while maintaining competitive market access that sustains innovation in lending product design and credit assessment methodology. Canada contributes approximately 14.6% of North American revenues through its large chartered bank personal lending programmes and growing fintech lending ecosystem.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Personal Loans Market Insights

Europe is a sophisticated personal loans market characterised by well-established bank personal lending programmes across all major national markets, progressive open banking regulatory infrastructure under PSD2 that is enabling the account information service providers and payment initiation service providers who power the frictionless digital lending experiences of European fintech lenders, and a consumer credit regulatory environment under the Consumer Credit Directive and its proposed revised CCD2 framework that mandates responsible lending assessments and fee transparency requirements that shape product design across the lending market. The United Kingdom accounts for approximately 26.2% of European personal loans revenues as the region's most competitive personal lending market, where challenger banks including Monzo, Starling, and Revolut have built personal loan products directly into their digital-first banking propositions and traditional lenders including Barclays, HSBC, and Lloyds compete actively on digital application experience and pricing.

Asia Pacific Personal Loans Market Insights

Asia Pacific is the fastest-growing personal loans market, driven by the combination of rapidly expanding middle-class populations with growing disposable income and credit demand, progressive financial services digitization across China, India, South Korea, Southeast Asia, and Australia that is making formal personal lending accessible to previously underbanked consumer segments, and the extraordinary growth of mobile-first digital lending platforms that provide instant personal loan approval and disbursement through smartphone applications without requiring bank branch visits or extensive documentation submission. China accounts for approximately 44.1% of Asia Pacific personal loans revenues through the world's largest mobile lending ecosystem where platforms including Ant Group's Huabei consumer credit and WeBank's digital personal loan products serve hundreds of millions of consumers with small-ticket personal loans accessible through super-app interfaces that integrate lending seamlessly with daily commerce, communication, and entertainment activities.

MEA & Latin America Personal Loans Market Insights

The Middle East and Africa and Latin America represent growing personal loans markets were expanding financial inclusion initiatives, rapid smartphone penetration enabling mobile lending access, and progressive reduction in the share of adult population that remains unbanked or underbanked are creating new personal lending addressable markets across consumer segments that formal credit has not previously served. Saudi Arabia leads MEA personal loans revenues at approximately 29.7% of regional revenues through its combination of high per-capita income creating substantial consumer credit demand, well-developed commercial banking sector offering competitive personal lending products, and Sharia-compliant personal financing products that structure loan economics through murabaha and ijara frameworks that serve the Islamic finance principles of the majority population without interest-bearing conventional loan structures. Brazil leads Latin American revenues at approximately 43.5% of regional revenues through its large consumer credit market, the proliferation of Brazilian digital fintech lenders including Nubank, C6 Bank, and Creditas that have rapidly expanded personal credit access to previously underserved consumer segments.

Market Dynamics

Growth Drivers: Rising consumer debt, expanding digital lending platforms, and AI-based underwriting technologies are driving growth in the personal loan market.

The primary structural growth drivers for the personal loans market are the substantial and in most major markets persistently growing aggregate consumer credit card debt that creates ongoing demand for debt consolidation personal loans whose lower interest rates and fixed repayment schedules provide measurable financial benefit to credit card balance carriers who qualify for refinancing, combined with the digital lending platform revolution that has made personal loan application, approval, and funding accessible within minutes rather than days through mobile interfaces that eliminate the documentation friction and branch visit requirements that historically made personal loans considerably more burdensome to obtain than credit card limit increases or cash advances. The expansion of AI-powered alternative credit assessment to consumer segments that traditional bureau score-based underwriting would decline, including gig economy workers with variable income, recent immigrants with limited credit file depth, young adults with thin credit histories, and recently unemployed borrowers with strong prior credit records, is enlarging the addressable personal loans market by bringing creditworthy consumers within the bankable population that can access unsecured personal credit.

Restraints: Rising interest rates, increasing credit default risks, and stricter lending regulations are limiting market growth and lender profitability.

A significant restraint on the personal loans market is the sensitivity of personal loan demand to the interest rate cycle, where rising benchmark rates that translate directly into higher personal loan pricing can reduce the debt consolidation value proposition for borrowers who acquired credit card debt at lower rate environments, making the interest differential between personal loan and credit card rates less compelling and reducing the pool of borrowers for whom consolidation refinancing delivers meaningful savings. Credit quality deterioration risk in economic downturns represents a structural restraint on personal lending expansion, as unsecured personal loans lack collateral protection against default-related loss, making personal loan portfolios systematically more sensitive to unemployment increases, income disruption, and recession-related consumer financial stress than secured lending categories.

Opportunities: Embedded finance solutions, payroll-linked lending platforms, and green personal loan products are creating new growth opportunities in the market.

The embedded finance model, where personal loan origination is integrated directly into the digital platforms where consumers encounter the financial need that motivates borrowing, represents the most structurally significant distribution channel opportunity in the personal loans market, as platforms including home improvement marketplaces that embed contractor financing, healthcare payment platforms that offer medical expense instalment lending, and educational programme registration platforms that provide income-share agreements are demonstrating that personal credit demand captured at the point of need converts at dramatically higher rates than equivalent offers presented through standalone lending platform marketing. Earned wage access platforms that provide workers with access to earned but not yet paid wages between payroll cycles represent a complementary financial product that addresses short-term liquidity needs without the debt creation of traditional personal lending.

Recent Developments:

-

2025: SoFi Technologies reported continued growth in its personal loan’s origination volume, with AI-enhanced underwriting enabling approval of a broader credit spectrum than traditional bank competitors while maintaining credit quality metrics, and launched an enhanced mobile app experience incorporating personalized financial planning tools that position personal loan products within comprehensive financial wellness management.

-

2025: Upstart Holdings expanded its AI lending platform partnerships with additional bank and credit union lenders across the United States, reporting that its machine learning credit assessment model approved approximately 27% more loans at equivalent or better default rates compared with traditional FICO-based underwriting, demonstrating the alternative credit assessment value proposition that is driving bank technology partnership investment.

-

2025: LendingClub completed migration of its marketplace lending operations to a bank charter model following its Radius Bank acquisition, enabling direct balance sheet personal lending alongside its platform origination capabilities and providing access to lower-cost deposit funding that improves its competitive pricing position relative to non-bank fintech lending competitors.

Personal Loans Market Key Players

-

JPMorgan Chase & Co.

-

Bank of America Corporation

-

Wells Fargo & Company

-

Citigroup Inc.

-

SoFi Technologies Inc.

-

LendingClub Corporation

-

Upstart Holdings Inc.

-

Marcus by Goldman Sachs

-

Discover Financial Services

-

American Express Company

-

Avant LLC

-

Prosper Marketplace Inc.

-

Best Egg (Marlette Holdings)

-

OneMain Financial Group

-

PNC Financial Services Group

-

Earnest (Navient)

-

Nubank

-

Klarna Bank AB

-

Affirm Holdings Inc.

-

Funding Circle Holdings

Personal Loans Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 320.73 Billion |

| Market Size by 2035 | USD 813.0 Billion |

| CAGR | CAGR of 9.75% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Loan Type (Unsecured Loans, Secured Loans, Debt Consolidation Loans, Personal Lines of Credit) • By Loan Tenure (Short-term, Medium-term, Long-term) • By Lender Type (Banks, Credit Unions, Online Lenders, Non-Banking Financial Companies) • By Loan Purpose (Debt Consolidation, Home Improvement, Medical Expenses, Education, Travel & Leisure, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | JPMorgan Chase & Co., Bank of America Corporation, Wells Fargo & Company, Citigroup Inc., SoFi Technologies Inc., LendingClub Corporation, Upstart Holdings Inc., Marcus by Goldman Sachs, Discover Financial Services, American Express Company, Avant LLC, Prosper Marketplace Inc., Best Egg (Marlette Holdings), OneMain Financial Group, PNC Financial Services Group, Earnest (Navient), Nubank, Klarna Bank AB, Affirm Holdings Inc., and Funding Circle Holdings. |

Get in Touch