Personal Cloud Storage Market Report Scope & Overview:

The Personal Cloud Storage Market size is valued at USD 46.10 Billion in 2025 and is projected to reach USD 216.91 Billion by 2035, growing at a CAGR of 16.75% during 2026-2035.

The Personal Cloud Storage Market analysis highlights the growing adoption of secure, scalable, and user-friendly storage solutions driven by digitalization and data proliferation. Market growth is driven by increasing demand remote accessibility, data synchronization and privacy-oriented platforms.

Global individual data creation reached 10.2 zettabytes in 2024, with consumers storing 40% more photos, videos, and documents than in 2020 - driving demand for personal cloud storage

Market Size and Forecast:

-

Market Size in 2025: USD 46.10 Billion

-

Market Size by 2035: USD 216.91 Billion

-

CAGR: 16.75% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Personal Cloud Storage Market - Request Free Sample Report

Personal Cloud Storage Market Trends

-

Increasing integration of AI and automation enhances data organization, predictive storage management, and personalized user experiences in personal cloud systems.

-

Rising adoption of hybrid and multi-cloud models improves flexibility, data security, and cost optimization for personal storage users.

-

Growing demand for encrypted and privacy-focused storage solutions due to rising cyber threats and stringent global data protection regulations.

-

Expansion of mobile-first cloud storage platforms driven by smartphone usage and seamless cross-device synchronization needs among consumers.

-

Integration of blockchain technology ensures transparent, tamper-proof, and decentralized data management in personal cloud storage ecosystems.

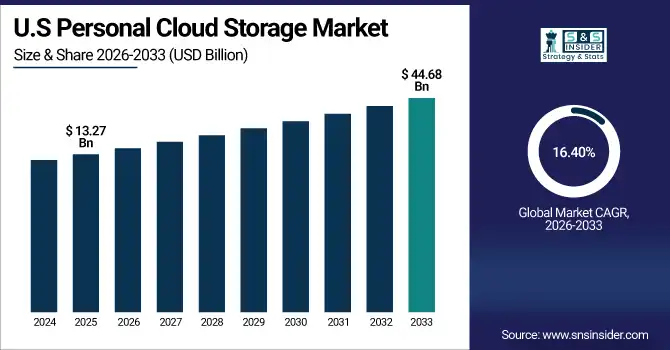

The U.S. Personal Cloud Storage Market size is valued at USD 13.27 Billion in 2025 and is projected to reach USD 60.59 Billion by 2035, growing at a CAGR of 16.40% during 2026-2035. Personal Cloud Storage Market is dominating by the high penetration of smartphones and generation of digital data. Self-hosted apps are getting popular but consumers want the flexibility of cloud based, secure, scalable and easy to access solution that they can use for both personal and professional purpose.

Personal Cloud Storage Market Growth Drivers:

-

Growing Data Generation and Rising Demand for Secure, Accessible Personal Storage Solutions

The surge of digital content from smartphones, IoT devices and smart home appliances drives the need for secure (yet flexible) local and remote personal storage solutions with anywhere access. Consumers demand easy access to data on all of their devices with AI-based backup and file management features. The prevalence of global personal cloud market has also increased amid rising digitalization, greater uptake of remote working and advent of multimedia sharing, which in turn stimulate continuous expansion.

In 2025, the average smartphone user created 2.5 GB of personal data per month, with photo and video content accounting for 70%, a behavior driving the consumption of cloud backup solutions.

Personal Cloud Storage Market Restraints:

-

Concerns over Data Privacy, Cybersecurity Risks, and Limited Internet Infrastructure in Developing Regions

Data breaches, hacking systems, and privacy issues are the reality that personal and business users must cope with. Without trust or regulatory concerns, many users would not feel comfortable storing sensitive personal or financial data on a server not operated by themselves. Furthermore, the adoption of cloud-based storage is low in areas with insufficient access to broadband or poor internet connections. These cyber vulnerabilities and digital infrastructure inequities are stifling global market expansion, specifically in developing markets where digital maturity is far from achieving its potential.

Personal Cloud Storage Market Opportunities:

-

Integration of AI, Edge Computing, and Blockchain for Advanced Personal Cloud Ecosystems

Emerging technologies like artificial intelligence, blockchain, and edge computing are unlocking new growth opportunities in personal cloud storage. AI adds smart data classification, predictive file access and storage efficiency, blockchain increases security and transparency. For personal cloud users, real-time access and latency can be improved using edge computing. Combined, these breakthroughs are poised to transform storage efficiency, improve privacy and establish new subscription-based services with substantial market potential for stakeholders.

In 2025, 60% of leading personal cloud platforms (e.g., Google One, iCloud+) deployed AI to auto-delete duplicates, compress files, and predict backup needs - reducing user storage waste by 25%

Personal Cloud Storage Market Segment Analysis

-

By User Type, Individuals led the market with a 46.80% share in 2025, while Enterprises are projected to be the fastest-growing segment with a CAGR of 9.20%.

-

By Application, Photos & Videos dominated the market with a 41.50% share in 2025, whereas Documents are expected to witness the fastest growth at a CAGR of 8.80%.

-

By End-User, Smartphones & Tablets accounted for the largest share at 49.60% in 2025, while Smart TVs are anticipated to register the highest growth rate with a CAGR of 9.10%.

-

By Storage Type, Primary Storage held a 44.30% market share in 2025, and Archive Storage is likely to expand the fastest with a CAGR of 8.60%.

-

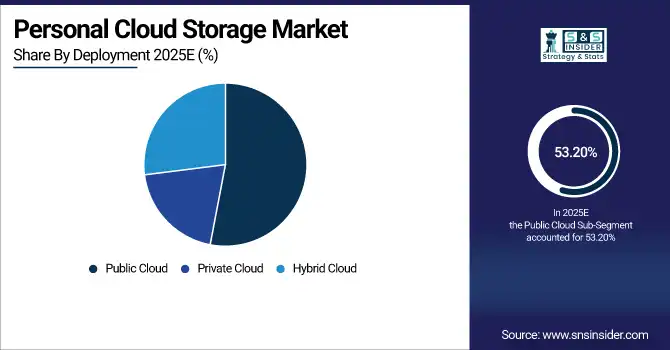

By Deployment, the Public Cloud segment led with 53.20% share in 2025, while the Hybrid Cloud segment is projected to grow the fastest at a CAGR of 9.40%.

By User Type, Individual Leads Market While Enterprises Registers Fastest Growth

By User Type, individuals lead the personal cloud storage market in 2025, driven by growing smartphone usage, digital content creation, and increasing awareness of data backup solutions. Enterprises is expected to be the fastest growing as personal cloud service are becoming an integral part of the business as they store, manage and share data securely on a real-time basis. The move to hybrid work and the increasing demand for flexible collaboration tools also add to enterprise adoption. Both receive strong encryption, any-device syncing, and cost-effective subscription plan options that keep your experience smooth and storage needs low.

By Application, Photos & Videos Dominate While Documents Shows Rapid Growth

By Application, photos and videos dominate the market in 2025, supported by the rapid increase in multimedia creation using smartphones, digital cameras and social media. The need for a secure, simple way to store and instantly access personal media files worldwide is growing rapidly. At the same time, the documents segment is taking off as professionals and students increasingly stash vital files online for quick access and collaborative purposes. Also, the increasing penetration of productivity applications and documents management software solutions based on cloud platform adds in further growth prospects to this segment.

By End-User, Smartphones & Tablets Lead While Smart TVs Registers Fastest Growth

By End-User, smartphones and tablets lead the market due to the high volume of personal data generated daily from mobile apps, social media, and content creation. The increasing penetration of 5G networks and mobile-first cloud applications enhances real-time synchronization and storage. Smart TVs are registering the fastest growth as streaming services and connected entertainment ecosystems expand, requiring more personalized and cloud-linked storage for digital media access, downloads, and backups. This trend highlights the growing convergence between personal devices and cloud ecosystems.

By Storage Type, Primary Storage Lead While Archive Storage Grow Fastest

By Storage Type, primary storage leads the market in 2025, fueled by user preference for easily accessible, always-synced data solutions. Individuals and small businesses rely on personal clouds for daily data storage and instant retrieval. Archive storage is growing the most as users look for long-term data storage for large amounts of seldom- or never-accessed information. This growth is further accelerated with the cost-effective and scalable cloud offerings along with better compression technologies reducing dependence on physical storage but ensuring data security and availability.

By Deployment, Public Cloud Lead While Hybrid Cloud Grow Fastest

By Deployment, the public cloud segment is leading the personal cloud storage market, driven by cost-effectiveness, scalability, and availability of services provided by vendors such as Google Drive, Dropbox, iCloud. The public cloud is still perfect for people who don’t want the headache of secure, user-friendly and cost-efficient storage. Although, hybrid cloud is increasing the most due to increase in enterprise adoption; on-premises control integrated with cloud flexibility. This model supports better adherence, personalization and performance among professionals or corporations that handle sensitive extensive digital data.

Personal Cloud Storage Market Regional Analysis:

North America Personal Cloud Storage Market Insights

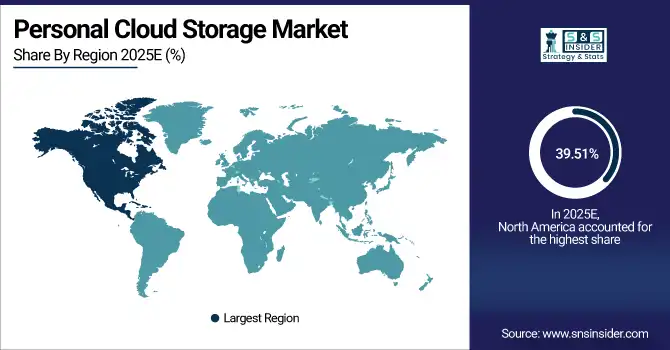

In 2025 North America dominated the Personal Cloud Storage Market and accounted for 39.51% of revenue share, this leadership is due to supported by advanced digital infrastructure, high consumer awareness, and strong adoption of subscription-based cloud platforms. The region benefits from major players like Google, Microsoft Amazon and Dropbox that wave a wider range of services. Smart devices and IoT applications contribute to the massive demand for data storage. Plus that’s something consumers are demanding more of solid, stable syncing between devices.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Personal Cloud Storage Market Insights

The U.S. remains the largest market for personal cloud storage, driven by a mature and technology adoption is early. Demand for storage is being driven by surging interest in remote work and digital content creation. Growth comes from high trust among users to manage data securely and flexible subscriptions.

Asia-pacific Personal Cloud Storage Market Insights

Asia-pacific is expected to witness the fastest growth in the Personal Cloud Storage Market over 2026-2035, with a projected CAGR of 17.35% due to rising smartphone adoption, increasing digitalization, and expanding internet infrastructure. Countries like India, Japan, and South Korea are key contributors. Affordable data plans and local cloud solutions enhance accessibility. Regional players are competing with global giants through customized offerings and language support.

China Personal Cloud Storage Market Insights

The personal cloud storage market in China is also growing rapidly, thanks to the massive use of smartphones and the roll-out of 5G services as well as the increasing generation of data from social media to e-commerce platform. Large providers, such as Tencent Cloud, Alibaba Cloud and Huawei, also have the edge with localised environments.

Europe Personal Cloud Storage Market Insights

In 2025, Europe emerged as a promising region in the Personal Cloud Storage Market, due to strong data protection laws under GDPR and high internet penetration. Consumers increasingly prefer European-based cloud services ensuring local data compliance. Adoption is driven by demand for secure file sharing, backup, and personal media management.

Germany Personal Cloud Storage Market Insights

Germany’s personal cloud storage market is characterized by strong data security awareness and preference for local cloud service providers. The country’s stringent data privacy regulations promote trust in domestic solutions. Growing remote work culture and increased cloud integration in education and business sectors drive usage.

Latin America (LATAM) and Middle East & Africa (MEA) Personal Cloud Storage Market Insights

The Personal Cloud Storage Market is experiencing moderate growth in the Latin America (LATAM) and Middle East & Africa (MEA) regions, due to the rising internet accessibility and smartphone adoption. Countries such as Brazil, Mexico, the UAE, and South Africa are key contributors. Increasing digital literacy and affordable data services are expanding user bases. Global players are entering partnerships with regional telecom providers to improve cloud accessibility.

Personal Cloud Storage Market Competitive Landscape:

AWS powers personal cloud storage through Amazon Drive and its robust cloud infrastructure. It provides users with scalable, secure, and flexible data management capabilities. The platform supports diverse personal storage needs, from backup to multimedia archiving. AWS leverages its vast global network to deliver fast and reliable data access. Its advanced encryption and affordability make it a preferred choice for millions of users worldwide.

-

In December 2024, AWS introduced new storage-class enhancements at its reinvent 2024 event, focused on improving cost efficiency, intelligent data tiering, and performance optimization for global cloud storage customers across enterprise, developer, and data-driven organizations.

Microsoft dominates the personal cloud storage space through its OneDrive platform integrated with Microsoft 365. The service allows users to store, sync, and share files securely across multiple devices. Its deep ecosystem integration enhances accessibility and productivity for both individuals and enterprises. Microsoft’s robust encryption and AI-driven organization tools add value to users’ storage experience. Its strong brand presence ensures continued market leadership and user trust.

-

In November 2024, Microsoft enforced new retail storage limits for Microsoft 365 users, effective November 13, reducing storage quotas across personal and business accounts. The move aimed to optimize storage management and encourage subscription upgrades for enhanced cloud capacity.

Oracle plays a pivotal role in the Personal Cloud Storage Market, leveraging its robust Oracle Cloud Infrastructure (OCI) platform. The company provides scalable, secure, and high-performance storage solutions catering to individuals, enterprises, and developers. Its cloud ecosystem integrates AI, analytics, and automation to optimize data management, enhance accessibility, and reduce operational costs. Oracle’s focus on hybrid and multi-cloud strategies positions it as a key enabler of digital transformation across industries.

-

In February 2025, Oracle launched Oracle Cloud Infrastructure (OCI) Data Storage Suite with advanced AI-driven optimization tools, providing faster data retrieval, lower latency, and better cost management for personal and enterprise cloud storage users worldwide.

Google’s Drive and Google One platforms are central to its dominance in personal cloud storage. The services offer unified, secure, and easy-to-access storage for documents, photos, and videos. Users benefit from seamless integration with Gmail, Android, and Workspace applications. Google emphasizes collaboration, enabling file sharing and real-time editing among users. Its global reach and affordable plans support strong adoption among individual and professional consumers.

-

In May 2025, Google partnered with Airtel to offer 100 GB of free Google One storage for six months to Airtel postpaid and Wi-Fi users, boosting user engagement and expanding its cloud subscription base in emerging markets.

Personal Cloud Storage Market Key Players:

Some of the Personal Cloud Storage Market Companies are:

-

Akamai Technologies

-

Microsoft

-

IBM

-

Edgio

-

Google

-

AWS

-

Amazon Web Services, Inc.

-

Hewlett Packard Enterprise Development LP

-

Oracle

-

RACKSPACE TECHNOLOGY

-

Dell Inc

-

Huawei Technologies Co., Ltd

-

Fujitsu

-

Hitachi Vantara LLC

-

ASUS Open Cloud

-

Citrix Systems, Inc.

-

Alibaba Cloud

-

VMware, Inc

-

Buffalo

-

Seagate Technology LLC

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 46.10 Billion |

| Market Size by 2035 | USD 216.91 Billion |

| CAGR | CAGR of 16.75% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By User Type (Individual, Professionals, Enterprises, and Educational Institutions) • By Application (Photos & Videos, Documents, Music, and Others) • By End-User (Smartphones & Tablets, Laptops & PCs, Smart TVs, and Others) • By Storage Type (Primary Storage, Backup Storage, and Archive Storage) • By Deployment (Public Cloud, Private Cloud, and Hybrid Cloud) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Akamai Technologies, Microsoft, IBM, Edgio, Google, AWS, Amazon Web Services, Inc., Hewlett Packard Enterprise Development LP, Oracle, RACKSPACE TECHNOLOGY, Dell Inc, Huawei Technologies Co., Ltd, Fujitsu, Hitachi Vantara LLC, ASUS Open Cloud, Citrix Systems, Inc., Alibaba Cloud, VMware, Inc, Buffalo, Seagate Technology LLC |

Frequently Asked Questions

North America dominated the Personal Cloud Storage Market in 2025.

The Primary Storage segment dominated during the projected period.

Growth is driven by rising data generation, increasing smartphone usage, and growing demand for secure, accessible, and scalable cloud storage solutions drive the Personal Cloud Storage Market.

The market is valued at USD 46.10 Billion in 2025 and is projected to reach USD 216.91 Billion by 2035.

The Personal Cloud Storage Market is expected to grow at a CAGR of 16.75% during 2026–2035.

Get in Touch