Pet Therapeutic Diet Market Report Scope & Overview:

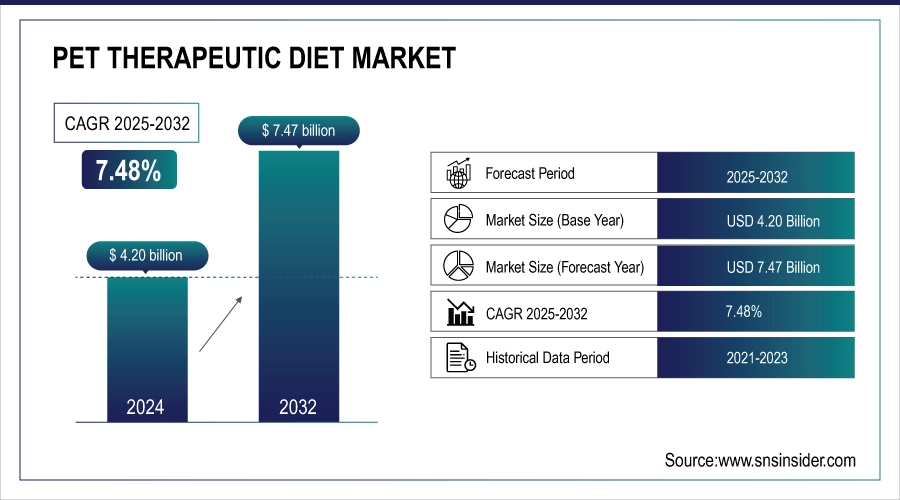

The pet therapeutic diet market was valued at USD 4.20 billion in 2024 and is expected to reach USD 7.47 billion by 2032, growing at a CAGR of 7.48% over the forecast period of 2025-2032.

To Get more information On Pet Therapeutic Diet Market - Request Free Sample Report

The global pet therapeutic diet market is driven by increasing inclination of pet owners toward pet preventive care and management of chronic diseases. As owners increasingly regard pets as family members, they spend on specialty diets designed for conditions including obesity and kidney disease. Educational efforts, veterinary advice, and access to telemedicine are behind this trend. The pet therapeutic diet market trends indicate an increasing demand for personalized nutrition, which is projected to be a consequence of elevated standards of pet care, preventive health management, and adoption of technology-driven veterinary care.

For instance, in May 2024, over 60% of the U.S. dogs and 55% of cats are obese, driving a 19% rise in therapeutic weight management diet sales.

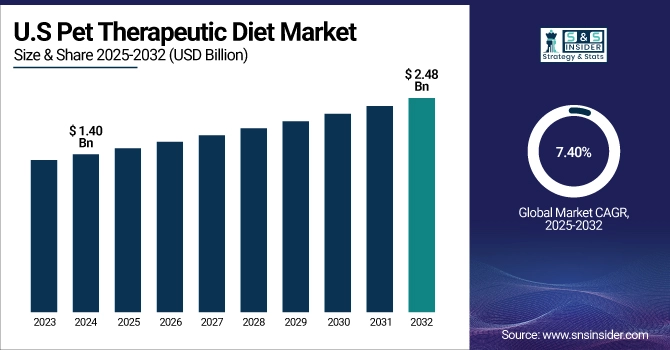

The U.S. pet therapeutic diet market was valued at USD 1.40 billion in 2024 and is expected to reach USD 2.48 billion by 2032, growing at a CAGR of 7.40% over 2025-2032.

The US has the largest pet health therapeutic diet market share as pet owners are led by veterinary practices through nutritional assessments and scientifically-based, responsible nutritional therapy options. And with some 93% of cat owners leaning on vets for advice, the veterinary profession is the biggest force driving demand for therapeutic and preventive diets. Its preventative attitudes to obesity, chronic disease, and changing dietary requirements have successfully propelled high penetration of therapeutic diets, with the U.S. being the world’s origin market for such products.

For instance, in February 2025, in the U.S., 68% of chronic disease consultations led to therapeutic diet recommendations by veterinarians, highlighting their pivotal role in clinical nutrition guidance.

Market Dynamics:

Drivers:

- Nutrition Is a Major Driving the Pet Therapeutic Diet Market Growth

The pet therapeutic diet market share is driven by a need for nutrition that supports preventive pet healthcare, which can help manage chronic ailments, improve immunity, and promote long life. Personalized diets can address obesity, allergies, and digestion-related problems, as demands for personalized care rise. As veterinarians recommend proactive nutrition, the pet therapeutic diet market grows as pet owners add health-oriented, preventive dietary choices to their sales.

For instance, in April 2025, APPA reported that 72% of U.S. pet owners choose therapeutic diets for chronic conditions, driving a significant rise in preventive nutrition-focused pet food sales.

Restraints:

- Competition Over Homemade Diets is a Significant Restraint on the Pet Therapeutic Diet Market Growth

Homemade diets also pose competition for the pet therapeutic diet market growth as many of the pet owners consider homemade diets to be healthier and natural. Nevertheless, homemade diets are still primarily preferred although they are nutrient-deficient and potentially contaminated because of myths, mistrust of commercial foods, and wish for ingredient control. This impression limits the acceptance of science-based therapeutic diets targeting chronic disease, and the expansion of the market for these therapeutic diets, although known to improve health.

For instance, in February 2025, ACVN reported 28% of U.S. pet owners use homemade diets, with 60% nutritionally inadequate, hindering pet therapeutic diet market adoption.

Segmentation Analysis:

By Product

Dry Food is the dominant and fastest growing segment in the global pet therapeutic diet market, with a 65.26% market share in 2024, owing to its long shelf life, easy storage, and thrifty convenience to pet owners. It facilitates accurate nutrient formulation for the treatment of diseases including obesity, diabetes, and renal disease. Furthermore, dry kibble promotes dental care and is well received by veterinarians. Its lower cost of production and extensive retail and hospital distribution all helped to establish its dominance in the space of pet therapeutic diets.

By Animal Type

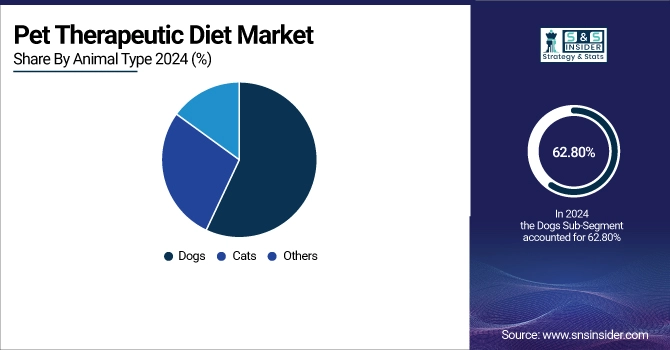

In 2024, the dogs dominated the pet therapeutic diet industry with a 62.80% market share, owing to the large number of dogs globally and increasing knowledge about canine health problems, including obesity, joint disease, and kidney disease. Therapeutic diets for the management of these disorders have become the diet of choice for many pet owners. Veterinary endorsement and the emotional bond between owners and dogs are other factors that bring demand for preventive care, positioning dogs as the leading consumer segment in the therapeutic pet nutrition market.

The cats segment is the fastest growing aspect of the pet therapeutic diet market analysis, with A CAGR of 8.01% over the forecast period, driven by the growing number of cat owners, higher prevalence of cat-specific diseases, including renal disease, urinary tract diseases, and later on, more knowledge on customized nutrition for cats. Pet parents are searching for specific diets to help manage chronic conditions, and more veterinarians recommend therapeutic foods, driving adoption in the growing feline healthcare category.

By Indication

Obesity Care held a dominant pet therapeutic diet market share of 20.89% of the pet therapeutic diet market industry in 2024. Driven by the increasing percentage of overweight pets, or dogs, especially. Demand for weight management diets is driven by rising awareness of health conditions associated with obesity, including joint pain, diabetes, and heart disease. Veterinarians commonly recommend weight management therapeutic foods, which drive the long-term health of pets and drive the segment growth significantly.

Renal Care is emerging as the fastest growing segment in the pet therapeutic diet industry with the highest CAGR of 8.16%, propelled by increased cases of chronic kidney disease in older pets. The demand for renal-specific nutrition is mainly fuelled by early and accurate diagnosis and growing veterinary assistance. Such targeted dietary interventions support longevity and management of symptoms, playing a major role in the pet therapeutic diet market growth as owners seek effective, long-term nutritional solutions for chronic conditions, including kidney disease.

By Distribution Channel

Veterinary hospitals & clinics are the largest segment of the pet therapeutic diet industry, offering greater use of veterinarian-prescribed nutrition for disease treatment. Pet parents believe in the clinical efficacy of condition-specific diets and are more compliant. Nutritional therapy through this channel is precise, fortifying its leading position and strongly contributing towards the overall distribution of the market share.

The E-commerce segment is witnessing the highest growth in the pet therapeutic diet market, fuelled by the growing digital adoption, ease of home delivery, and wider product assortment. Online purchasing of therapeutic diets is becoming more popular with pet owners for repeat purchases. Subscription services and the availability of vet-approved diets at competitive prices add to this growth, expanding reach and access to the pet therapeutics diet market in a meaningful way.

Regional Analysis:

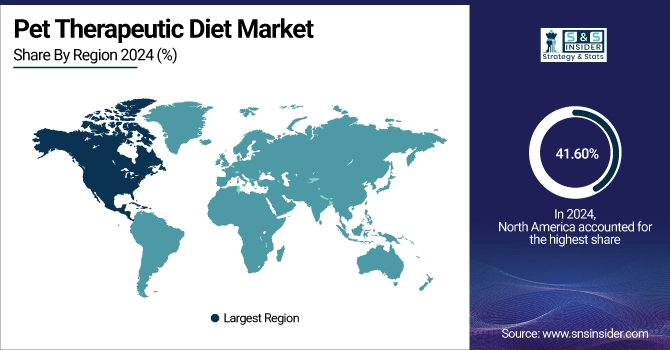

In 2024, the North American region holds the largest market share of the pet therapeutic diet industry and dominates the market with a 41.60% market share, owing to the large pet population, education regarding pet health, and a solid veterinary infrastructure. High demand is also fuelled by the region’s mature pet care industry and increasing prevalence of long-term conditions including obesity and kidney problems in pets, combined with the ready availability of therapeutic diets. Furthermore, premiumization of pet food, increased e-commerce penetration, and the advent of proactive pet parenting also drive market growth. Strong presence of the key players also serves to augment the dominance of North America in the pet therapeutic diet market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe is the second-largest market for the global pet therapeutic diet market as owners become more conscious of their pets’ health, are visiting the vet more, and looking for specialized food. Countries including Germany, France, and the UK lead the way in terms of pet adoption and spending. Rising adoption of preventive pet healthcare, high-end pet food products, and government initiatives for animal welfare change the dynamics of the region in the pet therapeutic diet market

Asia-Pacific emerges as the fastest-growing region with the highest CAGR of 8.28%, driven by growing pet ownership, higher disposable incomes, and rising awareness on companion animal health. Urbanisation in countries including China, India, Japan, and South Korea has contributed to a rise in nuclear families rearing pets, particularly dogs and cats. Demand is also rising for therapeutic diets that address obesity, renal problems, and allergies, as more pet owners are informed about prevention. Moreover, broadening veterinary base, emergence of pet e-commerce platforms, and increased penetration of western pet care trends are fuelling the growth of the market. Adoption of government policies for animal welfare, and rising popularity of premium international brands, are the major drivers of the pet therapeutic diet market in the Asia-Pacific.

The Middle East & Africa has the least pet therapeutic diet market share and is attributed to less pet ownership, poor knowledge of pet nutrition, and the nascent status of the veterinary healthcare industry. Economic limitations and cultural constraints limit the use of specialized pets’ diets. Strict regulations for veterinarians, coupled with the shortage of drugs and less awareness about animal health, are some of the restraining factors for the growth of the market in this region.

The pet therapeutic diet market in Latin America is estimated to have a moderate share due to urbanization, increasing penetration of pets, and awareness of pet health. Demand for specialized diets is growing in countries including Brazil and Mexico, where veterinary care is on the rise. However, progress is hindered by disparities in income, erratic product availability, and much weaker penetration by premium therapeutic brands than in North America and Western Europe. Yet the region has been demonstrating consistent potential.

Key Players

Pet therapeutic diet Companies, including Hill’s Pet Nutrition, Royal Canin, Purina Pro Plan Veterinary Diets, Blue Buffalo, Farmina Vet Life, Rayne Clinical Nutrition, Virbac, Dechra, IAMS Veterinary Formula, VetDiet, Veterinary Diet Solutions, Balance IT, JustFoodForDogs, Nom Nom, SquarePet, Petcurean, Trovet, Animonda, Vetnova, Affinity Petcare, and other players.

Recent Developments

-

In February 2025, Hill’s launched Prescription Diet Derm Complete in February 2025, targeting chronic skin issues in pets. It uses bioactives and Omega-3s to reduce allergic flare-ups and support skin health.

-

In January 2025, Blue Buffalo reformulated GI Gastrointestinal Support dog food with enhanced digestibility, natural ingredients, and antioxidant fibers to better manage digestive disorders and promote gut health.

-

In April 2025, Virbac expanded its Veterinary HPM diet range with a new Obesity Management formula for dogs, aiming to improve weight loss outcomes through high-protein, low-carb nutrition.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 4.20 billion |

| Market Size by 2032 | USD 7.47 billion |

| CAGR | CAGR of 7.48% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Wet Food, Dry Food, Others) • By Animal Type (Dogs, Cats, Others) • By Indication (Renal Care, Obesity Care, Diabetic Care, Dental Care, Gastrointestinal Care, Recovery Care, Joint Care, Others) • By Distribution Channel(E-commerce, Veterinary hospitals & clinics, Retail Pharmacies, Others)" |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Hill’s Pet Nutrition, Royal Canin, Purina Pro Plan Veterinary Diets, Blue Buffalo, Farmina Vet Life, Rayne Clinical Nutrition, Virbac, Dechra, IAMS Veterinary Formula, VetDiet, Veterinary Diet Solutions, Balance IT, JustFoodForDogs, Nom Nom, SquarePet, Petcurean, Trovet, Animonda, Vetnova, Affinity Petcare and other players. |

Get in Touch