Petroleum Sorbent Pads Market Report Scope & Overview:

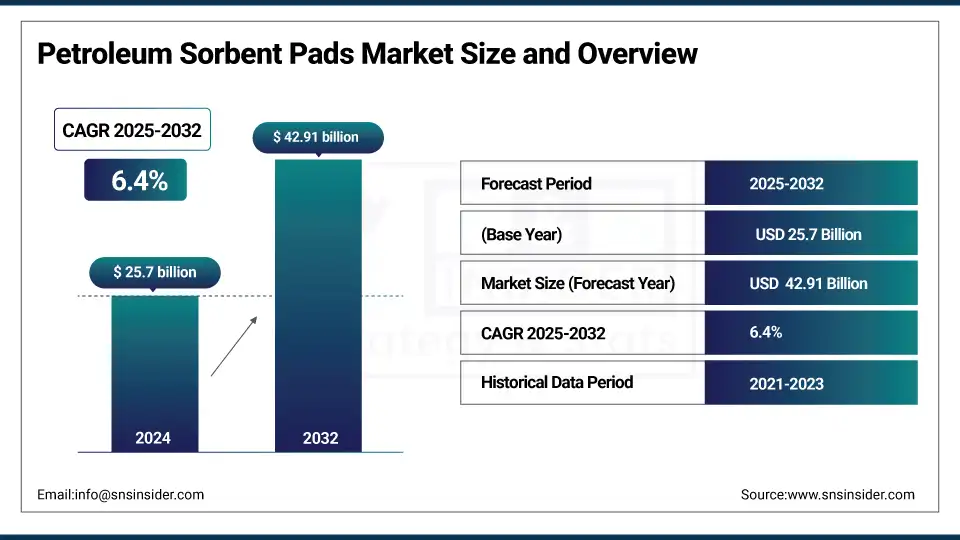

The Petroleum Sorbent Pads market size was valued at USD 25.7 billion in 2024 and is expected to reach USD 42.91 billion by 2032, growing at a CAGR of 6.4% over the forecast period of 2025-2032.

Rising environmental legislation, growing industrial spill occurrences, and surging demand for sustainable oil sorbent pads and industrial sorbent pads are the key factors driving the petroleum sorbent pads market. Oil Absorbent Pads manufacturers are focusing on smart absorbent technologies and creating biodegradable spill cleanup absorbents for effective and regulatory compliance. The petroleum sorbent pads market is set to witness steady growth, driven by increasing use of natural-fiber pads on the open sea and custom-engineered pads at refineries, according to a new report.

To Get more information On Petroleum Sorbent Pads Market - Request Free Sample Report

Oil facilities are required to comply with the spill prevention control under the U.S. EPA SPCC (Spill Prevention Control and Countermeasure) rule, which will enhance the petroleum sorbent pads market size. 3M’s 2025 Global Impact Report reports the addition of new recycled-content pads, and New Pig introduced its PIG Barrel Top Mat for drum spills. These trends are dictating terms in terms of the petroleum sorbent pads market share and remain consistent across the petroleum sorbent pads industry, while petroleum sorbent pads market dynamics trends favour safety, performance, and sustainability.

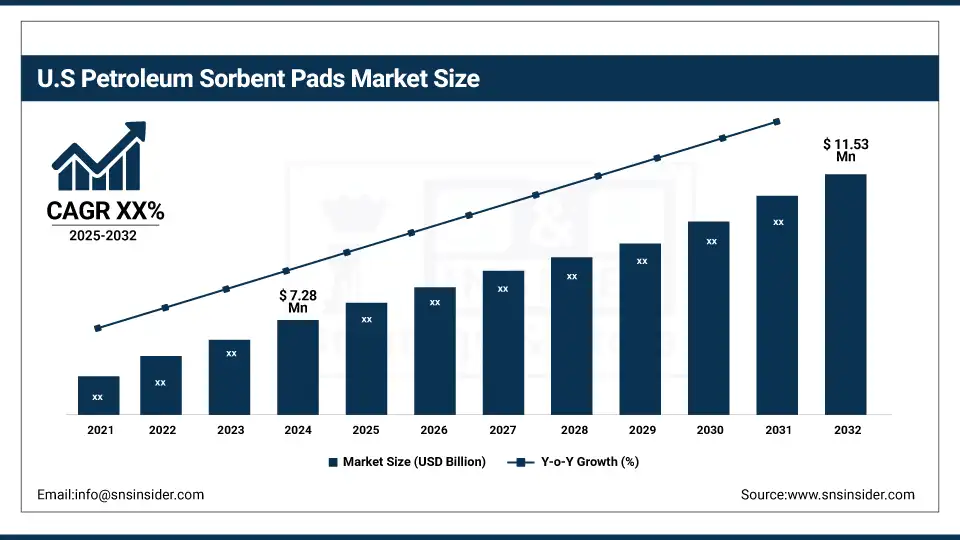

The U.S. is the largest contributor within North America, with a market size of USD 7.28 million in 2024 and is projected to reach a value of USD 11.53 million by 2032, with a market share of about 63%. This domination is driven by its huge energy industry and its power of regulation. The U.S. Coast Guard’s National Response Center lists more than 8,000 oil spill incidents that occur each year, so the importance of quality oil sorbent pads cannot be understated. Agencies such as the Bureau of Safety and Environmental Enforcement (BSEE) require stringent spill prevention controls on offshore rigs and refineries. Top U.S.-based petroleum sorbent pads manufacturers increase capacity to support these requirements in keeping with petroleum sorbent pads market trends for heavy-duty, high-absorbent industrial sorbent pads.

Market Dynamics:

Drivers:

- Increasing regulatory compliance for spill prevention fuels the petroleum sorbent pads market growth

Heavy regulations such as the U.S EPA SPCC rule demand that oil storage facilities demonstrate efficient spill control, which in turn fosters the petroleum sorbent pads market growth. Petroleum sorbent pads suppliers are offering green and highly efficient oil sorbent pads and industrial sorbent pads. Regulatory enforcement promotes usage, which is a favorable factor driving the petroleum sorbent pads market size and share. This need for compliant spill cleanup absorbers is front and center with regard to the advancement of the oil sorbent pads industry

- Rising adoption of biodegradable oil sorbent pads enhances the petroleum sorbent pads market growth

Sustainability trends are driving demand for cellulose and natural fiber-based biodegradable petroleum sorbent pads. Oil sorbent pad manufacturers such as New Pig are creating more biodegradable spill cleanup absorbents to comply with environmental laws. The trend is promoting the growth of the petroleum sorbent pads market because users are selecting environment-friendly products. With the increasing relevance of sustainability across sectors, this trend is altering the industry landscape of the petroleum sorbent pads market size, and the petroleum sorbent pads industry size is getting renewed focus on eco-friendly products.

Restraints:

- Competition from reusable and mechanical spill control systems restricts the petroleum sorbent pads market growth

Mechanical spill containment and the use of reusable pads are aiding in reducing the dependence on single-use petroleum sorbent pads. Refineries and other facilities using skimmers and booms are reporting a 25% reduction in absorbent pad use, the U.S. Department of Energy says. These options provide cost benefits over time, and less waste is created, reducing the usage of traditional spill cleanup absorbents. This transition restricts the market size of petroleum sorbent pads, especially for mature or capital-intensive industrial sectors.

Segmentation Analysis:

By Product Type

Lightweight pads dominated in 2024 with a market share of 45.57%. Their popularity depends on them being relatively inexpensive and able to rapidly absorb oil in industrial and commercial spill-prone areas. The SPCC (Spill Prevention, Containment, and Countermeasures) regulations of the U.S. Environmental Protection Agency (EPA) establish that petroleum sorbent pads be included in the spill response plans, utilizing lightweight sorbent pads that are more convenient and perform well. Their applicability and wide application in manufacturing and utilities justify their prominent share in the petroleum sorbent pads market, ensuring a strong petroleum sorbent pads market share and continued petroleum sorbent pads industry penetration.

Mediumweight pads are the fastest growing with a CAGR of 7.48%. This growth is primarily due to the growing penetration in the logistics terminals, municipal utilities, and warehouse applications that require medium absorption with increased fold endurance. The US Department of Energy also says mediumweight pads accomplish better performance in a continuous leak scenario than lighter pads. These pads are suitable for facilities, which are following the spill prevention plan, which is anticipated to serve as one of the key factors for the significant growth of the petroleum sorbent pads market and their place in the petroleum sorbent pads market trends.

By Material

Synthetic materials dominated in 2024 with a market share of 68.17%. Artificial petroleum sorbent pads, especially those of polypropylene, provide excellent oil-only absorbency, long storage life, and low water retention, such that it is well-suited for marine docks, oil platforms, and pipeline spill areas. According to the U.S. Department of Energy, this material is widely used in emergency spill intervention kits. These traits have made synthetic pads industry benchmarks, reaffirming their leadership in the petroleum sorbent pads market by geography and the petroleum sorbent pads market trends.

Organic materials are the fastest growing with a CAGR of 7.55%. Organic-based petroleum sorbent pads from cotton, kenaf, and cellulose are increasing in popularity because of sustainability requirements, particularly the USDA BioPreferred Program. Federal and city procurement of environmentally friendly goods is helping that occur. These pads biodegrade for less environmental impact and lower disposal cost. With environmental protection gaining significance and zero-waste operations gaining momentum, companies in the petroleum sorbent pads market are developing ecologically sound products, in line with the overall growth trend in the petroleum sorbent pads market and changing regulations.

By Absorbency

Medium absorbency pads dominated in 2024 with a market share of 51.56%. Their balanced cost-to-performance ratio and widespread use in general-purpose industrial maintenance have cemented their leading market position. According to the Occupational Safety and Health Administration (OSHA), medium absorbency petroleum sorbent pads are most suitable for daily maintenance in factories, auto shops, and refueling zones. They support quick response to mid-range spills and minimize material waste. As industrial facilities adopt standardized spill kits, medium absorbency continues to lead the petroleum sorbent pads market trends and usage across sectors.

High absorbency pads are the fastest growing with a CAGR of 7.41%. High absorbency petroleum sorbent pads are gaining demand across offshore platforms, fuel depots, and chemical plants due to their capacity to control large-volume spills. The U.S. Coast Guard requires high-capacity absorbents for oil containment booms and vessel-based emergency kits. Their rapid oil saturation capacity ensures faster spill containment, improving safety compliance. This rising requirement, especially in coastal and heavy-industry applications, is accelerating the petroleum sorbent pads market growth across mission-critical environments with high environmental sensitivity.

By End-use

Oil & gas dominated in 2024 with a market share of 41.67%. The oil and gas sector continues to be the largest consumer of petroleum sorbent pads, driven by strict spill control mandates. The Bureau of Safety and Environmental Enforcement (BSEE) requires proactive oil spill response preparedness, making these absorbents a regulatory necessity. Upstream drilling sites and downstream refineries rely heavily on petroleum sorbent pads to manage operational hazards. Their high-frequency use in pipelines, storage tanks, and rig equipment contributes significantly to the petroleum sorbent pads market share in this sector.

Transportation & logistics is the fastest growing with a CAGR of 7.56%. Increased movement of petroleum products via ports, rail, and air transport has elevated spill risks, driving demand for petroleum sorbent pads in logistics. The U.S. Department of Transportation’s PHMSA regulations enforce absorbent use at fuel handling and hazardous transfer points. Terminal operators and fleet maintenance hubs are increasingly investing in spill cleanup absorbents for safety compliance. This segment's growth reflects evolving petroleum sorbent pads market trends across supply chains and global trade environments.

Regional Analysis:

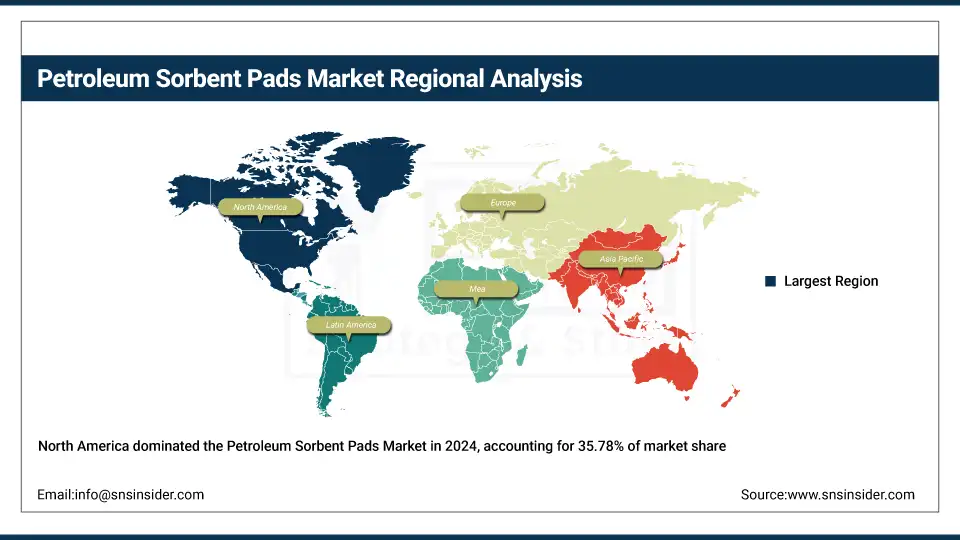

North America dominates the petroleum sorbent pads market with a 35.78% share, driven by the strict environmental & pollution control laws, including the U.S. EPA's Spill Prevention, Control, and Countermeasure (SPCC) rule. Its large oil & gas infrastructure and petrochemical industries consume huge quantities of spill cleanup absorbents for safety regulation compliance. Continuing petroleum sorbent pads market expansion, owing to extensive energy infrastructure modernization projects along with rising offshore drilling safety measures, is contributing to the market growth. These regulatory and industry drivers continue to support North America’s leadership over the petroleum sorbent pads market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific is the fastest-growing region in the petroleum sorbent pads market with a CAGR of 7.37%, driven by rising industrialization, port expansion, and stronger environmental policies. China and India are among the countries that are implementing strict measures to help prevent spills and protect the marine environment. The most vigorous enforcement comes from China's Ministry of Ecology and Environment (MEE), which mandates the use of oil sorbent pads at ports and industrial parks. The rising development of petrochemical plants and increasing offshore operations subsequently surge the industrial sorbent pads. The regional petroleum sorbent pads industry players are associated with the government sustainability goals that contribute to substantial product demand across logistics, marine, and energy sectors.

Key Players:

The major petroleum sorbent pads market competitors include 3M Company, New Pig Corporation, Brady Corporation (SPC), Oil-Dri Corporation of America, ENPAC LLC, Meltblown Technologies Inc., Chemtex, Sellars Absorbent Materials, Inc., Global Spill Control, and Darcy Products Ltd.

Recent Developments:

- In April 2025, FyterTech marked Earth Day by upgrading its Sustayn line to 90% recycled content with accelerated biodegradation technology, third‑party ASTM D5511 validation shows three‑times faster breakdown in landfill conditions, underscoring eco‑innovation in spill cleanup absorbents

- In February 2024, 3M inaugurated a new plastic‑recycling line at its Itapetininga, Brazil plant, enabling a significant increase in recycled content in its workspace solutions, now including sorbents supporting its sustainability targets and reducing virgin‑plastic use by 98.2 million pounds since 2021

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 647.73 million |

| Market Size by 2032 | USD 1,124.73 million |

| CAGR | CAGR of 7.14% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Product Type (Lightweight Pads, Mediumweight Pads, and Heavyweight Pads) •By Material (Organic, Inorganic, and Synthetic) •By Absorbency (High Absorbency, Medium Absorbency, Low Absorbency), •By End-use (Oil & Gas, Transportation & Logistics, Industrial & Manufacturing, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | 3M Company, New Pig Corporation, Brady Corporation (SPC), Oil-Dri Corporation of America, ENPAC LLC, Meltblown Technologies Inc., Chemtex, Sellars Absorbent Materials, Inc., Global Spill Control, and Darcy Products Ltd. |

Frequently Asked Questions

Key petroleum sorbent pad companies include 3M, New Pig, Brady, Oil-Dri, ENPAC, and Meltblown Technologies.

North America dominates the petroleum sorbent pads market, with Asia Pacific being the fastest-growing region.

Oil and gas, transportation, and manufacturing industries are key end-users in the petroleum sorbent pads industry.

Stringent regulations, rising spill incidents, and demand for biodegradable sorbents are fueling the petroleum sorbent pads market growth globally.

The petroleum sorbent pads market is valued at USD 647.73 million in 2024, growing at 7.14% CAGR through 2032.

Get in Touch