Pharmaceutical Isolator Market Report Scope & Overview:

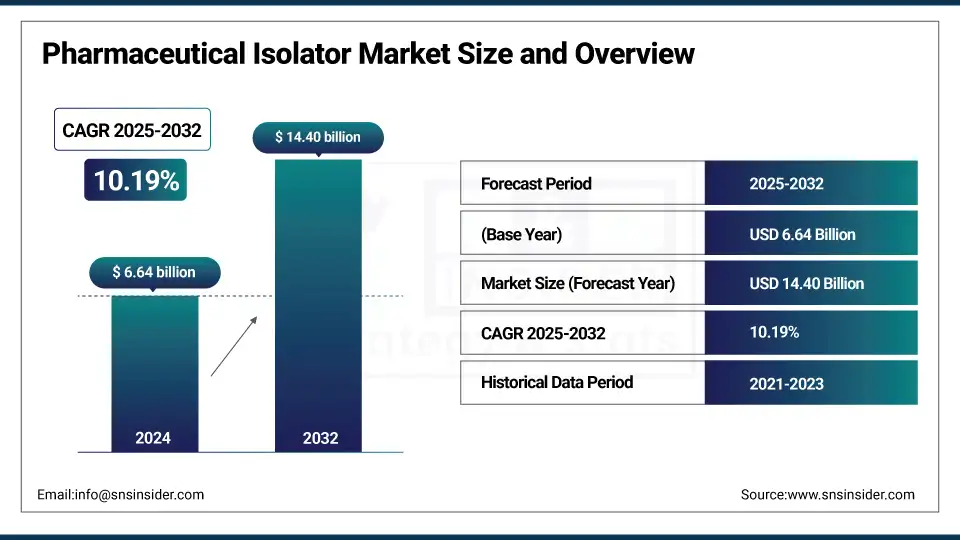

The pharmaceutical isolator market size was valued at USD 6.64 billion in 2024 and is expected to reach USD 14.40 billion by 2032, growing at a CAGR of 10.19% over the forecast period of 2025-2032.

The global pharmaceutical isolator market is poised for robust expansion, fueled by several key trends including a growing need for sterile manufacturing environments and heightened regulatory pressure to prevent contamination. Technological progress in isolators, such as gloveless and robotic isolators, is improving the process safety and efficacy. Biopharmaceutical and contract manufacturing sectors also boost the market. The expansion of GMP-compliant facilities and containment solutions aiming for increased overall production will drive solid growth in North America, Europe, and emerging markets in Asia-Pacific.

To Get more information On Pharmaceutical Isolator Market - Request Free Sample Report

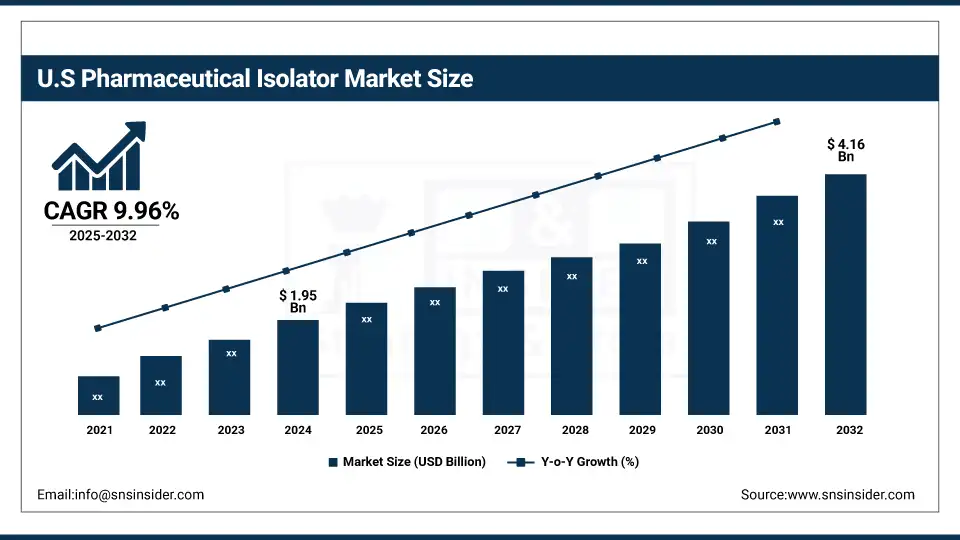

The U.S. pharmaceutical isolator market size was valued at USD 1.95 billion in 2024 and is expected to reach USD 4.16 billion by 2032, growing at a CAGR of 9.96% over the forecast period of 2025-2032.

North America is the largest pharmaceutical isolator market, with the U.S. accounting for more than two-thirds of the pharmaceutical isolator market in the region, attributed to well-established pharmaceutical manufacturing setups in the country and stringent compliance with the regulatory guidelines. Such high adoption by biopharma and contract manufacturers further solidifies the leading position of the country in the region.

Market Dynamics:

Drivers

-

Stringent Regulatory Requirements for Sterile Manufacturing are Fueling the Market Growth

Regulatory agencies heavily regulate pharmaceutical manufacture in order to maintain product safety and efficacy. Stringent guidelines have been issued by various regulatory agencies, including the U.S. FDA, European Medicines Agency (EMA), and World Health Organization (WHO), which makes aseptic processing, particularly for sterile injectable drugs, an important area of focus. Pharmaceutical isolators are designed to comply with these regulatory requirements by providing a physically closed, controlled environment to reduce human interaction and eliminate contamination. As they can maintain the interior environment within the isolator chamber at Grade A conditions, they offer a perfect solution for compliant sterile drug manufacturing, leading to their growth in demand across the industry.

The publication of EudraLex “Manufacture of Sterile Medicinal Products” by EMA promotes the use of advanced isolator and barrier systems for higher sterility assurance and lower patient risk.

Recently, the FDA has proposed a broader expansion of its oversight into compounding and contract manufacturing facilities, officially designating isolators built within them under cGMP specifications, perhaps similar to those imposed upon pharmaceutical manufacturers.

In a regulatory panel, FDA personnel reminded the audience that, even when isolators are used as a means to mitigate risk through contract manufacturing, installations will still be held to a higher bar when it comes to aseptic processing standards (ISPE Aseptic Conference, 2023, 18-20 Oct 2023).

-

The Market is Driven by the Increasing Demand for Sterile Pharmaceutical Products

The proactive rise in demand for sterile pharmaceutical products — partly due to the growing manufacturing of biologics, vaccines, and potent pharmaceutical products such as oncology medications — serves as a significant driving factor for the sterile injectable market. These are sensitive products and are produced in aseptic environments to maintain their safety and effectiveness. The production of these sterile products, which must be free of contaminants, therefore takes place in pharmaceutical isolators, enabling a contamination-free environment. The growing demand for isolation systems is also due to the expanding global demand for healthcare and the rising pharmaceutical isolator market.

Restraint

-

High Initial Capital Investment and Operational Costs Are Restraining the Market from Growing

The large initial capital investment and high running costs of pharmaceutical isolators are creating a significant restraint for the market. These systems entail significant capital investments for hardware, facility systems improvements, integration, and validation. Moreover, there are continuous and high costs of maintenance and energy, for replacing filters and for regular decontamination. These expenditures can be insurmountable for small- and mid-sized pharmaceutical companies, particularly those in emerging markets. Consequently, while isolators can offer better contamination control and compliance benefits, many firms are choosing less expensive options, such as restricted access barrier systems (RABS), which limit broader adoption of isolators.

Segmentation Analysis:

By Type

The closed isolators segment dominated the pharmaceutical isolator market share with 38.6% in 2024 on account of their better containment capabilities compared to other types, which help minimize human intervention and lower contamination risks during aseptic manufacturing processes. Such type of penetrations is popularly found in high containment pharmaceutical applications like sterile filling, handling of hazardous and potent compounds, and vaccine manufacturing using isolators. Due to the regulatory agencies such as the FDA and EMA's preference towards the systems that operate under strict environmental control, the higher uptake of closed isolators is witnessed in the mature phase of pharmaceutical manufacturing facilities, along with the contract development and manufacturing organizations (CDMO).

The bio isolators segment is projected to be the fastest-growing segment in the forecast years, owing to the growing need for sterility in biopharmaceutical production and research. The growing market presence of biologics, cell, and gene therapies is encouraging manufacturers to leverage bio isolators as they can ensure a high sterility assurance level for several critical processes. Moreover, mounting investment towards personalized medicine along with increasing biopharma R&D is likely to promote bio isolators application in small-batch, high-potency drug production and create new adoption avenues across emerging regions and dedicated factories.

By Application

The aseptic processing segment dominated the pharmaceutical isolator market, primarily due to its critical step in maintaining sterility of the product when drug manufacturing. Pharmaceutical isolators operate in a controlled environment and help minimize the chances of contamination of sterile drugs when filling, sealing, or compounding these drugs, an important process with injectable biologics and vaccines. Due to regulatory bodies highlighting that production must be contamination-free, especially for parenteral drugs, isolators have been widely accepted in aseptic workflows. Moreover, the growing trend of outsourcing sterile manufacturing to CDMO is also contributing to the growth of the isolators market in this segment.

Sterility testing is estimated to be the fastest-growing segment in the forecast period, owing to increasing requirements regarding quality control in the manufacturing of pharmaceutical and biopharmaceutical products. Drug manufacturers are under pressure to meet increasing global regulatory expectations, which has resulted in sterility testing being conducted with more intensity, especially in the case of advanced therapies and sensitive formulations. Compared to traditional cleanrooms, the better control and risk-free sterility testing environment that pharmaceutical isolators provide, tailored to compliance needs, promotes their use during various sterility testing.

By System Type

The modular systems segment held the largest share in the pharmaceutical isolator market with around 55.4% in 2024, and this is attributed to its high adaptability, scalability, and ease of integration in existing cleanroom environments. These systems have customizable configurations (aseptic filling, sterility testing, or compounding) based on the process, and so are more favorable with pharmaceutical manufacturers. Modular isolators enable easy upgrade while maintaining stringent standards, ensuring the facility runs cost-effectively and dependably.

Skid-mounted systems segment is expected to see the fastest growth through 2032, propelled by an upsurge in demand for plug-and-play, compact, and transportable systems for pharmaceutical manufacturing setups. The use of pre-engineered units ensures quick deployment and less time on site, thus more attractive to contract manufacturers and emerging pharma companies who are more focused on faster time-to-market. The trend of increased biologics production and personalized medicine has also created a demand for modular, flexible, and mobile isolator systems, which skid-mounted systems provide uniquely well.

By End User

Based on end-user, the pharmaceutical & biotechnology companies segment held the largest share of the 2024 pharmaceutical isolator market with 54.4% owing to high demand for maintaining aseptic conditions in drug manufacturing, particularly in sterile injectable production and biologics. To meet the high and stringent regulatory requirements of the FDA, EMA, etc., these companies invest heavily in advanced isolator technologies. Additionally, the growing emphasis on QA, risk mitigation, and prevention of cross-contamination of drugs in production processes has prompted many large pharmaceutical companies to accept isolator systems as the cleanroom standard, helping to solidify their position in the market.

On the other hand, the contract manufacturing organizations (CMOs) segment is expected to experience the fastest growth during the forecast period, owing to the trend towards cost-saving of outsourcing of pharmaceutical production, allowing for better scale-up scenarios. CMOs are enhancing their capabilities to secure partnerships with big Pharma and are thus making investments in state-of-the-art isolator systems to comply with global regulatory standards. This need for flexible, high-throughput, and contamination-free production systems is, in turn, fuelling the adoption of isolators within this segment, especially for both small-scale and personalized medicines.

Regional Analysis:

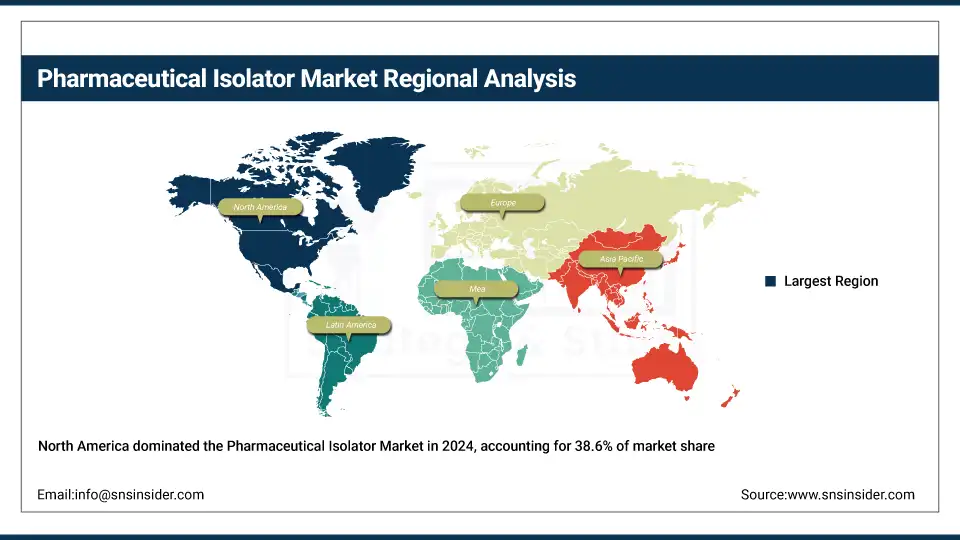

The North American region dominated the pharmaceutical isolator market trend with a 38.6% market share in 2024, owing to the solid pharma and biopharma industry and strict regulatory frameworks imposed by agencies such as the FDA. High levels of sterility and contamination control required by these regulations are stimulating the widespread adoption of isolator technologies. This further strengthens the position of North America in this market, owing to the number of contract development and manufacturing organizations (CDMOs) available in the region and dedicated investments in advanced manufacturing infrastructure.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific is expected to be the fastest-growing region due to growing pharmaceutical production, increasing investment in healthcare infrastructure, and a rising emphasis on compliance with regulations. Which, with China, India, and South Korea ramping up production for domestic and export needs. The increasing regulatory environment, coupled with government initiatives to support local production capabilities for pharmaceuticals and the growing trend of international players outsourcing manufacturing to Asia Pacific, is also expected to propel the growth of the pharmaceutical isolators market in the region.

Europe holds a major share of the pharmaceutical isolator market owing to stringent regulatory standards set by regulatory agencies, including the EMA and national health authorities. Such regulations drive high sterility and containment requirements in pharmaceutical manufacturing, which triggers the usage of isolator technology. Moreover, robust pharmaceutical industries already exist in Germany, the UK, France, and Italy, which are investing in advanced manufacturing solutions such as isolators. Furthermore, the region is witnessing an upward trend in isolator adoption as more biosimilars and personalized medicines are being produced in the region, along with the outsourcing of drug manufacturing to contract organizations.

The growth pharmaceutical isolator market in Latin America is gradual, propelled by increased active pharmaceutical ingredient (API) production capabilities and tightening regulatory expectations for aseptic markets.

MEA pharmaceutical isolator market analysis is moderate due to increasing infrastructure investment in healthcare, continued pharmaceutical production expansion (with a focus on Saudi Arabia, UAE, Egypt, and South Africa), and harmonization efforts that improve regional alignment of regulatory processes.

Key Players:

The pharmaceutical isolator market companies are SKAN AG, Getinge AB, Azbil Telstar S.L., Comecer S.p.A., Esco Micro Pte. Ltd., Fedegari Autoclavi S.p.A., Germfree Laboratories Inc., Hosokawa Micron Group, Jacomex, Syntegon Technology GmbH, Tema Sinergie S.p.A., Bioquell (An Ecolab Solution), Extract Technology Ltd., IsoTech Design, Block Engineering, Air Science USA LLC, Telstar Life Science Solutions, Weber Scientific, Labconco Corporation, NuAire Inc., and other players.

Recent Developments:

-

Getinge revealed on October 6, 2023, the release of ISOPRIME, a budget-friendly rigid-wall isolator specifically designed for typical aseptic processes. ISOPRIME is positioned as an entry-level option, introducing main aseptic processing features like a 4‑glove configuration, integrated Steritrace hydrogen peroxide decontamination, and FDA 21 CFR Part 11 compliance while maintaining traceability and simplicity of maintenance.

-

Telstar launched a dual-mode isolator system in March 2024 at Pharma Congress, Wiesbaden, which could perform both containment and aseptic mode. This versatile design responds to post-pandemic needs for flexible systems, allowing pharmaceutical companies to process multiple sterile operations with one single unit, reducing footprint, capital investment, and operating expense.

Pharmaceutical Isolator Market Report Scope:

Report Attributes Details Market Size in 2024 USD 6.64 Billion Market Size by 2032 USD 14.40 Billion CAGR CAGR of 10.19% From 2025 to 2032 Base Year 2024 Forecast Period 2025-2032 Historical Data 2021-2023 Report Scope & Coverage Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook Key Segments • By Type (Open Isolators, Closed Isolators, Glovebox Isolators, Containment Isolators, Bio Isolators, Sterility Test Isolators, Aseptic Isolators)

• By Application (Aseptic Processing, Sterility Testing, Containment, Mixing & Blending, Sampling & Dispensing)

• By System Type (Modular Systems, Skid-Mounted Systems, Floor-Mounted Systems)

• By End User (Pharmaceutical & Biotechnology Companies, Research Laboratories, Contract Manufacturing Organizations (CMOs), Academic & Research Institutes, Hospitals and Clinics)Regional Analysis/Coverage North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) Company Profiles SKAN AG, Getinge AB, Azbil Telstar S.L., Comecer S.p.A., Esco Micro Pte. Ltd., Fedegari Autoclavi S.p.A., Germfree Laboratories Inc., Hosokawa Micron Group, Jacomex, Syntegon Technology GmbH, Tema Sinergie S.p.A., Bioquell (An Ecolab Solution), Extract Technology Ltd., IsoTech Design, Block Engineering, Air Science USA LLC, Telstar Life Science Solutions, Weber Scientific, Labconco Corporation, NuAire Inc., and other players.

Frequently Asked Questions

North America dominated the Pharmaceutical Isolator Market in 2024.

The “Closed Isolators” segment dominated the Pharmaceutical Isolator Market.

Stringent Regulatory Requirements for Sterile Manufacturing are Fueling the Market Growth.

The Pharmaceutical Isolator Market was USD 6.64 billion in 2024 and is expected to reach USD 14.40 billion by 2032.

The Pharmaceutical Isolator Market is expected to grow at a CAGR of 10.19% from 2025 to 2032.

Get in Touch