Omics-Based Clinical Trials Market Report Scope & Overview:

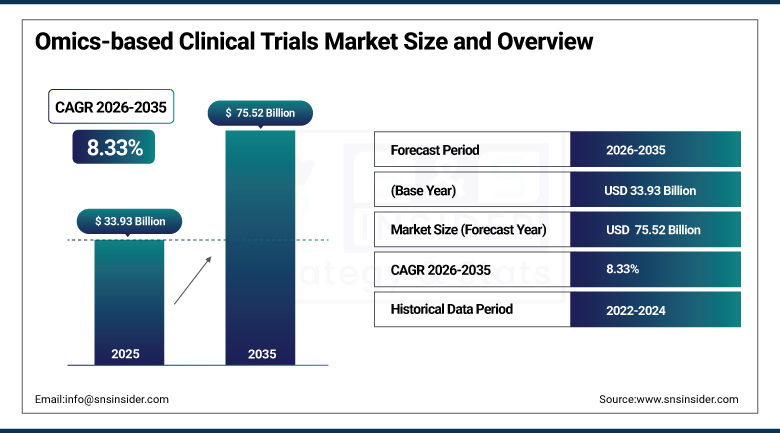

The Omics-Based Clinical Trials Market was valued at USD 33.93 Billion in 2025 and is expected to reach USD 75.52 Billion by 2035, growing at a CAGR of 8.33% from 2026 to 2035.

Omics-based clinical trials market is growing as a number of clinical trials are being conducted using genomic, proteomic, transcriptomic and metabolomic technologies in order to help in discovering biomarkers, conducting patient stratification and therapy optimization. There is continued growth in the need for personalized medicine which makes more and more pharma companies and biotech companies use multi-omics approach which enables them to match therapy with the right patient to avoid costly failure at the later stages and thus make drug development much faster and more clinically significant. Continued emphasis on translational research, growing government funding, availability of biobanks and advances like HiFi sequencing technology are some factors which are further aiding the transformation in the industry.

Bruker Corporation completed its acquisition of Biocrates Life Sciences in June 2025, a strategic move exemplifying industry consolidation aimed at enhancing multi-omics capabilities by enabling integration of metabolomics technologies and delivering more robust workflows for clinical research applications.

Market Size and Forecast

- Market Size in 2026E: USD 36.76 Billion

- Market Size by 2035: USD 75.52 Billion

- CAGR: 8.33% from 2026 to 2035

- Fastest Growing Region: Asia Pacific

- Largest Region: North America

To Get more information On Omics-based Clinical Trials Market- Request Free Sample Report

Omics-Based Clinical Trials Market Trends

- Rising adoption of multi-omics methodologies is letting researchers integrate genomic, proteomic, and metabolomic data within single trial designs.

- AI-enabled patient recruitment tools are improving trial enrollment efficiency and reducing time to first patient dosed.

- Growing regulatory acceptance of omics-based endpoints is expanding the range of trials that can incorporate molecular biomarkers.

- Expanding biobank availability is providing researchers with greater access to longitudinal molecular and clinical data.

- Increasing collaboration between pharmaceutical companies and academic institutions continues accelerating translational research capability.

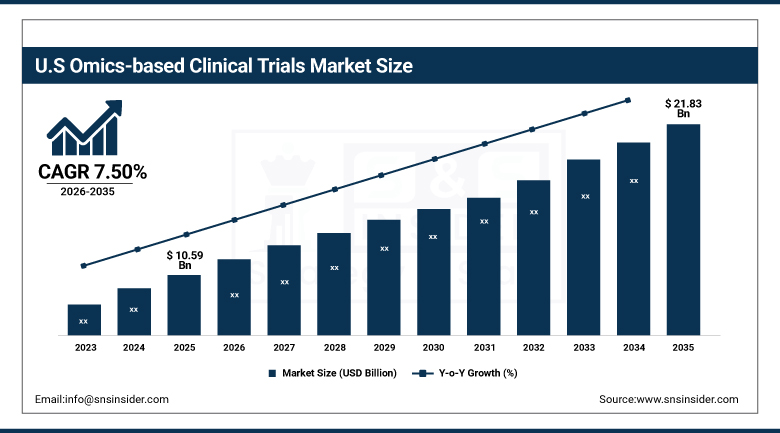

The United States Omics-Based Clinical Trials Market Outlook

The United States Omics-Based Clinical Trials Market was valued at USD 10.59 Billion in 2025 and is expected to reach USD 21.83 Billion by 2035, growing at a CAGR of 7.50% from 2026 to 2035.

The U.S. held a dominant position regarding omics-based clinical trials demand in North America owing to the presence of large pharma companies, advanced sequencing technologies, and increasing demand for omics-based clinical trials in cancer studies and rare disease research programs. The government funding towards research activities and academic-industry collaborations ensured that the U.S. remained one of the most commercially important national markets of the technology during the year.

In October 2024, Pacific Biosciences, whose company is based in Menlo Park, California, collaborated with A*STAR and Macrogen to set up a state-of-the-art genomics lab in Singapore using long-read HiFi sequencing technology for genomic analysis within the context of global clinical trial cooperation.

Omics-Based Clinical Trials Market Segment Analysis

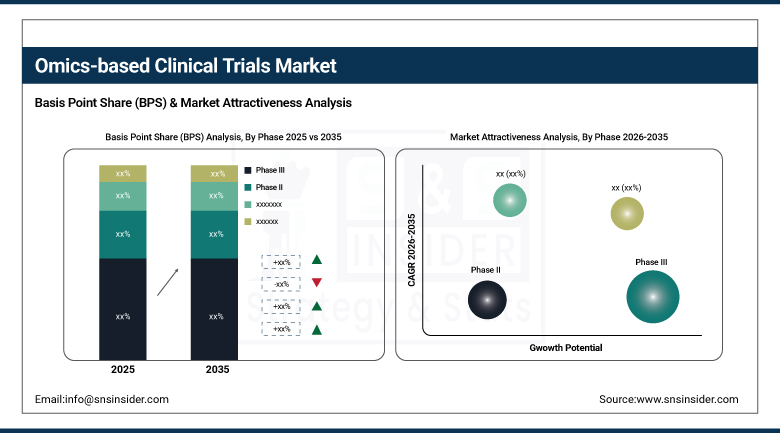

- By Phase, the phase III segment held approximately 54.50% share in 2025, while the phase II segment is the fastest growing.

- By Omics Type, the genomics segment held the largest share in 2025, while the multi-omics segment is the fastest growing.

- By Application, the oncology segment held the largest share in 2025, while the rare genetic diseases segment is the fastest growing.

- By End User, the pharmaceutical companies segment held the largest share in 2025, while the contract research organizations segment is the fastest growing.

By Phase, phase III led the market, phase II grew fastest

The phase III segment dominated the phase category in 2025, holding approximately 54.50% of total revenue, anchored by the large patient populations and extensive molecular profiling that late-stage confirmatory trials require to satisfy regulatory submission standards. That scale requirement continues keeping Phase III trials the largest single revenue contributor across the broader phase segmentation.

The phase II segment is projected to grow at the fastest CAGR during the forecast period, as sponsors increasingly incorporate omics-based biomarker strategies earlier in clinical development to identify likely responders before committing to expensive Phase III programs. Rising adoption of adaptive trial designs that use molecular data to refine patient selection continues pushing this phase category's growth rate ahead of the broader phase segmentation.

By Omics Type, genomics led the market, multi-omics grew fastest

The genomics segment held the largest omics type share in 2025, anchored by its established role as the foundational molecular profiling technology across the majority of biomarker-driven clinical trial designs. That foundational, well-validated technology base continues keeping genomics firmly at the top of the broader omics type segmentation across nearly every major disease indication.

The multi-omics segment is projected to grow at the fastest CAGR during the forecast period, as researchers increasingly integrate genomic, transcriptomic, proteomic, and metabolomic data within single trial designs to build a more complete molecular picture of disease and treatment response. Rising availability of integrated bioinformatics platforms capable of analyzing multiple omics layers simultaneously continues pushing this omics type category's growth rate ahead of the broader omics type segmentation.

By Application, Oncology led the market, Rare Genetic Diseases grew fastest

The oncology segment held the largest application share in 2025, reflecting the historically high levels of oncology trial activity and the field's early, sustained adoption of molecular biomarker-driven patient stratification. That established precision oncology infrastructure continues keeping this application category firmly at the center of overall omics-based clinical trial demand worldwide.

The rare genetic diseases segment is projected to grow at the fastest CAGR during the forecast period, as omics-based approaches increasingly prove essential for identifying the small, genetically defined patient populations that rare disease trials require. Growing regulatory acceptance of omics-based endpoints for orphan drug development continues pushing this application category's growth rate ahead of the broader application segmentation.

By End User, Pharmaceutical Companies led the market, Contract Research Organizations grew fastest

The pharmaceutical companies segment held the largest end-user share in 2025, anchored by sustained internal research and development investment in precision medicine programs across the industry's largest drug developers. That substantial internal R&D investment continues keeping pharmaceutical companies firmly at the top of the broader end-user segmentation across nearly every major omics-based trial program.

The contract research organizations segment is projected to grow at the fastest CAGR during the forecast period, as pharmaceutical and biotechnology sponsors increasingly outsource specialized omics data generation and bioinformatics analysis capability rather than building it entirely in-house. Rising demand for flexible, scalable omics trial support services continues pushing this end-user category's growth rate ahead of the broader end-user segmentation.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.90% |

|

Europe |

Germany |

27.20% |

|

Asia Pacific |

China |

35.60% |

|

Middle East & Africa |

UAE |

26.70% |

|

Latin America |

Brazil |

37.60% |

North America Omics-Based Clinical Trials Market Insights

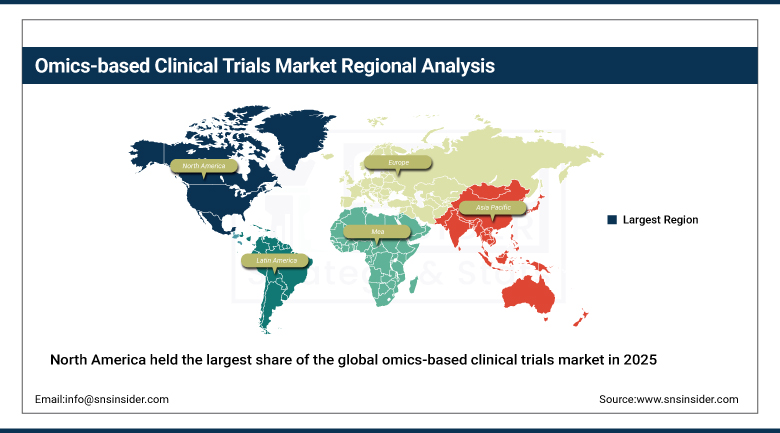

North America held the largest share of the global omics-based clinical trials market in 2025, at approximately 38.00%, attributable to the presence of major pharmaceutical companies, availability of advanced sequencing technologies, and rising demand for omics-based clinical trials across the region's largest research institutions. That combination of pharmaceutical industry concentration and technology infrastructure continued keeping North America firmly ahead of every other region in this market throughout the year.

The United States accounted for roughly 84.90% of regional revenue, reflecting its dense concentration of pharmaceutical companies, biotechnology firms, and academic research institutions conducting omics-based trials. The contribution of Canada to the regional income was lower yet increasingly steady owing to its growing research environment in genomics, ensuring that North America remained one of the most commercially viable regions for conducting omics-based clinical trials.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Omics-Based Clinical Trials Market Insights

Europe held a meaningful share of the global omics-based clinical trials market in 2025, anticipated to witness lucrative growth over the projected period, supported by strong academic research infrastructure and growing pharmaceutical industry investment in precision medicine across the continent. Germany accounted for roughly 27.20% of regional revenue, supported by its concentration of pharmaceutical companies and research institutions integrating omics technologies into clinical development programs.

France, the United Kingdom, and the Nordic countries followed a broadly similar trajectory, as continued academic-industry collaboration and biobank expansion extended omics-based clinical trial demand across the continent's largest research markets. Continued regulatory support for biomarker-driven trial designs is expected to keep supporting steady European demand through the remainder of the forecast period.

Asia Pacific Omics-Based Clinical Trials Market Insights

Asia Pacific was the fastest-growing region in the global Omics-Based Clinical Trials Market, driven by expanding genomics research infrastructure, growing pharmaceutical industry investment, and rising government support for precision medicine initiatives across the region's largest economies. Continued collaboration among global scientists and local institutions, alongside training programs and shared access to high-throughput sequencing infrastructure, continued fostering innovation and capacity-building throughout the region.

Asia Pacific represented nearly 35.60% of the total revenue in the region, driven by heavy investments in genomics research infrastructure by the governments along with capabilities within the pharmaceutical industry of the region. Japan and South Korea further boosted the regional demands from their genomics research and pharmaceutical production bases, which helped establish the dominance of the region in this market segment.

MEA & Latin America Omics-Based Clinical Trials Market Insights

The Middle East and Africa region recorded steady growth in omics-based clinical trials adoption in 2025, driven by expanding genomics research investment and growing government support for precision medicine initiatives across the Gulf states in particular. The UAE accounted for roughly 26.70% of regional revenue, supported by national genomics strategy investment and rising enterprise interest in precision medicine research infrastructure.

Latin America expanded at a comparable pace, led by Brazil at roughly 37.60% of regional revenue, where growing pharmaceutical research investment continued to support category growth. Mexico and Argentina followed a similar trajectory as regional clinical research infrastructure expanded further through the remainder of the forecast period.

Growth Drivers: Personalized medicine adoption and biobank infrastructure expansion

An increasing number of clinical trials incorporating omics technologies continues to be the central force behind omics-based clinical trials market growth, driven by heightened focus on translational research and rising government investments. Greater availability of biobanks continues providing researchers with expanded access to the longitudinal molecular and clinical data that biomarker-driven trial designs require.

The rising demand for personalized medicine, broader adoption of multi-omics methodologies, and expanding collaboration between biotech firms and research institutions continue reinforcing this structural growth trajectory. Innovations including HiFi sequencing technology continue revolutionizing data analysis in clinical trials, improving trial outcomes and reinforcing sustained demand growth across nearly every major disease indication worldwide.

Restraints: High technology costs and data integration complexity

The substantial cost of advanced sequencing and multi-omics profiling technology continues to restrict adoption among smaller biotechnology companies and academic research programs operating with constrained budgets. That cost barrier continues concentrating the most sophisticated omics-based trial capability among well-capitalized pharmaceutical companies and large contract research organizations.

Integrating genomic, transcriptomic, proteomic, and metabolomic data within a single coherent analytical framework continues posing genuine technical and bioinformatics challenges for trial sponsors. That data integration complexity continues requiring specialized bioinformatics expertise that not every research organization possesses in-house, adding cost and complexity to comprehensive multi-omics trial designs.

Opportunities: AI-enabled trial design and expanding biobank collaboration networks

Growing adoption of AI-enabled patient recruitment and trial design tools presents substantial opportunity for technology providers positioned to serve sponsors seeking more efficient enrollment and molecular-driven patient stratification. Providers capable of delivering genuinely predictive, AI-enhanced trial optimization tools stand to capture a growing share of demand as trial sponsors increasingly prioritize efficiency alongside scientific rigor.

Additional avenues for growth include continued expansion of international biobank partnership networks, which is demonstrated through genomics laboratories working in collaboration across borders. Companies that have the capability of developing these partnership networks will be able to create new sources of income as more omics trials will continue to take place in the coming years up until 2035.

Recent Developments:

- 2025: Thermo Fisher Scientific continued expanding its clinical sequencing and multi-omics analysis platform portfolio, strengthening its position serving pharmaceutical and biotechnology customers conducting biomarker-driven clinical trials.

- 2025: Illumina continued advancing its clinical genomics sequencing technology roadmap, targeting expanded adoption among contract research organizations and academic medical centers conducting omics-based trial programs.

- 2024: QIAGEN continued expanding its bioinformatics and molecular diagnostics platform capability, strengthening its position supporting biomarker discovery and patient stratification workflows across omics-based clinical trial programs.

Omics-Based Clinical Trials Market key players are:

- Pfizer Inc.

- F. Hoffmann-La Roche Ltd.

- Thermo Fisher Scientific Inc.

- Pacific Biosciences of California, Inc.

- Bruker Corporation

- Macrogen Inc.

- Illumina, Inc.

- QIAGEN N.V.

- Agilent Technologies, Inc.

- Bio-Rad Laboratories, Inc.

- Charles River Laboratories International, Inc.

- IQVIA Holdings Inc.

- Laboratory Corporation of America Holdings

- ICON plc

- Parexel International Corporation

- Syneos Health, Inc.

- Medpace Holdings, Inc.

- A*STAR

- Eurofins Scientific SE

- Twist Bioscience Corporation

Omics-Based Clinical Trials Market Report Scope :

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 33.93 Billion |

| Market Size by 2035 | USD 75.52 Billion |

| CAGR | CAGR of 8.33% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Phase (Phase III, Phase II, Phase I, Phase IV) • By Omics Type (Genomics, Transcriptomics, Proteomics, Multi-Omics) • By Application (Oncology, Rare Genetic Diseases, Neurology, Cardiovascular Diseases) • By End User (Pharmaceutical Companies, Biotechnology Companies, Contract Research Organizations) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Pfizer Inc., F. Hoffmann-La Roche Ltd., Thermo Fisher Scientific Inc., Pacific Biosciences of California, Inc., Bruker Corporation, Macrogen Inc., Illumina, Inc., QIAGEN N.V., Agilent Technologies, Inc., Bio-Rad Laboratories, Inc., Charles River Laboratories International, Inc., IQVIA Holdings Inc., Laboratory Corporation of America Holdings, ICON plc, Parexel International Corporation, Syneos Health, Inc., Medpace Holdings, Inc., A*STAR, Eurofins Scientific SE, Twist Bioscience Corporation |

Frequently Asked Questions

The Phase III segment held approximately 54.50% share in 2025.

North America held the largest share of the Omics-Based Clinical Trials Market in 2025, at approximately 38.00%.

Rising personalized medicine adoption combined with broader multi-omics methodology integration is the major growth factor.

The Omics-Based Clinical Trials Market was valued at USD 33.93 Billion in 2025.

The Omics-Based Clinical Trials Market is expected to grow at a CAGR of 8.33% from 2026 to 2035.

Get in Touch