Veterinary Surgical Instruments Market Report Scope & Overview:

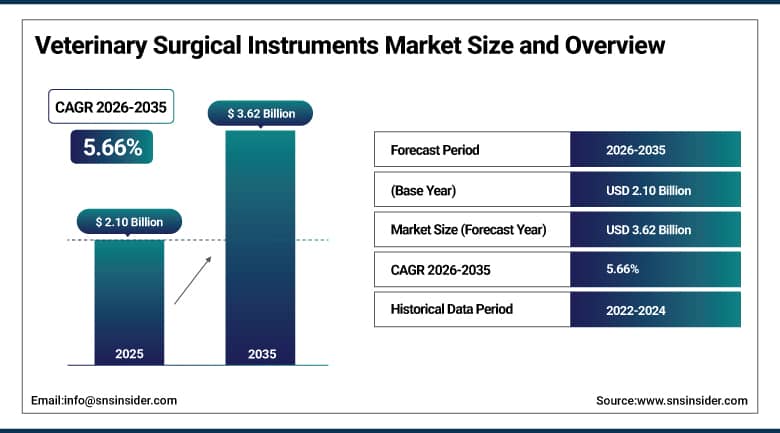

The Veterinary Surgical Instruments Market was valued at USD 2.10 Billion in 2025 and is expected to reach USD 3.62 Billion by 2035, growing at a CAGR of 5.66% from 2026–2035.

The global market of veterinary surgical instruments is expanding at a steady pace on account of increasing companion animal ownership, improved standards of care of animals, and increasing usage of surgical devices in veterinary practices. The range of veterinary surgical instruments includes manual tools such as forceps, scalpels, scissors, needle holders, and retractors, which form the basic set of tools required during any surgical operation, electrosurgery equipment used for hemostasis control, orthopedic implants used for bone fractures treatment, ophthalmology equipment, and dental tools for companion animal dentistry.

In 2024, IDEXX Laboratories partnered with several leading veterinary surgical instrument manufacturers to integrate pre-surgical diagnostic data directly into surgical planning workflows, enabling veterinarians to access real-time patient haematology, biochemistry, and imaging data during instrument selection and surgical preparation.

Market Size and Forecast

-

Market Size in 2026E: USD 2.22 Billion

-

Market Size by 2035: USD 3.62 Billion

-

CAGR: 5.66% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Veterinary Surgical Instruments Market - Request Free Sample Report

Veterinary Surgical Instruments Market Trends

-

Minimally invasive veterinary surgery adoption is increasing as laparoscopic, thoracoscopic, and arthroscopic procedures improve recovery outcomes and create demand for advanced surgical instruments

-

Veterinary orthopaedic specialization is expanding with growing use of complex procedures such as joint replacements and fracture repairs, driving demand for specialized surgical tools and implant systems

-

Companion animal dental surgery is gaining importance as awareness of periodontal disease rises, increasing the need for dental extraction and periodontal treatment instruments

-

Disposable and single-use surgical instruments are witnessing greater adoption as veterinary clinics focus on infection control, operational efficiency, and sterilization cost reduction

-

Telemedicine-assisted veterinary surgery is improving access to specialist expertise by enabling real-time remote guidance for complex procedures in rural and underserved locations

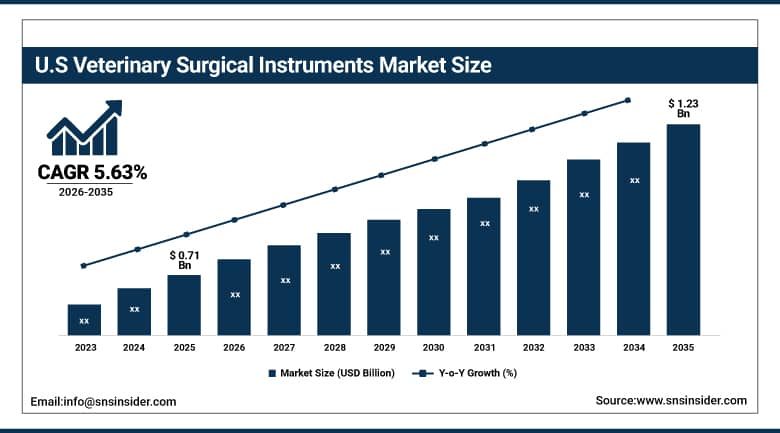

U.S. Veterinary Surgical Instruments Market Outlook

The U.S. Veterinary Surgical Instruments Market was valued at approximately USD 0.71 Billion in 2025 and is expected to reach approximately USD 1.23 Billion by 2035, growing at a CAGR of approximately 5.63%.

The United States is the world's most commercially significant veterinary surgical instruments market through its combination of the highest pet ownership rates among major economies, the most extensive specialist veterinary hospital network including over 4,000 AVMA-accredited veterinary facilities, and the per-animal healthcare spending culture that motivates investment in advanced surgical intervention rather than euthanasia as the default response to surgically treatable conditions.

In 2025, Integra LifeSciences expanded its veterinary surgical instruments portfolio through the launch of a comprehensive small animal orthopaedic instrument set incorporating titanium alloy construction and enhanced ergonomic handle design developed through collaboration with board-certified veterinary orthopaedic surgeons at leading academic veterinary medical centres.

Veterinary Surgical Instruments Market Segment Analysis

-

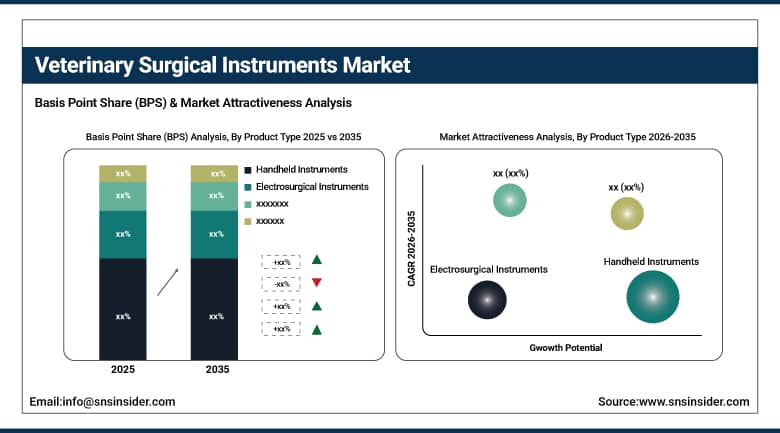

By Product Type, the Handheld Instruments segment dominated the Veterinary Surgical Instruments Market with approximately 38% share in 2025,while the Electrosurgical Instruments segment is the fastest growing product type.

-

By Animal Type, the Companion Animals segment dominated the Veterinary Surgical Instruments Market with approximately 62% share in 2025,while the Livestock segment retains significant commercial importance across agricultural veterinary practice.

-

By End User, the Veterinary Hospitals segment dominated the Veterinary Surgical Instruments Market with approximately 47% share in 2025,while the Ambulatory Surgical Centers segment is the fastest growing end user.

By Product Type, handheld instruments dominate, electrosurgical instruments grow fastest

Handheld instruments retained the dominant product type position with approximately 38% of the veterinary surgical instruments market in 2025. The universal requirement for handheld instruments across companion animal, livestock, and equine surgical settings creates a broad and consistent demand base whose growth tracks overall veterinary surgical case volume without dependence on the specialist facility concentration that more advanced instrument categories require.

Electrosurgical instruments are growing fastest as the adoption of monopolar and bipolar electrosurgery, ultrasonic vessel sealing, and radiofrequency tissue ablation across veterinary surgical specialties creates demand for energy-based surgical devices whose haemostatic capability reduces intraoperative blood loss, minimises surgical time, and improves post-operative outcome metrics that specialist veterinary facilities use to document clinical performance.

By End User, veterinary hospitals dominate, ambulatory surgical centers grow fastest

Veterinary hospitals retained the dominant end user position with approximately 47% of the veterinary surgical instruments market in 2025. Their commercial leadership reflects their role as the primary setting for complex, specialist, and emergency surgical procedures whose instrument requirements are the most comprehensive, highest-value, and most rapidly evolving in the veterinary surgical instruments market

Ambulatory surgical centres are the fastest growing end user because their outpatient surgical model, which combines the procedural capability of a surgical suite with the cost efficiency of non-hospitalisation-based care delivery, addresses the growing pet owner demand for effective surgical intervention at economics that the general practice veterinary clinic cannot accommodate due to facilities and equipment limitations and the specialist referral hospital cannot match due to overnight hospitalisation cost.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.47% |

|

Europe |

Germany |

28.47% |

|

Asia Pacific |

China |

38.47% |

|

Middle East & Africa |

UAE |

22.84% |

|

Latin America |

Brazil |

43.84% |

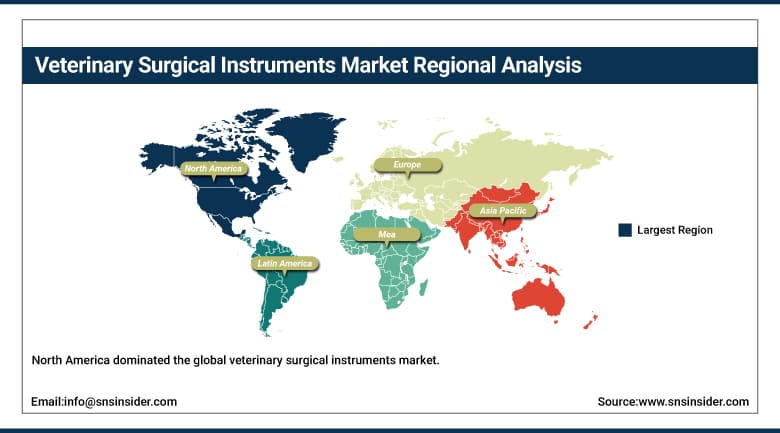

North America Veterinary Surgical Instruments Market Insights

North America dominated the global veterinary surgical instruments market in 2023, accounting for the largest regional revenue share. The United States accounts for approximately 82.47% of North American revenues through the world's highest per-animal veterinary spending, the most extensive specialist veterinary hospital infrastructure, and the concentrated commercial presence of major veterinary surgical instrument manufacturers. The American pet humanisation culture whose companion animal healthcare investment increasingly mirrors human medicine standards creates a commercial pull for advanced veterinary surgical instruments that sustains North American market leadership independent of overall pet population growth rates.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Veterinary Surgical Instruments Market Insights

Europe held a significant share of the global Veterinary Surgical Instruments Market in 2025. Germany, France, the United Kingdom, the Netherlands, and Sweden are the leading national markets whose advanced veterinary medicine traditions, well-funded companion animal healthcare ecosystems, and established specialist veterinary practice networks create consistent surgical instrument demand. Germany accounts for approximately 28.47% of European revenues through its large domestic companion animal population, the commercial presence of Aesculap Veterinary and other European instrument manufacturers, and the advanced specialist veterinary practice infrastructure at university teaching hospitals including Hanover, Munich, and Berlin whose surgical volumes drive premium instrument procurement.

Asia Pacific Veterinary Surgical Instruments Market Insights

Asia Pacific is the fastest-growing regional veterinary surgical instruments market, driven by the rapid growth of companion animal ownership across China, Japan, South Korea, India, and Southeast Asian markets whose urban middle-class populations are adopting pet ownership at rates that are creating new veterinary care infrastructure investment. China accounts for approximately 38.47% of Asia Pacific revenues through its extraordinary pace of companion animal market development, whose pet cat and dog population has grown to an estimated 120 million animals creating demand for veterinary hospitals, specialist practices, and the surgical instrument procurement they require.

MEA & Latin America Veterinary Surgical Instruments Market Insights

The UAE leads MEA revenues at approximately 22.84% of the regional total through its advanced veterinary healthcare infrastructure, the premium companion animal and equine healthcare demands of its affluent population, and the commercial presence of specialist veterinary facilities whose advanced surgical requirements create instrument procurement above regional average quality and value. The equine veterinary surgery market in the UAE and Gulf Cooperation Council is particularly commercially significant given the cultural and financial importance of horse ownership whose surgical care requirements encompass expensive orthopaedic and soft tissue instrument sets.

Brazil leads Latin American revenues at approximately 43.84% of the regional total through its large companion animal population estimated at over 140 million pets, the growing middle class's veterinary healthcare investment, and the increasing availability of specialist veterinary surgical services in major urban centres. Mexico and Colombia are growing secondary markets within the region whose expanding veterinary practice networks and growing companion animal ownership are creating increasing surgical instrument demand that international manufacturers are progressively addressing through direct distribution investment.

Market Dynamics:

Growth Drivers: Rising companion animal ownership accelerating surgical case volumes and progressive adoption of specialist veterinary surgical techniques creating premium instrument demand

The veterinary surgical instruments market's growth is driven by the compounding effect of pet population expansion increasing the absolute number of animals eligible for surgical intervention and the progressive adoption of advanced surgical techniques raising the per-animal instrument investment required to serve each surgical case optimally. Global companion animal populations are growing at above-GDP rates across virtually every major economy as demographic trends including urbanisation, delayed family formation, empty-nester pet adoption, and the well-documented mental health benefits of pet ownership expand the pet-owning population and deepen the emotional investment that motivates healthcare spending. Each additional companion animal in a household with veterinary care access represents a potential surgical case whose lifetime surgical probability, driven by orthopaedic conditions, oncological interventions, gastrointestinal emergencies, and elective dental procedures, creates ongoing surgical instrument consumption across the clinical settings serving that animal.

Restraints: High instrument procurement cost and the veterinary specialist shortage constraining advanced surgical procedure adoption in price-sensitive and geographically underserved markets

Premium veterinary surgical instrument sets represent significant capital investments whose procurement cost places them beyond the financial reach of smaller independent veterinary clinics whose patient volume cannot amortise specialist instrument investment across sufficient annual procedure count. A complete laparoscopic veterinary surgery tower and instrument set requires an investment of USD 30,000 to USD 80,000, while comprehensive orthopaedic implant and instrument systems for tibial plateau levelling osteotomy represent comparable investment levels whose justification requires annual procedure volumes achievable only at specialist or high-volume referral facilities. The veterinary specialist shortage, which is pronounced in rural areas and developing economies whose geographic distance from specialist facilities forces owners to choose between costly referral travel and foregone advanced surgical care, limits the geographic expansion of specialist surgical instrument adoption beyond urban specialist facility concentrations.

Opportunities: Minimally invasive veterinary surgical instrument innovation and emerging market veterinary infrastructure investment creating new growth frontiers

Minimally invasive veterinary surgery represents the most commercially dynamic instrument innovation frontier whose adoption trajectory, following the pattern established in human surgery, is progressively expanding from specialist academic veterinary hospitals toward general specialist referral practices as instrument cost declines with competitive market development and veterinary surgeon laparoscopic training completion rates grow. Each veterinary practice that adds laparoscopic or thoracoscopic surgical capability adds a full instrument set procurement event whose initial capital purchase and ongoing consumable replacement creates sustained instrument revenue above general surgery baseline. Emerging market veterinary infrastructure investment across China, India, Brazil, and Southeast Asian economies, where companion animal adoption rates are growing at 10 to 15% annually and government veterinary modernisation programmes are funding hospital infrastructure development, creates greenfield instrument procurement opportunities in markets whose baseline instrument quality level is progressively upgrading toward international standards.

Recent Developments:

-

2025: Integra LifeSciences launched a comprehensive small animal orthopaedic instrument set in titanium alloy with enhanced ergonomic design developed with board-certified veterinary orthopaedic surgeons at leading academic veterinary centres, targeting the growing specialist surgical market's demand for precision instruments that improve surgeon comfort and procedural outcomes.

-

2024: IDEXX Laboratories partnered with veterinary surgical instrument manufacturers to integrate pre-surgical diagnostic data into surgical planning workflows, enabling real-time haematology, biochemistry, and imaging data access during instrument selection and surgical preparation to improve surgical decision-making and reduce anaesthetic risk.

-

2023: Medtronic expanded its veterinary surgical instruments commercial programme through distribution agreements with specialist veterinary distributors in North America and Europe, making its LigaSure vessel sealing technology and advanced monopolar and bipolar electrosurgical platforms more accessible to specialist veterinary referral hospitals and university teaching facilities.

Veterinary Surgical Instruments Market Key Players

-

IDEXX Laboratories Inc.

-

Medtronic PLC

-

Johnson & Johnson (Ethicon Veterinary)

-

Integra LifeSciences Corporation

-

Sklar Surgical Instruments

-

Jorgensen Laboratories Inc.

-

Miltex Instrument Company

-

Kruuse A/S

-

Aesculap Veterinary (B. Braun)

-

Neogen Corporation

-

Roboz Surgical Instrument Co.

-

Veterinary Orthopedic Implants Inc.

-

BioMedtrix LLC

-

Arthrex Veterinary Systems

-

Synthes Veterinary (DePuy Synthes)

-

Surgi-Vet Inc.

-

Stryker Veterinary (Stryker Corporation)

-

GerVetUSA Inc.

-

Dispomed Ltd.

-

World Precision Instruments Inc.

Veterinary Surgical Instruments Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.10 Billion |

| Market Size by 2035 | USD 3.62 Billion |

| CAGR | CAGR of 5.66% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Product Type (Handheld Instruments, Electrosurgical Instruments, Orthopaedic Instruments, Ophthalmic Instruments, Dental Instruments, Others) • by Animal Type (Companion Animals, Livestock, Poultry, Others) • by End User (Veterinary Hospitals, Veterinary Clinics, Ambulatory Surgical Centers, Academic & Research Institutes, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | IDEXX Laboratories Inc., Medtronic PLCm Johnson & Johnson (Ethicon Veterinary), Integra LifeSciences Corporation, Sklar Surgical Instruments, Jorgensen Laboratories Inc., Miltex Instrument Company, Kruuse A/S, Aesculap Veterinary (B. Braun), Neogen Corporation, Roboz Surgical Instrument Co., Veterinary Orthopedic Implants Inc., BioMedtrix LLC, Arthrex Veterinary Systems, Synthes Veterinary (DePuy Synthes), Surgi-Vet Inc., Stryker Veterinary (Stryker Corporation), GerVetUSA Inc., Dispomed Ltd., World Precision Instruments Inc. |

Frequently Asked Questions

The Veterinary Surgical Instruments Market is expected to grow at a CAGR of 5.66% from 2026 to 2035.

The Veterinary Surgical Instruments Market was valued at USD 2.10 Billion in 2025.

Rising global companion animal ownership expanding surgical case volumes, progressive adoption of minimally invasive and specialist veterinary surgical techniques creating premium instrument demand.

The Handheld Instruments segment dominated the Veterinary Surgical Instruments Market with approximately 38% share in 2025, while the Electrosurgical Instruments segment is the fastest growing due to rising energy-based surgical device adoption.

North America dominated the Veterinary Surgical Instruments Market in 2023 as the world's most commercially advanced veterinary healthcare market, with the United States accounting for approximately 82.47% of North American revenues.

Get in Touch