Pharmaceutical Plastic Bottles Market Report Scope & Overview:

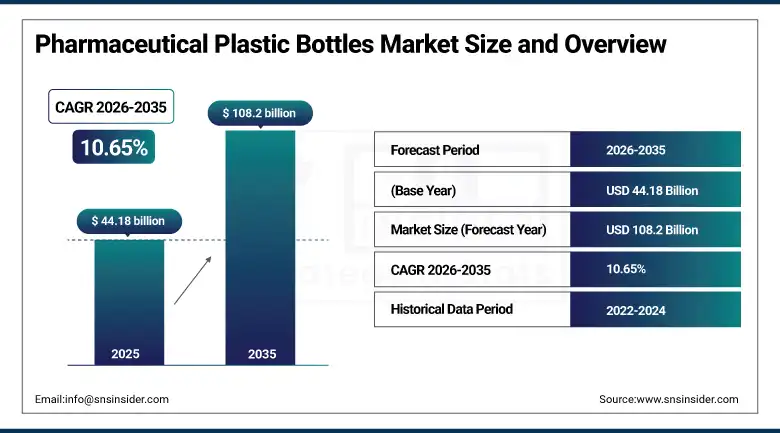

The Pharmaceutical Plastic Bottles Market was valued at USD 44.18 Billion in 2025 and is expected to reach USD 108.2 Billion by 2035, growing at a CAGR of 10.65% from 2026–2035.

Pharmaceutical plastic bottles are purpose-designed containers that store, protect, and dispense medication in a way that maintains drug stability, prevents contamination, and ensures patient safety throughout the product's approved shelf life. Plastic has displaced glass in the majority of pharmaceutical bottle applications because it is lighter, shatter-resistant, more design-flexible, and manufacturable at a lower cost per unit. The market's commercial scale reflects the pharmaceutical industry's extraordinary production volume and the universal requirement for compliant, validated, tamper-evident packaging that meets the regulatory specifications of every market where drugs are sold. Every tablet bottle, cough syrup bottle, eye drop vial, and prescription liquid container represents a unit of pharmaceutical plastic bottle demand. The pharmaceutical industry's global growth, driven by ageing populations, rising chronic disease prevalence, expanding healthcare access in developing markets, and the extraordinary innovation pipeline of new drugs, creates a structurally expanding demand base for pharmaceutical plastic bottles across every product category and geographic market.

Industry research indicates that 85% of pharmaceutical professionals cite plastic packaging's barrier performance against moisture, light, and oxygen as its primary advantage over alternative formats. A further 72% highlight the patient convenience advantages of lightweight, shatter-resistant plastic bottles relative to glass as a key factor sustaining plastic's dominance in pharmaceutical packaging across all dosage form categories.

Market Size and Forecast

-

Market Size in 2026E: USD 48.88 Billion

-

Market Size by 2035: USD 108.2 Billion

-

CAGR: 10.65% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Pharmaceutical Plastic Bottles Market - Request Free Sample Report

Pharmaceutical Plastic Bottles Market Trends

-

High-barrier plastic bottle development for oxygen-sensitive and moisture-sensitive biologic medications is growing as pharmaceutical companies seek plastic packaging alternatives to glass that maintain the stringent barrier performance.

-

Child-proofing and senior-proofing closures are being developed together in parallel, as per regulatory guidelines for child-proof packaging and patient activism.

-

Research in sustainable biodegradable plastic bottles for medicines is being undertaken due to pressure from both corporations toward sustainability goals and regulatory authorities in Europe.

-

The use of smart packaging technologies such as NFC tags, QR-coded patient information, time-temperature indicators, and electronic adherence tracking systems is progressing from conceptualization towards realization in the design and implementation of pharmaceutical bottles.

-

Pharmaceutical manufacturing for emerging markets is expanding rapidly in countries such as India, China, Southeast Asia, and Africa, which requires local manufacturing capability for pharmaceutical bottles.

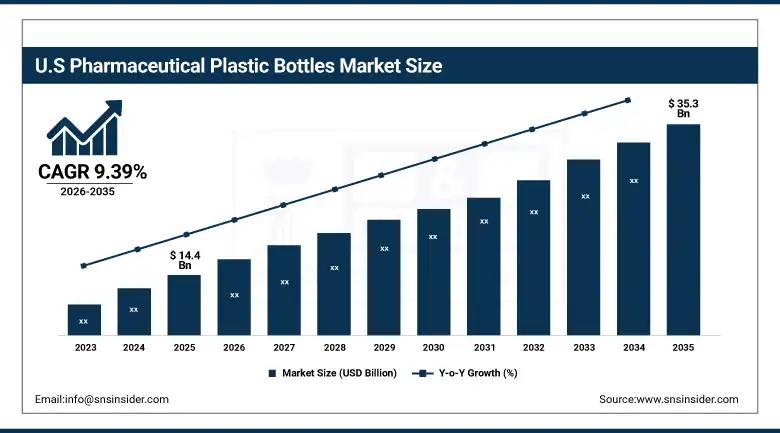

The U.S. Pharmaceutical Plastic Bottles Market Outlook

The U.S. pharmaceutical plastic bottles market was valued at approximately USD 14.4 Billion in 2025 and is expected to reach approximately USD 35.3 Billion by 2035, growing at a CAGR of 9.39%.

The United States is the world's largest pharmaceutical market by revenue, and its pharmaceutical plastic bottle demand reflects both the scale of American drug production and the complexity of U.S. packaging regulatory requirements. The FDA's requirements for pharmaceutical packaging qualification, extractables and leachable testing, and container-closure system validation create a compliance framework that pharmaceutical bottle manufacturers serving the U.S. market must satisfy for every bottle and closure combination used for a specific drug product. Child-resistant packaging requirements under the U.S. Poison Prevention Packaging Act apply to most prescription medications and require bottles with closures that satisfy standardized child resistance performance testing while remaining accessible to adults. American pharmaceutical bottle manufacturers including Berry Global, Gerresheimer, and Alpha Packaging serve both the prescription drug packaging and the over-the-counter consumer health product markets. The expansion of pharmaceutical manufacturing within the United States through the process of reshoring increases the demand for pharmaceutical packaging made within the country.

There is a possibility that a 22% increase in demand may occur by 2035 due to an increasing number of biologics, mRNA vaccines, and specialty drugs requiring better packaging performance. Since these are more premium medicines, they require improved packaging that leads to greater average revenue per bottle compared to solid oral dosage packaging.

Pharmaceutical Plastic Bottles Market Segment Analysis

-

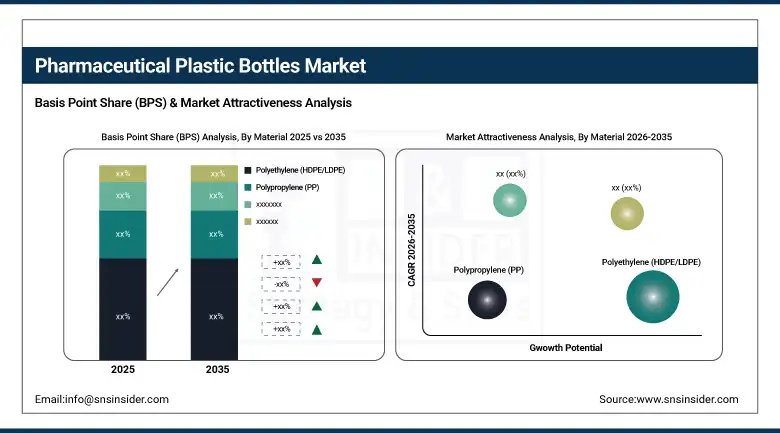

By Material, high-density polyethylene dominated the market with the largest share in 2025; PET is growing rapidly.

-

By Bottle Type, solid formulation bottles held the largest share in 2025; dropper bottles are the fastest-growing type.

-

By End User, pharmaceutical companies held the largest share in 2025; contract packaging organizations are the fastest-growing end user.

By Material, HDPE dominates, PET grows fastest

High-density polyethylene held the dominant position in the pharmaceutical plastic bottles market in 2025. HDPE's combination of excellent moisture barrier performance, chemical resistance across a wide range of pharmaceutical formulations, broad regulatory acceptance, opaque appearance that provides light protection for photosensitive medications, and competitive price point makes it the default material choice for prescription solid oral dosage form packaging globally. HDPE is compatible with most tablet and capsule formulations and does not interact with the vast majority of pharmaceutical active ingredients at commercially relevant concentrations. Its impact resistance prevents breakage in the handling and distribution environments that pharmaceutical bottles experience between production and patient use, reducing product waste and quality incidents.

Polyethylene terephthalate is the fastest-growing material through its exceptional clarity, which enables visual inspection of bottle contents, and its superior oxygen barrier properties relative to HDPE that make it preferred for liquid oral medications and specialty packaging applications where product appearance is commercially important. PET pharmaceutical bottles are widely used for cough syrups, antacid suspensions, and liquid nutritional supplements where consumers expect to see the product through the container. The development of pharmaceutical-grade PET with enhanced chemical resistance and extractables profiles is expanding PET's applicability beyond conventional liquid formulation packaging into more chemically demanding specialty drug applications.

By Bottle Type, solid formulation bottles dominate, dropper bottles grow fastest

Solid formulation bottles held the largest share of the pharmaceutical plastic bottles market in 2025. The overwhelming volume of pharmaceutical production globally is in solid oral dosage form, where tablets and capsules are the most manufactured and most consumed drug delivery formats. Every prescription bottle of blood pressure medication, cholesterol medication, diabetes treatment, antibiotic, or pain reliever represents a pharmaceutical plastic bottle unit. The scale of this demand base is extraordinary, with billions of prescriptions fills annually in the U.S. alone and the global equivalent many times larger. Solid dosage form bottle designs are well established with standardized closure options meeting child-resistance requirements and well-understood material and quality specifications across the regulatory jurisdictions where drugs are sold.

Dropper bottles are the fastest-growing bottle type through the expanding market for ophthalmic medications, nasal spray products, and oral liquid medications requiring precise, controlled-volume dosing. The growing prevalence of dry eye disease and glaucoma requiring regular ophthalmic medication, increasing nasal allergy medication use, and the growth of specialty oral liquid formulations for pediatric and elderly patients who cannot swallow solid dosage forms are all expanding dropper bottle demand. Precision dispensing dropper systems are becoming more sophisticated, with unit-dose dispensing, preservative-free multidose dropper systems, and antimicrobial bottle neck designs that prevent contamination during repeated use representing active innovation areas in premium dropper bottle product development.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.7% |

|

Europe |

Germany |

26.4% |

|

Asia Pacific |

China |

41.3% |

|

Middle East & Africa |

UAE |

27.8% |

|

Latin America |

Brazil |

44.2% |

North America Pharmaceutical Plastic Bottles Market Insights

North America dominated the global pharmaceutical plastic bottles market in 2025 through its combination of the world's highest pharmaceutical market revenues, strict packaging compliance requirements that sustain product differentiation investment, and established manufacturing capacity from leading pharmaceutical bottle producers. The United States accounts for approximately 82.7% of North American revenues. American pharmaceutical companies including Pfizer, Johnson and Johnson, AbbVie, Merck, and Eli Lilly collectively represent extraordinary pharmaceutical bottle procurement volumes across their extensive product portfolios. Retail pharmacy chains including CVS, Walgreens, and Rite Aid repackage bulk medications into labelled bottles whose quality and compliance specifications their pharmacies must maintain as the dispensing container.

Get Customized Report as per Your Business Requirement - Enquiry Now

Canadian pharmaceutical packaging meet Health Canada container-closure system requirements aligned with ICH Q3E extractables and leachable guidelines that are progressively being harmonized globally. The Canadian market benefits from close supply chain integration with U.S. pharmaceutical bottle manufacturers who serve both markets.

Europe Pharmaceutical Plastic Bottles Market Insights

Europe is a large and regulation-driven pharmaceutical plastic bottle market where EU packaging regulations, EMA container-closure system requirements, and progressive sustainability policy are simultaneously shaping demand. Germany accounts for approximately 26.4% of European revenues as the EU's largest pharmaceutical manufacturing economy and the location of pharmaceutical bottle producers including Gerresheimer AG, one of the world's most commercially significant pharmaceutical glass and plastic packaging companies. European pharmaceutical packaging is increasingly subject to the EU Packaging and Packaging Waste Regulation's recyclability and recycled content requirements, creating demand for pharmaceutical-grade recycled or bio-based plastic bottle materials that maintain the performance and regulatory compliance characteristics of conventional pharmaceutical packaging.

The European pharmaceutical packaging landscape is characterized by above-average investment in child-resistant and senior-friendly closure innovation, sustainable material development, and serialization-compatible bottle design that enables track-and-trace compliance with EU Falsified Medicines Directive requirements. These regulatory-driven specification areas sustain the product development investment that differentiates European pharmaceutical bottle suppliers from commodity packaging competitors.

Asia Pacific Pharmaceutical Plastic Bottles Market Insights

Asia Pacific is the fastest-growing pharmaceutical plastic bottle market through the extraordinary expansion of pharmaceutical manufacturing in India, China, South Korea, Japan, and Southeast Asia. China accounts for approximately 41.3% of Asia Pacific revenues as the world's largest PET resin producer and one of the largest domestic pharmaceutical markets. China's pharmaceutical manufacturing sector produces enormous volumes of both domestic and export medications in plastic bottle packaging that meets the standards of both Chinese national drug regulations and the international GMP standards required for export market access. India's pharmaceutical manufacturing sector produces generic drugs for global export, creating large pharmaceutical plastic bottle demand that is served by a well-developed domestic bottle manufacturing industry.

MEA & Latin America Pharmaceutical Plastic Bottles Market Insights

The Middle East and Africa and Latin America are growing pharmaceutical plastic bottle markets where pharmaceutical manufacturing investment and healthcare spending growth are creating expanding packaging demand. The UAE leads MEA revenues at approximately 27.8% of the regional share through its growing domestic pharmaceutical manufacturing sector and its position as a pharmaceutical distribution hub for the broader Middle East and African markets. Brazil leads Latin American revenues at approximately 44.2% through its large domestic pharmaceutical manufacturing sector regulated by ANVISA that produces both branded and generic drugs for the Brazilian population and for export across Latin American markets.

Market Dynamics

Growth Drivers: Pharmaceutical industry global expansion and specialty drug pipeline requiring advanced packaging performance are driving pharmaceutical plastic bottles market growth.

Global pharmaceutical industry expansion driven by ageing population demographics, rising chronic disease prevalence, and expanding healthcare access in developing markets is the foundational driver of pharmaceutical plastic bottle demand growth. The revolutionary innovation pipeline in the pharma sector with over 6,000 new products being developed in clinical trials around the world in 2025 is generating an unprecedented multi-year wave of new commercial product launches that will need regulatory approved packaging systems, which include plastic bottles. The pipeline of biologics and specialty drugs is generating demand for plastic pharmaceutical bottles in key commercial classes. Biologics, which includes monoclonal antibodies, biosimilar drugs, cell and gene therapy products, and RNA platforms, are highly sensitive, requiring packaging with high barrier properties, extractables and leachables performance up to the safety requirements of complex biologics, and convenience attributes. Premium specialty drug packaging commands significantly higher revenue per unit than standard solid oral dosage packaging, creating value growth in the pharmaceutical plastic bottle market that outpaces volume growth as the product mix shifts toward higher-value specialty formats.

Restraints: Environmental regulatory pressure on pharmaceutical plastic packaging, raw material price volatility are restraining market growth.

Environmental regulatory pressure on pharmaceutical plastic packaging is creating compliance cost and operational complexity for pharmaceutical bottle manufacturers. EU packaging sustainability requirements, national plastic taxes in France, the UK, and several other However, pharmaceutical packaging has legitimate patient safety arguments for current material specifications, and the extractables and leachable testing required to qualify new recycled or bio-based materials for pharmaceutical contact is expensive and time-consuming. Raw material price volatility is a persistent challenge for pharmaceutical bottle manufacturers. Polyethylene, PET, and polypropylene prices fluctuate with crude oil and natural gas prices in ways that are difficult to predict or hedge over the multi-year supply contracts that pharmaceutical company customers prefer. The industry's ongoing interest in bio-based polymers is partly motivated by the desire to reduce petroleum price exposure, though bio-based feedstocks carry their own agricultural commodity price volatility characteristics.

Opportunities: High-barrier specialty bottles for biologic and mRNA drug packaging, sustainable pharmaceutical plastic bottle innovations are creating market growth opportunities.

High-barrier specialty pharmaceutical plastic bottles represent the most commercially premium growth opportunity in the market. The expansion of biologic, mRNA, and gene therapy drug production is creating demand for packaging solutions with oxygen and moisture barrier performance approaching or matching glass without glass's fragility, weight, and limited design flexibility. Smart packaging integration is moving from concept to commercial deployment as pharmaceutical companies seek to address medication non-adherence, improve patient safety through authentication, and satisfy EU Falsified Medicines Directive serialization requirements. NFC-enabled pharmaceutical bottles that connect to patient medication management applications, time-temperature indicator strips that confirm cold chain integrity for biologics, and electronic reminder caps that track opening frequency for adherence monitoring are each creating new functionality value that supports premium pricing and brand differentiation beyond conventional bottle specification competition.

Recent Developments:

-

2025: Amcor plc launched new pharmaceutical-grade polyethylene bottle formulations with enhanced oxygen barrier properties for sensitive biologic drug packaging applications, expanding the company's specialty pharmaceutical packaging product range beyond conventional HDPE solid dosage form bottles.

-

2025: Berry Global Inc. introduced new recycled-content pharmaceutical plastic bottles incorporating post-consumer recycled HDPE that meet FDA food-contact regulations and pharmaceutical extractables compliance requirements, addressing growing demand for sustainable pharmaceutical packaging.

-

2025: Gerresheimer AG expanded its ClearJect polymer syringe platform and announced investment in expanded plastic pharmaceutical packaging production capacity in India, positioning for pharmaceutical manufacturing growth in the Asia Pacific region.

-

2025: AptarGroup launched new connected pharmaceutical closure systems integrating NFC and Bluetooth adherence monitoring for specialty and chronic disease medications, enabling pharmaceutical companies to offer digital patient engagement alongside conventional medication dispensing.

Pharmaceutical Plastic Bottles Market Key Players are:

-

Amcor plc

-

Berry Global Inc.

-

Gerresheimer AG

-

AptarGroup Inc.

-

Alpha Packaging Company

-

Comar LLC

-

Drug Plastics Group

-

Alpack Inc.

-

United States Plastic Corporation

-

Silgan Holdings Inc.

-

Altium Packaging LLC

-

Pretium Packaging

-

ALPLA Werke Alwin Lehner GmbH & Co. KG

-

Bormioli Pharma S.p.A.

-

Weener Plastics Group BV

-

Origin Pharma Packaging

-

C.L. Smith Company

-

Pro-Pac Packaging Group

-

Frapak Packaging BV

-

Graham Packaging Company

Pharmaceutical Plastic Bottles Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 44.18 Billion |

| Market Size by 2035 | USD 108.2 Billion |

| CAGR | CAGR of 10.65% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material (Polyethylene (HDPE/LDPE), Polyethylene Terephthalate (PET), Polypropylene (PP), Others) • By Bottle Type (Solid Formulation Bottles, Liquid Formulation Bottles, Ophthalmic/Nasal Bottles, Dropper Bottles, Others) • By End User (Pharmaceutical Companies, Compounding Pharmacies, Contract Packaging Organizations, Healthcare Institutions, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Amcor plc, Berry Global Inc., Gerresheimer AG, AptarGroup Inc., Alpha Packaging Company, Comar LLC, Drug Plastics Group, Alpack Inc., United States Plastic Corporation, Silgan Holdings Inc., Altium Packaging LLC, Pretium Packaging, ALPLA Werke Alwin Lehner GmbH & Co. KG, Bormioli Pharma S.p.A., Weener Plastics Group BV, Origin Pharma Packaging, C.L. Smith Company, Pro-Pac Packaging Group, Frapak Packaging BV, Graham Packaging Company |

Frequently Asked Questions

North America dominated the pharmaceutical plastic bottles market in 2025.

High-Density Polyethylene dominated with the largest share of revenues in 2025.

Global pharmaceutical industry expansion and the growing biologic and specialty drug pipeline requiring advanced packaging performance are the primary drivers.

The pharmaceutical plastic bottles market was valued at USD 44.18 Billion in 2025.

The pharmaceutical plastic bottles market is expected to grow at a CAGR of 10.65% from 2026 to 2035.

Get in Touch