Pharmacokinetics Services Market Report Scope & Overview:

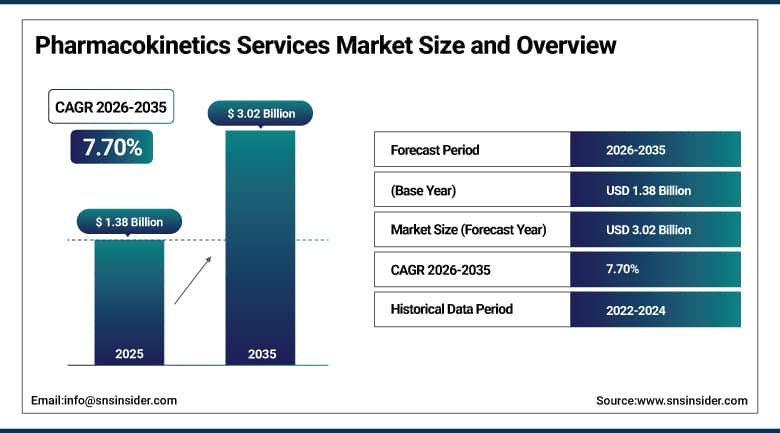

The Pharmacokinetics Services Market was valued at USD 1.38 Billion in 2025 and is expected to reach USD 3.02 Billion by 2035, growing at a CAGR of 7.70% from 2026–2035.

The global pharmacokinetics services market is growing at a sustained pace. Pharmacokinetics services encompass the quantitative characterisation of how drugs move through the body over time including absorption, distribution, metabolism, and excretion processes that collectively determine a drug candidate's dosing requirements, exposure-response relationships, and safety profile. These services are foundational to drug development success, enabling dose selection, formulation optimisation, drug-drug interaction assessment, and regulatory submission support across all clinical development phases.

In 2023, Charles River Laboratories expanded its pharmacokinetics services portfolio by introducing advanced bioanalytical platforms for small molecules and biologics. The expansion reflects the commercial recognition that pharmaceutical clients' increasing biologics pipeline requires bioanalytical service capability that goes beyond conventional small molecule PK assay infrastructure, necessitating investment in large molecule quantification methods including ligand binding assays and hybrid immunoaffinity LC-MS/MS approaches whose technical complexity creates differentiation for specialist PK service providers.

Market Size and Forecast:

-

Market Size in 2026E: USD 1.49 Billion

-

Market Size by 2035: USD 3.02 Billion

-

CAGR: 7.70% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Pharmacokinetics Services Market - Request Free Sample Report

Pharmacokinetics Services Market Trends:

-

Growing adoption of PK/PD modeling and simulation is supporting model-informed drug development and improving dose selection, clinical trial design, and regulatory submissions

-

Rising development of biologics and complex therapeutics is increasing demand for specialized pharmacokinetic services, including immunogenicity and target-mediated drug disposition studies

-

AI and machine learning technologies are enhancing PK modeling efficiency through automated data analysis, model optimization, and virtual population simulations

-

Increasing use of physiologically based pharmacokinetic (PBPK) modeling is enabling more accurate prediction of drug behavior across patient populations and clinical scenarios

-

Expanding oncology drug development is driving demand for advanced PK services to support precision medicine, immunotherapies, and antibody-drug conjugate programs

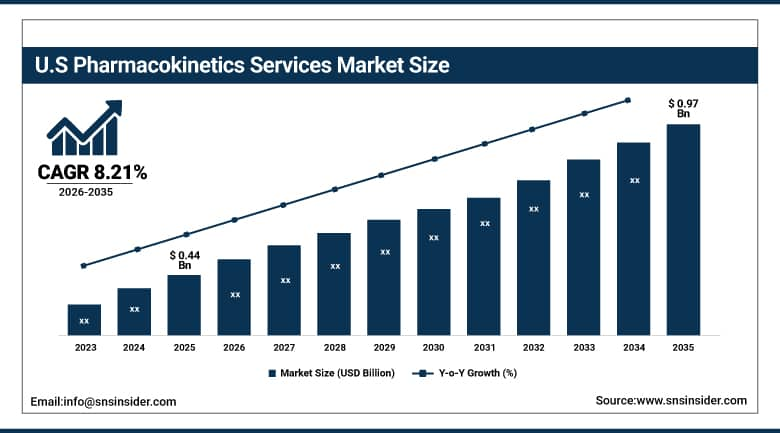

U.S. Pharmacokinetics Services Market Outlook:

The U.S. Pharmacokinetics Services Market was valued at approximately USD 0.44 Billion in 2025 and is expected to reach approximately USD 0.97 Billion by 2035, growing at a CAGR of approximately 8.21%.

The U.S. is the world's most commercially significant pharmacokinetics services market within North America's dominant revenue position. Charles River Laboratories, Covance (Labcorp Drug Development), ICON plc, PAREXEL, and Certara's U.S. operations collectively define the commercial PK services landscape. The FDA's Model-Informed Drug Development guidance, ICH E11(R1)'s paediatric extrapolation modelling framework, and the U.S. biopharmaceutical industry's extraordinary clinical trial activity collectively create the most commercially concentrated PK services demand globally.

In January 2024, Labcorp received FDA approval for its innovative PK modelling software integrating AI to predict drug behaviour in the human body. The software's AI-powered prediction capability enables clinical pharmacologists to identify optimal dose regimens from sparse PK data with greater statistical confidence, reducing the sample size requirements for first-in-human Phase I studies whose cost and timeline reduction creates commercial value for pharmaceutical clients seeking to accelerate clinical development programmes.

Pharmacokinetics Services Market Segment Analysis:

-

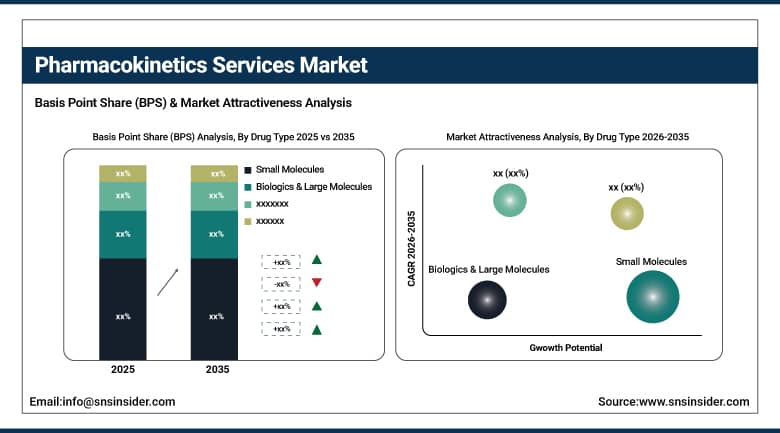

By Drug Type, the Small Molecules segment dominated the Pharmacokinetics Services Market with approximately 68% share in 2025, while the Biologics & Large Molecules segment is the fastest growing.

-

By Service Type, the Bioanalytical Services segment dominated the Pharmacokinetics Services Market with approximately 42% share in 2025, while the PK/PD Modelling & Simulation segment is the fastest growing.

-

By Clinical Phase, the Preclinical segment dominated the Pharmacokinetics Services Market with approximately 35% share in 2025, while the Phase I segment is the fastest growing.

-

By End User, the Pharmaceutical & Biotechnology Companies segment dominated the Pharmacokinetics Services Market with approximately 52% share in 2025, while the Contract Research Organizations segment is the fastest growing.

By Drug Type, small molecules dominate, biologics grow fastest

Small molecules retained the dominant drug type position with approximately 68% of the pharmacokinetics services market in 2025. The established regulatory framework, validated bioanalytical methods, and extensive historical PK data library for small molecule pharmaceuticals create a mature and commercially certain service category whose procurement scales with the global small molecule drug pipeline. Each new small molecule IND application creates defined PK service requirements across species ADME characterisation, first-in-human PK sampling, and food effect and DDI study design whose service procurement compounds with the active small molecule clinical pipeline volume. The generic pharmaceutical industry's bioequivalence PK study requirements create additional non-innovative PK service procurement that sustains market volume independently of novel drug development cycles.

Biologics and large molecules are the fastest-growing drug type because the biopharmaceutical pipeline's progressive shift toward monoclonal antibodies, bispecific antibodies, ADCs, gene therapies, and RNA therapeutics creates PK service requirements that substantially exceed the conventional small molecule bioanalytical and modelling infrastructure. Each biologic's target-mediated drug disposition complexity, immunogenicity assessment requirement, and receptor occupancy measurement create multi-analyte PK study designs whose specialised service requirement creates above-average commercial relationships with technically qualified specialist PK service providers.

By Service Type, bioanalytical dominates, PK/PD modelling grows fastest

Bioanalytical services retained the dominant service type position with approximately 42% of the pharmacokinetics services market in 2025. Bioanalytical services' commercial primacy reflects the foundational requirement for quantitative drug concentration measurement whose accurate and precise assessment in biological matrices creates the primary data that all pharmacokinetic analysis, modelling, and regulatory submission is based upon. Each PK study conducted at any clinical development phase requires validated bioanalytical methods whose regulatory GLP or GCP compliance creates structured service procurement from accredited bioanalytical laboratories. The biologics industry's requirement for ligand binding assay and immunogenicity assessment creates additional bioanalytical service demand beyond conventional LC-MS/MS small molecule methods.

PK/PD modelling and simulation is the fastest-growing service type because regulatory agencies' progressive acceptance of model-informed drug development as a regulatory submission tool creates structured demand for high-quality population PK analysis, exposure-response modelling, and clinical trial simulation. FDA's Model-Informed Drug Development qualification guidance and EMA's similar framework create the regulatory precedent whose adoption across therapeutic areas creates systematic PK/PD modelling service procurement in clinical development programmes whose dose selection and paediatric extrapolation decisions benefit from quantitative modelling approaches.

By Clinical Phase, preclinical dominates, Phase I grows fastest

Preclinical PK services retained the dominant clinical phase position with approximately 35% of the pharmacokinetics services market in 2025. The preclinical phase's commercial dominance reflects the universal requirement for species ADME characterisation, toxicokinetic study support, and lead candidate selection PK profiling that every drug development programme undertakes before IND submission. Each drug candidate whose development programme progresses from discovery through lead optimisation creates preclinical PK service procurement whose early-stage investment is a prerequisite for clinical development initiation. High-throughput in-vitro ADME screening, multi-species PK profiling, and protein binding assessment create substantial preclinical PK service volume that compounds with the global pharmaceutical discovery pipeline's breadth.

Phase I clinical PK is the fastest-growing clinical phase because the first-in-human study's intensive PK sampling design, the multiple Part A/B/C study elements including single and multiple ascending dose cohorts, and the food effect, drug interaction, and special population studies that Phase I encompasses create concentrated high-value PK service procurement whose per-study commercial value substantially exceeds preclinical or post-approval alternatives. The growing oncology Phase I programme volume, whose expansion from conventional cytotoxic dose escalation toward targeted therapy combination studies creates complex multi-analyte PK service designs, sustains Phase I's fastest-growing status.

By End User, pharma & biotech dominate, CROs grow fastest

Pharmaceutical and biotechnology companies retained the dominant end-user position with approximately 52% of the pharmacokinetics services market in 2025. The pharmaceutical industry's PK service procurement encompasses both in-house PK department operations and outsourced CRO partnerships whose combined investment defines the most commercially concentrated PK service demand category. Each pharmaceutical company's clinical pipeline creates systematic PK service procurement from IND-enabling studies through Phase III whose regulatory submission quality requirements sustain long-duration service relationships with qualified PK service providers. The biotechnology industry's rapidly growing clinical pipeline creates above-average new PK service procurement as biotech companies whose small internal science teams outsource the majority of their PK work to specialist CROs.

Contract research organisations are the fastest-growing end user because specialised PK service provision and CRO-to-CRO service outsourcing are creating above-average procurement growth from organisations whose PK service capabilities may not span all required specialisations. Large CROs without internal PK/PD modelling capability outsource modelling work to specialist modelling boutiques, and CROs without validated large molecule bioanalytical infrastructure outsource biologic PK sample analysis to specialist ligand binding assay laboratories, creating CRO-to-CRO service procurement that compounds with the overall CRO sector's growth.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Pharmacokinetics Services Market Insights

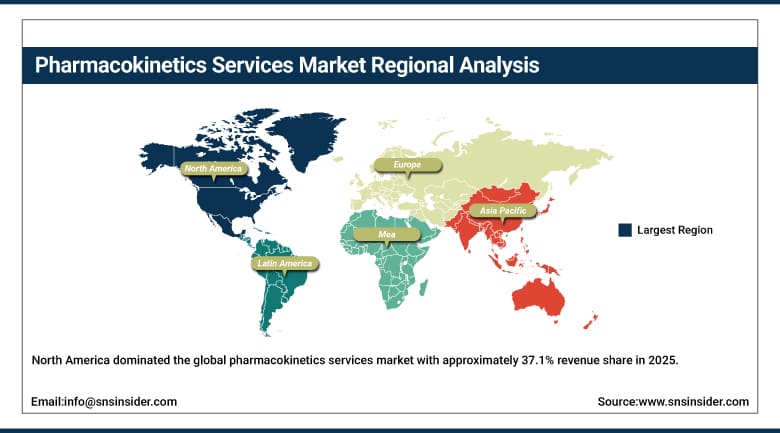

North America dominated the global pharmacokinetics services market with approximately 37.1% revenue share in 2025, driven by the large pool of skilled professionals, advanced bioanalytical infrastructure, and the presence of major pharmaceutical companies and CROs. The United States accounts for approximately 87.4% of North American revenues through Charles River Laboratories, Covance (Labcorp Drug Development), ICON plc, PAREXEL, and Certara's commercial presence whose combined portfolio defines the commercial PK services standard.

Canada contributes approximately 12.6% of North American revenues through its pharmaceutical research community, university academic PK programme, and the federal government's clinical trial investment that creates consistent PK service procurement.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Pharmacokinetics Services Market Insights

Europe is a technically sophisticated pharmacokinetics services market where EMA's regulatory framework, the EU's pharmaceutical industry's clinical trial activity, and leading CROs including Evotec, Eurofins Scientific, and SGS create a complete PK services ecosystem. Germany accounts for approximately 22.3% of European revenues through its pharmaceutical industry's preclinical and clinical PK investment, the Fraunhofer Institute's translational research programmes, and the CRO sector's European operations.

The United Kingdom and Switzerland are significant secondary markets where the NHS's clinical trial infrastructure, AstraZeneca and Novartis's European research operations, and specialised clinical pharmacology CROs create consistent PK service procurement.

Asia Pacific Pharmacokinetics Services Market Insights

Asia Pacific is the fastest-growing regional pharmacokinetics services market, driven by China's growing pharmaceutical CRO industry, India's Department of Biotechnology's USD 265 million research investment, Japan's regulatory agency's model-informed drug development adoption, and the region's cost-competitive clinical trial infrastructure. China accounts for approximately 44.8% of Asia Pacific revenues through WuXi AppTec and WuXi AppTec's Analytical testing services whose comprehensive PK analytical capability creates domestic service procurement for both international and Chinese pharmaceutical clients.

India is the most commercially dynamic emerging market within Asia Pacific where the growing domestic pharmaceutical industry's clinical development investment, the government's biotechnology R&D funding, and the established CRO sector's PK service capacity create above-average market growth that compounds with India's growing role as a clinical trial centre for international pharmaceutical programmes.

MEA & Latin America Pharmacokinetics Services Market Insights

UAE leads MEA revenues at approximately 38.4% through its growing pharmaceutical investment, the biomedical research institute network, and the region's emerging clinical trial infrastructure. Brazil leads Latin American revenues at approximately 44.2% through its pharmaceutical industry's clinical development investment, ANVISA's clinical trial regulatory framework, and the academic research community's PK study capacity.

Saudi Arabia's Vision 2030 pharmaceutical investment and South Africa's established clinical trial infrastructure create significant MEA secondary markets whose PK service procurement reflects the progressive development of domestic pharmaceutical research capability.

Market Dynamics:

Growth Drivers: Expanding biopharmaceutical pipeline and regulatory model-informed drug development adoption

The expanding biopharmaceutical pipeline's increasing complexity is the pharmacokinetics services market's most commercially certain structural growth driver. Each new IND application creates a defined PK service procurement pathway from preclinical ADME through clinical bioanalysis and PK/PD modelling whose service spending per programme compounds with the global active clinical trial count growth. The biologics and gene therapy pipeline's above-average PK complexity creates above-average service procurement per programme that sustains revenue growth above the rate of IND volume increase alone. FDA's 2024 guidance on model-informed drug development creates regulatory motivation for PK/PD modelling service investment that previously discretionary programmes now treat as standard practice.

Regulatory model-informed drug development adoption is simultaneously creating structured PK modelling service demand that was historically a discretionary analytical enhancement. FDA's acceptance of population PK analysis for paediatric extrapolation, EMA's guideline on model-informed drug development, and ICH E11(R1)'s framework collectively create a regulatory expectation that sustains PK modelling service procurement across therapeutic areas and development stages whose combined effect creates systematic market demand growth.

Restraints: High service cost and specialised expertise requirement limiting access for smaller biotechs

High pharmacokinetics service cost creates access barriers for small biotechnology companies whose preclinical and early clinical development budgets require prioritisation of essential PK studies over comprehensive ADME characterisation programmes. Each regulatory-required PK study whose necessary scope creates cost that exceeds the small biotech's available budget requires either scope reduction or service postponement whose commercial impact limits the PK services market's penetration into the small biotech customer segment.

Specialised expertise requirements for complex PK modelling, large molecule bioanalysis, and physiologically based pharmacokinetic modelling create talent constraints that limit service provider capacity expansion pace. The clinical pharmacologist and PK modeller talent pool whose combined academic training, software proficiency, and regulatory experience creates the most commercially limited resource in PK services market supply.

Opportunities: AI-powered PK prediction and emerging market CRO expansion

AI-powered PK prediction platforms represent the most commercially innovative near-term market development direction. Labcorp's 2024 FDA-approved AI PK modelling software demonstrates the regulatory pathway whose successful navigation creates validated AI tools that pharmaceutical clients can specify for regulatory submission quality PK analysis. Each AI capability improvement that reduces modelling timeline while maintaining regulatory acceptance creates commercial value that sustains above-average pricing for AI-enabled PK services.

Emerging market CRO expansion in China, India, and Southeast Asia represents the most commercially significant capacity growth opportunity. Each new CRO facility in these cost-competitive regions that achieves GLP and GCP accreditation creates PK service capacity whose competitive pricing attracts international pharmaceutical client outsourcing. WuXi AppTec's extraordinary expansion demonstrates the commercial model whose successful execution creates significant market share capture from established North American and European PK service providers.

Recent Developments:

-

2023: Charles River Laboratories expanded its pharmacokinetics services portfolio in 2023 by introducing advanced bioanalytical platforms for small molecules and biologics, reflecting the commercial requirement for large molecule PK analytical capability as the biopharmaceutical pipeline's biologics proportion continues to grow.

-

2024: Labcorp received FDA approval in January 2024 for its innovative PK modelling software integrating AI to predict drug behaviour, enabling more efficient clinical development programme design through AI-powered pharmacokinetic prediction and dose optimisation.

-

2024: Certara expanded its Phoenix WinNonlin population PK modelling platform in 2024 with enhanced AI-assisted model selection, covariate analysis automation, and regulatory submission report generation, targeting clinical pharmacologists seeking to reduce modelling time while maintaining regulatory submission quality standards.

Pharmacokinetics Services Market Key Players:

-

Charles River Laboratories International Inc.

-

Covance Inc. (Labcorp Drug Development)

-

ICON plc

-

PAREXEL International Corporation

-

Certara L.P.

-

Eurofins Scientific

-

WuXi AppTec Co., Ltd.

-

Evotec AG

-

SGS SA

-

Frontage Laboratories

-

Pharmaceutical Product Development LLC (PPD)

-

MPI Research

-

GVK Biosciences

-

Envigo (Inotiv)

-

Pacific BioLabs

-

Absorption Systems (Cyprotex)

-

XenoTech by BioIVT

-

Aptuit (Evotec)

-

Creative Bioarray

-

Svar Life Science AB

Pharmacokinetics Services Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.38 Billion |

| Market Size by 2035 | USD 3.02 Billion |

| CAGR | CAGR of 7.70% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Drug Type (Small Molecules, Biologics & Large Molecules) • by Service Type (Bioanalytical Services, PK/PD Modelling & Simulation, In-Vitro ADME Studies, Clinical PK Studies, In-Vivo PK Studies, Others) • by Clinical Phase (Preclinical, Phase I, Phase II, Phase III, Post-Approval) • by End User (Pharmaceutical & Biotechnology Companies, Contract Research Organizations, Academic & Research Institutions, Government & Regulatory Bodies) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Charles River Laboratories International Inc., Covance Inc. (Labcorp Drug Development), ICON plc, PAREXEL International Corporation, Certara L.P., Eurofins Scientific, WuXi, AppTec Co., Ltd., Evotec AG, SGS SA, Frontage Laboratories, Pharmaceutical Product, Development LLC (PPD), MPI Research, GVK Biosciences, Envigo (Inotiv), Pacific BioLabs, Absorption Systems (Cyprotex), XenoTech by BioIVT, Aptuit (Evotec), Creative Bioarray, Svar Life Science AB |

Frequently Asked Questions

The Pharmacokinetics Services Market is expected to grow at a CAGR of 7.70% from 2026 to 2035.

The Pharmacokinetics Services Market was valued at USD 1.38 Billion in 2025.

Expanding biopharmaceutical pipeline complexity requiring sophisticated ADME characterisation and regulatory-quality PK/PD modelling.

Small Molecules dominated the Pharmacokinetics Services Market with approximately 68% share in 2025, while Biologics & Large Molecules is the fastest growing segment.

North America dominated the Pharmacokinetics Services Market with approximately 37.1% revenue share in 2025, with the United States accounting for approximately 87.4% of North American revenues.

Get in Touch