Veterinary Pharmacovigilance Market Report Scope & Overview:

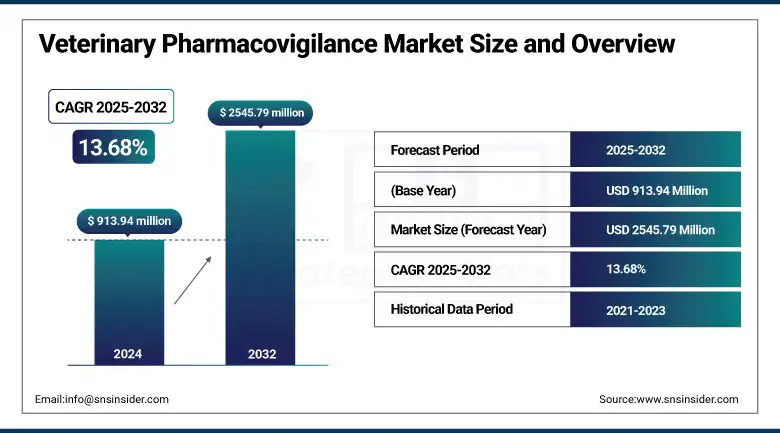

The veterinary pharmacovigilance market size was valued at USD 913.94 million in 2024 and is expected to reach USD 2545.79 million by 2032, growing at a CAGR of 13.68% over 2025-2032.

The veterinary pharmacovigilance market is gaining momentum due to the escalating complexities and application of animal healthcare products, increasing number of regulations, and focus on adverse event monitoring related to both companion and livestock animals. With growth of over 60% of the global veterinary pharmacovigilance market derived from the companion animal segments, the growing number of pets and increased expenditure on animal health are driving demand. The U.S. veterinary pharmacovigilance market is experiencing significant regulations from the FDA-CVM and an increase in ADRs, which require pharmaceutical companies in the U.S. to invest in pharmacovigilance solutions. Additionally, an increase in outsourcing trends suggests that 52.5% of veterinary pharma firms are opting for contract services in comparison to their in-house counterparts is altering the veterinary pharmacovigilance market trends.

To Get more information On Veterinary Pharmacovigilance Market - Request Free Sample Report

Cloud-based integration with AI-enabled signal detection solutions is enabling a 40% reduction in manual intervention in reporting processes. R&D investment in the veterinary Medicines Industry crossed USD 1.2 billion in 2023, and there have been higher allocations toward post-market safety surveillance solutions contributing to veterinary pharmacovigilance market growth. Other regulatory harmonization programs, such as VICH and EMA, are also helping to ensure similar enforcement of pharmacovigilance systems across regions, thereby boosting the growth of the global veterinary pharmacovigilance market. Increasing awareness and slow progress in ADE (adverse drug event) reporting in developing economies is a new possibility, especially as veterinary segment participants prioritize compliance and digitalization.

In March 2024, ArisGlobal launched an enhanced AI-powered safety platform tailored for animal health firms to enhance real-time adverse events detection and assessment.

In other substantial developments, during Q4 2023, Ceva Santé Animale announced a tie-up with a regulatory tech company to transform its global pharmacovigilance activity on the basis of a new cloud-native platform, standing as a momentous veterinary pharmacovigilance market investment.

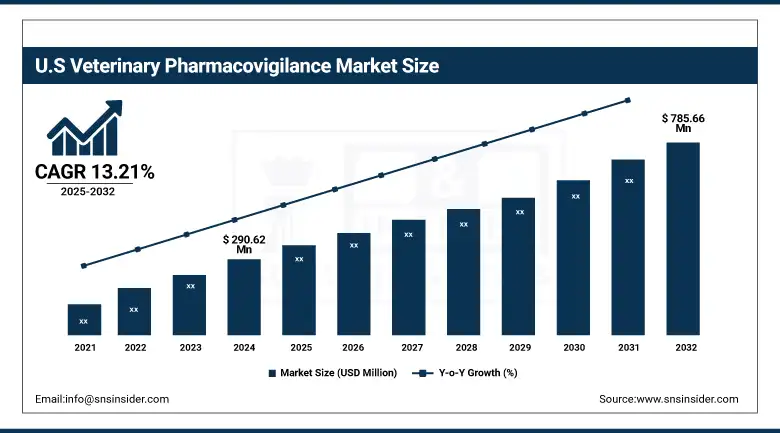

The U.S. veterinary pharmacovigilance market size was valued at USD 290.62 million in 2024 and is expected to reach USD 785.66 million by 2032, growing at a CAGR of 13.21% over 2025-2032. The U.S. dominated the regional industry and was propelled by the requirement of stringent FDA-CVM reporting and the high penetration of the leading veterinary pharmaceutical manufacturers. More than 70% of veterinary ADE reports in North America are from the U.S, indicative of its mature pharmacovigilance infrastructure. In Canada, uptake is gradually increasing, facilitated by public-private partnerships to promote animal health surveillance. The U.S. veterinary pharmacovigilance market also has established key solution providers with AIPV tools, which have lifted it to the leading position.

Market Dynamics:

Drivers:

-

Rising Regulatory Enforcement and Drug Complexity Driving Demand Propel Market Expansion

The global veterinary pharmacovigilance market is driven by the rising incidence of adverse drug reactions, which is the reason for higher demand for the safety of animal health products. As regulatory bodies, such as the EMA require EudraVigilance Vet reporting and the FDA-CVM enforce pharmacovigilance adherence for animal drugs, drug companies must implement effective surveillance systems. Second, the increasing trend of veterinary drug innovation (monoclonal antibodies, gene therapy, and immunomodulators) requires more effective post-marketing safety monitoring.

During 2020-2023, 67.2% of the new veterinary drugs approved had new mechanisms of action, and we should pay more attention to them. Increased public awareness and the mounting threat of litigation in ADEs are also driving investment. Already, in 2023, the world animal health industry has allocated over USD 750 million toward safety compliance and digital monitoring tools. All these factors strongly exercise pressure on demand for integrated platforms, contract pharmacovigilance services, and AI-powered safety analytics as critical aspects of the veterinary pharmacovigilance market growth.

Restraints:

-

Operational Complexity and Low Reporting Awareness is Hindering Market Expansion

The veterinary pharmacovigilance market also encounters some challenges, such as fragmented operational workflows, low harmonization among different countries, and a low level of knowledge among veterinarians and livestock owners. In these low-to-middle-income areas, sub-optimal is significant, and only 15–20% of real adverse events are likely to be reported, given the absence of digital infrastructure and the limited training that health-care workers receive. Besides, it is technically difficult and also costly to incorporate PV systems. Most of the smaller veterinary pharma is still using manual methods or ad-hoc surveillance, resulting in a delayed capacity to detect signals and comply.

A lack of international consistency in the timing of transition to product liability-related reporting requirements, even where guidelines (VICH GL24) and country-specific pharmacovigilance requirements have already been agreed upon, prevents submission in consistent formats and data quality. Furthermore, there are supply-side constraints, such as a lack of trained vet PV professionals, high costs, low penetration of compliance tools, and slow acceptance of the cloud-based software solutions, which make it difficult to scale. These macro-level challenges also limit the growth of the global veterinary pharmacovigilance market analysis and are responsible for lowering the adoption of services in the long run.

Segmentation Analysis:

By Type

The type category was led by the contract outsourcing segment in the veterinary pharmacovigilance market in 2024, with over 61% of the veterinary pharmacovigilance market share on account of animal health companies preferring to work with specialized pharmacovigilance vendors to minimize operational costs and stay globally compliant.

The in-house segment, by type, is the largest and the fastest-growing market, as large veterinary pharmaceutical companies are focusing on improving their internal safety monitoring systems to protect data more securely and deliver faster regulatory reporting turnaround.

By Solution

Based on the solution segment, the services category accounted for the major veterinary pharmacovigilance market share in 2024, with around 68% of the market, due to the growing requirement for professional safety monitoring, case processing, and signal detection, more so among mid-sized organizations.

The software segment is the most promising, driven by the growing adoption of AI-enabled and cloud-based PV solutions, which help in simplifying and enhancing real-time adverse event reporting and automating workflows.

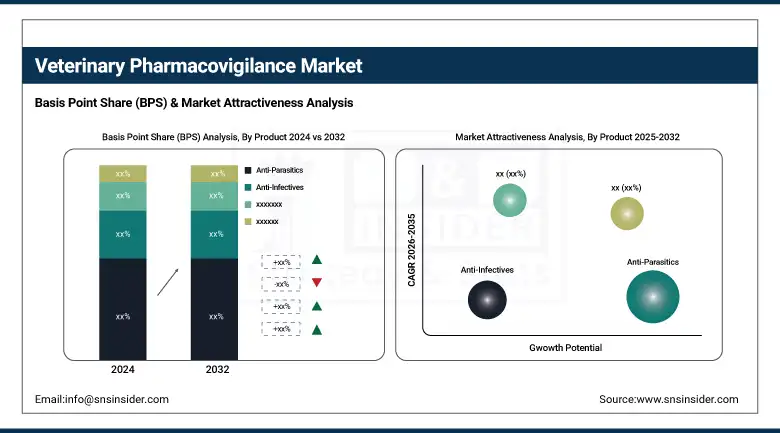

By Product

In the product-wise category, anti-parasitics dominated with about 34% of the share in 2024, since they are widely used in livestock and companion animals, and the risk of adverse drug reactions has increased, which, in turn, is creating a need for pharmacovigilance.

Biologics were the fastest growing, stimulated by increasing approvals of vaccines and monoclonal antibodies, which required comprehensive post-market monitoring for complex safety profiles.

By Delivery Mode

On-premise dominated the market at 58% market share, as regulatory bodies and pharma juggernauts love having full control of their sensitive safety data. The fastest growing mode of delivery is cloud-based, enabled by its cost effectiveness, flexibility, and the growing prevalence of remote PV.

By Animal Type

Dogs were the leading segment, and accounted for a 36% share in 2024, owing to high ownership of companion animals and rising vet visits for medication and monitoring in developed countries.

The livestock segment was the fastest-growing segment, as a result of government initiatives to implement pharmacovigilance frameworks and mandatory reporting in food-producing animals, especially in Europe and APAC.

By End-User

Veterinary pharmaceutical companies were the largest end-user with 41% market share, due to their direct accountability of safety reporting to regulatory bodies and substantial investments in compliance infrastructure.

Regulatory authorities are the fastest-growing end-user, driven by the implementation of new electronic reporting criteria and centralized safety databases, such as the EMA’s Union Pharmacovigilance Database for veterinary medicinal products.

Regional Analysis:

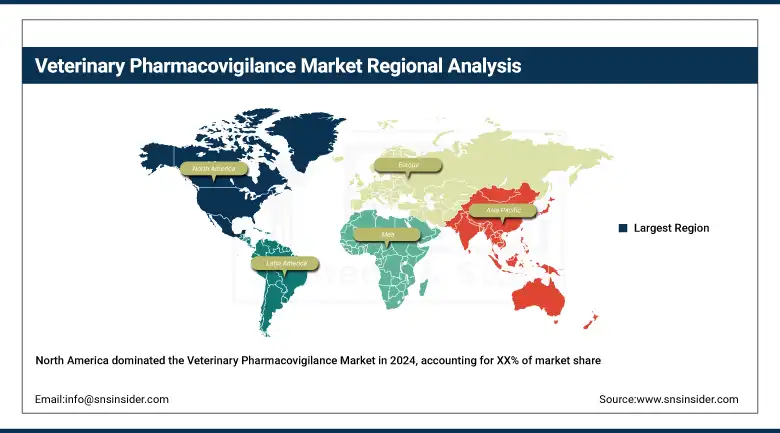

North America was the largest market in 2024 and is anticipated to remain the largest market due to stringent regulatory guidelines, high consumption of veterinary medicines, and a strong digital footprint.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe emerged as the second fastest growing region, underpinned by the introduction of the EU Veterinary Medicinal Products Regulation (Regulation (EU) 2019/6), which came into force in 2022 and enforces centralized pharmacovigilance. Germany is ahead in the region owing to its significant livestock industry and high level of regulatory displacement. The U.K. and France are likewise rapidly progressing, now with digital reporting systems being invested in and also pharmacovigilance service-focused partnership opportunities. The Union Pharmacovigilance Database of the EMA has generated robust demand for formal PV mechanisms in member states, thereby contributing to the veterinary pharmacovigilance market growth.

The Asia Pacific region is the fastest-growing regional segment in the global veterinary pharmacovigilance market, with the high growth in this segment attributed mainly to growth in the livestock population, an increase in the number of veterinary drug approvals, and increased adoption of post-market surveillance. India has taken a headway forward, as it has a large national veterinary pharmaceutical market, and with the improvement of its regulatory system under the CDSCO. China is progressing fast with the support of the government in veterinary R&D and safety monitoring of food-producing animals. Novel Japan is introducing electronic PV reporting systems, such as those for companion animal medicine. An increasing number of regional players and partnerships with international PV companies are driving the regional veterinary pharmacovigilance market.

Key Players:

Leading veterinary pharmacovigilance companies driving the market include ArisGlobal, Accenture, Ennov, Sarjen Systems Pvt. Ltd., Pharsafer Associates Limited, Knoell, Biologit, Indivirtus, Azierta Contract Science Support Consulting, Oy Medfiles Ltd., EXTEDO GmbH, MakroCare, Navitas Life Sciences, Oracle Health Sciences, IQVIA (Animal Health Division), Techsol Corporation, Wingspan Technology (part of IQVIA), Tata Consultancy Services (TCS Life Sciences), PRA Health Sciences (acquired by ICON plc), AB Cube (PV software provider), Sentrx Animal Health, and Syneos Health.

Recent Developments:

In March 2025, ArisGlobal introduced new AI-powered pharmacovigilance solutions, LifeSphere Unify, NavaX Insights, and Advanced Compliance Docs, aimed at streamlining veterinary safety workflows, automating compliance documents, and improving real-time signal detection through cloud-native integration.

In December 2024, a top-tier veterinary pharmaceutical company transitioned to an end-to-end AI-powered cloud platform for pharmacovigilance. The system automates literature surveillance, case processing, and safety reporting, enhancing speed, accuracy, and global regulatory compliance.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 913.94 million |

| Market Size by 2032 | USD 2545.79 million |

| CAGR | CAGR of 13.68% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (In-house, Contract Outsourcing) • By Solution (Software, Services) • By Product (Biologics, Anti-Infectives, Anti-Parasitics, NSAIDs & Analgesics, Other Products) • By Delivery Mode (On-premise, Cloud-based) • By Animal Type (Dogs, Cats, Horses, Livestock [Cattle, Pigs, Poultry], Other Animal Types) • By End-user (Veterinary Clinics & Hospitals, Animal Research Institutes, Veterinary Pharmaceutical Companies, Regulatory Agencies) |

| Regional Analysis/Coverage | North America (U.S., Canada), Europe (Germany, France, UK, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America) |

| Company Profiles | ArisGlobal, Accenture, Ennov, Sarjen Systems Pvt. Ltd., Pharsafer Associates Limited, Knoell, Biologit, Indivirtus, Azierta Contract Science Support Consulting, Oy Medfiles Ltd., EXTEDO GmbH, MakroCare, Navitas Life Sciences, Oracle Health Sciences, IQVIA (Animal Health Division), Techsol Corporation, Wingspan Technology (part of IQVIA), Tata Consultancy Services (TCS Life Sciences), PRA Health Sciences (acquired by ICON plc), AB Cube (PV software provider), Sentrx Animal Health, and Syneos Health. |

Frequently Asked Questions

Trends include AI-driven analytics, real-time adverse event reporting, and cloud PV tools. These innovations enhance efficiency and compliance across the value chain.

North America, especially the U.S., leads due to strict regulations and pharma presence. Europe follows, while Asia Pacific shows the fastest adoption rate.

The market is growing significantly in 2025 due to higher safety compliance and drug monitoring. The U.S. and Asia Pacific are major contributors to this expansion.

Growth is driven by rising animal drug use, regulatory mandates, and digital PV tools. Increasing adverse event reporting and global safety awareness also fuel market expansion.

It refers to monitoring, detecting, and evaluating the adverse effects of animal drugs. The market ensures drug safety for livestock and companion animals through structured reporting systems.

Get in Touch