Piping System of Ultrapure Water for Semiconductor Market Report Scope & Overview:

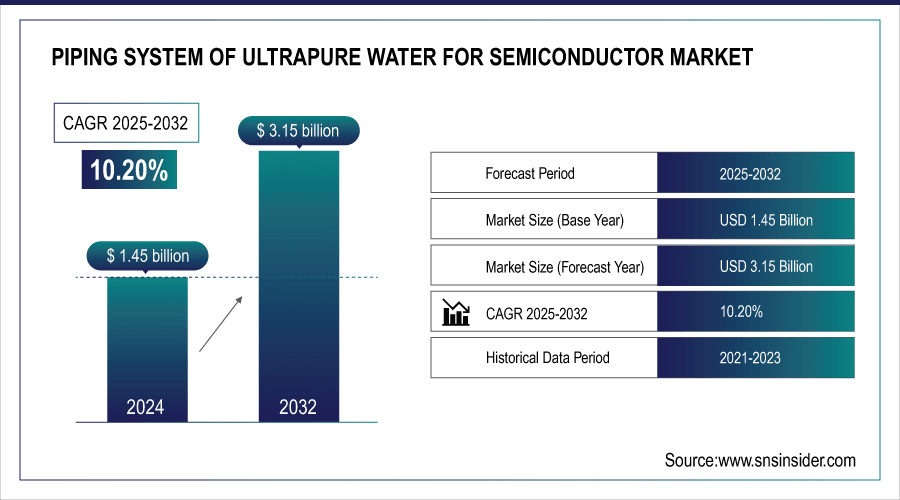

The Piping System of Ultrapure Water for Semiconductor Market Size was valued at USD 1.45 billion in 2024 and is expected to reach USD 3.15 billion by 2032 and grow at a CAGR of 10.20% over the forecast period 2025-2032.

The Global Piping System of Ultrapure Water for Semiconductor Market is primarily driven by the increasing demand for high-purity water in semiconductor fabrication processes. Ultrapure Water (UPW) is necessary for many steps in advanced semiconductor manufacturing, such as wafer cleaning, etching and chemical deposition, where even small contaminants could impact product yield and quality. This dense influx of semiconductor fabs in Asia Pacific, North America, and Europe has generated a high demand for large-scale, non-contaminating piping systems. With the move to advanced nodes (3nm, 2nm and below) comes a need for more robust UPW distribution networks, which in turn requires new materials including PVDF and polypropylene that can withstand the rigours of UPW chemistries during fabrication such as chemical resist, low leach-out and durability. According to study, over 50 new semiconductor fabs are planned globally by 2030, with increasing adoption of advanced 3nm and 2nm nodes requiring high-purity water distribution.

To Get More Information On Piping System of Ultrapure Water for Semiconductor Market - Request Free Sample Report

Piping System of Ultrapure Water for Semiconductor Market Trends

-

Increasing adoption of advanced semiconductor nodes is driving demand for high-purity UPW piping systems.

-

Rapid expansion of global semiconductor fabs is boosting the need for contamination-free water distribution networks.

-

Customized and multi-loop piping systems are gaining traction in modern fabs.

-

Use of robust materials like PVDF and polypropylene ensures chemical resistance and low leach-out.

-

Smart monitoring integration is becoming increasingly important for maintaining water quality and operational efficiency.

-

Technological innovations in piping design are enabling scalable and reliable UPW infrastructure

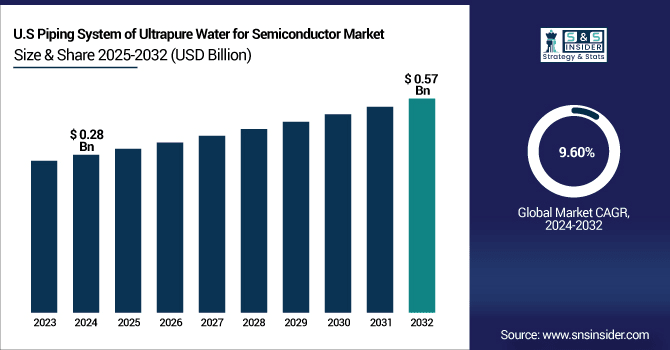

The U.S. Piping System of Ultrapure Water for Semiconductor Market size was USD 0.28 billion in 2024 and is expected to reach USD 0.57 billion by 2032, growing at a CAGR of 9.60% over the forecast period of 2025-2032. Drive by integration of smart monitoring systems, automation, and AI-driven solutions to enhance operational efficiency, reliability, and water quality control.

Piping System of Ultrapure Water for Semiconductor Market Growth Drivers:

-

Rising Demand for Ultrapure Water in Advanced Semiconductor Manufacturing

The market is primarily driven by the increasing demand for ultrapure water (UPW) in advanced semiconductor manufacturing. With smaller nodes (3nm, 2nm), semiconductor fabs which now require high-purity water for critical processes such as wafer cleaning, etching, and chemical deposition, because critical processes yield degrades with impurities affecting product yield. Sufficient chemical durability, minimal leach-out, and contamination-free delivery is guaranteed by materials such as PVDF and polypropylene.The need for reliable UPW piping systems grew with Asia Pacific, North America and Europe fabs in their quest for sustaining production quality and meeting fab expansion with the true UPW (ultra-purified wafer) features.

a single 300mm wafer fabrication plant consumes approximately 1,000–2,000 cubic meters of UPW daily, with purity standards demanding particle counts below 1 per milliliter and conductivity under 0.055 µS/cm.

Piping System of Ultrapure Water for Semiconductor Market Restraints:

-

High Installation and Maintenance Costs Limiting Adoption

UPW piping systems can be very expensive to install and maintain, which is one of the major factors that act as a restraint. Specialized engineering, fittings, and clean room compliant installation are required for advanced materials such as PVDF and multi-loop or customized configurations. Additionally, keeping pipelines free of particles and chemicals in itself creates higher operational costs, especially for smaller fabs or in new semiconductor markets. Furthermore, the regulatory standards for ultrapure water infrastructure are so strict that it can prolong deployment and drive-up costs, making it challenging to deploy in cost sensitive areas despite a boom in demand for the treated water.

Piping System of Ultrapure Water for Semiconductor Market Opportunities:

-

Expansion of Global Semiconductor Fabs Driving Demand

The rising number of new semiconductors fabs globally presents a significant growth opportunity for UPW piping systems. With more than 70 fabs under construction in East Asia and the U.S., high-capacity, contamination-free water distribution networks are in increasing demand. As fabs advance to the next generation of device nodes, twisted, looping, customized piping systems with innovative materials & design and smart monitoring applications are becoming mainstream. Such trend is allowing market enhancement and UPW infrastructure technology advancement.

Rapidus Corporation in Japan is building fabs with 2nm and 1nm technology nodes, showing demand for advanced manufacturing.

Piping System of Ultrapure Water for Semiconductor Market Segment Analysis

-

By type of material, PVDF (polyvinylidene fluoride) led the market with ~40.05% share in 2024, while polypropylene is expected to be the fastest growing segment during 2025–2032, registering a CAGR of 10.99%.

-

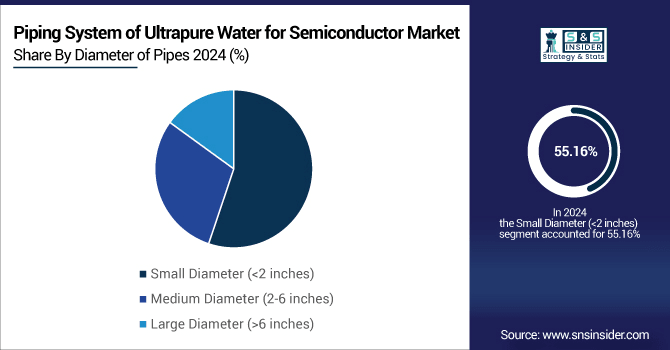

By diameter of pipes, small diameter (<2 inches) accounted for ~55.16% share in 2024, whereas medium diameter (2–6 inches) pipes are projected to grow at the fastest pace with a CAGR of 10.69% over 2025–2032.

-

By system configuration, multi-loop systems dominated the market with ~44.84% share in 2024, while customized pipe systems are anticipated to witness the fastest growth at a CAGR of 12.43% during the forecast period 2025–2032.

-

By application, chip manufacturing held the largest share of ~50.05% in 2024, whereas cleaning and rinsing applications are forecast to expand at the highest CAGR of 11.48% between 2025 and 2032.

-

By end-use industry, semiconductor manufacturing led the market with ~54.80% share in 2024, while the electronics segment is expected to register the fastest growth at a CAGR of 11.41% during 2025–2032.

By Diameter of Pipes, Small Diameter (<2 inches) Leads Market While Medium Diameter (2-6 inches) Fastest Growth

By 2024, Small Diameter (<2 inches) in the Piping System of Ultrapure Water for Semiconductor Market segment will have a huge market share due to its efficiency in providing ease of installation and appropriate flow control option that is commonly found in most standard semiconductor fab applications. Efficient ultrapure water distribution, reduced contamination likelihood, and solution fit to system-specific requirements of compact piping infrastructure with high level of reliability are the key features offered by these systems. Between 2024-2032 Medium Diameter (2-6 inches) segment is expected to register the fastest growth during this time frame, due to needs for higher flow capacity and customized piping loops for chemical delivery systems in fabs, as well as for advanced multi-loop UPW distribution systems. At the same time, in other parts of the market, large-diameter piping solutions are beginning to command greater interest for fabs that continue on the path of expanding and integrating high-vol water systems together.

By Type of Material, PVDF (Polyvinylidene Fluoride) Leads Market While Polypropylene Solutions Fastest Growth

Piping System of Ultrapure Water for Semiconductor PVDF (Polyvinylidene Fluoride) segment is expected to dominate the Global Ultrapure Water for Semiconductor Market demand in 2024, due to excellent chemical resistance, high purity, and high-temperature resistance provided by PVDF, which makes it an ideal material of construction for contamination-sensitive semiconductor fabrication processes. They provide consistent water quality, are built to last, and meet stringent rules and regulations as outlined in industry standards. During this period, the Polypropylene segment is anticipated to experience the fastest growth in 2024–2032, owing to its economical nature, easy installation and other feature which can make it convenient for many applications in semiconductor. At the same time, there are also continuous material innovations being developed in the market where manufacturers are trying to find an equilibrium between the high performing PVDF solution and the more economical polypropylene piping used in the growing UPW infrastructure.

By System Configuration, Multi-Loop Systems Leads Market While Customized Pipe Systems Fastest Growth

n 2024, the Piping System of Ultrapure Water for Semiconductor Market Multi-Loop Systems segment will dominate the market, as they offer advantages such as improved water circulation, redundancy for critical processes, and consistent purity levels across semiconductor fabs. These systems ensure reliable UPW distribution, reduce downtime risks, and align with the industry’s focus on efficiency and contamination control. During this period, the Customized Pipe Systems segment is anticipated to experience the fastest growth in 2024–2032, driven by fabs seeking tailored solutions for unique layouts, advanced nodes, and specialized multi-loop configurations. Simultaneously elsewhere in the market, single-loop systems continue to serve standard applications, maintaining steady adoption in conventional fabs.

By Application, Chip Manufacturing Leads Market While Cleaning and Rinsing Fastest Growth

In 2024, the Piping System of Ultrapure Water for Semiconductor Market Chip Manufacturing segment is dominate the market, due it provides high-purity water distribution, contamination-free processing, and is critical for upstream (etching, deposition, and wafer cleaning) and downstream (dicing, wafer bonding) steps in semiconductor chip manufacturing. It means that these systems guarantee product quality and high yield while maintaining stringent industry standards. During this period, the fastest, 2024–2032 segment of growth is expected to be in the area of Cleaning and Rinsing, driven by fabs needing dedicated UPW systems that can deliver optimal soft and hard particle removal, chemical rinsing and increased equipment lifetime. At the same time, other applications, such as cooling and transport continue to increase at a steady pace, underlying stability of fab operations elsewhere in the market.

By End-User Industry, Semiconductor Manufacturing Leads Market While Electronics Fastest Growth

In 2024, the Piping System of Ultrapure Water for Semiconductor Market Semiconductor Manufacturing segment will dominate the market, as it requires high-purity water for critical fabrication processes, including wafer cleaning, etching, and chemical deposition. These systems ensure consistent water quality, prevent contamination, and support high-yield production in advanced semiconductor fabs. During this period, the Electronics segment is anticipated to experience the fastest growth in 2024–2032, due to the increasing need for high-purity water in electronics assembly, PCB manufacturing, and consumer electronics applications. At the same time, other parts of the market are witnessing new cases of UPW piping solutions being adopted from industries like pharmaceuticals and biotechnology, which can gradually extend top-down market reach.

North America Piping System of Ultrapure Water for Semiconductor Market Insights:

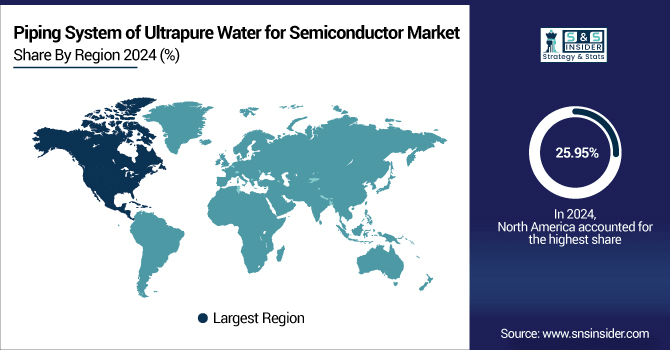

North America emerging the Piping System of Ultrapure Water for Semiconductor Market in 2024 with a 25.95% share owing to the presence of established semiconductor fabs and the early adoption of advanced UPW piping technology. High-purity water distribution system, multi-loop system, and smart monitoring integration guarantee contamination-free operation and enable high-yield manufacturing. Some of the drivers supporting these numbers are the strength of government support within the region, along with the strengthening of the infrastructure and critical market players with a focus on advanced semiconductor nodes.

Get Customized Report as Per Your Business Requirement - Enquiry Now

U.S. Leads Piping System of Ultrapure Water for Semiconductor Market with Policy Support and High-Efficiency Deployment

The U.S. is leading the region by the semiconductor fabs expanding faster, shifting to the 3nm and 2nm advanced nodes and very heterogenous market and high demand for stable reliable UPW systems. The market rate is constantly reinforced by investments in the multi-loop and tailor-made piping solutions, and in sustainable water management aboard. By using smart monitoring and automation, manufacturers make sure that the water is clean, the operations run smooth, and more importantly, they meet all strict industry standards.

Asia-Pacific Piping System of Ultrapure Water for Semiconductor Market Insights

In 2024, Asia Pacific dominated and the fastest-growing region, supported by a CAGR of 10.93%, fueled by rapid fab expansions in China, Taiwan, South Korea, and Southeast Asia. Increasing investments in semiconductor manufacturing, adoption of advanced technology nodes, and modernization of UPW piping infrastructure are driving the market. Manufacturers are focusing on multi-loop and customized systems to meet high-purity water requirements, ensuring efficiency, contamination control, and scalability.

China and India Drive Rapid Growth in Piping System of Ultrapure Water for Semiconductor Market

In China, Taiwan and South Korea, the rapid expansion of semiconductor fabs, advanced nodes (3nm and 2nm) adoption and stringent awareness for contamination free, ultrapure water distribution is driving the market. Rising new fab construction and modification of existing facilities are creating high demand multi-loop and customized UPW piping systems. This is further driving the demand of high purity water infrastructure in the region owing to government initiatives as well as private investments in the semiconductor manufacturing.

Europe Piping System of Ultrapure Water for Semiconductor Market Insights

In 2024, Europe accounted for 20.18% of the Piping System of Ultrapure Water for Semiconductor Market, owing modernization of semiconductor fabs, growing adoption of PVDF and polypropylene piping, and increasing focus on sustainable operations. Countries such as Germany, France, and the UK are implementing advanced UPW distribution systems to improve manufacturing efficiency, ensure consistent water purity, and comply with strict industry standards.

Germany Leads Europe in Piping System of Ultrapure Water for Semiconductor Market Growth

The region is led by Germany and France as a consequence of the early adoption of multi-loop and custom piping systems, incorporation of intelligent monitoring technologies, and strong semiconductor industry. With the help of high purity materials, automation, and process optimization, enterprises are improving water quality management and operational efficiency and sustainability practices. This, coupled with the intense emphasis on energy efficiency along with the reliable distribution of water as well, is yet again expected to drive the demand for the UPW piping system in Europe.

Latin America (LATAM) and Middle East & Africa (MEA) Piping System of Ultrapure Water for Semiconductor Market Insights

Latin America and MEA are poised to serve as developing markets for Piping System of Ultrapure Water for Semiconductor in 2024. Brazil and Mexico and other LATAM countries are adding semiconductor assembly and packaging sites, boosting demand for high-purity, multi-loop, and medium-diameter piping systems. The investments in semiconductor plants and research centers in UAE, Israel, and South Africa is increasing the use of UPW piping solutions that meet the requirements of the stiff chemical resistant and customize them accordingly in MEA. Enhancements in modernization, contamination-free production and government incentives are driving the growth of the market in both regions.

Piping System of Ultrapure Water for Semiconductor Market Competitive Landscap:

Asahi/America specializes in high-purity piping systems for critical water applications in semiconductor fabs. Their Purad® UHP PVDF piping system is manufactured in stringent cleanroom conditions, ensuring ultrapure water quality measured in parts per trillion. Alongside their PP-Pure® return line solutions, Asahi/America focuses on contamination-free water distribution, cost-effective piping options, and providing complete support for semiconductor manufacturers seeking reliable and high-performance UPW systems.

-

In March 2024, Asahi/America introduced the Purad® UHP PVDF piping system, manufactured under stringent cleanroom conditions to meet ultrapure water requirements measured in parts per trillion, alongside their PP-Pure return line solutions.

Entegris is a key supplier of advanced materials and systems for semiconductor manufacturing. The opening of its Korea Technology Center at Hanyang University ERICA Campus highlights the company’s commitment to innovation and customer support. This facility provides end-to-end ultrapure water (UPW) solutions, technical expertise, and research capabilities tailored to semiconductor fabs, enhancing process reliability, operational efficiency, and adoption of advanced UPW distribution technologies in the region.

-

In February 2024, Entegris opened its Korea Technology Center at Hanyang University ERICA Campus, providing advanced technical innovations and end-to-end UPW solutions for semiconductor manufacturers in Korea.

Saint-Gobain is a global leader in high-performance materials and piping solutions for critical industries, including semiconductors. Their Furon® HP PFA 400 tubing is specifically engineered to handle harsh chemicals while maintaining the ultra-high purity required in semiconductor fabrication. Saint-Gobain’s focus on product reliability, compliance with industry standards, and innovation ensures that semiconductor manufacturers can achieve contamination-free water distribution and maintain high yields in advanced manufacturing processes.

-

In January 2024, Saint-Gobain launched Furon® HP PFA 400 tubing, designed for the harshest chemicals and meeting high-purity requirements in semiconductor manufacturing.

Piping System of Ultrapure Water for Semiconductor Market Key Players:

Some of the Piping System of Ultrapure Water for Semiconductor Market Companies

-

GF Piping Systems

-

Asahi/America

-

AGRU

-

Entegris

-

Saint-Gobain

-

Parker Hannifin

-

Swagelok

-

SMC Corporation

-

IPEX

-

SIMONA

-

Pexco

-

Advanced Polymer Tubing (APT)

-

Arkema, Solvay

-

Veolia Water Technologies & Solutions

-

Xylem (Evoqua)

-

Kurita Water Industries

-

Ovivo

-

GEMÜ Group

-

KITZ SCT

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 1.45Billion |

| Market Size by 2032 | USD 3.15 Billion |

| CAGR | CAGR of 10.20% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type of Material (Polypropylene, PVDF (Polyvinylidene Fluoride), Stainless Steel, Silicone, Others) • By Diameter of Pipes (Small Diameter (<2 inches), Medium Diameter (2–6 inches), Large Diameter (>6 inches)) • By System Configuration (Single-Loop Systems, Multi-Loop Systems, Cascade Systems, Customized Pipe Systems) • By Application (Chip Manufacturing, Cleaning and Rinsing, Cooling Systems, Transport and Storage, Others) • By End-use Industry (Semiconductor Manufacturing, Electronics, Pharmaceuticals, Biotechnology, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Taiwan, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Rest of Latin America) |

| Company Profiles | GF Piping Systems, Asahi/America, AGRU, Entegris, Saint-Gobain, Parker Hannifin, Swagelok, SMC Corporation, IPEX, SIMONA, Pexco, Advanced Polymer Tubing (APT), Arkema, Solvay, Veolia Water Technologies & Solutions, Xylem (Evoqua), Kurita Water Industries, Ovivo, GEMÜ Group, KITZ SCT, and Others |

Get in Touch