Plant-Based Food Market Report Scope & Overview:

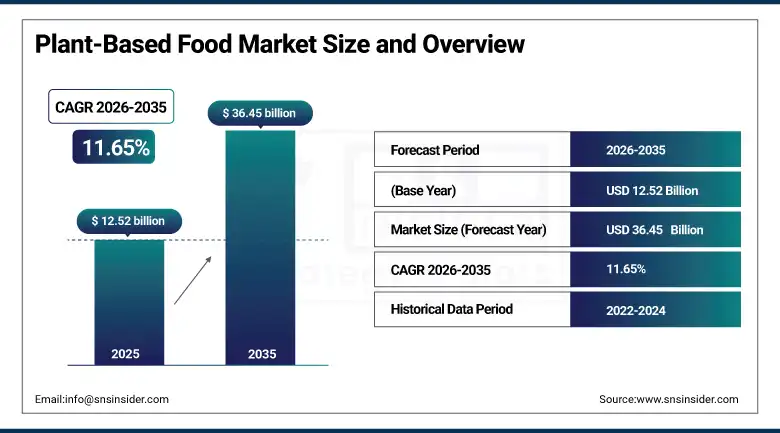

The Plant-Based Food market was valued at USD 12.52 billion in 2025 and is expected to reach USD 36.45 billion by 2035, growing at a CAGR of 11.65% from 2026–2035.

Plant-based food encompasses the rapidly expanding category of food products, serving the growing population of consumers who are motivated by some combination of personal health improvement, environmental sustainability concern, animal welfare consideration, and food allergy or intolerance management to reduce or eliminate animal product consumption. The market encompasses the complete spectrum of plant-based alternative food categories from the meat alternative products that have attracted the most commercial attention and investment through their high-profile mainstream retail and foodservice launches, through the dairy alternative segment whose plant-based milk, cheese, yogurt, butter, and ice cream products have achieved the highest penetration of any plant-based category into conventional grocery baskets, to the emerging plant-based seafood, egg substitute, and RTD beverage categories whose commercial development is still in relatively early stages compared with the mature and competitive meat and dairy alternative segments. Plant-based food consumption reached 8.3 million tons in 2025, driven by the combination of rising demand for protein-rich sustainable alternatives and expanding distribution across retail and foodservice channels that has made plant-based options accessible to mainstream consumers who are not committed vegans or vegetarians but are willing to substitute plant-based alternatives in specific use contexts where the product quality, price, and convenience are competitive with conventional equivalents.

The Good Food Institute's 2025 State of the Industry report confirming that plant-based food retail sales in the United States totaled approximately USD 8 billion across all categories in 2024, representing approximately 2% of total food sales in the categories where plant-based alternatives compete, demonstrates both the substantial commercial scale that the category has achieved and the enormous remaining headroom for growth if plant-based alternatives can overcome the taste, price, and habit barriers that currently limit their penetration to a fraction of the total protein and dairy consumer market.

Market Size and Forecast

-

Market Size in 2026E: USD 13.98 Billion

-

Market Size by 2035: USD 36.45 Billion

-

CAGR (2026 to 2035): 11.65%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Plant-Based Food Market - Request Free Sample Report

Plant-Based Food Market Trends

-

Precision fermentation improves plant-based meat texture using haem proteins and structured plant protein matrices.

-

Clean-label demand is rising for minimally processed plant-based foods with short, recognizable ingredient lists.

-

Foodservice adoption expands as major chains introduce plant-based menus, increasing consumer trial and acceptance globally.

-

Investment is growing in alternative proteins like algae, single-cell, duckweed, and insect-based protein sources.

-

Plant-based products are expanding in sports and functional nutrition with high-protein, performance-focused formulations.

The U.S. Plant-Based Food Market Outlook

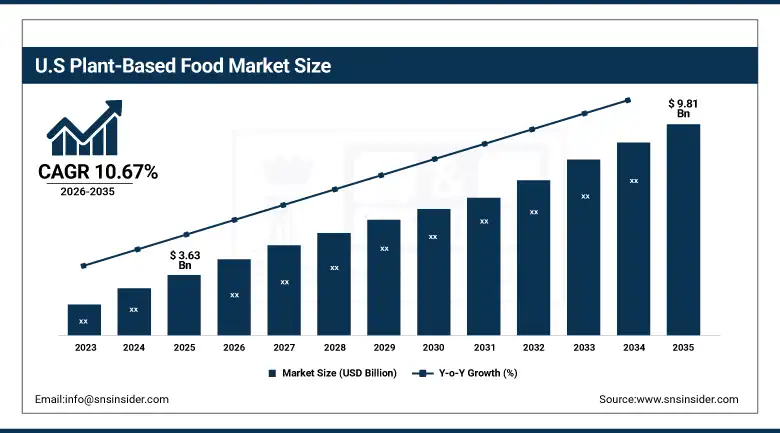

The U.S. Plant-Based Food Market was valued at approximately USD 3.63 billion in 2025 and is expected to reach approximately USD 9.81 billion by 2035, growing at a CAGR of 10.67%. The United States is the commercially developed plant-based food market in terms of product innovation velocity, retail distribution depth, and investment ecosystem activity, anchored by the headquarters of Beyond Meat and Impossible Foods who pioneered the mainstream accessible plant-based burger that transformed the category's commercial profile from health food niche to mainstream CPG investment thesis. U.S. plant-based food retail distribution has reached the point where major plant-based meat, dairy alternative, and egg substitute products are available in virtually every mainstream grocery channel from mass market Walmart and Kroger through premium Whole Foods Market and Sprouts, providing the accessibility necessary for trial purchase by consumers who are not specifically seeking plant-based options but are willing to try them when conveniently co-located with their conventional equivalents. The U.S. market is currently navigating a post-peak demand normalization following the extraordinary growth of 2020 to 2021, with category performance bifurcating between the growing dairy alternative and functional protein segments and the more challenged conventional meat alternative formats whose mainstream trial is not converting to habitual repeat purchase at the rates initial volume growth projected.

The Plant Based Foods Association's 2025 retail sales data showing that plant-based dairy alternatives maintained positive growth while plant-based meat retail volume declined in its third consecutive year of contraction demonstrates the category-level heterogeneity within the plant-based food market that aggregate market statistics can obscure, with the dairy alternative's higher mainstream penetration rate reflecting the successful flavor and texture parity achieved by oat and almond milk specifically in coffee and cereal applications where the sensory comparison point is a liquid product easily replicated.

Plant-Based Food Market Segment Analysis

-

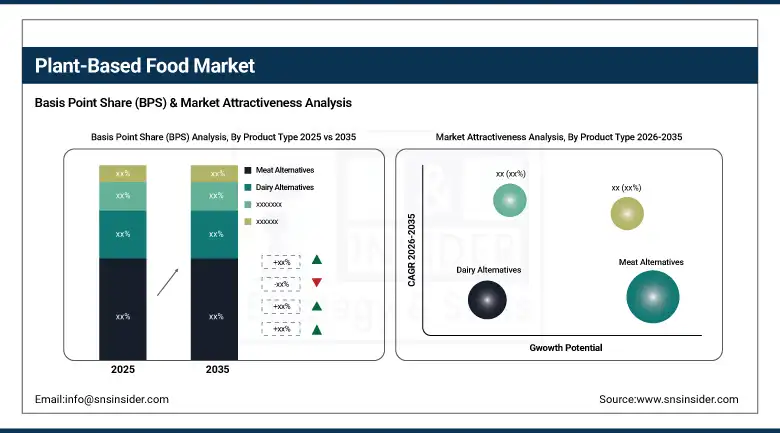

By Product Type, meat alternatives dominated with approximately 38.75% in 2025; dairy alternatives are the fastest-growing segment at a CAGR of 13.20%.

-

By Source, soy dominated with approximately 33.50% in 2025; pea is the fastest-growing at a CAGR of 14.15%.

-

By Application, home consumption led through retail grocery channel plant-based food sales to consumers preparing plant-based meals; food service segment is growing.

-

By Distribution Channel, supermarkets & hypermarkets led with the largest share in 2025; online retail is the fastest-growing channel.

By Product Type, meat alternatives dominate, dairy alternatives are expected to grow fastest

Meat alternatives retained the dominant product type position with approximately 38.75% of the plant-based food market in 2025, reflecting the cumulative commercial investment that has been concentrated in the plant-based burger, sausage, ground meat, and chicken alternative categories that have attracted the most media attention, retail investment, and consumer trial activity of any plant-based food segment. The commercial scale of the meat alternative category reflects both the high per-unit revenue of premium plant-based meat products whose price premiums over conventional meat have been the persistent commercial challenge limiting mainstream adoption, and the foodservice channel's significant contribution through plant-based burger listing at major quick-service restaurant chains that generate high-volume single-channel sales from mainstream consumers who would not seek out plant-based options in retail grocery.

Dairy alternatives are the fastest-growing segment at a CAGR of 13.20% through 2035, driven by the extraordinary commercial success of oat milk whose neutral flavor, creamy texture, and exceptional coffee frothing performance have converted millions of mainstream dairy milk consumers who do not identify as vegan or even flexitarian to habitual oat milk adoption in coffee shop and home beverage preparation contexts, demonstrating that plant-based alternatives can achieve genuine mainstream penetration when product quality in the specific application context matches or exceeds the conventional alternative. The plant-based cheese category, historically the most sensorially challenged dairy alternative, is experiencing accelerating quality improvement through precision fermentation-derived caseins that replicate the melt, stretch, and flavor complexity of conventional dairy cheese in ways that first-generation nut and starch-based vegan cheeses could not achieve.

By Source, soy dominates, pea is expected to grow fastest

Soy retained the dominant source position with approximately 33.50% of plant-based food market revenues in 2025, as the most extensively studied, most widely produced, and most functionally versatile plant protein source whose complete amino acid profile, high protein extraction efficiency, and decades of food manufacturing application experience make it the default formulation choice for plant-based meat, dairy, and protein supplement applications across every major producing region. Soy protein's functional advantages including its ability to form fibrous meat-like textures through thermoplastic extrusion, its gel-forming capability enabling dairy alternative textures, and its relatively neutral flavor after deodorization processing make it the plant protein with the broadest application versatility across the full spectrum of plant-based food product categories.

Pea protein is the fastest-growing source at a CAGR of 14.15% through 2035, driven by its freedom from the top eight allergens that soy triggers, its non-GMO positioning appealing to clean-label consumers who have concerns about genetically modified soy varieties, its neutral flavor profile enabling use in flavor-sensitive applications where soy's beany taste notes require extensive masking, and its rapidly improving functional properties as pea protein processing technology advances toward the isolation and fractionation methods that extract higher-purity protein concentrates with superior water solubility, emulsification, and gelation characteristics.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

85.1% |

|

Europe |

Germany |

25.4% |

|

Asia Pacific |

China |

44.3% |

|

Middle East & Africa |

UAE |

27.8% |

|

Latin America |

Brazil |

43.6% |

North America Plant-Based Food Market Insights

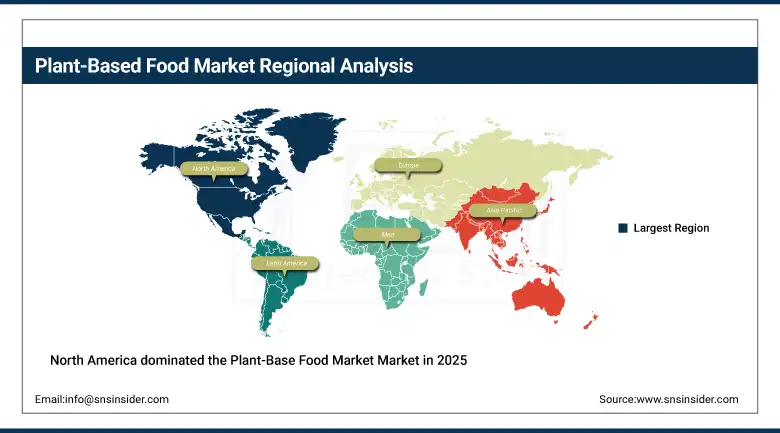

North America dominated the Plant-Base Food Market in 2025, with the United States accounting for approximately 85.1% of North American revenues as the most commercially developed plant-based food market with the broadest product range, deepest retail distribution, and most active innovation ecosystem. The region's market leadership reflects the concentration of major plant-based food brand headquarters including Beyond Meat, Impossible Foods, Oatly America, and Ripple Foods whose product development and marketing investments have established the product quality and consumer awareness that sustain market growth, alongside the most extensive alternative protein research ecosystem at universities including UC Davis, MIT, and Tufts whose food science innovation feeds the commercial product pipeline.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Plant-Based Food Market Insights

Europe is a sophisticated and commercially mature plant-based food market where the combination of strong veganism and flexitarians adoption particularly in the United Kingdom, Germany, and the Netherlands, the most comprehensive food labelling and sustainability disclosure requirements that make environmental product differentiation commercially visible to consumers, and the world's largest plant-based food retail market in absolute sales when European countries are aggregated collectively makes Europe a critical commercial priority for every major plant-based food brand. Germany accounts for approximately 25.4% of European revenues as the EU's largest plant-based food market where the strong consumer preference for organic and sustainable food products has created exceptionally favorable conditions for premium plant-based brand positioning.

Asia Pacific Plant-Based Food Market Insights

Asia Pacific is the fastest-growing plant-based food market, driven by the extraordinary scale of the region's population and the progressive adoption of plant-based protein alternatives across China, India, South Korea, Japan, and Southeast Asia where the combination of traditional soy-based food cultures that make plant protein conceptually familiar, rapidly growing health consciousness creating openness to functional food innovation, and increasingly capable domestic plant-based food brands that are developing culturally appropriate products for Asian palates rather than adapting Western plant-based burger concepts. China accounts for approximately 44.3% of Asia Pacific revenues through its massive consumer market, deep traditional tofu, tempeh, and soy food culture that provides the acceptance foundation for modern plant-based food innovation, and growing middle-class consumer investment in premium health-conscious food products.

MEA & Latin America Plant-Based Food Market Insights

The Middle East and Africa and Latin America are growing plant-based food markets where rising health consciousness among urban middle-class consumers, increasing vegetarian dietary traditions particularly in South Asian expatriate communities in the Gulf states, and the progressive availability of international plant-based food brands in premium grocery retail are creating initial but expanding commercial opportunities. UAE leads MEA revenues at approximately 27.8% through its health-conscious multicultural consumer population and premium grocery retail infrastructure. Brazil leads Latin American revenues at approximately 43.6% through its large urban consumer market, growing vegetarian and flexitarian food culture in major cities, and the active Brazilian plant-based food startup ecosystem.

Market Dynamics

Growth Drivers: Rising consumer health consciousness and environmental sustainability awareness

The primary structural growth drivers for the plant-based food market are the sustained expansion of the flexitarian consumer segment whose occasional plant-based food adoption driven by health and environmental motivation represents the largest addressable commercial opportunity beyond the committed vegan and vegetarian consumer base whose size limits the peak penetration of plant-based alternatives designed exclusively for full animal product replacement, combined with the progressive improvement in plant-based food product quality driven by investment in precision fermentation, advanced protein processing, and AI-enabled formulation optimization that is systematically closing the remaining taste and texture gaps between the best plant-based alternatives and their conventional equivalents in the most commercially significant product categories.

Restraints: Persistent price premium over conventional animal products limiting mainstream adoption among price-sensitive consumer segments

A significant restraint on the plant-based food market is the persistent and commercially significant price premium of plant-based meat and dairy alternatives over conventional equivalents that limits adoption beyond the health-motivated or environmentally committed consumer segments willing to pay premium prices for sustainability-aligned products, while the mass market flexitarian consumer whose plant-based food adoption would drive volume growth at scale remains price-sensitive to premiums that current plant-based food cost structures cannot eliminate without the production scale that mainstream adoption would itself require.

Opportunities: Precision fermentation enabling next-generation ingredient quality that resolves remaining sensory limitations

Precision fermentation, where microorganisms are programmed to produce specific food proteins, fats, and functional ingredients including dairy casein and whey proteins, myoglobin for meat-like taste, and structured fat analogues through fermentation rather than animal agriculture, represents the most transformative ingredient technology for plant-based food quality improvement, as precision fermentation-derived dairy proteins can match the functional and nutritional properties of conventional dairy ingredients exactly because they are biologically identical rather than merely analogous, enabling plant-based dairy alternatives whose cheese stretch, yogurt tartness, and ice cream creaminess are indistinguishable from their dairy equivalents.

Recent Developments:

-

2026: Beyond Meat launched Beyond Immerse, a plant-based protein beverage representing strategic product portfolio diversification beyond meat alternatives into the functional nutrition beverage category, leveraging its brand recognition among health-motivated consumers to enter the growing plant-based protein supplement market.

-

2026: Impossible Foods partnered with Equii to develop protein-enhanced plant-based meals incorporating Equii's high-protein wheat fermentation technology, combining Impossible's brand and distribution reach with Equii's novel protein enrichment process to create plant-based convenience meal products targeting the health and performance nutrition consumer segments.

-

2025: Danone acquired Kate Farms to strengthen its plant-based and specialized nutrition portfolio, integrating Kate Farms' plant-based medical and general nutrition formulas into Danone's healthcare nutrition business and extending its reach into the growing plant-based medical food segment.

Plant-Based Food Market key players are:

-

Beyond Meat Inc.

-

Impossible Foods Inc.

-

Oatly Group AB

-

Danone S.A. (Alpro, Silk)

-

Nestlé S.A. (Garden Gourmet, Sweet Earth)

-

Unilever plc (The Vegetarian Butcher)

-

Tyson Foods Inc. (Raised & Rooted)

-

Kellogg Company (MorningStar Farms)

-

Ripple Foods

-

Eat Just Inc.

-

Nature's Fynd

-

Lightlife Foods

-

Gardein (Conagra Brands)

-

Tofurky (Field Roast)

-

Violife (Upfield Group)

-

Follow Your Heart (Vegenaise)

-

Miyoko's Creamery

-

Forager Project

-

JUST Inc.

-

Renegade Foods

Plant-Based Food Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 12.52 Billion |

| Market Size by 2035 | USD 36.45 Billion |

| CAGR | CAGR of 11.65% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Meat Alternatives, Dairy Alternatives, Seafood Alternatives, Baked Goods & Confectionery, RTD Beverages, RTE Meals, Others) • By Source (Soy, Pea, Wheat, Canola, Lentil, Others) • By Application (Home Consumption, Food Service, Food Processing) • By Distribution Channel (Supermarkets & Hypermarkets, Specialty Stores, Online Retail, Foodservice, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Beyond Meat Inc., Impossible Foods Inc., Oatly Group AB, Danone S.A. (Alpro, Silk), Nestlé S.A. (Garden Gourmet, Sweet Earth), Unilever plc (The Vegetarian Butcher), Tyson Foods Inc. (Raised & Rooted), Kellogg Company (MorningStar Farms), Ripple Foods, Eat Just Inc., Nature's Fynd, Lightlife Foods, Gardein (Conagra Brands), Tofurky (Field Roast), Violife (Upfield Group), Follow Your Heart (Vegenaise), Miyoko's Creamery, Forager Project, JUST Inc., Renegade Foods |

Frequently Asked Questions

North America dominated the plant-based food market in 2025.

Meat Alternatives dominated with approximately 38.75% of revenues in 2025.

The plant-based food market was valued at USD 12.52 billion in 2025.

The plant-based food market is expected to grow at a CAGR of 11.65% from 2026 to 2035.

Get in Touch