Plasticizers Market Report Scope & Overview:

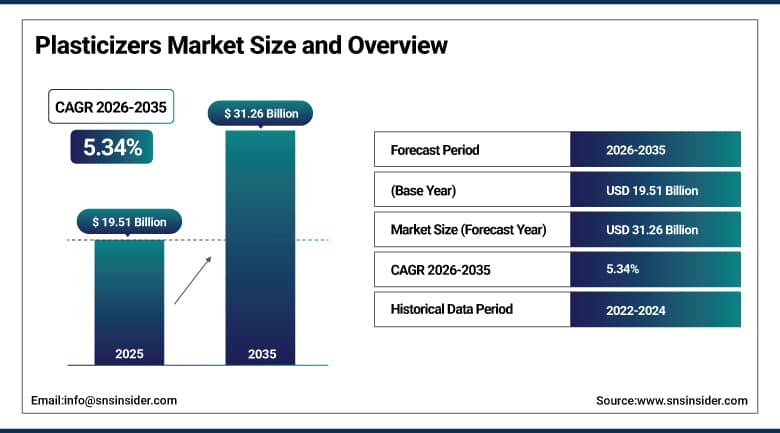

The Plasticizers Market was valued at USD 19.51 Billion in 2025 and is expected to reach USD 31.26 Billion by 2035, growing at a CAGR of 5.34% from 2026 to 2035.

There are many reasons why The Plasticizers Market is changing. First, this report looks at the variations in prices of raw materials, with a particular focus on supply shortages that influence costs in the global market. Next, it analyzes the geographical segmentation of plasticizers, looking into the emerging market of Asia Pacific, as well as diverse trends in North America and Europe. The new focus on sustainability in this market has resulted in government subsidies that encourage the use of green plasticizers. Finally, it looks at the role of trade policies in affecting the plasticizers market, along with their environmental effects.

In January 2024, Evonik Industries expanded its line of eco-friendly chemicals by launching a new high performance, non-phthalate plasticizer that is suitable for vital applications such as the making of tubing used in hospitals as well as food packaging. The launch of this product will help address the increasing demand for non-toxic plasticizers in applications that must meet strict compliance requirements due to human and food contact.

Market Size and Forecast

-

Market Size in 2026E: USD 20.55 Billion

-

Market Size by 2035: USD 31.26 Billion

-

CAGR: 5.34% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get More Information On Plasticizers Market - Request Free Sample Report

Plasticizers Market Trends

-

Regulatory pressure on phthalates in Europe and North America is increasing demand for compliant non-phthalate and bio-based alternatives.

-

Renewable energy expansion drives demand for weather-resistant cables requiring advanced high-performance plasticizer formulations in solar and wind systems.

-

Government housing and infrastructure programs boost plasticizer use in pipes, flooring, and wall coverings in developing economies.

-

Bio-based plasticizers from plant oils and sugars gain traction due to sustainability demand and circular economy regulations in Europe.

-

Electric vehicle growth increases plasticizer applications in lightweight interior components and complex automotive wire harness systems.

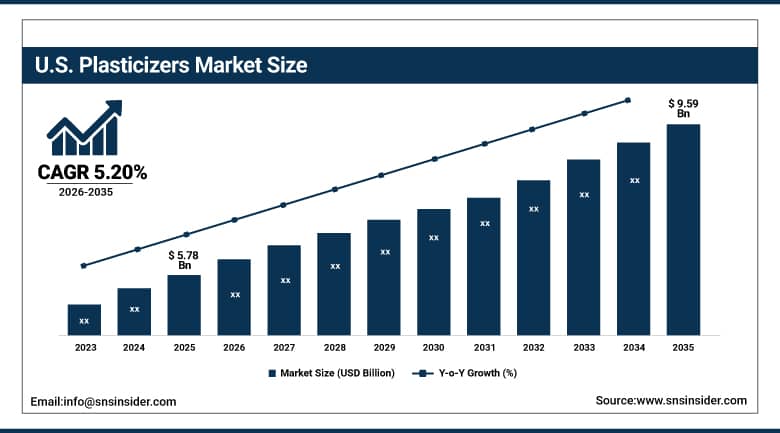

The U.S. Plasticizers Market Outlook

The U.S. Plasticizers Market was valued at approximately USD 5.78 Billion in 2025, and is expected to reach approximately USD 9.59 Billion by 2035, growing at a CAGR of approximately 5.20%.

The U.S. Plasticizers Market is witnessing growth on account of increased demand in various applications like automobile, construction, and medical applications. The shift to non-phthalate plasticizers is being promoted as people seek out health and environmental benefits with companies like ExxonMobil leading the charge when it comes to developing eco-friendly solutions. American Chemistry Council has emphasized the need for production of safer chemicals. Moreover, the growing wire and cable industry in America is adding to the increasing demand for plasticizers, with Eastman Chemical Company concentrating on producing high-performance plasticizers for this application.

The company BASF SE increased its manufacturing capacity for environmentally friendly plasticizers at its Ludwigshafen plant, Germany, in February 2024 as a reaction to the growing demand for plasticizers that have low emissions of VOC and are REACH compliant in both Europe and North America. The growth in capacity shows the commercial implications of how the shift in demand for the regulated plasticizer formulations has taken place, where those manufacturers unable to manufacture non-phthalate grades find themselves at a disadvantage due to the regulations.

Plasticizers Market Segment Analysis

-

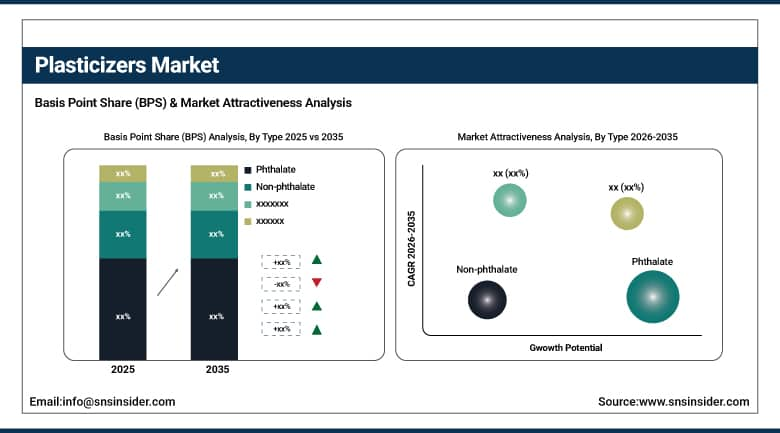

By Type, the phthalate segment dominated the plasticizers market in 2025 with a market share of 59.4%, while the non-phthalate segment is fastest growing.

-

By Application, the wires & cables segment dominated the plasticizers market in 2025 with a market share of 29.7%, while the floorings & wall coverings segment is fastest growing.

-

By Polymer Type, the PVC segment dominated the plasticizers market in 2025 with a market share of 72.1%, while the polyurethane segment is the fastest-growing segment.

-

By End-use Industry, the building & construction segment dominated the plasticizers market in 2025 with a market share of 38.4%, while the healthcare segment is the fastest-growing segment.

By Type, phthalate dominates, non-phthalate grows

Plasticizer type was the most prominent among all market segments and accounted for a 59.4% share of the plasticizers market in 2025. Among plasticizer types, Dioctyl Phthalate is the highest market revenue segment because of its high performance capability, cost-effectiveness, and industrial applicability. DOP has good efficiency and compatibility with PVC; therefore, it is extensively used as a plasticizer in vinyls. With its applications including insulation for cables and walls, and in flooring applications, DOP improves flexibility and longevity that are required for the application performance. Besides, other phthalates include Diisononyl Phthalate and Diisodecyl Phthalate which are extensively used in the automobile and construction industries due to their low volatility and weathering properties.

The Non phthalate segment is growing as regulatory restrictions and consumer safety preferences drive systematic substitution toward safer alternatives. The transition is particularly pronounced in European and North American markets where regulatory bodies including the EPA and ECHA have enacted restrictions on specific phthalate applications. Each product category that shifts specification from phthalate to non-phthalate formulations create structured demand for alternatives including DPHP, DINCH, citrates, and bio-based plasticizers whose premium pricing sustains above average revenue growth relative to volume-based phthalate alternatives.

By Application, wires and cables dominates, floorings and wall coverings grows fastest

Wires and cables dominated the plasticizers market in 2025 with a market share of 29.7%. The growth in dominance can be credited primarily to the growing global demand for electricity, telecommunication systems, and electronics, which in turn need robust and flexible wiring solutions. The use of plasticizers such as phthalates like DOP and DINP is necessary to provide flexibility to the PVC used in the insulation and sheathing of wires and cables. The urbanization of the developing nations, along with large scale infrastructure projects such as the Smart Cities mission in India and the Belt and Road initiative in China, are important drivers for the rising demand for wires and cables.

Floorings and wall coverings continue to represent a significant and growing application as urbanization drives demand for moisture resistant, durable, and aesthetically versatile vinyl flooring products across both residential and commercial construction markets. Each new residential construction project and commercial renovation that specifies vinyl flooring creates plasticizer procurement whose commercial aggregate across global construction activity sustains this application segment's consistent demand trajectory throughout the forecast period.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

69% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

Asia Pacific Plasticizers Market Insights

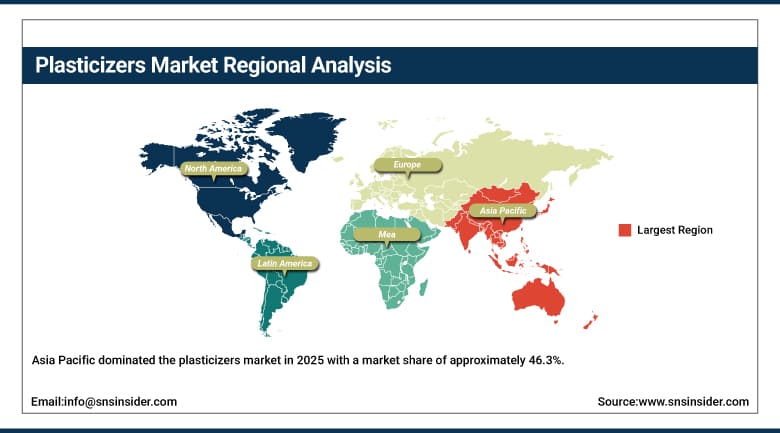

Asia Pacific dominated the plasticizers market in 2025 with a market share of approximately 46.3%, driven by strong demand from construction, automotive, and packaging industries across China, India, and Southeast Asia. A strong supply chain, along with the presence of several PVC and plasticizer manufacturers, is responsible for the high-cost effectiveness of production in the region. Government policies like “Made in China 2025” policy and “Smart City Mission” of India have been supportive of investments in industrial and manufacturing sectors that drive plasticizer market growth. China is responsible for around 44.8% revenue of the Asia Pacific region owing to its huge PVC production.

India represents the most commercially dynamic emerging market within Asia Pacific where the surge in real estate and infrastructure development under programs like Pradhan Mantri Awas Yojana has boosted consumption of plasticizers in flooring, cables, and wall coverings, while Southeast Asian nations witness strong investments in electronics manufacturing and automotive assembly.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Plasticizers Market Insights

North America emerged as the fastest-growing region in the plasticizers market during the forecast period, registering a CAGR of 5.6%. This growth is primarily driven by the rising demand for sustainable and non-phthalate plasticizers, advancements in manufacturing technologies, and increasing investments in construction and renewable energy projects. The United States accounts for approximately 69% of North American revenues through ExxonMobil, Eastman Chemical Company, BASF's domestic operations, and other major plasticizer manufacturers.

The contribution from Canada is an important part of North American revenue generation from the construction industry growth and the increased use of phthalate-free plasticizer formulations in response to regulation conformity with U.S. and international safety guidelines.

Europe Plasticizers Market Insights

Europe is a technically sophisticated plasticizers market where EU REACH regulatory frameworks drive demand for low migration and low toxicity formulations that comply with food contact and consumer product safety requirements. Germany accounts for approximately 22.3% of European revenues through BASF's domestic manufacturing headquarters and the country's strong automotive and construction polymer processing industries.

The UK and France are important secondary markets because their polymer processing industries have grown and because their sustainability policies require constant purchasing of plasticizers. The German-based company headquarters of Evonik Industries, together with other specialty chemical companies located throughout Europe, ensures supply in the plasticizer markets of Europe.

MEA & Latin America Plasticizers Market Insights

Saudi Arabia leads MEA revenues through its rapidly developing petrochemical and construction sectors that create substantial domestic plasticizer demand alongside regional export operations, supported by ongoing industrial diversification investment under Vision 2030 economic transformation programs across multiple industrial sectors. The UAE's growing construction and manufacturing sector adds complementary regional demand.

Brazil dominates Latin America’s income streams due to its extensive construction and automotive production industries, which need steady supply of plasticizers. Mexico’s burgeoning manufacturing industry and construction industry in Argentina contribute towards the continued growth of the market until 2035.

Market Dynamics

Growth Drivers: Electrical and electronics industry expansion and infrastructure development

The expansion of the electrical and electronics sector is significantly driving demand for plasticizers. Electrical products such as wires and cables need greater flexibility and strength so that they can withstand the harshness of heat and mechanical stress. The fast development of technologies taking place globally in industries like telecommunication, renewable energy, and electric cars is creating a demand for flexible and strong materials. Plasticizers are essential in ensuring this requirement. The development of the electronic industry in the wake of smartphones and wearable electronics has also created a demand for high-performance materials.

Both LG Chem and ExxonMobil have been able to respond to this need by offering customized plasticizers that help make sure that the electrical parts are up to required standards of performance and safety. In the growing renewable energy industry, owing to the rise in investment in solar panel production and electric vehicles, plasticizers play an important role in making flexible cables and other parts perform optimally. As the demand for new electronics increases, the Plasticizers Market stands to gain from further innovations and an expanded consumer base in the electronics industry.

Restraints: Regulatory constraints on phthalates increasing development costs

Regulatory constraints surrounding phthalates and other harmful chemical additives continue to be a significant restraint in the Plasticizers Market. All around the world, governments are becoming more and more stringent in their regulations regarding the chemicals that have been found to be hazardous for humans and the environment. In parts of the world such as Europe and North America, phthalates are under intense investigation and are being found in consumer goods and medical equipment. Bans have been placed on certain uses of phthalates by organizations like the FDA and ECHA.

This situation forces manufacturers to use safer and non-toxic substitutes. But there is the problem that the development of plasticizers without phthalates usually requires increased research and development expenses, because companies should make sure that these substitutes can fulfill all the necessary requirements regarding durability for various industries like automotive, construction, and packaging. In addition, the growth of traditional plasticizers may be restricted by regulation, which results in increased product prices.

Opportunities: Bio-based plasticizers and sustainable packaging

The growing trend towards sustainability in packaging is creating a significant opportunity for the Plasticizers Market, particularly through the increasing adoption of bio based plasticizers. There have been many criticisms for the use of traditional petroleum-based plasticizers because of their environmental effects. Therefore, it has become necessary to find a solution that is environment-friendly. The use of bio-based plasticizers is one such answer.

As consumer demand for environmentally responsible products grows, the packaging industry is turning to these bio based solutions to reduce the carbon footprint and improve sustainability. The EU’s Circular Economy Action Plan and other government policies are aimed at encouraging manufacturers to phase out the use of harmful chemicals in their packaging products. Companies such as BASF and Evonik have seen the importance of the use of bio-based plasticizers and have therefore developed innovative technology for the production of these materials.

Recent Developments:

-

2026: Eastman Chemical Company expanded its Tritan and non-phthalate plasticizer portfolio in January 2026 to support growing demand for food-contact and medical-grade applications.

-

2026: BASF SE advanced capacity optimization initiatives in March 2026, strengthening production efficiency for high-performance plasticizer intermediates across European facilities.

-

2026: Evonik Industries AG introduced enhanced specialty plasticizer solutions in 2026 focused on improving flexibility and regulatory compliance for sensitive healthcare applications.

-

2026: LG Chem Ltd. expanded its PVC and polymer additive product line in 2026 to meet rising demand from automotive and construction industries across Asia Pacific.

Plasticizers Market Key Players are:

-

BASF SE

-

Evonik Industries AG

-

ExxonMobil Chemical Company

-

Eastman Chemical Company

-

LG Chem Ltd.

-

Perstorp Holding AB

-

Nan Ya Plastics Corporation

-

UPC Technology Corporation

-

Polynt S.p.A.

-

Lanxess AG

-

Hanwha Solutions Corporation

-

Aekyung Petrochemical Co. Ltd.

-

KH Neochem Co. Ltd.

-

OQ Chemicals (formerly Oxea GmbH)

-

Repsol S.A.

-

Valtris Specialty Chemicals

-

Shandong Qilu Plasticizers Co. Ltd.

-

Zhejiang Jianye Chemical Co. Ltd.

-

Hefei TNJ Chemical Industry Co. Ltd.

-

DIC Corporation

Plasticizers Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 19.51 Billion |

| Market Size by 2035 | USD 31.26 Billion |

| CAGR | CAGR of 5.34% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Phthalate, Non-phthalate) • By Polymer Type (Polyvinyl Chloride (PVC), Rubber, Acrylics, Polyurethanes, Others) • By Application (Wires & Cables, Floorings & Wall Coverings, Films & Sheets, Coated Fabrics, Consumer Goods, Others) • By End-use Industry (Building & Construction, Automotive, Electrical & Electronics, Packaging, Healthcare, Consumer Goods, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BASF SE, Evonik Industries AG, ExxonMobil Chemical Company, Eastman Chemical Company, LG Chem Ltd., Perstorp Holding AB, Nan Ya Plastics Corporation, UPC Technology Corporation, Polynt S.p.A., Lanxess AG, Hanwha Solutions Corporation, Aekyung Petrochemical Co. Ltd., KH Neochem Co. Ltd., OQ Chemicals (formerly Oxea GmbH), Repsol S.A., Valtris Specialty Chemicals, Shandong Qilu Plasticizers Co. Ltd., Zhejiang Jianye Chemical Co. Ltd., Hefei TNJ Chemical Industry Co. Ltd., DIC Corporation |

Frequently Asked Questions

The Plasticizers Market is expected to grow at a CAGR of 5.34% from 2026 to 2035.

Asia Pacific dominated the Plasticizers Market.

Phthalate plasticizers dominated the Plasticizers Market in 2025 with a market share of 59.4%.

The expansion of the electrical and electronics sector driving demand for flexible and durable materials in wires, cables, and electronic components.

The Plasticizers Market was valued at USD 19.51 Billion in 2025.

Get in Touch