Polymer Binders Market Report Scope & Overview:

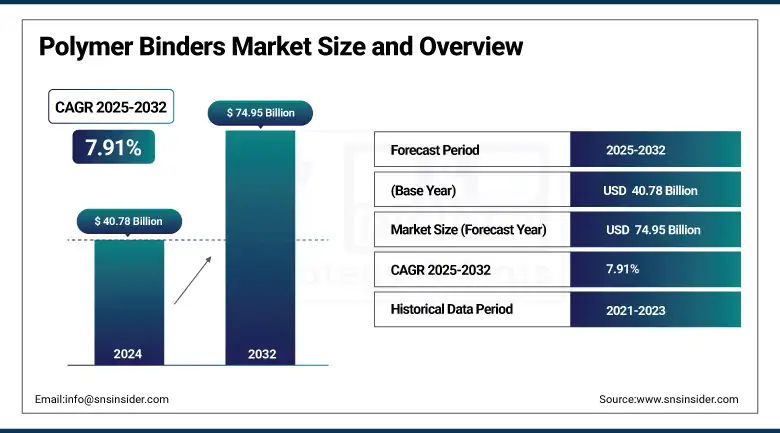

The Polymer Binders market size was valued at USD 40.78 billion in 2024 and is expected to reach USD 74.95 billion by 2032, growing at a CAGR of 7.91% over the forecast period of 2025-2032.

The global polymer binders market is experiencing robust growth due to emerging green trends, compliance with regulations, and higher requirements for low-VOC products. Advancements in acrylic polymer binders, including BASF ACRONAL MB containing biomass-balanced content, are gaining popularity in coatings and adhesives. Increasing consumption of ethyl cellulose binder in pharmaceutical and packaging-related sectors, supported by an increase in the adoption of electric vehicles propelled by the use of anode-grade binders such as Licity, is stimulating polymer binder rents. Polymer binder companies such as BASF are expanding strategically and also following evolving polymer binder market trends across Asia-Pacific. Construction spending, which approached $2.2 trillion in 2024 in the U.S., supported demand in coatings and sealants. Currently, the polymer binders industry is projected to have a 1.4% year-over-year growth rate through April 2025. These advancements are contributing to the polymer binders market size, affecting polymer binders market share, and shaping the global polymer binders market analysis.

To Get more information On Polymer Binders Market - Request Free Sample Report

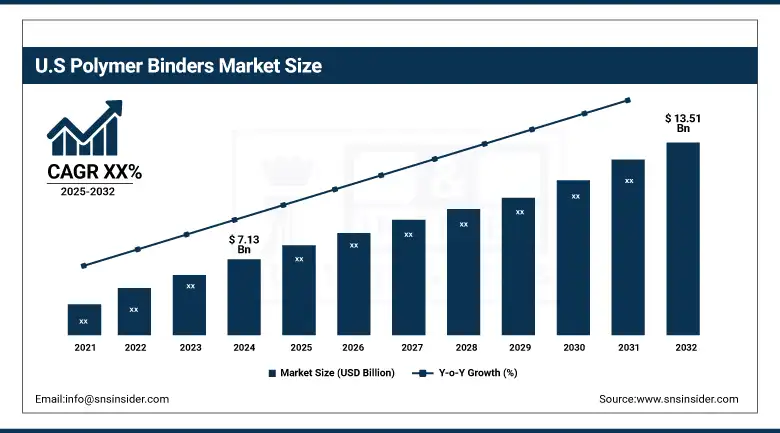

The U.S. dominates within North America with a market size of USD 7.13 billion in 2024 and is projected to reach USD 13.51 billion by 2032. It benefits from EPA guidelines promoting acrylic polymer binder use in low-VOC applications and increased investments by polymer binders companies in bio-based binder technologies. Canada’s growth is fueled by rising infrastructure projects aligned with sustainability goals. These dynamics reflect positive polymer binders market trends and robust polymer binders market growth in the region.

Market Dynamics:

Drivers:

-

Growing electric vehicle production increases demand for specialized anode polymer binders

Worldwide, more than 17 million electric cars were sold in 2024, representing over 20% of all light‑duty vehicle sales. This increase has driven demand for high‑performance ethyl cellulose binder grades used in lithium‑ion battery anodes, which represent a fast-growing arm of the polymer binders market. Companies involved in polymer binders have begun to announce year‑over‑year order increases for battery-grade binders, which demonstrates how automotive electrification is increasing the polymer binders market size. The same trend is also valid for polymer binder market analyses, now more focused on energy storage applications.

-

Expansion of global construction investments stimulates architectural coatings binder consumption

U.S. construction spending was USD 2.163 trillion in December 2024, increasing 1.4% year-over-year through April 2025, according to U.S. Census Bureau data. The upswing in investment has resulted in increased consumption of architectural coatings, and hence, in the volume of acrylic polymer binders in the polymer binders market. Large polymer binder manufacturers are expanding their production to support increased coatings in the residential and commercial application segments. The construction‑related dynamics remain the backbone of any sound polymer binders market growth forecast and polymer binders market trends analysis.

Restraints:

-

Competition from alternative biobased adhesive technologies limits polymer binders industry growth

USDA’s BioPreferred Program reports that biobased products contributed $489 billion to the U.S. economy in 2021, a 5.1% increase over 2020. Incentives for bio‑adhesives and biopolymers are drawing formulators away from traditional polymer binders, curbing polymer binders' market share in segments like packaging and textiles. This shift underscores a key restraint on the polymer binders market size, as decision‑makers integrate renewable alternatives. Tracking these competitive pressures is essential for accurate polymer binders market analysis and forecasting.

Segmentation Analysis:

By Type

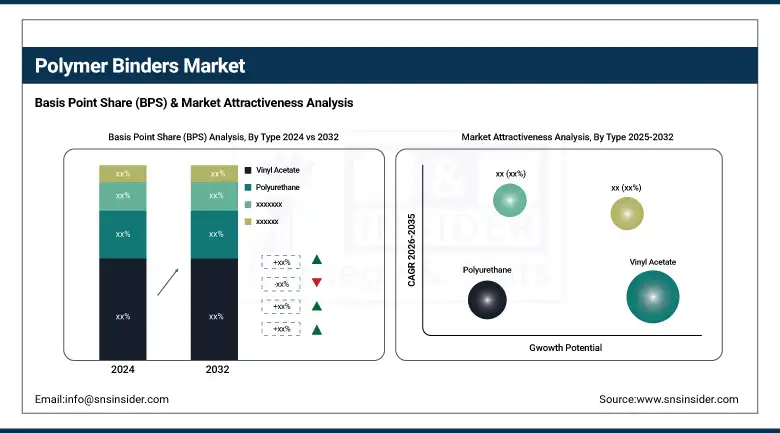

Vinyl acetate dominated with a 34.0% market share in 2024, driven by its strong presence in architectural coatings. The emulsion-grade vinyl acetate segment remains a top choice due to superior binding strength, film integrity, and affordability. The U.S. Green Building Council’s LEED initiatives and the EPA’s VOC emission regulations have directly boosted adoption in low-VOC paints. Additionally, public sector infrastructure projects increasingly mandate environmentally compliant coatings, strengthening vinyl acetate's hold in the polymer binders market. The National Institute of Building Sciences also recognizes its contribution to green building compliance.

Acrylic polymer binder emerged as the fastest-growing segment with an 8.26% CAGR in 2024, primarily due to its waterborne formulations. Acrylic binders have gained significant traction across adhesives, sealants, and flexible coatings, supported by rapid industrial adoption. The EPA’s Clean Air Act standards encourage replacement of solvent-borne systems, boosting acrylic-based solutions. Furthermore, Dow and BASF have announced new investments in bio-based and high-solids acrylic dispersions, aligning with rising sustainability trends. Government-supported research into energy-efficient coating applications further underpins acrylic’s expansion across the polymer binders industry, notably in environmentally regulated North American and European markets.

By Form

Powder-based binders dominated the polymer binders market with a 41.5% share in 2024, supported by energy-efficient and VOC-free features. Powder polymer binders are widely adopted in building materials and protective coatings due to their solvent-free, eco-compliant characteristics. The U.S. Department of Energy continues to endorse powder coatings for energy savings and waste reduction, strengthening their market position. These binders offer enhanced storage stability and are ideal for humid environments. Their recyclability and lower environmental footprint resonate with public infrastructure policies and sustainable building codes, establishing powder binders as a durable, cost-effective segment with broad commercial and regulatory support.

Liquid polymer binders were the fastest-growing segment in 2024 with an 8.29% CAGR, driven by waterborne and high-solids variants. Liquid binders are popular in flexible adhesives, coatings, and sealants, especially where smooth application and fast drying are required. The EPA actively promotes waterborne liquid solutions under the Safer Choice program, making them ideal for indoor and industrial uses. Major manufacturers like Arkema and Celanese have introduced low-VOC liquid formulations, enhancing adoption. Demand for advanced architectural finishes and green-certified materials continues to expand this segment across both developed and emerging markets, accelerating polymer binders market growth overall.

By Application

Paints and coatings dominated with a 37.5% market share in 2024, owing to high demand for eco-friendly formulations. Acrylic polymer binders in paints and coatings offer strong adhesion, chemical resistance, and weather durability, critical for modern architectural and industrial applications. EPA’s national VOC guidelines and LEED mandates for green construction are major drivers behind this dominance. Leading polymer binders companies have introduced multifunctional binder technologies to support evolving coating systems. Government investments in residential construction and infrastructure modernization, especially in the U.S., continue to stimulate this segment’s expansion, reinforcing its role in polymer binders market share leadership.

Adhesives were the fastest-growing application segment with an 8.76% CAGR in 2024, fueled by the packaging and building sectors. Ethyl cellulose binder technologies are gaining traction for biodegradable and high-tack adhesive applications in flexible packaging and construction. USDA’s BioPreferred Program supports these innovations, encouraging polymer binders companies to adopt renewable raw materials. Additionally, heightened demand for quick-setting, low-emission adhesives in flooring and insulation has accelerated market penetration. Advancements in sustainable formulation chemistries and regional subsidies for green building adhesives continue to shape the polymer binders market trends and ensure long-term segmental growth.

Regional Analysis:

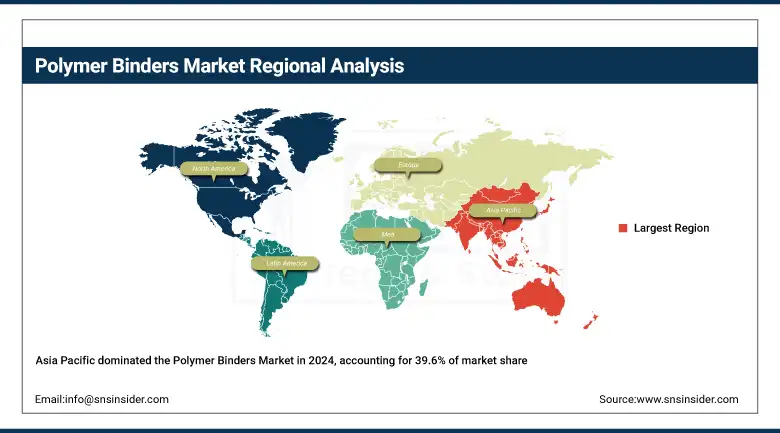

Asia Pacific dominates the polymer binders market with a commanding 39.6% market share in 2024, driven by rapid urbanization, industrial expansion, and growing demand for eco-friendly building materials. China is the key contributor, propelled by government initiatives such as the China Green Building Council’s promotion of low-VOC acrylic polymer binder usage. India’s expanding paints and adhesives industries further bolster demand for advanced binders like ethyl cellulose binders in flexible packaging. Investments by polymer binders companies in regional manufacturing hubs reflect strong polymer binders market growth and emerging polymer binders market trends, making Asia Pacific the leader in polymer binders market size and share.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America is the second dominating region in the polymer binders market in 2024, with a 24.3% market share, and was also the fastest growing region with the highest CAGR of 8.40%. This growth is driven by strong industrial activity, green building initiatives supported by the U.S. Green Building Council, and government regulations limiting volatile organic compounds (VOCs) in paints and coatings.

Europe held the third dominating position with a significant 22.9% market share in 2024, supported by stringent environmental regulations from the European Chemicals Agency (ECHA) and the European Union’s Green Deal, which push polymer binder companies toward sustainable binder development. Germany leads the region with its large automotive and construction sectors increasingly adopting acrylic polymer binder solutions in coatings and adhesives to meet eco-friendly standards. France and the UK also contribute significantly through policies incentivizing energy-efficient coatings. These regulatory frameworks and polymer binders market analysis confirm Europe’s critical role in advancing the polymer binders industry's sustainability, further reinforcing polymer binders market growth and market share.

LAMEA is emerging as a promising region in the polymer binders market, driven by rising construction activities, sustainable infrastructure projects, and the adoption of eco-friendly materials. Brazil leads in Latin America with government incentives for bio-based and waterborne polymer binders in coatings, while regulatory alignment with global standards fosters further growth. In the Middle East and Africa, countries like the United Arab Emirates and Saudi Arabia are promoting sustainable building practices and green initiatives, such as Vision 2030, boosting the demand for acrylic polymer binder technologies and supporting regional polymer binder market growth.

Key Players:

The major polymer binders market competitors include BASF SE, Dow Inc., Wacker Chemie AG, Celanese Corporation, Arkema Group, Synthomer PLC, Trinseo S.A., OMNOVA Solutions Inc., Toagosei Co., Ltd., and Dairen Chemical Corporation.

Recent Developments:

-

In May 2025, Austroads introduced ATM 104, a new test method to evaluate storage stability of hybrid polymer-modified binders, enhancing accuracy in detecting polymer separation during long-term high-temperature storage.

-

In February 2025, WACKER launched VINNOL H 15/45 M (Renewable Energy), a low-carbon solid polymer binder using renewable electricity, cutting carbon footprint by 19% and certified by TÜV Rheinland for industrial applications.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 40.78 billion |

| Market Size by 2032 | USD 74.95 billion |

| CAGR | CAGR of 7.91% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Type (Acrylic, Vinyl Acetate, Latex, Polyurethane, Polyester, Others) •By Form (Powder, Liquid, High Solids) •By Application (Paints & Coatings, Adhesives, Textiles, Construction, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | BASF SE, Dow Inc., Wacker Chemie AG, Celanese Corporation, Arkema Group, Synthomer PLC, Trinseo S.A., OMNOVA Solutions Inc., Toagosei Co., Ltd., and Dairen Chemical Corporation |

Frequently Asked Questions

Asia Pacific dominated the Polymer Binders Market in 2024 with a 39.6% share due to industrial expansion, green building initiatives, and polymer binders industry investments.

Powder-based binders dominated the Polymer Binders Market in 2024 with a 41.5% share due to energy-efficient, VOC-free features ideal for construction applications.

Brazil leads the LAMEA Polymer Binders Market due to government incentives for bio-based and waterborne binders in paints and adhesives for green infrastructure.

Polymer Binders Market trends in North America are driven by green building mandates, VOC limits, and EPA-backed use of acrylic polymer binder in coatings.

The Polymer Binders Market size was valued at USD 40.78 billion in 2024, driven by eco-friendly formulations and expanding construction and electric vehicle applications.

Get in Touch