Polyvinyl Alcohol (PVOH) Market Report Scope & Overview:

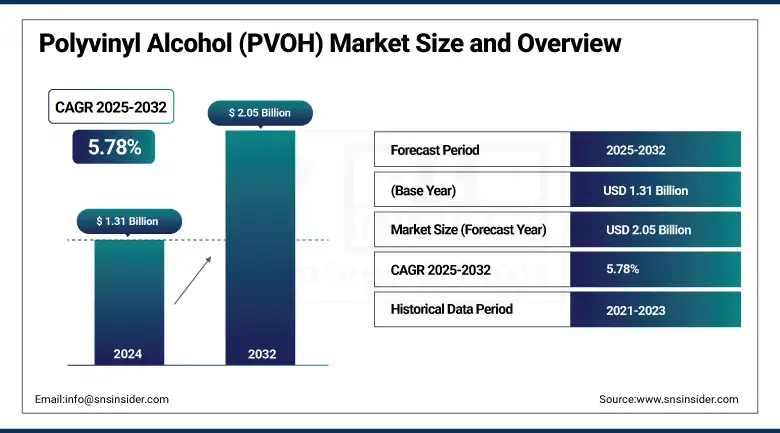

The polyvinyl alcohol (PVOH) market size was valued at USD 1.31 billion in 2024 and is expected to reach USD 2.05 billion by 2032, growing at a CAGR of 5.78% over the forecast period of 2025-2032.

To Get more information On Polyvinyl Alcohol (PVOH) Market - Request Free Sample Report

The polyvinyl alcohol (PVOH) market analysis indicates that the growing demand for biodegradable PVA resin in the packaging and textile industries drives the market growth exponentially. Top polyvinyl alcohol (PVOH) market companies, including Kuraray, are driving the sustainability trend with the raw material being awarded with ISCC PLUS certification, thus supporting the polyvinyl alcohol (PVOH) market growth. Developments in the medical grade polyvinyl alcohol (PVA) market, FDA-approved hydrogels for tissue engineering, and for ophthalmic drug delivery are driving demand in the healthcare industry. According to the regulatory bodies such as JECFA and EFSA, the safe use of polyvinyl alcohol (PVOH) has accelerated its worldwide application in industries. The FDA GRAS notice also further provides evidence of safety with a recommended daily intake of up to 360 mg, directly impacting both the polyvinyl alcohol (PVOH) market size and the polyvinyl alcohol (PVOH) market share. These dual regulatory and innovation phenomena underscore changing polyvinyl alcohol (PVOH) market trends in all regions.

-

For instance, in April 2024, Kuraray declared to raise the prices by USD 220/ton in North America, which will affect the market size and analysis. These factors are the force driving polyvinyl alcohol (PVOH) market growth.

Market Dynamics:

Drivers:

-

Increased Demand for Polyvinyl Alcohol in Eco-Friendly Packaging Solutions Drives Market Growth

Increasing demand for eco-friendly packaging is significantly increasing demand for polyvinyl alcohol (PVOH), especially for food packaging. The biodegradable nature of PVOH makes it an attractive substitute for plastic, particularly in the food industry, where water-soluble films are becoming more common. Organizations, such as Kuraray, are concentrating on green polyvinyl alcohol (PVOH) production, which is further expanding the market size. The fact that packaging waste is a huge environmental issue means the shift toward biodegradable polymers, such as PVOH, is firmly on the list of global sustainability challenges, driving market expansion.

-

Medical Industry Growth Accelerates Demand for Polyvinyl Alcohol in Drug Delivery Systems

The use of polyvinyl alcohol has been increasing more and more in the medical field, and especially in the delivery of drugs and tissue engineering, as it can be easily used by the human body. Polyvinyl alcohol (PVOH) market growth is spurred by products, such as PVOH hydrogels, that have been approved by the FDA for a range of uses. These hydrogels are important in the biomedical field for wound dressing or ocular surgery. Furthermore, the growing healthcare infrastructure in developing nations is anticipated to strengthen the market for PVOH-based medical products, making it an important material for future medical breakthroughs.

Restraints:

-

Supply Chain Issues and Raw Material Shortages Pose Challenges for Polyvinyl Alcohol Production

Vinyl Acetate, a critical raw material in the manufacture of polyvinyl alcohol, is subject to market fluctuations, which are constraining production efficiency. Disruptions in the supply chain, when it comes to global supply chains, geopolitical and environmental factors impact the supply chain, thus impacting PVOH manufacturers. The dependence on particular raw material sources in a few regions presents additional challenges, leading to a possible delay in production and disruption in the polyvinyl alcohol (PVOH) market.

-

Stringent Regulatory Requirements for Polyvinyl Alcohol in Medical and Food Applications Limit Adoption

The rules for polyvinyl alcohol are increasingly restrictive, especially when used in medical and food quality applications. Mandatory adherence to different regional standards, such as the EU’s REACH and the U.S. FDA regulations, can slow product approval and raise costs for companies. Such challenges, especially in the medical and food sectors, act as barriers impeding market growth as organizations are compelled to work on longer approval timelines and higher operating expenses to comply with the rising regulatory standards.

Segmentation Analysis:

By Type

Partially hydrolyzed polyvinyl alcohol (PVOH) held the highest market share of 50.3% in 2024. This segment is the largest owing to its versatile properties, such as high-water solubility, excellent film-forming capacity, and adhesion, enabling the use of collagens across various industries, particularly in food packaging, textiles, and adhesives. Players, such as Kuraray, have developed sophisticated formulations of partially hydrolyzed PVOH for these applications, further supporting demand.

The PVOH hydrogels emerged as the fastest-growing segment and have experienced a rapid increase with a CAGR of 6.83% in 2024. The segment’s growth is mainly driven by their increasing demand in the medical field, such as drug delivery and wound dressings. Their biocompatibility, high water content, and drug-controlled release trigger their use in health. Based on information from the National Institutes of Health, PVOH-based biomaterials are under extensive investigation for ophthalmic and regenerative uses, and are anticipated to be the leading defect solution in medical-grade polyvinyl alcohol (PVA), which is produced with long-term growth.

By Application

Food packaging dominated the polyvinyl alcohol (PVOH) market by 35.7% in 2024 due to the demand for it for being biodegradable and resistant to moisture. In addition, greater regulation from the U.S. Food and Drug Administration [FDA] on sustainable food-grade packaging has driven uptake. However, many of these multinationals are moving toward PVOH-based films to achieve the environmental and consumer push for greener packaging. The development is also being aided by advances from PVOH companies specifically targeting the edible and water-soluble film markets.

Also, the paper application segment is growing the fastest with 6.87% CAGR due to the rising consumption of environmentally friendly coated paper in packaging and publishing. PVOH provides improved strength to paper and printability, and oil and grease resistance. Growth of the segment is attributed to increased demand for recyclable packaging in North America and Europe, which is influencing manufacturers to replace other polyvinyl alcohol formulations with water-based PVOH coatings.

Regional Analysis:

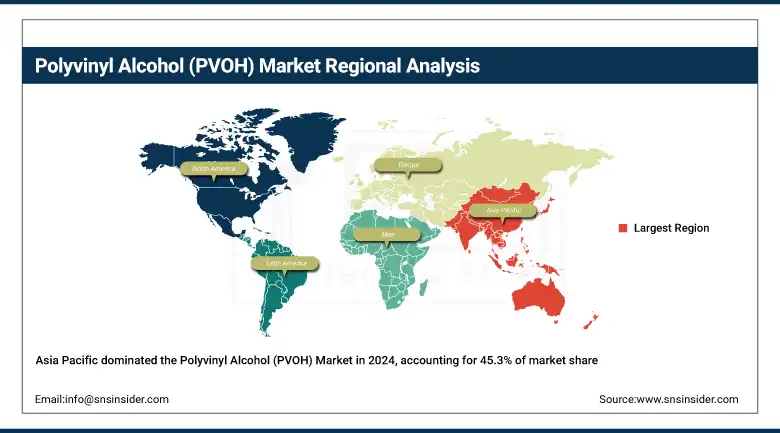

Asia Pacific leads the polyvinyl alcohol (PVOH) market with a 45.3% share on the back of national green initiatives and strong manufacturing. Chinese “Green Manufacturing” policy and the National Mission on Sustainable Agriculture introduced in India have further promoted the use of biodegradable PVOH film in agrochemicals sachets/packaging. Polyvinyl alcohol (PVOH) companies such as Kuraray and Chang Chun Petrochemicals are both looking to increase capacity in the case of textile and medical-grade polyvinyl alcohol applications, and China, which accounts for upwards of 30% of regional output, dominates this end of the market. Japanese Ministry of Economy, Trade, and Industry backs R&D of PVOH hydrogel for ophthalmic and regenerative medicine, underlining Asia Pacific’s dominance in the polyvinyl alcohol (PVOH) market trends.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America is projected to be the fastest-growing region with the highest CAGR of 6.65% from 2025 to 2032. Strict regulatory framework and increasing end-use industries are driving the polyvinyl alcohol (PVOH) market. The U.S dominated the North America polyvinyl alcohol (PVOH) market with a USD 189.58 million market size in 2024, which is approximately 76% of the North America PVOH market due to FDA’s GRAS notice for PVOH coatings in food contact applications that has further promote its demand in sustainable food packaging and water-soluble films. The Clean Growth Program, which includes the federal incentives in Canada, has increased demand for the PVA Resin in textile and paper coatings, whereas Mexico has also increased the usage of the Medical Grade Polyvinyl Alcohol hydrogels for the controlled release drug delivery in the pharmaceutical industry. The same influence collectively makes North America the fastest-growing region.

Europe’s market for polyvinyl alcohol (PVOH), with a share of 22.1%, is propelled by leadership in regulations and innovation. The EU Single-Use Plastics Directive has driven manufacturers to replace traditional plastics with PVOH-based biodegradable films, especially in food packaging. Germany leads in Europe’s demand, with over 30% through expansions at Wacker Chemie’s VINNOL resin plant in Burghausen for automotive and packaging uses. The approval by ANSES (French Agency for Food, Environmental and Occupational Health & Safety) of PVOH in food contact applications in France as well as ENEA-patented R&D funded by Italy for PVOH hydrogels in medical devices, are the latest examples of Europe’s commitment to supporting circular economy solutions and their support go some way to corroborating the market trends in synthetic polymers.

LAMEA is witnessing increasing growth on the back of changing regulations and accelerating circular-economy efforts. Brazil’s Anvisa issued a revised positive list for food-contact polymers, driving the development of water-soluble, edible PVOH films for detergent pods and agrochemical sachets. In the UAE, the Circular Packaging Association, part of the Ministry of Climate Change and Environment, legislates extended producer responsibility, driving demand for compostable packaging made from PVOH. Low-VOC PVOH coatings are being promoted by South Africa's Department of Trade and Industry in construction as well as automotive paints, as part of the gradual transition of the region towards a sustainable synthetic polymer market analysis.

Key Players:

The major competitors in the polyvinyl alcohol (PVOH) market include Kuraray Co., Ltd., Sekisui Chemical Co., Ltd., Mitsubishi Chemical Corporation, Wacker Chemie AG, Chang Chun Petrochemicals Co., Ltd., Anhui Wanwei Group Co., Ltd., Sinopec Sichuan Vinylon Works, Nippon Synthetic Chemical Industry Co., Ltd., Japan Vam & Poval Co., Ltd., and Denka Co., Ltd.

Recent Developments:

-

April 2025: Mitsubishi Chemical’s Okayama Plant received ISCC PLUS certification, confirming its sustainable PVOH production using biomass and recycled raw materials, aligning with global environmental standards.

-

July 2024: Wego Chemical Group added polyvinyl alcohol to its offerings, expanding supply across Latin America, Turkey, and Europe to meet rising demand in coatings, textiles, and pharma sectors.

-

April 2024: Kuraray launched PVA hydrogel microcarriers for regenerative medicine, enhancing cell culture efficiency with improved durability and reduced debris for tissue engineering and therapeutic applications.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 1.31 billion |

| Market Size by 2032 | USD 2.05 billion |

| CAGR | CAGR of 5.78% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Type (Fully hydrolyzed, Partially hydrolyzed, PVOH hydrogels, Others) •By Application (Paper, Food Packaging, Construction, Electronics, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Kuraray Co., Ltd., Sekisui Chemical Co., Ltd., Mitsubishi Chemical Corporation, Wacker Chemie AG, Chang Chun Petrochemicals Co., Ltd., Anhui Wanwei Group Co., Ltd., Sinopec Sichuan Vinylon Works, Nippon Synthetic Chemical Industry Co., Ltd., Japan Vam & Poval Co., Ltd., Denka Co., Ltd. |

Frequently Asked Questions

Major players in the Polyvinyl Alcohol (PVOH) market include Kuraray, Sekisui Chemical, Mitsubishi Chemical, Wacker Chemie, and Chang Chun Petrochemicals.

Asia Pacific dominates the Polyvinyl Alcohol (PVOH) market with a 45.3% share due to green policies and manufacturing strength.

Food packaging leads the Polyvinyl Alcohol (PVOH) market with a 35.7% share due to its moisture resistance and FDA compliance.

Partially hydrolyzed PVOH dominates the Polyvinyl Alcohol (PVOH) market with 50.3% share due to its solubility and adhesion properties.

The Polyvinyl Alcohol (PVOH) market is projected to reach USD 2.05 billion by 2032, growing at a CAGR of 5.78%.

Get in Touch