Polysilicon Market Report Scope & Overview:

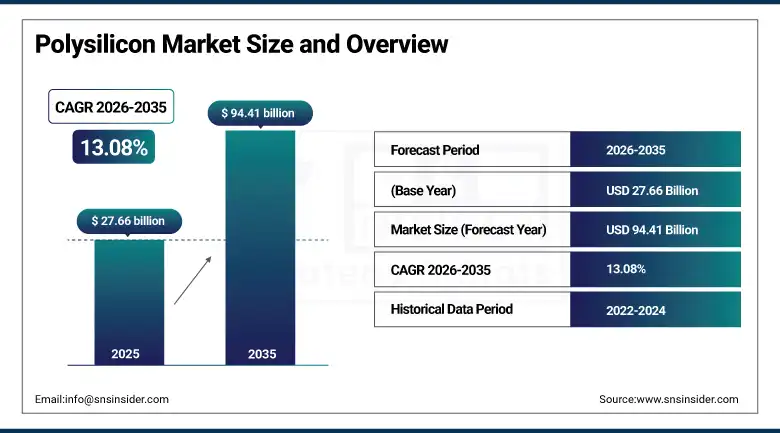

The Polysilicon Market was valued at USD 27.66 Billion in 2025 and is expected to reach USD 94.41 Billion by 2035, growing at a CAGR of 13.08% from 2026–2035.

The polysilicon market worldwide is experiencing tremendous growth due to the growing commercial deployment of solar photovoltaic technology, where there is always a need for the production of high-quality polysilicon that gets converted to silicon wafers, solar cells, and solar modules, which provide the basis of the most commercially viable renewable energy technology in the world. Solar photovoltaics' contribution to electricity generation worldwide is growing at a fast rate due to the declining costs of solar modules, combined with government targets on the usage of renewable energy in more than 130 countries around the world. This two-pronged demand landscape has elevated the importance of polysilicon from just another chemical commodity to a strategic energy source.

Tokuyama Corporation launched a new fluidized bed reactor process for electronic-grade polysilicon production in April 2025, reducing energy consumption by 12% per ton and positioning the company for high-purity semiconductor supply growth. The development reflects the competitive pressure among electronic-grade polysilicon producers to achieve the cost efficiency and purity standards that advanced semiconductor manufacturers including TSMC and Samsung require as they scale 3nm and 2nm production volumes.

Polysilicon Market Size and Forecast

-

Market Size in 2026E: USD 31.28 Billion

-

Market Size by 2035: USD 94.41 Billion

-

CAGR: 13.08% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information On Polysilicon Market - Request Free Sample Report

Polysilicon Market Trends

-

Rising demand for solar photovoltaic (PV) panels and renewable energy generation is driving the polysilicon market.

-

Growing adoption in semiconductor manufacturing and electronics production is boosting market growth.

-

Expansion of solar power installations and global clean energy initiatives is fueling polysilicon consumption.

-

Increasing focus on high-purity silicon materials for improved energy conversion efficiency is shaping adoption trends.

-

Advancements in polysilicon production technologies and energy-efficient manufacturing processes are enhancing output quality and cost efficiency.

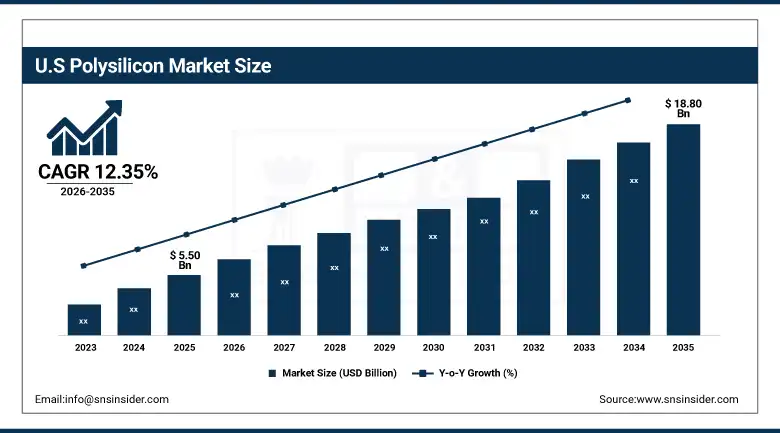

U.S. Polysilicon Market Outlook

The U.S. Polysilicon Market was valued at approximately USD 5.50 Billion in 2025 and is expected to reach approximately USD 18.80 Billion by 2035, growing at a CAGR of approximately 12.35%.

The United States is investing substantially in domestic polysilicon production capacity under the CHIPS and Science Act and the Inflation Reduction Act’s domestic content requirements for solar modules qualifying for the ITC and PTC incentive programmes. Hemlock Semiconductor received a USD 325 million CHIPS Incentives Program investment to construct a new semiconductor-grade polysilicon manufacturing facility, directly responding to the national security imperative of reducing U.S. dependence on Chinese polysilicon supply for both its solar energy transition and its advanced semiconductor manufacturing programmes.

REC Silicon announced the commercial restart of its Moses Lake, Washington polysilicon production facility in 2024, supported by a long-term supply agreement with Hanwha Qcells. The restart directly addresses the U.S. solar module manufacturing sector’s requirement for domestically produced polysilicon feedstock to qualify for the full IRA domestic content bonus credit that generates meaningful project economics improvement for solar developers whose projects incorporate qualifying domestic content.

Polysilicon Market Segment Analysis

-

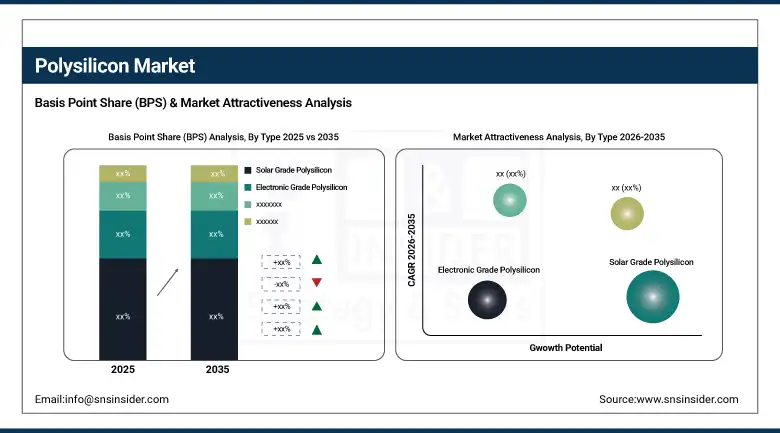

By Type, Solar Grade Polysilicon segment dominated the Polysilicon Market in 2025 with 82% share; Electronic Grade Polysilicon segment is the fastest growing segment.

-

By Production Method, Chemical Vapor Deposition (CVD) segment dominated the market in 2025 with 71% share; Silane Gas Phase segment is the fastest growing segment.

-

By Application, Photovoltaic (PV) Solar Cells segment dominated the market in 2025 with 79% share; Semiconductor Industry segment is the fastest growing segment.

-

By End-Use Industry, Solar Energy Industry segment dominated the market in 2025 with 76% share; Automotive & Electric Vehicles segment is the fastest growing segment.

By Type, solar grade polysilicon segment dominated the polysilicon market, electronic grade polysilicon segment is the fastest growing

The Solar Grade Polysilicon segment dominated the Polysilicon Market in 2025 owing to the fast-growing demand for solar photovoltaic panels and installations around the world. Solar grade polysilicon is highly utilized in producing solar wafers and modules that are both inexpensive and efficient. Factors contributing to the growth include government initiatives that encourage energy efficiency, increased use of utility-scale solar panels, and more spending on renewable power generation. Moreover, reduced production costs and increased attention towards carbon neutrality have played an important role in this segment's growth.

The Electronic Grade Polysilicon segment is the fastest growing driven by rising demand for modern semiconductor and electronic products. The Electronic grade polysilicon is known to possess extremely high levels of purity needed to manufacture semiconductors, microprocessors, and advanced communication equipment. Growing usage of artificial intelligence, 5G technology, cloud computing, and consumer electronics production is boosting market growth significantly. In addition to that, more spending on chip factories and electric vehicle production is also fueling growth.

By Production Method, chemical vapor deposition (CVD) segment dominated the polysilicon market, silane gas phase segment is the fastest growing

The Chemical Vapor Deposition (CVD) segment dominated the Polysilicon Market in 2025 due to the capability of producing highly pure polysilicon with great consistency and high efficiency. The process is highly regarded for its suitability for large-scale production of photovoltaic-grade and electronic-grade polysilicon owing to the consistency and efficiency of the process. The increase in the production of solar panels globally along with the increase in the demand for semiconductors led to the high growth in the application of CVD. Advancements in technology enhancing the efficiency of production and the purity of the product have also contributed to the segment's dominance.

The Silane Gas Phase segment is the fastest growing in the Polysilicon Market as the demand for highly pure polysilicon is rising in order to manufacture semiconductor devices. The production process is highly energy-efficient compared to other methods along with being efficient for depositing the materials. There is an increasing use of electronic products and other smart devices that have driven the demand for silane gas phase production. Environmental sustainability is another aspect of growth in this segment.

By Application, photovoltaic (PV) solar cells segment dominated the polysilicon market, semiconductor industry segment is the fastest growing

The Photovoltaic (PV) Solar Cells segment dominated the Polysilicon Market in 2025 due to the massive usage of solar energy in various sectors such as residences, businesses, and utilities. Polysilicon is an essential component used in the manufacturing of crystalline silicon solar cells that generate electricity through photovoltaic panels. The growing use of solar power and falling installation costs of photovoltaics led to the increasing demand for polysilicon from the solar cells market. In addition, environmental awareness and reduction of carbon footprints worldwide propelled the market.

The Semiconductor Industry segment is the fastest growing in the Polysilicon Market due to the ever-increasing need for pure silicon materials in producing semiconductors. The expanding industries like artificial intelligence, 5G network connectivity, cloud computing, consumer electronics, and data centers have resulted in a massive increase in semiconductor production. For the efficient functioning of semiconductor devices, they require highly pure polysilicon. Moreover, the development of domestic fabs and use of smart technology are majorly propelling the market growth during the forecast period.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

61.7% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Polysilicon Market Insights

North America is the fastest-growing regional polysilicon market at a CAGR of 9.22%, fueled by investments made by the U.S. Government in the production of polysilicon in the country via the CHIPS Act and Inflation Reduction Act, the reopening of REC Silicon’s facility in Moses Lake, and rising manufacturing investments at TSMC’s Arizona manufacturing plants and Intel Ohio manufacturing facilities that are creating new domestic demands for electronic grade polysilicon in the region. The U.S. is responsible for about 87.4% of the revenue generated by North America through Hemlock Semiconductor’s plants in Michigan and new production capacity being built in the country to satisfy IRA requirements.

Canada contributes approximately 12.6% of North American revenues through its semiconductor and electronics manufacturing sector and the nascent solar energy project development market that is creating growing polysilicon derivative demand across Ontario, Alberta, and British Columbia solar installation programmes supported by federal and provincial clean energy investment.

According to the U.S. Energy Information Administration, solar accounted for approximately 81% of all new U.S. electricity-generating capacity additions in 2025, with utility-scale solar additions exceeding 37 GW during the year.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Polysilicon Market Insights

Europe is a significant polysilicon market whose solar PV installation programme, advanced semiconductor manufacturing base, and strategic autonomy policy motivation for supply chain diversification are collectively creating growing demand for both domestic and non-Chinese sourced polysilicon supply. Germany accounts for approximately 22.3% of European revenues through Wacker Chemie’s polysilicon production operations, which represent Europe’s largest domestic polysilicon manufacturing capacity and a critical supply chain asset for the EU’s strategic goal of reducing dependence on Chinese solar supply chains.

According to the European Commission, the EU added approximately 65.5 GW of new solar PV capacity in 2025, bringing cumulative installed solar capacity above 338 GW across the bloc. The EU’s REPowerEU strategy targets over 600 GW of installed solar capacity by 2030, creating substantial long-term demand for polysilicon, wafers, and photovoltaic modules.

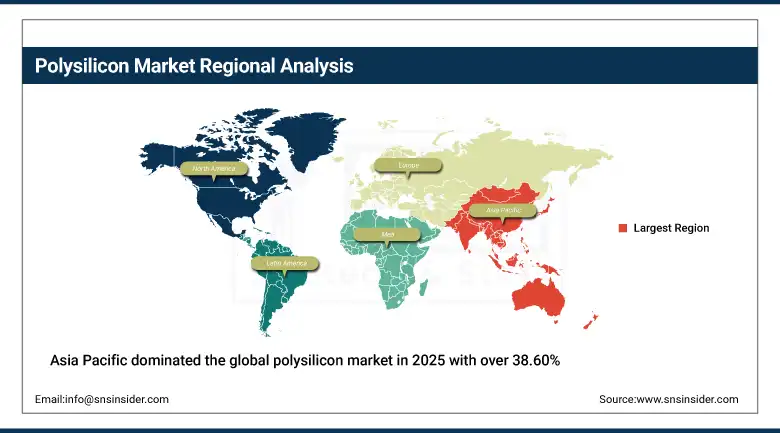

Asia Pacific Polysilicon Market Insights

Asia Pacific dominated the global polysilicon market in 2025 with over 38.60% of revenue share, driven by China’s extraordinary concentration of polysilicon manufacturing capacity and the region’s dominance of global solar PV module production. China accounts for approximately 61.7% of Asia Pacific revenues through its combination of the world’s largest polysilicon manufacturing capacity, the largest solar module production base, and the most aggressive solar PV installation programme of any national market. GCL-Poly, Daqo New Energy, TongWei Group, and TBEA collectively represent the world’s largest polysilicon production cluster, whose combined capacity constitutes the majority of global solar grade polysilicon supply.

According to the International Energy Agency, China controls more than 80% of global solar manufacturing capacity across polysilicon, wafers, cells, and modules. China also accounted for over 95% of global wafer production capacity in 2025.

China’s National Energy Administration reported that the country added approximately 278 GW of new solar capacity in 2025, bringing total installed solar capacity above 880 GW, the highest globally.

MEA & Latin America Polysilicon Market Insights

The Middle East and Africa and Latin America are growing polysilicon derivative markets where ambitious solar energy installation programmes are creating growing demand for polysilicon-derived PV modules whose procurement currently depends on Asian supply chains that governments are increasingly seeking to diversify or localise. Saudi Arabia leads MEA revenues at approximately 31.2% of the regional total through Vision 2030’s solar energy investment, which is creating both end-market module demand and industrial diversification investment in solar manufacturing value chain development that includes polysilicon-derived materials.

Brazil leads Latin American revenues at approximately 44.2% of the regional total through its substantial solar energy installation programme and growing semiconductor and electronics manufacturing sector whose demand for polysilicon derivatives creates consistent import procurement.

Growth Drivers: Global solar deployment, semiconductor investment, and energy security policies accelerating structural polysilicon demand growth worldwide.

The structural growth driver for the polysilicon market is the solar PV industry’s extraordinary global deployment acceleration, whose commercial momentum is sustained by the combination of declining module costs that make solar the lowest-cost new electricity generation technology in the majority of global markets and government renewable energy commitments that create policy-mandated installation volume requirements through the forecast period. Each gigawatt of solar PV installed capacity requires approximately 4 to 5 metric tonnes of polysilicon, creating a direct and quantifiable demand growth pathway that scales precisely with the installation volumes that government targets and commercial economics are jointly delivering. Semiconductor advanced node investment creates a structurally distinct and premium-priced demand stream for electronic grade polysilicon whose growth is driven by the digital economy’s insatiable demand for more powerful and more energy-efficient computing hardware.

Restraints: Chinese supply concentration, energy-intensive production, and solar installation volatility creating polysilicon pricing and profitability pressures.

The extraordinary concentration of global polysilicon manufacturing capacity in Chinese producers creates a supply chain risk and market pricing power concentration that importing countries and module manufacturers outside China are actively seeking to mitigate through domestic production investment and supply source diversification. Western solar module manufacturers, whose supply chains are heavily dependent on Chinese polysilicon, face both geopolitical risk and commercial pricing risk from this concentration whose mitigation requires the multi-year production capacity development investments that government programmes are beginning to support.

Polysilicon price volatility has been extreme in recent years, with solar grade pricing declining by over 80% from 2022 peaks due to Chinese capacity expansion outpacing demand growth. This price collapse creates margin pressure for all polysilicon producers outside the lowest-cost Chinese operations and challenges the investment economics of new domestic production capacity in North America and Europe whose production costs cannot initially match Chinese scale economies.

Opportunities: IRA incentives, AI semiconductor expansion, and emerging solar markets creating new polysilicon investment opportunities.

The U.S. Inflation Reduction Act’s domestic content requirements create a commercially significant opportunity for North American polysilicon producers whose material qualifies for the domestic content bonus credit available to solar projects using domestically manufactured components throughout the value chain. Hemlock Semiconductor’s CHIPS funding and REC Silicon’s facility recommissioning are direct commercial responses to this incentive structure whose value justifies production cost premiums over Chinese import alternatives for the U.S. solar manufacturing customer segment specifically targeting IRA-compliant project economics. The AI data centre construction wave’s semiconductor demand creation is the most commercially transformative near-term opportunity for electronic grade polysilicon producers whose ultra-high-purity material specification and established semiconductor customer relationships insulate them from the solar grade pricing volatility that dominates the broader polysilicon market’s commercial dynamics.

Recent Developments:

-

2025: Tokuyama Corporation launched a new fluidized bed reactor process for electronic-grade polysilicon production in April 2025, reducing energy consumption by 12% per ton and expanding its manufacturing capability for the ultra-high-purity semiconductor-grade feedstock that advanced chip process node manufacturers require as they scale 3nm and 2nm production volumes across Taiwan, South Korea, and U.S. fabrication facilities.

-

2025: East Hope Group signed agreements in October 2025 to build a new silicon production cluster in Ningxia, China, with an investment of RMB 150 billion targeting 400,000 metric tonnes per year of high-purity crystalline silicon plus integrated wafer, cell, and module manufacturing at full build-out, representing the most significant single polysilicon capacity investment commitment of the year.

-

2024: REC Silicon announced the commercial restart of its Moses Lake, Washington polysilicon production facility in 2024 under a long-term supply agreement with Hanwha Qcells, directly providing U.S.-produced polysilicon feedstock for the domestic solar module manufacturing operations whose IRA domestic content compliance generates project economics benefits that require verified U.S. origin material throughout the solar supply chain.

Polysilicon Market Key Players

-

Tongwei Co., Ltd.

-

GCL Technology Holdings Ltd.

-

Daqo New Energy Corp.

-

Xinte Energy Co., Ltd.

-

Asia Silicon (Qinghai) Co., Ltd.

-

Xinjiang East Hope New Energy Co., Ltd.

-

OCI Company Ltd.

-

Hemlock Semiconductor Operations LLC

-

Tokuyama Corporation

-

REC Silicon ASA

-

Hoshine Silicon Industry Co., Ltd.

-

East Hope Group Co., Ltd.

-

Sichuan Yongxiang Co., Ltd.

-

Kirloskar Ferrous Industries Ltd.

-

Qatar Solar Technologies

-

United Silicon Corporation

-

Elkem ASA

-

Luxshares Corp.

-

HPQ Silicon Inc

Polysilicon Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 27.66 Billion |

| Market Size by 2035 | USD 94.41 Billion |

| CAGR | CAGR of 13.08% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Electronic Grade Polysilicon, Solar Grade Polysilicon) • By Production Method (Chemical Vapor Deposition (CVD), Silane Gas Phase) • By Application (Photovoltaic (PV) Solar Cells, Semiconductor Industry) • By End-Use Industry (Solar Energy Industry, Electronics & Semiconductor Industry, LED Manufacturing, Automotive & Electric Vehicles, Industrial & Chemical Applications, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Tongwei Co. Ltd GCL Technology Holdings Ltd. Daqo New Energy Corp. Xinte Energy Co. Ltd. Wacker Chemie AG Asia Silicon (Qinghai) Co. Ltd. Xinjiang East Hope New Energy Co. Ltd. OCI Company Ltd. Hemlock Semiconductor Operations LLC Tokuyama Corporation REC Silicon ASA Hoshine Silicon Industry Co. Ltd. East Hope Group Co. Ltd. Sichuan Yongxiang Co. Ltd. Kirloskar Ferrous Industries Ltd. Qatar Solar Technologies United Silicon Corporation Elkem ASA Luxshares Corp. HPQ Silicon Inc., and Others. |

Frequently Asked Questions

Asia Pacific dominated the Polysilicon Market in 2025 with over 38.60% revenue share, with China accounting for the majority of the region’s polysilicon production capacity and consumption volume.

Solar Grade Polysilicon dominated the Polysilicon Market with 65% share in 2025.

Global solar deployment, semiconductor investment, and energy security policies accelerating structural polysilicon demand growth worldwide.

The Polysilicon Market was valued at USD 27.66 Billion in 2025.

The Polysilicon Market is expected to grow at a CAGR of 13.08% from 2026 to 2035.

Get in Touch