Polyurethane Dispersions Market Report Scope & Overview:

The Polyurethane Dispersions Market was valued at USD 2.75 billion in 2025 and is expected to reach USD 5.10 billion by 2035, growing at a CAGR of 6.4% from 2026–2035.

There is an unusual change taking place in the industry of PUD due to the fact that there have been efforts by various companies across the globe in replacing solvent-based paints and adhesives with the advanced type of water-based paints and adhesives. PUD consists of polyurethane particles suspended in water as opposed to organic solvents and are highly durable, having high chemical resistance, mechanical properties, and stability against UV rays. PUD is highly effective in terms of its adhesive properties and its uses extend to several industries including car coating, artificial leather, textiles, construction, and packaging. Due to increasing green movements around the world, spearheaded by regulations such as REACH and EPA, PUD is increasingly essential.

Innovations in polymer technology continue to push the boundaries through advanced anionic, cationic, self-crosslinking, and hybrid PUD formulations. It is in particular the hybrid PUDs, consisting of both polyurethane and acrylic or other polymer technologies, that have set new benchmarks in terms of scratch resistance and weathering properties as well as formulation versatility. Renewable-content or bio-based PUDs represent the new cutting-edge realm of development, in line with efforts toward minimizing the carbon footprint. Combining PUDs with two-component (2K) technologies opens up entirely new possibilities in coatings.

It is important to note that according to industry data, the adoption of waterborne PUD coatings reduces VOC emissions by up to 80% compared to conventional solvent-borne polyurethanes; furthermore, as of 2025, over 65% of leading coatings and adhesives manufacturers globally have incorporated PUD-based formulations as a core part of their sustainable product strategy.

Polyurethane Dispersions Market Size and Forecast

-

Market Size in 2025: USD 2.75 Billion

-

Market Size by 2035: USD 5.10 Billion

-

CAGR: 6.4% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Polyurethane Dispersions Market - Request Free Sample Report

Polyurethane Dispersions Market Trends

-

Increasing move from solvent-borne to waterborne PUD coatings due to stringent VOC regulations (REACH, EPA, and their equivalents), which compel companies to revamp their formulations for automotive, furniture, and industrial coatings markets.

-

Growth in the adoption of composite PU dispersion technologies involving the use of the polymer in combination with other polymers including acrylics, epoxy, or silicones, which enhance cross-linking potential and UV resistance of the PUD products.

-

Quick growth in the acceptance of two component (2K) PUD formulations for applications in high-abrasion resistant floor coatings, refinishing paints, and industrial maintenance coatings.

-

Development of polyurethane dispersions made from renewable raw materials such as castor oil and succinic acid, meeting sustainability requirements and minimizing the use of petrochemical raw materials.

-

Increasing demand from synthetic leather applications, where producers of shoes, automobile upholstery, and fashion accessories replace DMF-based polyurethane with eco-friendly waterborne PUD coatings.

-

Growth in production capacity in the Asia-Pacific region, with big companies like Wanhua Chemical building new facilities for waterborne resins, which would impact the global value chain.

-

Evolving application of PUD in high-performance textile finishes offering moisture management, fire resistance, and microbial control features for advanced textiles used in the medical, sports apparel, and military industries.

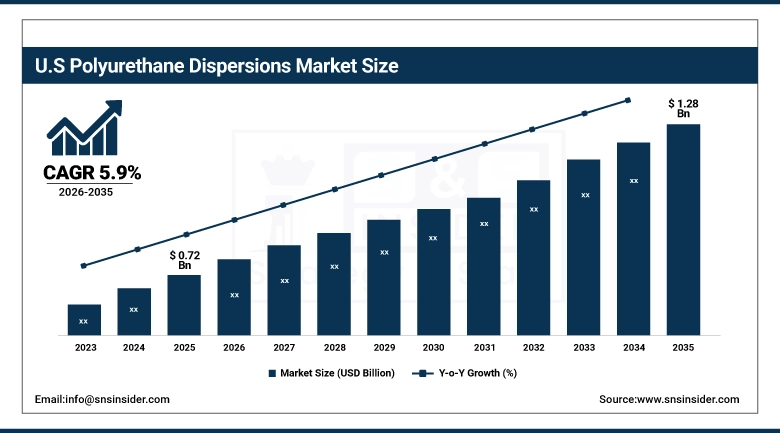

U.S. Polyurethane Dispersions Market was valued at USD 0.72 billion in 2025 and is expected to reach USD 1.28 billion by 2035, registering a CAGR of 5.9% during 2026–2035.

U.S. Polyurethane Dispersions Market dominates North America, thanks to the stringent National Emission Standards for Hazardous Air Pollutants (NESHAP) and Architectural Coating Regulations from the EPA, which force coatings companies to use water-based coatings with low-VOCs. The American automotive industry, which is considered one of the biggest in the world, demands PUD-based coatings, primers, and interior adhesives for its operations. Large chemical companies like Dow, Lubrizol, and Huntsman have made huge investments in PUD production in order to meet the local demand in various segments such as construction, laminated products, and textile finishing.

Stringent environmental regulations enforced by the U.S. EPA continue to be a powerful market accelerant, with the agency’s National Volatile Organic Compound Emission Standards for consumer and industrial products significantly narrowing the viable product space for solvent-borne systems and compelling formulators to adopt PUD-based alternatives for architectural, automotive, and industrial coating applications.

Polyurethane Dispersions Market Segment Insights

-

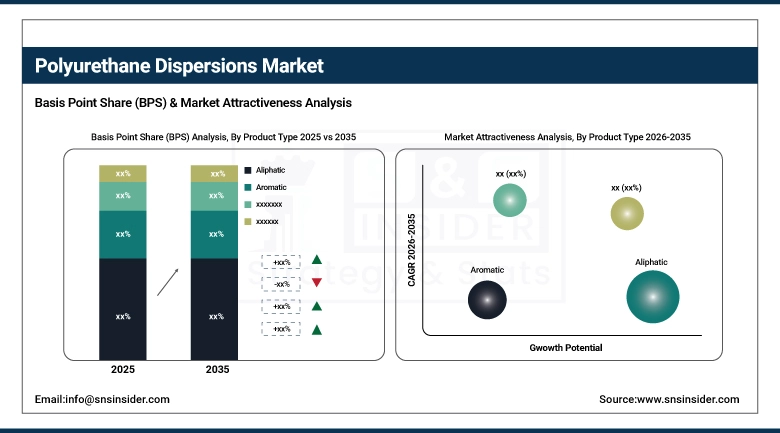

Based on Product Type, Aliphatic PUDs accounted for the largest market share (~55.2%) in 2025; Hybrid PUDs expected to be the fastest-growing segment (CAGR).

-

Based on Application, Coatings accounted for the largest market share (~42.8%) in 2025; Leather Finishing expected to be the fastest-growing segment (CAGR).

-

Based on End-Use Industry, Automotive accounted for the largest market share (~31.5%) in 2025; Construction expected to be the fastest-growing segment (CAGR).

Polyurethane Dispersions Market Segment Analysis

By Product Type, Aliphatic dominates, Hybrid expected to grow fastest

Aliphatic polyurethane dispersions dominated the Polyurethane Dispersions Market in 2025 owing to their superior UV resistance, excellent weatherability, and long-term color retention properties. Aliphatic variants resist yellowing under prolonged sunlight exposure, making them highly preferred for exterior architectural coatings, automotive topcoats, wood finishes, and premium industrial coatings. Their high durability, abrasion resistance, and anti-chalking performance further strengthen adoption across outdoor and high-performance applications.

The polyurethane dispersion hybrids segment is projected to exhibit the fastest growth rate throughout the forecast period. The latest generation of polyurethane dispersion products features an amalgamation of polyurethane dispersion along with acrylic, epoxy, or silicone chemistry. It provides improved bonding properties, flexibility, chemical resistance, and mechanical strength. The rising demand for environmentally friendly low-VOC coatings, textile coatings, automobile original equipment manufacturer (OEM) coatings, and industrial coatings is fueling the market's growth.

By Application, Coatings dominates, Leather Finishing expected to grow fastest

Coatings constituted the largest market segment of Polyurethane Dispersions in 2025 owing to the extensive application of PUDs in architectural paint, automotive coatings, industrial coatings, and wood coatings. Coatings exhibit remarkable performance in terms of durability, flexibility, abrasion resistance, and lower VOC levels. Increased activities in constructions and infrastructural development across the world are contributing significantly to the demand for waterborne coatings.

Leather finishing would be the most promising market segment in 2026–2035 owing to stringent regulations against solvent-based compounds like DMF. Superior flexibility and finish quality along with environmental compatibility make waterborne PUD an ideal choice for leather finishing in shoes, upholstery, automobile interior, and accessories.

By End-Use Industry, Automotive dominates, Construction expected to grow fastest

The automotive industry dominated the Polyurethane Dispersions Market in 2025 due to extensive use of PUDs in automotive coatings, interior adhesives, leather finishing, and protective systems. Increasing adoption of waterborne coating technologies and rising electric vehicle production are driving demand for advanced low-VOC polyurethane dispersions with enhanced durability, flexibility, and thermal stability.

The construction segment is expected to witness the fastest growth during 2026–2035 due to rising infrastructure investments and expanding residential and commercial development activities. Growing regulatory preference for sustainable waterborne coatings is increasing adoption of PUD-based floor coatings, waterproofing membranes, facade coatings, and construction adhesives across global building projects.

Polyurethane Dispersions Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

38% |

|

Europe |

Germany |

26% |

|

Asia Pacific |

China |

44% |

|

Middle East & Africa |

Saudi Arabia |

30% |

|

Latin America |

Brazil |

48% |

North America Polyurethane Dispersions Market Insights

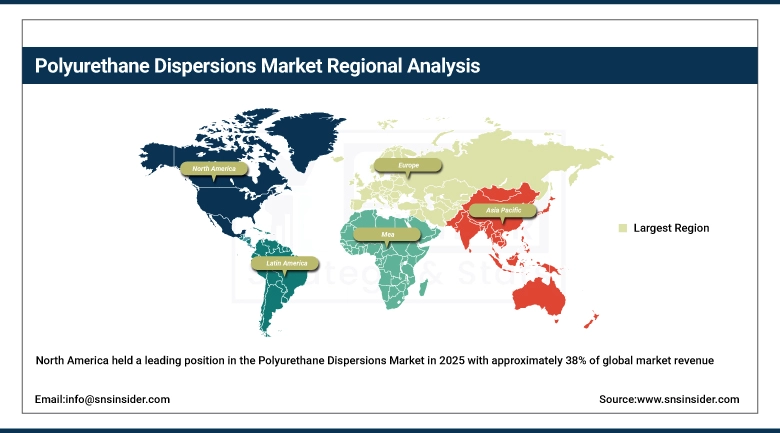

North America held a leading position in the global Polyurethane Dispersions Market in 2025 with approximately 38% of global market revenue. The region’s market leadership is anchored by some of the world’s most stringent VOC emission standards — including EPA’s National Coating Rules and state-level regulations such as California’s South Coast Air Quality Management District (SCAQMD) requirements — which have driven widespread reformulation of industrial, architectural, and automotive coatings toward waterborne PUD technologies. The United States hosts a deep cluster of PUD innovators, formulators, and end-users, with Dow, Lubrizol, Huntsman, and Covestro’s U.S. operations collectively representing a significant proportion of global PUD R&D investment. Canada contributes to regional demand through its substantial oil sands infrastructure maintenance coatings market and growing automotive assembly sector.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Polyurethane Dispersions Market Insights

The Asia Pacific region is forecasted to grow at the highest CAGR throughout the forecast period from 2026 to 2035. This dynamism is driven by China — the world’s largest producer and consumer of polyurethane dispersions — where domestic manufacturers such as Wanhua Chemical and numerous regional players are rapidly scaling production capacity while simultaneously upgrading formulation capabilities. India represents the region’s fastest-growing individual national market, fueled by a rapidly expanding construction sector, growing domestic automotive production, and intensifying regulatory pressure on VOC emissions under the National Clean Air Programme (NCAP). Japan and South Korea contribute sophisticated demand for high-performance aliphatic and specialty PUD systems in automotive OEM, electronics component coatings, and precision industrial applications.

Europe Polyurethane Dispersions Market Insights

In 2025, Europe continued to hold a prominent share of the global Polyurethane Dispersions Market, with Germany, France, the United Kingdom, the Netherlands, and Italy forming the core of regional demand. Europe’s market is uniquely shaped by the world’s most comprehensive chemical regulatory framework — REACH — along with the EU’s Ambient Air Quality Directive and Decopaint Directive, which together create an unambiguous long-term regulatory mandate for low-VOC waterborne coating technologies. European coatings manufacturers have been at the forefront of PUD adoption and product innovation for decades, with companies like BASF, Covestro, and Allnex pioneering next-generation aliphatic and hybrid PUD chemistries. The EU’s Green Deal and Fit for 55 climate package are further accelerating the transition toward bio-based and circular-economy-aligned PUD formulations.

Middle East & Africa and Latin America Polyurethane Dispersions Market Insights

Both the Middle East & Africa and Latin America constitute regions with high-growth opportunities for the polyurethane dispersions market. In the Middle East, the UAE, Saudi Arabia, and Qatar will contribute to increased demand due to the Vision 2030 and Centennial 2071 building programs that require the use of high-performing and climate-resilient coatings. The African region offers a promising long-term growth outlook due to an increase in construction in countries within the sub-Saharan region along with regulatory modernization efforts. For Latin America, the Brazilian market represents 48% of revenue within the region owing to the significant presence of automotive assembly and furniture/footwear production industries within the country.

Polyurethane Dispersions Market Growth Drivers:

Stringent VOC regulations and sustainability mandates accelerating the global transition to waterborne PUD-based coatings and adhesives across all major industries

The primary driver of the Polyurethane Dispersions Market is the intensifying global regulatory pressure to reduce VOC emissions from industrial coating and adhesive processes. Legislative frameworks across North America (EPA NESHAP, SCAQMD), Europe (REACH, Ambient Air Quality Directive), and Asian markets (China’s Blue Sky Action Plan, India’s NCAP) are tightening permissible VOC levels in coatings, adhesives, and sealants — foreclosing the long-term viability of solvent-borne polyurethane systems while creating a structural, non-cyclical growth channel for waterborne PUD alternatives. This regulatory transition is compounded by corporate sustainability commitments from Fortune 500 companies across automotive, consumer goods, and others, which have established Science Based Targets (SBTi) that require the elimination of solvent-borne coatings from their supply chains by 2030 or earlier.

The convergence of regulatory mandates, corporate sustainability pledges, advanced PUD formulation technology, and rising environmental literacy among procurement decision-makers positions polyurethane dispersions as the defining coatings and adhesives technology.

Polyurethane Dispersions Market Restraints

Higher production costs and formulation complexity compared to conventional solvent-based polyurethane systems limiting adoption in cost-sensitive applications

One important limitation for the Polyurethane Dispersions Market is the high manufacturing costs associated with producing premium quality PUD compared to those of solvent-based polyurethanes. The manufacturing of PUD demands unique process equipment, namely, high-shear dispersers, precise temperature regulation, and efficient emulsification technology, which makes the manufacturing process much more expensive compared to regular polyurethane manufacturing. High-end aliphatic and aliphatic-aromatic PUDs, which have the highest level of performance, are estimated to be two to four times more expensive per kilogram than their aromatic solvent counterparts. This becomes an important barrier of entry for the PUD market when it comes to commodities such as architectural paint and industrial maintenance paint where price competition is fierce. Another challenge that the PUD market faces is the difficulty in formulating stable high-solid waterborne dispersions due to problems in shelf life, freeze-thaw stability, and film formation at low temperatures.

Polyurethane Dispersions Market Opportunities

Bio-based PUD innovation, 2K system adoption, and digital formulation platforms unlocking new high-value market segments through 2035

The greatest potential for growth in the Polyurethane Dispersions Market emanates from the convergence of sustainability-focused chemical innovation and evolving needs in premium end-user markets. Bio-based PUDs, which use biorenewable ingredients like castor oil polyols, succinic acid, and bio-based isocyanates, constitute an emerging category within the industry that satisfies the sustainability policies of companies and future regulations on the bio content of industrial products. The two-component (2K) waterborne polyurethane dispersions are paving the way for the exploitation of lucrative applications like automotive OEM, aerospace interior coating, and heavy-duty industrial flooring coating that could only be addressed by 1K waterborne technology before. The digital formulation platform and artificial intelligence-assisted PUD polymer design are expediting the product development process, allowing companies to tailor application-specific grades of polyurethane dispersions.

Recent Developments:

-

2026: BASF announced the development of an advanced 2K waterborne PUD system that has been developed for the application of automotive OEM clearcoats with performance similar to that of solvent-borne coatings in terms of gloss, scratch resistance, and chemical resistance, and at the same time meets the toughest VOC emission standards globally.

-

2026: BASF increased its dispersion manufacturing capacity in Durban, South Africa. The company also opened a new application lab in order to increase regional supply of sustainable coating and construction materials.

-

2026: Covestro continued the development of its range of INSQIN waterborne polyurethanes. This is designed to create sustainable textile coatings and synthetic leather for automotive and fashion industries.

Polyurethane Dispersions Market Key Players

Some of the Polyurethane Dispersions Market Companies are:

-

BASF SE

-

Covestro AG

-

Dow Chemical Company

-

Lubrizol Corporation

-

Huntsman Corporation

-

Wanhua Chemical Group

-

LANXESS AG

-

Alberdingk Boley GmbH

-

Allnex Group

-

Perstorp Holding AB

-

Mitsui Chemicals Inc.

-

DIC Corporation

-

Stahl Holdings B.V.

-

Hauthaway Corporation

-

VCM Polyurethanes Pvt. Ltd.

-

Cytec Industries

-

Lamberti S.p.A.

-

Coim S.p.A.

-

Evermore Chemical Industry Co., Ltd.

-

Omnova Solutions

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.75 Billion |

| Market Size by 2035 | USD 5.10 Billion |

| CAGR | CAGR of 6.4% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Aliphatic, Aromatic, Hybrid) • By Application (Coatings, Adhesives & Sealants, Textiles, Leather Finishing, Paper & Packaging) • By End-Use Industry (Automotive, Construction, Furniture, Textiles, Packaging) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BASF SE, Covestro AG, Dow Chemical Company, Lubrizol Corporation, Huntsman Corporation, Wanhua Chemical Group, LANXESS AG, Alberdingk Boley GmbH, Allnex Group, Perstorp Holding AB, Mitsui Chemicals Inc., DIC Corporation, Stahl Holdings B.V., Hauthaway Corporation, VCM Polyurethanes Pvt. Ltd., Cytec Industries, Lamberti S.p.A., Coim S.p.A., Evermore Chemical Industry Co., Ltd., Omnova Solutions |

Frequently Asked Questions

North America dominated the Polyurethane Dispersions Market in 2025, accounting for approximately 38% of global market revenue.

The Coatings segment dominated the Polyurethane Dispersions Market in 2025 with approximately 42.8% revenue shares.

The Aliphatic Polyurethane Dispersions segment dominated the Polyurethane Dispersions Market in 2025, accounting for approximately 55.2% of global revenue.

Stringent global VOC emission regulations — including REACH in Europe and EPA standards in North America — combined with sweeping corporate sustainability mandates, are the primary structural drivers compelling manufacturers across automotive, construction, and textile industries to transition from solvent-based polyurethane systems to high-performance waterborne PUD alternatives through 2035.

The Polyurethane Dispersions Market was valued at USD 2.75 billion in 2025.

The Polyurethane Dispersions Market is expected to grow at a CAGR of 6.4% from 2026 to 2035.

Get in Touch