Formic Acid Market Report Scope & Overview:

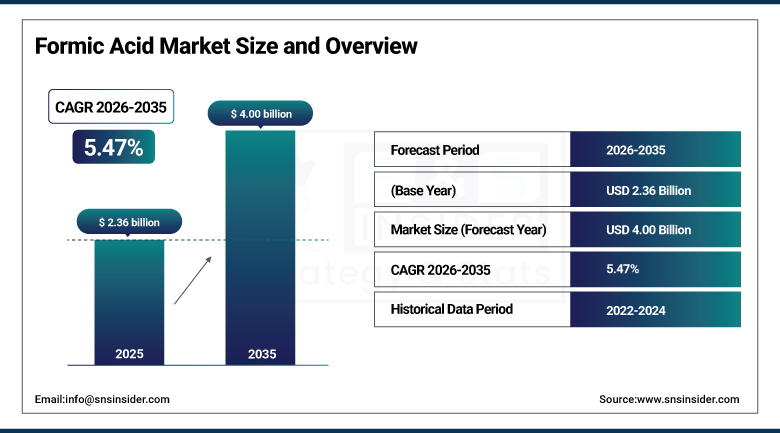

The Formic Acid Market was valued at USD 2.36 Billion in 2025 and is expected to reach USD 4.00 Billion by 2035, growing at a CAGR of 5.47% from 2026–2035.

The global formic acid market is growing at a steady and commercially broad-based pace. Formic acid (methanoic acid, HCOOH) is the simplest carboxylic acid, a colorless corrosive liquid with a pungent odor that occurs naturally in ant venom and is produced industrially via methanol carbonylation and methyl formate hydrolysis. The market is driven by rising adoption in the leather and textile industry which is the primary market growth driver, growing demand as an animal feed preservative and silage acidifier, and expanding applications in rubber processing, chemical synthesis, and pharmaceutical manufacturing. The report analyses production capacity and utilization rates, feedstock price trends affecting methanol and carbon monoxide input economics, regulatory landscape and trade policies, and sustainability metrics including bio-based formic acid development from CO₂ reduction processes.

In 2024, BASF expanded its formic acid production capacity at its Ludwigshafen facility, responding to growing European demand from the leather and textile industries and increasing agricultural silage preservation adoption in European farming systems. The expansion reflects the commercial recognition that EU agricultural policy’s antibiotic reduction mandate in animal husbandry creates structural formic acid demand growth as farmers transition from antibiotic growth promoters to organic acid preservation systems whose formic acid component creates consistent feed quality and microbial control.

Market Size and Forecast

-

Market Size in 2026E: USD 2.49 Billion

-

Market Size by 2035: USD 4.00 Billion

-

CAGR: 5.47% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information on Formic Acid Market - Request Free Sample Report

Formic Acid Market Trends

-

Development of bio-based formic acid from CO₂ reduction technologies is creating sustainable production opportunities aligned with green chemistry and carbon-neutral manufacturing initiatives

-

The shift away from antibiotic growth promoters in animal feed is increasing demand for formic acid as an effective feed acidifier and antimicrobial agent

-

Rising demand for high-purity formic acid in pharmaceutical manufacturing and advanced industrial applications is supporting growth in premium-grade products

-

Emerging use of formic acid as a hydrogen carrier is attracting investment in fuel cell and clean energy technologies due to its safe and efficient hydrogen storage potential

-

Expanding utilization of formic acid in textile processing, fiber production, and dyeing applications is driving steady industrial demand growth worldwide

U.S. Formic Acid Market Outlook

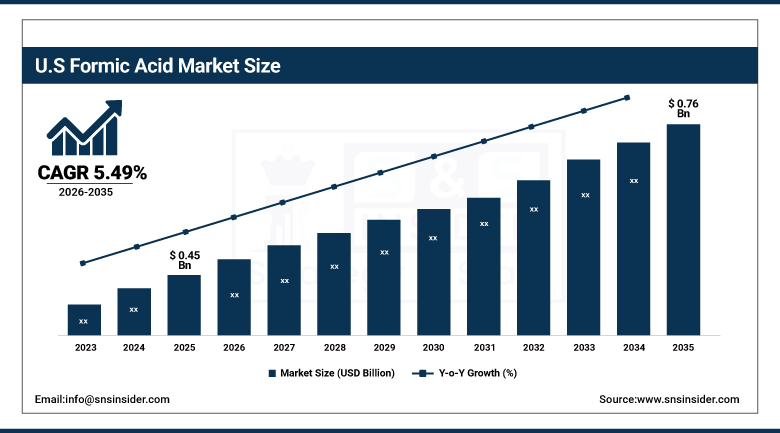

The U.S. Formic Acid Market was valued at approximately USD 0.45 Billion in 2025 and is expected to reach approximately USD 0.76 Billion by 2035, growing at a CAGR of approximately 5.49%.

The U.S. is the most commercially significant formic acid market within the fastest-growing North American region. BASF’s U.S. distribution, Kemira’s North American operations, and import supply from European and Asian producers collectively serve the domestic agricultural, leather, and industrial markets. The U.S. FDA’s GRAS approval for formic acid as a food and feed additive creates regulatory foundation for agricultural adoption. The poultry and swine production sectors’ growing organic acid adoption for feed preservation and pathogen reduction creates structured agricultural procurement that compounds with antibiotic stewardship programme expansion.

Kemira Oyj expanded its formic acid distribution network in North America in 2024, partnering with agricultural chemical distributors to improve access for livestock and poultry feed producers seeking formic acid-based antimicrobial feed preservation solutions. The network expansion reflects commercial recognition that U.S. agricultural sector’s growing organic acid adoption creates distribution infrastructure investment opportunity whose market development compounds with antibiotic reduction programme adoption across integrated poultry and swine production systems.

Formic Acid Market Segment Analysis

-

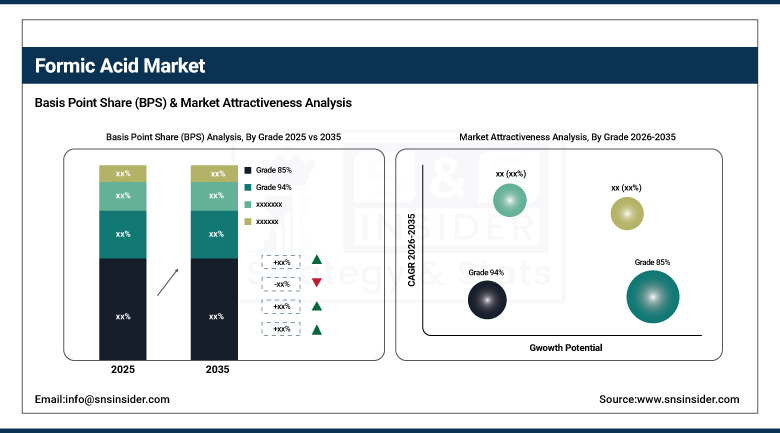

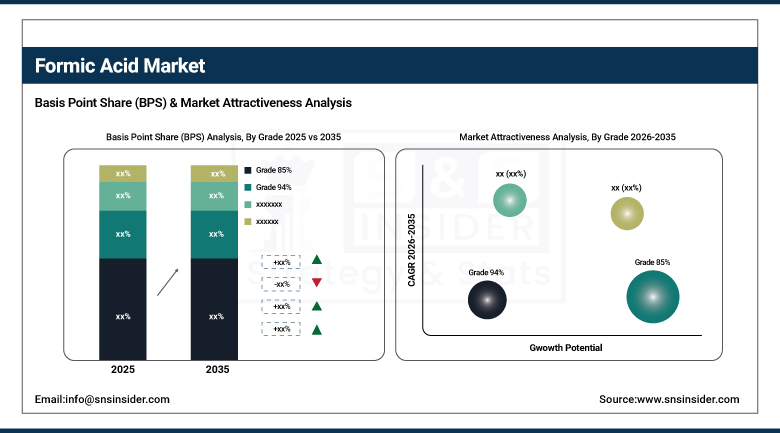

By Grade, the Grade 85% segment dominated the Formic Acid Market with approximately 52% share in 2025, while the Grade 99% segment is the fastest growing.

-

By Application, the Animal Feed & Silage Preservation segment dominated the Formic Acid Market with approximately 38% share in 2025, while the Leather Tanning & Processing segment is the fastest growing.

-

By End Use, the Agriculture segment dominated the Formic Acid Market with approximately 42% share in 2025, while the Chemical & Pharmaceutical segment is the fastest growing.

By Grade, Grade 85% dominates, Grade 99% grows fastest

Grade 85% formic acid retained the dominant grade position with approximately 52% of the formic acid market in 2025. Grade 85%’s commercial primacy reflects its position as the standard commercial concentration whose balance of active acid content and handling safety creates the most cost-effective specification for the majority of agricultural, leather, and textile applications. Each animal feed additive formulation that specifies formic acid for antimicrobial preservation creates Grade 85% procurement whose per-ton cost economics sustain specification preference over higher-concentration alternatives whose additional handling precautions increase operational cost. The leather industry’s pH adjustment and tanning assistant application, textile’s fiber treatment, and rubber’s coagulation agent collectively create industrial demand that sustains Grade 85%’s aggregate commercial leadership.

Grade 99% formic acid is the fastest-growing grade because pharmaceutical synthesis requiring anhydrous high-purity formic acid, fuel cell electrolyte research, and specialty chemical synthesis collectively create premium procurement whose per-ton commercial value substantially exceeds agricultural-grade alternatives. Each pharmaceutical API whose synthesis route requires high-purity formic acid creates qualified supplier relationships whose long-term procurement sustains Grade 99% commercial momentum. The fuel cell technology’s formic acid hydrogen carrier research creates new Grade 99% procurement that compounds with clean energy investment.

By Application, animal feed dominates, leather & textile grows fastest

Animal feed and silage preservation retained the dominant application position with approximately 38% of the formic acid market in 2025. The global livestock, poultry, and dairy production systems’ feed preservation requirement creates consistent formic acid procurement whose antimicrobial and acidifying properties maintain feed quality, reduce pathogen load, and improve nutrient bioavailability. EU antibiotic ban’s systematic replacement of antibiotic growth promoters with organic acid alternatives creates structural formic acid demand whose regulatory mandate motivation sustains procurement independently of commodity price variation. Each integrated poultry, swine, or dairy operation that adopts formic acid-based feed preservation creates commercial relationships whose programme consistency sustains above-average annual procurement.

Leather tanning and processing is the fastest-growing application because the global leather goods industry’s expanding production, particularly in Asia Pacific’s extraordinary leather manufacturing capacity, creates above-average formic acid consumption growth whose deliming, pH adjustment, and chromium fixation roles create consistent per-hide formic acid consumption. Each new tannery established in India, China, or Vietnam creates formic acid procurement whose aggregate across the global leather industry’s progressive capacity expansion sustains the application’s fastest-growing commercial momentum as confirmed by SNS Insider.

By End Use, agriculture dominates, chemical & pharma grows fastest

Agriculture retained the dominant end-use position with approximately 42% of the formic acid market in 2025. The agricultural sector’s formic acid consumption encompasses feed preservation, silage acidification, and the growing crop protection application whose combined procurement creates commercial scale across both livestock and arable farming systems. Each European, North American, and Asian livestock operation whose feed quality and animal health programme creates formic acid procurement sustains agriculture’s dominant end-use commercial position. Government support for organic acid alternatives to antibiotic growth promoters, whose food safety motivation creates institutional procurement motivation beyond individual farm economics, sustains agricultural segment demand.

Chemical and pharmaceutical is the fastest-growing end use because the extraordinary global expansion of specialty chemical and pharmaceutical production creates growing formic acid intermediate demand whose synthesis route application creates procurement that compounds with production volume growth. Each pharmaceutical facility whose API synthesis employs formic acid as a reducing agent, protecting group, or solvent creates procurement whose quality specification requirement sustains premium commercial relationships with high-purity producers.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

Asia Pacific Formic Acid Market Insights

Asia Pacific dominated the global formic acid market in 2025 with the highest revenue share. China accounts for approximately 44.8% of Asia Pacific revenues through its position as the world’s largest formic acid producer and consumer, whose integrated leather manufacturing, textile processing, and animal feed industries create the most commercially concentrated formic acid demand globally.

India’s large leather and textile manufacturing sectors, Japan’s specialty chemical industry, and South Korea’s chemical processing create significant secondary markets whose combined procurement sustains Asia Pacific’s commercial dominance.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Formic Acid Market Insights

North America is the fastest-growing regional formic acid market, driven by growing antibiotic-free animal production creating organic acid adoption, pharmaceutical sector growth, and rubber processing demand. The United States accounts for approximately 87.4% of North American revenues through BASF and Kemira’s distribution infrastructure, the agricultural sector’s growing organic acid adoption, and the chemical industry’s synthesis intermediate procurement.

Canada contributes approximately 12.6% of North American revenues through its livestock production’s feed preservation demand and the chemical industry’s formic acid intermediate consumption.

Europe Formic Acid Market Insights

Europe is a technically sophisticated formic acid market where BASF’s integrated production at Ludwigshafen, the EU antibiotic ban’s structural agricultural demand creation, and the leather and textile sectors’ established application creates consistent procurement. Germany accounts for approximately 22.3% of European revenues through BASF’s commercial operations, the chemical industry’s synthesis intermediate procurement, and the leather processing sector’s established formic acid application.

France, Italy, and Poland are significant secondary markets where livestock production’s feed preservation demand, leather processing, and the chemical industry’s procurement create consistent formic acid consumption.

MEA & Latin America Formic Acid Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its chemical industry’s procurement, the growing poultry and livestock sector’s feed preservation adoption, and the food processing industry’s application. Brazil leads Latin American revenues at approximately 44.2% through its large livestock sector’s organic acid adoption, the leather industry’s processing demand, and the chemical manufacturing sector’s procurement.

Market Dynamics

Growth Drivers: EU antibiotic ban creating organic acid feed demand and leather & textile industry expansion

EU Regulation 1831/2003’s ban on antibiotic growth promoters in animal feed is the formic acid market’s most commercially certain structural growth driver in European and progressively global markets. Each livestock and poultry operation that transitions from antibiotic growth promoter to organic acid feed preservation creates formic acid procurement whose regulatory compliance motivation sustains demand independently of price cycle variation. The WHO’s global action plan on antimicrobial resistance and the progressive adoption of antibiotic-free production standards by retail food chain operators create commercial motivation for organic acid adoption that extends the EU mandate’s market impact beyond European geography.

Rising adoption in the leather and textile industry is SNS Insider’s confirmed primary market growth driver. The global leather goods industry’s production expansion, particularly in Asia Pacific’s tannery capacity growth, creates above-average formic acid demand whose per-hide and per-ton leather processing consumption compounds with the industry’s production volume growth. Textile’s nylon spinning bath, synthetic fiber processing, and dyeing application create industrial consumption that sustains the application category’s fastest-growing commercial momentum.

Restraints: Methanol feedstock price volatility and corrosive handling requirements creating logistics cost

Formic acid’s production from methanol carbonylation and methyl formate hydrolysis creates commercial cost dependency on methanol feedstock pricing whose crude oil correlation creates production cost volatility. Each methanol price spike that compresses formic acid manufacturer margins creates pricing pressure whose downstream commercial impact moderate’s procurement in price-sensitive agricultural and industrial applications.

Formic acid’s corrosive properties requiring specialized storage vessels, corrosion-resistant transport equipment, and worker protective equipment create logistics cost whose aggregate above commodity organic acid alternatives moderates cost-sensitive procurement in applications where less corrosive alternatives provide equivalent performance.

Opportunities: Bio-based formic acid from CO₂ and fuel cell hydrogen carrier development

Bio-based formic acid production from electrochemical CO₂ reduction represents the most commercially innovative production pathway whose carbon capture and utilization chemistry creates a sustainable formic acid source whose green credentials sustain premium specification in environmentally sensitive procurement contexts. Each demonstration plant that achieves commercially viable bio-based formic acid economics creates adoption momentum.

Formic acid’s potential as a liquid hydrogen carrier for fuel cell energy storage represents a long-term commercial development whose hydrogen release chemistry creates energy density advantages whose successful technical and commercial demonstration creates new premium procurement beyond conventional chemical markets.

Recent Developments:

-

2024: BASF expanded its formic acid production capacity at its Ludwigshafen facility in 2024, targeting growing European demand from leather, textile, and agricultural silage preservation sectors, and supporting the structural demand growth from EU antibiotic ban’s organic acid adoption.

-

2024: Kemira Oyj expanded its formic acid distribution network in North America in 2024, partnering with agricultural distributors to improve access for livestock and poultry feed producers seeking organic acid-based antimicrobial feed preservation solutions.

-

2024: Perstorp Group launched a new high-purity Grade 99% formic acid product line in 2024 targeting the pharmaceutical synthesis and specialty chemical markets whose API manufacturing and research grade chemical procurement requirements create premium commercial relationships above agricultural-grade alternatives.

Formic Acid Market Key Players

-

BASF SE

-

Kemira Oyj

-

Perstorp Group AB

-

Yara International ASA

-

Eastman Chemical Company

-

Evonik Industries AG

-

Gujarat Narmada Valley Fertilizers & Chemicals Ltd. (GNFC)

-

Luxi Chemical Group Co., Ltd.

-

Feicheng Acid Chemicals Co., Ltd.

-

Rashtriya Chemicals and Fertilizers Ltd.

-

Chongqing Chuandong Chemical Group Co., Ltd.

-

Anhui Asahi Kasei Chemical Co., Ltd.

-

Wuhan Ruisunny Chemical Co., Ltd.

-

Shandong Baoyuan Chemical Co., Ltd.

-

Beijing Chemical Industry Group Co., Ltd.

-

Celanese Corporation

-

TCI Chemicals (India) Pvt. Ltd.

-

Polioli S.p.A.

-

Shandong Qingyun Weiye Chemical Co., Ltd.

-

Fujian Shaowu Yongfei Chemical Co., Ltd

Formic Acid Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.36 Billion |

| Market Size by 2035 | USD 4.00 Billion |

| CAGR | CAGR of 5.47% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Grade (Grade 85%, Grade 94%, Grade 99%, Others) • by Application (Animal Feed & Silage Preservation, Leather Tanning & Processing, Textile Dyeing & Finishing, Rubber Processing, Chemical Synthesis, Pharmaceutical & Food Additive, Others) • by End Use (Agriculture, Leather Industry, Textile & Apparel, Rubber Industry, Chemical & Pharmaceutical, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | BASF SE, Kemira Oyj, Perstorp Group AB, Yara International ASA, Eastman Chemical Company, Evonik Industries AG, Gujarat Narmada Valley Fertilizers & Chemicals Ltd. (GNFC), Luxi Chemical Group Co., Ltd., Feicheng Acid Chemicals Co., Ltd., Rashtriya Chemicals and Fertilizers Ltd., Chongqing Chuandong Chemical Group Co., Ltd., Anhui Asahi Kasei Chemical Co., Ltd., Wuhan Ruisunny Chemical Co., Ltd., Shandong Baoyuan Chemical Co., Ltd., Beijing Chemical Industry Group Co., Ltd., Celanese Corporation, TCI Chemicals (India) Pvt. Ltd., Polioli S.p.A., Shandong Qingyun Weiye Chemical Co., Ltd., Fujian Shaowu Yongfei Chemical Co., Ltd. |

Frequently Asked Questions

The Formic Acid Market is expected to grow at a CAGR of 5.47% from 2026 to 2035.

The Formic Acid Market was valued at USD 2.36 Billion in 2025.

Rising adoption in the leather and textile industry which drives market growth, and growing demand for organic acid-based animal feed preservation as EU antibiotic bans and global antimicrobial resistance action plans create structural formic acid procurement in livestock and poultry production systems.

Grade 85% dominated the Formic Acid Market with approximately 52% share in 2025, while Grade 99% is the fastest growing for pharmaceutical and specialty chemical applications. As confirmed by SNS Insider, Grade 85% will grow rapidly in the Formic Acid Market.

Asia Pacific dominated the Formic Acid Market in 2025 with the highest revenue share, while North America is the fastest-growing region.

Get in Touch