Functional Fluids Market Analysis & Overview

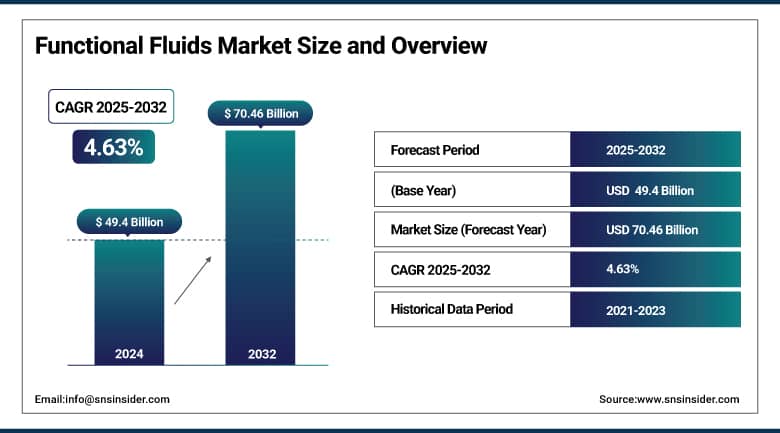

The Functional Fluids Market size was USD 49.4 billion in 2024 and is expected to reach USD 70.46 billion by 2032, growing at a CAGR of 4.63% over the forecast period of 2025-2032.

Functional fluids market analysis highlights the increasing utilization across the aerospace and defense industries. These industries demand highly specialized fluids such as hydraulic fluids, lubricants, and heat transfer fluids that can withstand extreme temperatures, pressures, and operational stresses. Functional fluids are essential in ensuring the performance, safety, and longevity of critical aerospace components like turbines, actuators, and landing gear systems. In defense applications, reliability under combat and mission-critical conditions is paramount, further elevating the need for high-performance functional fluids which drive the functional fluids market growth.

Additionally, with increased global investments in military modernization, aircraft manufacturing, and space exploration programs, the demand for advanced fluids tailored to these high-stakes environments continues to grow. This trend is further supported by technological advancements that enhance fluid performance and compliance with stringent aerospace standards, positioning the sector as a key driver in the overall functional fluids market.

In fluid systems, specifically hydraulic and cleaning fluids, the EPA National Emission Standards for Hazardous Air Pollutants (NESHAP) for aerospace operations must be met, creating an ongoing need for high-performance, low-toxicity functional fluids.

According to the Aerospace Industries Association, the US aerospace & defense industry provided USD 533 billion in direct economic output, representing a total of USD 955 billion in economic activity in 2023, including direct and indirect economic impact.

To Get More Information On Functional Fluids Market - Request Free Sample Report

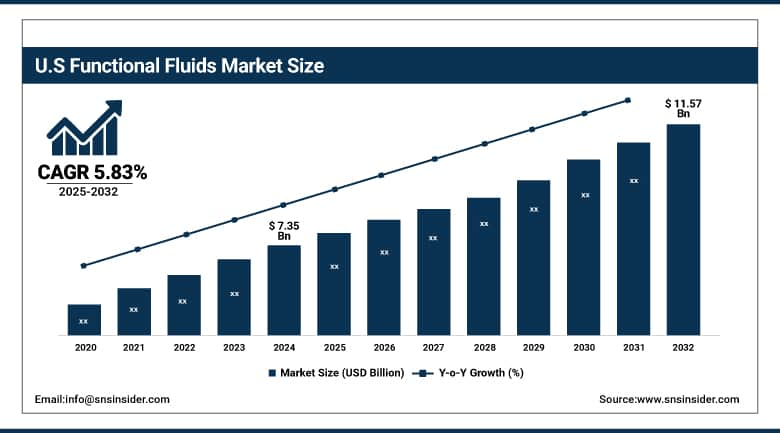

The U.S. Functional Fluids Marketsize was USD 7.35 billion in 2024 and is expected to reach USD 11.57 billion by 2032 and grow at a CAGR of 5.83% over the forecast period of 2025-2032. It is driven by an extensive ecosystem of manufacturing industries; a high pace of technological innovation, and a dominant share in end-use sectors such as automotive, aerospace, manufacturing, and oil & gas. The U.S., being the largest economy in the world, has many multinationals and manufacturing centers that utilize a large degree of functional fluids to ensure that the machinery works well, to manage heat, and to optimize processes.

Functional Fluids Market Drivers

-

Rising demand for data centers and electronics cooling drives the market growth.

The functional fluids market growth is driven by the increase in consumption of data centers and electronics cooling. The unprecedented increase in internet penetration, cloud computing, and digital services has resulted in a phenomenal growth in the number and size of data centers across the world. Such facilities create a considerable amount of heat, thus requiring advanced cooling technologies that rely extensively on high-performance heat transfer fluids. Functional fluids used in data center cooling systems help to maintain the operating temperature within safety limits, prevent equipment failure, and increase energy efficiency. Moreover, the increasing number of electronics in automotive, industrial automation, and consumer devices also drives the demand for reliable thermal management.

The Department of Energy (DOE) has the National Renewable Energy Laboratory (NREL) working on geothermal-based thermal energy storage systems that can be utilized to improve cooling efficiency in data centers, since up to 40% of the energy consumed by a data center is used to cool it.

The DOE estimates that energy use in U.S. data centers might triple over the next few years, and that they could eventually consume as much as twelve percent of total electricity.

Functional Fluids Market Restrain

-

Volatility in raw material prices may hamper the market growth.

The functional fluids market growth can be hindered, on the other hand, owing to the high dependency on petrochemical derivatives and base oils, concerning which raw material prices are volatile. The key inputs for these are derived from crude oil, the prices of which are very sensitive to geopolitical tensions, supply chain disruptions, regulation, global demand, etc. The profitability of manufacturers is greatly affected when crude oil prices jump, as it also causes a substantial increase in the cost of producing functional fluids (lubricants, hydraulic fluids, heat transfer fluids, etc.). Such volatility in pricing, however, is a challenge for companies to pass the additional costs to the end users, and therefore, these fluids are less than competitive in price-sensitive markets.

Functional Fluids Market Opportunities

-

Growing focus on defense modernization creates an opportunity in the market.

There is a major opportunity in the functional fluids market coming from the agenda of modernization of defense. Countries around the world are increasingly pouring a lot of money into strengthening their defense systems, building and buying the latest military vehicles, aircraft, naval fleets, and weapons systems. With modern high-performance materials such as high winds, fuel micro-meteors, and such, advanced defense platforms rely on highly specialized fluids (hydraulic fluids, thermal transfer fluids, lubricants, etc.) that operate reliably over wide temperature, pressure, and other such operational requirements. Functional fluids are essential to mission readiness, safety, and the long-term durability of high-performance equipment used by ground, sea, and air defense which drive the functional fluids market trends.

In its FY 2024 National Defense Industrial Strategy, the DoD directed USD 670 M+ in Defense Production Act grants and USD 1.6B in innovation funding to 160 projects, including hypersonics, shipbuilding, and critical materials. Investment incentives and grants for advanced manufacturing support domestic specialty fluid production and a secure supply chain of defense-grade fluid products.

Functional Fluids Market Segmentation Analysis

By Type

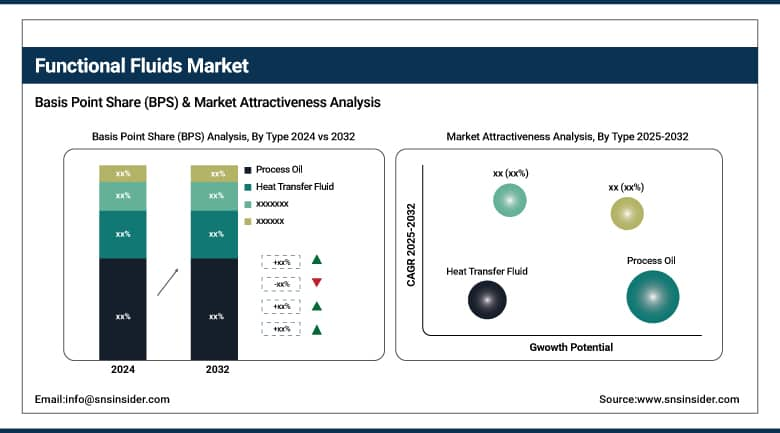

Process oil held the largest functional fluids market share, around 34%, in 2024. It is owing to the high usage of different functional fluids in various high-demand industries including rubber, plastic, textiles, and personal care. These oils are employed as processing aids & lubricants in material manufacturing for product quality improvement, performance enhancement, and lubricant oils supply equipment with proper machinery running. Because of the capabilities to alter viscosity and also to enhance flow behavior and assist in filler and additive dispersion, they are valuable in polymer and rubber compounding.

Heat transfer fluid held a significant functional fluids market share owing to its important function to maintain the optimal thermal performance in various industrial applications. These fluids are used in applications where efficient thermal energy exchange is essential to the success of the process, such as chemical processing, renewable energy plants (concentrated solar power), oil and gas refineries, food processing, and HVAC. This characteristic gives them suitability for extremely high and low-temperature industrial use, maintaining consistent and safe thermal management. The rise of elite manufacturing avenues and the need ratio of energy-efficient fluids has also led to an increase market share of heat transfer fluid.

By Application

The industrial segment held the largest market share, around 40.23%, in 2024. It is due to the large-scale use of functional fluids in various manufacturing and processing industries that the industrial segment occupied the largest share of the functional fluids market. Functional fluids play an important role in the industrial sectors, working to maintain the performance of machinery, reduce mechanical wear and tear, and ensure the smooth operation of equipment, including hydraulic fluids, metalworking fluids, lubricants, and heat transfer fluids. These fluids are vital to the successful operation and life of key industries such as automotive manufacturing, aerospace, heavy machinery, chemicals & electronics.

The construction holds a significant market share in the functional fluids market. It is owing to the utilization of hydraulic machinery, earth-moving equipment, and other performance-driven tools that require high-performance fluids for functioning in a safe and efficient manner. Hydraulic oils, transmission fluids, greases, and other functional fluids are important for the operation of cranes, excavators, bulldozers, concrete mixers, and other equipment utilized in major infrastructure activities. With the ongoing global urbanization process and an increase in investments by governments in the construction of roads, bridges, smart cities, and housing developments, the demand for construction machinery and the fluids that drive them is on the rise as well.

Functional Fluids Market Regional Outlook

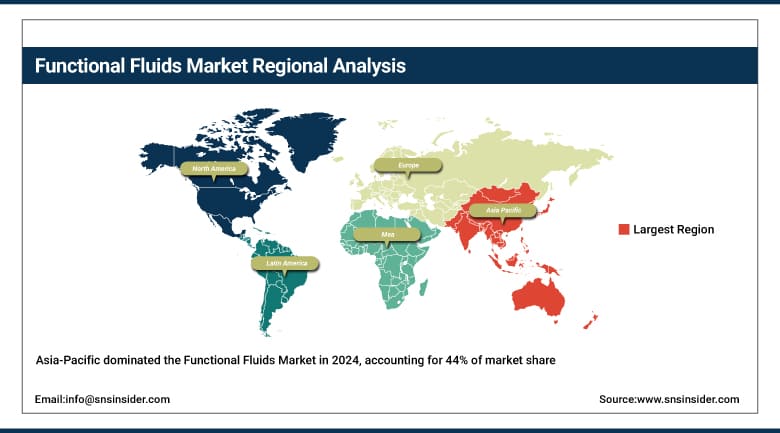

Asia-Pacific held the largest market share, around 44%, in 2024. It is owing to the rapidly expanding industrial base, growing automotive production, and the increasing construction activities across the key economies, including China, India, Japan, and South Korea. The region holds some of the largest manufacturing hubs globally, and functional fluids are used extensively for the maintenance of machinery, metalworking, lubrication, and thermal regulation. Furthermore, the expanding construction industry, bolstered by new infrastructure projects, urbanization, and government spending, expands the need for hydraulic and transmission fluids. With the growing automotive industry, especially in China and India, the demand for manufacturing and servicing of vehicles has increased the consumption of functional fluids in the Asia-Pacific and functional fluids companies focused on increasing their presence in the market.

In February 2024, Japan International Cooperation Agency (JICA) signed credit agreements worth USD 1.54 billion to develop transportation corridors and climate-resilient infrastructure in India, thus driving demand for industrial & Hydraulic fluids.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America functional fluids market held a significant market share and is the fastest-growing segment in the forecast period. It is account to its robust industrial infrastructure coupled with high-tech industrial know-how, and favorable demand from major end-use verticals including automotive, aerospace, construction, and manufacturing. High-performance functional fluids are used for lubrication, cooling, and hydraulic systems in many of the country’s top automotive and aerospace manufacturers located in the U.S. and Canada. Moreover, the existence of a challenging oil & gas infrastructure, metalworking, and chemical processing industries ensures a gradual volume of this fluid. The government's focus on modernizing infrastructure and higher investments in the defence and energy sectors has also boosted demand in the functional fluids industry.

The U.S. Department of Energy (DOE) awarded USD 78 million to its RAPID Institute, focused on advanced manufacturing technologies to accelerate industrial decarbonization in the chemical sector, including specialty and performance chemicals.

Europe held a significant market share in the forecast period. It is because of its well-established industrial base, strict environmental regulations, and high demand from the automotive, aerospace, manufacturing, and renewable energy industries during the forecast period. The functional fluids market is driven by the presence of major automotive manufacturers and leading aerospace companies in the region, which largely use functional fluids in the automotive and aerospace verticals, including lubrication, thermal management, and hydraulics. Moreover, the progressive sustainability trend in Europe boosted demand for environment-friendly and advanced formulations of the fluids, primarily in Germany, France and the Netherlands.

Functional Fluids Market Companies are:

-

ExxonMobil Corporation

-

BASF SE

-

Dow Inc.

-

TotalEnergies SE

-

Royal Dutch Shell plc

-

Clariant AG

-

Huntsman Corporation

-

Lubrizol Corporation.

Recent Development:

-

In 2024, Chevron unveiled Clarity BioEliteSyn AW, a new high-performance hydraulic fluid for marine and construction equipment. The container product is more than 90% renewable carbon-based, in compliance with strict eco-standards, matched with high performance and long-term durability.

-

In 2024, ENEOS introduced a line of EV/Hybrid fluids and high‑performance lubricants at the 2024 SEMA Show, targeting aftermarket and motorsport applications, underscoring the rising focus on electrified vehicle platforms.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 49.04 Billion |

| Market Size by 2032 | USD 70.46 Billion |

| CAGR | CAGR of 4.63% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Type (Process Oil, Hydraulic & Transmission Fluid, Metal Working Fluid, Heat Transfer Fluid, Other) •By Application (Industrial, Construction, Transportation, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | ExxonMobil Corporation, Chevron Corporation, BASF SE, Dow Inc., TotalEnergies SE, Royal Dutch Shell plc, Eastman Chemical Company, Clariant AG, Huntsman Corporation, Lubrizol Corporation. |

Frequently Asked Questions

Ans: Asia Pacific led the Functional Fluids Market in the region with the highest revenue share in 2024.

Ans: Rising demand for data centers and electronics cooling drives the market growth.

Ans: Industrial will grow rapidly in the Functional Fluids Market from 2025 to 2032.

Ans: The expected CAGR of the global Functional Fluids Market during the forecast period is 4.63%

Ans: The Functional Fluids Market was valued at USD 49.04 billion in 2024.

Get in Touch