Precision Genomic Testing Market Report Scope & Overview:

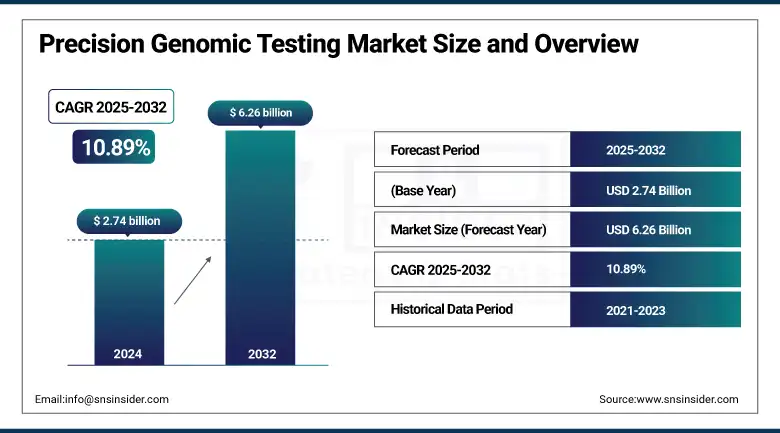

The precision genomic testing market size was valued at USD 2.74 billion in 2024 and is expected to reach USD 6.26 billion by 2032, growing at a CAGR of 10.89% over 2025-2032.

The global precision genomic testing market is witnessing rapid advancement due to the convergence of next-generation sequencing, AI-driven analytics, and personalized medicine. Increasing demand for tailored diagnostics in oncology, reproductive health, and rare diseases is a key growth factor. The U.S. precision genomic testing market is notably driven by payer coverage expansion and the integration of genomic data in clinical workflows. A significant surge in demand is observed, with nearly 8–12 times more requests for genome-based diagnostics over the past decade. Investments in this space are robust over USD 10 billion in venture capital funneled into genomic startups between 2020 and 2024.

To Get more information On Precision Genomic Testing Market - Request Free Sample Report

For instance, in May 2024, Illumina launched its PrimateAI-3D tool for clinical interpretation of genetic variants, advancing predictive genomics.

Additionally, the R&D spending by key precision genomic testing companies such as Thermo Fisher, Illumina, and Guardant Health has increased steadily, supporting innovation in AI and liquid biopsy tools. Regulatory support is strengthening: the U.S. FDA’s approval of multi-gene NGS panels and the CMS’ reimbursement coverage expansion are propelling adoption. Furthermore, cloud-based genomic data platforms and AI-enabled interpretation tools are improving accessibility and scalability, which is accelerating precision genomic testing market growth and transforming the healthcare landscape.

In July 2024, Guardant Health secured FDA approval for its Shield blood-based colorectal cancer screening test, reinforcing the regulatory momentum in the U.S. precision genomic testing market.

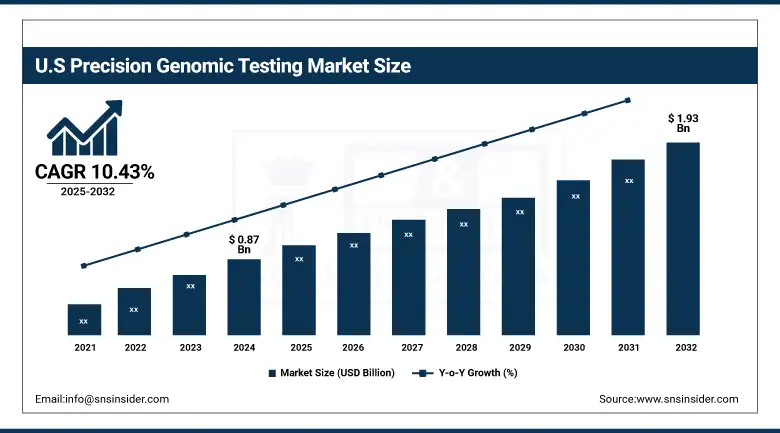

The U.S. precision genomic testing market size was valued at USD 0.87 billion in 2024 and is expected to reach USD 1.93 billion by 2032, growing at a CAGR of 10.43% over 2025-2032. The U.S. is the largest country in this region, and it's responsible for more than 65% of whole North American market. That supremacy has recently been strengthened by a proliferation of precision medicine projects, including NIH’s “All of Us” and FDA greenlighting of multi-gene diagnostic panels. Significant R&D spend of over USD 50 billion a year in biomedical research and a strong representation from key players such as Illumina, Thermo Fisher, and Guardant Health also underpins the region. Canada is also broadening its footprint and is home to government-supported organizations, including Genome Canada, which, by investing over CAD 940 million in genomics projects, is supporting a growing North American market.

Market Dynamics:

Drivers:

-

Technological Advancements, Rising Investments, and Increasing Clinical Utility are the Major Factors Fueling the Growth of the Precision Genomic Testing Market

The precision genomic testing market is primarily driven by increasing clinical adoption of genomic profiling across oncology, cardiology, and infectious diseases. Demand is surging due to the rise in personalized medicine and preventive health programs, with more than 80% of oncologists in the U.S. using some form of genetic testing to guide treatment decisions. On the supply side, massive R&D investments by companies like Exact Sciences and Agilent Technologies, which spent over USD 200 million collectively in R&D in 2023, are fueling innovation in multiplex assays, cfDNA tests, and CRISPR-based diagnostics.

Furthermore, regulatory support is accelerating adoption; the FDA approved FoundationOne CDx and MSK-IMPACT as companion diagnostics, setting clinical precedence. The global rise in genomic data generation, estimated at 40 exabytes annually, is also pushing demand for precision testing platforms integrated with AI and cloud computing. Additionally, initiatives such as the Global Alliance for Genomics and Health (GA4GH) are setting frameworks for data interoperability and privacy, further enabling growth in the global precision genomic testing market. These drivers combined are accelerating both clinical demand and commercial innovation, supporting sustainable precision genomic testing market growth.

Restraints:

-

High Costs, Data Privacy Concerns, and Disparities in Access are the Key Limitations Hindering the Growth of the Global Precision Genomic Testing Market

Despite significant progress, the precision genomic testing market faces several barriers. A major restraint is the high cost of sequencing and test interpretation, which limits accessibility in low-resource healthcare systems.

For instance, while whole-genome sequencing costs have dropped, downstream analysis and clinical interpretation remain expensive, averaging USD 1,000–USD 2,000 per patient.

Additionally, data security and patient privacy are growing concerns; a recent survey by the American Medical Association found that 58% of clinicians worry about the misuse of genomic data in insurance and employment settings. Moreover, regulatory inconsistencies across regions, especially in the validation and reimbursement of LDTs (Laboratory Developed Tests), slow down market penetration. The shortage of skilled genetic counselors also adds to operational challenges, with only 1 genetic counselor available for every 100,000 patients in many regions. Furthermore, lack of standardized clinical guidelines in emerging markets and limited awareness among general practitioners affect test uptake. These challenges collectively inhibit broader clinical adoption, particularly in non-oncology settings, despite the potential of precision testing. Addressing these restraints is critical for realizing the full potential of the precision genomic testing market share globally.

Segmentation Analysis:

By Product & Service

Consumables were the largest product segment in 2024, representing more than 35% of the precision genomic testing market share. Owing to their continual use in each cycle of genomic testing (e.g., extraction kits, library preparation reagents, amplification buffers), demand is expected to be stable. The bulk of consumables are consumed in labs and testing companies, not only as high-throughput platforms, for instance, NGS, become more prevalent.

By contrast, the software segment has been growing fastest, reflecting the rise of AI-based genomic interpretation tools. The requirement to process big amounts of genomic data and provide clinically relevant findings is also driving the investment in data analytics platforms. Cloud-based applications and incorporated workflow mapping software are becoming increasingly popular, with diagnostic labs and predictive diagnostic biotech firms leading the charge.

By Technology

The next-generation sequencing (NGS) segment accounted for the largest share of the global precision genomic testing market in 2024, and was valued at over 45%. Its high throughput, decreasing cost, and the possibility to interrogate multiple genes at the same time have become the basis of a wide array of applications including cancer genomics, inherited disease diagnostics, and population-scale screening. Adoption of NGS is skyrocketing as the technology transitions out of research labs and into the clinic.

The CRISPR/Cas system was identified as the most rapidly expanding technology segment, driven by increasing utilization in diagnostics and target validation. Its capacity to locate specific DNA mutations with high precision is transforming areas such as rare disease diagnosis and pathogen detection. This proliferation of CRISPR-based diagnostic startups and patent applications also illustrates its increasing impact in precision diagnostics.

By Application

In 2024, oncology held the application industry share of 57% of the precision genomics testing market. Statement on: Cancer remains a major global health issue, and precision testing is utilized to inform treatment choice, to monitor disease recurrence, and response to drugs. Meanwhile, companion diagnostics and liquid biopsies have added new life to this side of the segment.

In contrast, reproductive & prenatal health is the fastest-growing application sector. Rising consciousness regarding early genetic diagnosis, along with growing maternal age and demand for non-invasive prenatal screening (NIPS), is promoting the market development. It’s also becoming more common for fertility/IVF clinics to offer carrier screening and preimplantation genetic diagnosis (PGD), marking a move towards proactive, genomics-led reproductive care. It has both regulatory approval and technical availability to help this expansion process.

By Sample Type

Blood samples dominated the landscape on a sample type basis in 2024, with more than 44% of the market. Blood is still considered the gold standard for most genomic analyses because it is easy to collect, non-invasive, and can be used for technologies such as cfDNA analysis and liquid biopsy. Oncology, infectious disease, and rare disease applications are common use cases for blood-derived samples.

Meanwhile, saliva samples are the fastest-growing sample type, mainly driven by their adoption for direct-to-consumer (DTC) testing. Genomic assays testing on saliva are non-invasive, easy to use, and appropriate for remote, large-scale population research. Adoption is growing due to their expanded use in ancestry, wellness, and pharmacogenomics testing. Furthermore, the regulatory support for at-home collection approaches has improved their clinical and market potential.

By End User

The end-user segment is dominated by diagnostic laboratories in 2024, with market share of over 38%. These laboratories act as centralized high-throughput processing centers that have standardized and validated assays. Their utilization of advanced genomic platforms and expertise in NGS, PCR, and microarray techniques along with other sequencing technologies makes them the preferred supplier to hospitals, clinics, and laboratories.

On the other hand, pharmaceutical & biotechnology companies is the fastest-growing end-user segment. Growth is being enabled by companion diagnostics, pharmacogenomics, and genomic-based drug discovery. These firms are employing precision genomics testing to identify sub-populations of sick as well as well patients to validate new drug targets and to prevent drop outs in clinical trials. Investments in biomarker platforms and partnerships with diagnostic developers support their increasingly important role in this market.

Regional Analysis:

The precision genomic testing market in North America in 2024 was led by a well-developed healthcare system, growing use of genomics in clinical settings, and favorable reimbursement scenario.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe represents the second leading position in the overall precision genomic testing market due to the favorable regulatory pathways, government funding, and growing application of genomics in healthcare. Germany is the largest country in the region, and the high adoption of tests and government-supported precision health programs is driving the market. The country has deployed national genome sequencing efforts and invested significantly in AI-powered diagnostics. The UK is also moving swiftly, as exemplified by initiatives such as Genomics England or the integration of genomic medicine into the NHS. France and Italy see continued uptake in Oncology and Prenatal screening. Supported by Europe’s focus on ethical use of genomic data and cross-border regulation for data sharing, a joined-up framework has been established that has driven development and uptake of tests.

The precision genomic testing market in Asia Pacific is growing at the fastest rate owing to increasing access to healthcare, growing awareness, and supportive government initiatives. China is leading the pack in the region, supported by a national genomics strategy and significant investments in biotech with over USD 12 billion pledged for genomic medicine R&D up to 2025. Domestic innovation is being led by companies such as BGI Genomics and WuXi NextCODE. India is also seeing rapid growth, underpinned by government programs such as Genomics for Public Health and growing demand for DTC tests. Japan is still ahead of the game in the integration of research, especially oncology, in a close connection between academia and industry. High population-scale sequencing, rising middle-class healthcare spend, and adoption of AI-tech are amongst the factors that make Asia Pacific the fastest-growing region.

Key Players:

Leading precision genomic testing companies driving the market include Thermo Fisher Scientific, Illumina, Roche, QIAGEN, Agilent Technologies, Guardant Health, Foundation Medicine, Exact Sciences, Myriad Genetics, GRAIL, Oxford Nanopore Technologies, PacBio, 10x Genomics, Genomic Health, Revvity, GenScript, Maravai LifeSciences, Abbott Laboratories, Danaher Corporation, NantHealth.

Recent Developments:

In June 2024, Illumina Inc. launched its NextSeq 1000Dx sequencing system, receiving FDA 510(k) clearance for clinical use. This development strengthens its diagnostic platform portfolio and supports broader clinical adoption of genomic testing in certified labs.

In April 2024, Roche announced the CE-IVD approval of its AVENIO Tumor Tissue CGP Kit, enabling comprehensive genomic profiling (CGP) in decentralized labs across Europe. This advancement aims to enhance precision oncology access beyond centralized testing facilities.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 2.74 billion |

| Market Size by 2032 | USD 6.26 billion |

| CAGR | CAGR of 10.89% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product & Service [Consumables (Kits, Reagents), Instruments, Software, Services, Others (Laboratory automation tools, Storage and logistics solutions specific to genomic workflows)] • By Technology [Next-Generation Sequencing (NGS), Polymerase Chain Reaction (PCR), Microarray Technology, Sanger Sequencing, CRISPR/Cas Systems, Others (Whole Genome Amplification (WGA), Nanopore sequencing, Digital PCR (dPCR))] • By Application [Oncology, Cardiovascular Diseases, Neurological Disorders, Reproductive & Prenatal Health, Infectious Diseases, Rare Diseases, Others (Autoimmune diseases, Metabolic disorders, Personalized wellness, etc.)] • By Sample Type [Blood Samples, Tissue Samples, Saliva Samples, Urine Samples, Others (Buccal swabs, Amniotic fluid, etc.)] • By End User [Hospitals and Clinics, Diagnostic Laboratories, Research & Academic Institutes, Pharmaceutical & Biotechnology Companies, Others (Contract research organizations (CROs), Direct-to-consumer (DTC) genetic testing companies)] |

| Regional Analysis/Coverage | North America (U.S., Canada), Europe (Germany, France, UK, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America) |

| Company Profiles | Thermo Fisher Scientific, Illumina, Roche, QIAGEN, Agilent Technologies, Guardant Health, Foundation Medicine, Exact Sciences, Myriad Genetics, GRAIL, Oxford Nanopore Technologies, PacBio, 10x Genomics, Genomic Health, Revvity, GenScript, Maravai LifeSciences, Abbott Laboratories, Danaher Corporation, NantHealth. |

Frequently Asked Questions

Ans: NGS technologies are foundational in enabling fast, scalable, and cost-effective DNA sequencing, supporting applications from genomics in oncology to infectious disease diagnostics.

Ans: Major precision genomic testing companies include Illumina, Thermo Fisher Scientific, Roche, QIAGEN, Guardant Health, and 10x Genomics, all driving precision healthcare innovation.

Ans: North America, particularly the U.S., dominates due to strong regulatory support, R&D spending, and clinical integration, followed by Europe and the rapidly growing Asia Pacific market.

Ans: Key drivers include increasing adoption of personalized medicine, rapid advancements in NGS technologies, and growing demand for genomic profiling in oncology and rare diseases.

Ans: The precision genomic testing market refers to the segment of healthcare focused on using genomic information to tailor diagnosis, treatment, and prevention strategies. It involves advanced DNA sequencing technologies and bioinformatics to support precision healthcare.

Get in Touch