Precision Medicine Market Report Scope & Overview:

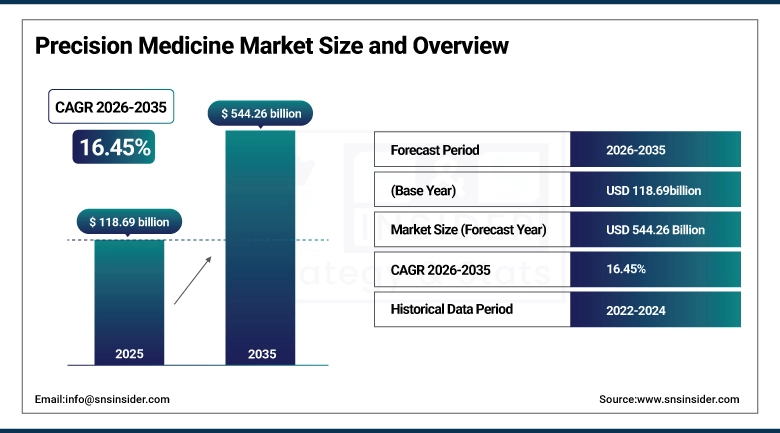

The Precision Medicine Market was valued at USD 118.69 Billion in 2025 and is projected to reach USD 544.26 Billion by 2035, growing at a CAGR of 16.45% during the forecast period 2026–2035.

The Precision Medicine Market analysis is a complete study of the current trends in the market, industry growth drivers, and restraints. It categorizes the market based on type, technology, application end user and region. Increasing adoption of personalized medicine and genome research supports market growth.

Precision Medicine reached 15 million patients in 2025, driven by genomic-based therapies and targeted treatments across oncology, cardiovascular, and rare diseases.

Precision Medicine Market Size and Forecast:

-

Market Size in 2025: USD 118.69 Billion

-

Market Size by 2035: USD 544.26 Billion

-

CAGR: 16.45% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Precision Medicine Market - Request Free Sample Report

Precision Medicine Market Trends:

-

Increasing attention toward personalized healthcare and patient centric treatments are expected to drive the adoption of targeted therapies and genomic medicine in oncology, cardiovascular and rare diseases.

-

The development of genomic sequencing and CRISPR technology coupled with big data has driven the pace of progress in genetic medicine, illuminating the possibilities by shortening diagnostic times and clarifying treatment options.

-

Precision medicine initiatives and personalized care policies by governments are fuelling hospitals, research institutes and pharma companies to employ advanced therapies.

-

AI and data analytics in support of clinical decision making are improving patient responsiveness, predictive diagnostics, and tailored therapy.

-

Rising patient consciousness along with increased demand for personalized therapies is broadening market avenues, especially in the oncology, rare genetic disorders and chronic diseases sector.

U.S. Precision Medicine Market Insights:

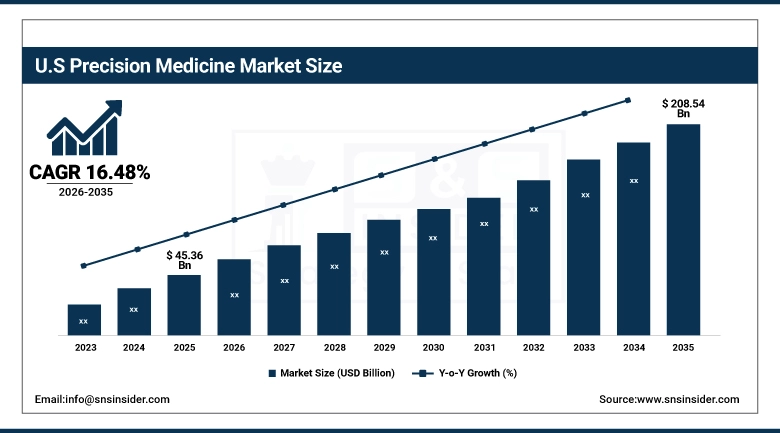

The U.S. Precision Medicine Market is projected to grow from USD 45.36 Billion in 2025 to USD 208.54 Billion by 2035 at a CAGR of 16.48%. Defined by targeted treatments and genomic testing Growth is fueled by Oncology, rare disease treatment and integration of AI into therapy, and proliferation of personalized medicine approaches.

Precision Medicine Market Growth Drivers:

-

Growing adoption of genomic-based therapies and AI-driven diagnostics is accelerating demand for personalized healthcare solutions.

Increasing use of genomic-based diagnostic, and treatment solutions is driving the Precision Medicine market growth. By 2025, more than 15 million patients had been treated with targeted therapies in oncology, cardiovascular and rare disease indications. The U.S., Germany and Japan are among countries that are scaling up genomic testing programmes and deploying AI tools in hospitals and research institutes. These activities further promote personalized therapy research, delivery of and access to it in turn expanding the market space where precision healthcare technologies can innovate.

Precision Medicine adoption enabled over 18 million targeted treatments in 2025, driven by oncology, rare genetic disorders, and cardiovascular applications.

Precision Medicine Market Restraints:

-

High costs of genomic testing and complex regulatory approvals are limiting widespread adoption of precision therapies.

The cost of genomic testing and regulatory hurdles are the key factors potential influencing the growth of Precision Medicine Market. In 2025, 40% of patients for whom targeted and genomic-guided therapy is indicated did not receive them due to affordability and access limitations. Smaller hospitals and clinics have a difficult time adopting sophisticated diagnostic platforms relative to their larger research- institute counterparts. In addition, long approval times, irregular reimbursement decisions and a shortage of skilled personnel restrict the widespread adoption of precision therapies despite increasing demand for personalized healthcare.

Precision Medicine Market Opportunities:

-

Integration of AI and wearable health technologies presents significant opportunities for expanding personalized and preventive healthcare solutions.

AI and Wearable Health devices are being integrated which is spurring the Precision Medicine sector. By 2025, more than 10 million patients had used AI-supported diagnoses or treatment devices and remote patient monitoring, with projections of an additional 25-million-plus by 2035. Hospitals, research centers and biotech companies are increasingly using these technologies to tailor treatments and prevent disease. Increases in "real-time" health monitoring and predictive analytics have transformed it into a practice that is more effective, accessible, and profitable.

AI-assisted diagnostics and wearable health technologies accounted for 20% of new precision treatments in 2025, driven by hospitals, research institutes, and preventive care.

Precision Medicine Market Segmentation Analysis:

-

By Type, Targeted Therapy held the largest market share of 45.72% in 2025, while Pharmacogenomics is expected to grow at the fastest CAGR of 18.27%.

-

By Technology, Next-Generation Sequencing (NGS) dominated with a 38.91% share in 2025, while CRISPR is projected to expand at the fastest CAGR of 19.05%.

-

By Application, Oncology accounted for the highest market share of 42.36% in 2025, and Rare & Genetic Disorders are projected to record the fastest CAGR of 18.78%.

-

By End User, Hospitals held the largest share of 40.58% in 2025, while Research Institutes are expected to grow at the fastest CAGR of 17.92%.

By Application, Oncology Dominates While Rare & Genetic Disorders Expand Rapidly:

Oncology sector dominated the Applications segment, having been used on over 7.2 million patients in 2025, due to the wide usage of targeted drugs and companion diagnostics. High incidence of cancer and robust treatment programs reinforce its pre-eminence. The Rare & Genetic Disorders sector is the fastest-growing Application segment and 2.3 million patients are treated in 2025 owing to genomic sequencing, personalized treatment plans, and the increasing investment for development of drugs for rare diseases.

By Type, Targeted Therapy Dominates While Pharmacogenomics Expands Rapidly:

Targeted Therapy sector dominated the Type segment with a market share of 6.8 million patients treated in 2025 due to its high acceptance in Oncology, Cardiovascular and Chronic disease management. Its primary is backed by evidence-based treatments, sophisticated diagnostics and it organizes the hospital's systems. The pharmacogenomics sector is the fastest-growing Type segment garnering a size of about 2.1 million patients by 2025 driven by increasing usage of personalized drug-response testing, genomic-guided prescriptions, and rising awareness among healthcare professionals and patients.

By Technology, Next-Generation Sequencing (NGS) Dominates While CRISPR Expands Rapidly:

The Next-Generation Sequencing (NGS) sector dominated the Technology segment with more than 5.5 million in number of tests performed in 2025 due to its use for detecting genetic mutations and driving targeted therapies. Its popularity is further supported by cost reductions and routine diagnostics incorporation. The CRISPR sector is the fastest-growing Technology segment, with 1.8 million patients benefiting in 2025 due to innovations in gene therapy, clinical trials and rising use of research for rare genetic diseases.

By End User, Hospitals Dominate While Research Institutes Expand Rapidly:

Hospitals sector dominated the End User segment, generating precision treatment for more than 8.1 million patients in 2025 on account of infrastructure development, trained professionals and integrated diagnosis systems. Their supremacy is an indication of volume and running efficiently. Research Institutes sector is the fastest growing End User segment which was estimated to be about 2.5 million patients served in 2025 due to increase adoption of AI assisted diagnostics, clinical trials and application for innovation in personalized medicine applications.

Precision Medicine Market Regional Analysis:

North America Precision Medicine Market Insights:

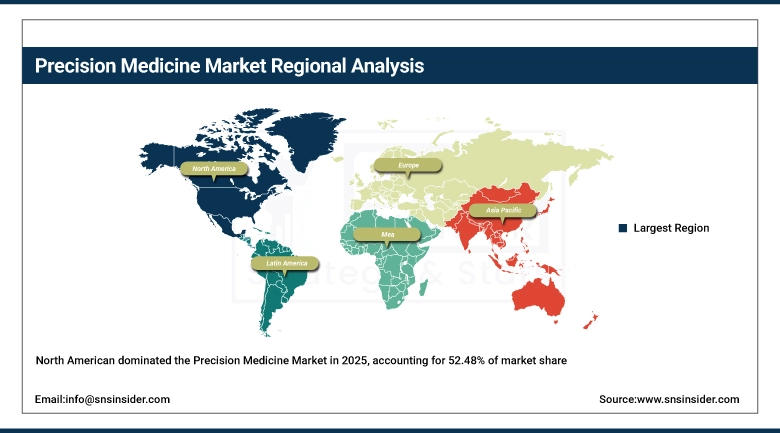

The North America region dominated the Precision Medicine Market with a 52.48% share in 2025, serving more than 7.5 million patients comprising oncology, cardiovascular conditions, and rare genetic disorders. Superior governing efforts and a high adaption rate of genome testing is influencing the region’s dominance. The growth of precision diagnostics and targeted therapies, and the rapid expansion of hospitals and research institutes are making North America the biggest market in the world - while stimulating innovation and technology uptake.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Precision Medicine Market Insights:

The U.S. administered precision treatments to over 6.8 million patients in 2025, including 4.2 million for cancer and 1.5 million for cardiovascular care. Massive growth is being driven by personalized treatment, genomic testing, AI/VR diagnostics and companion diagnostics and government initiatives while hospitals and research institutes increase their adoption of personalized healthcare.

Asia-Pacific Precision Medicine Market Insights:

Asia Pacific is the fastest growing in Precision Medicine Market with a CAGR of 18.55%, owing to rising usage of targeted treatments, genome testing and AI-based diagnosis. In 2025, China provided more than 3.5 million precision therapies and India treated nearly 1.8 million patients. Growth will be driven by government healthcare policy, growing awareness, the establishment of hospitals and increased clinical trial activities in oncology, cardiovascular and rare genetic diseases.

China Precision Medicine Market Insights:

China treated more than 3.5 million patients with precision therapies in 2025; over 2.2 million in oncology and close to 1.3 million for cardiovascular and rare diseases. Growth is supported by government healthcare programs, proliferation of genomic testing and AI diagnostics, hospital infrastructure investments and rising clinical trials across the country.

Europe Precision Medicine Market Insights:

Europe precision-medicined more than 5.8 million people in 2025. The leader was Germany, with 2.1 million infected patients, followed by France with 1.5 million and Italy with 1.2 million. The main volume of treatments was in oncology though cardiovascular and rare diseases treatments were also high. The growth is attributed to the government healthcare policies, approbation of genomic testing and AI diagnostics, growing hospital network & clinical trials in key regional markets.

Germany Precision Medicine Market Insights:

Germany provided over 2.1 million patients precision therapies in 2025, with more than one million oncological and 0.7 cardiovascular and rare disease treatments delivered. Targeted therapies dominated the market. Growth is spurred by government healthcare programs, implementation of genomic testing, AI diagnostics and increasing hospital infrastructure investment in both therapeutic & diagnostic applications.

Latin America Precision Medicine Market Insights:

Latin America treated 1.619 million patients in 2025, (52% Brazil, Argentina 30%, Colombia 18%). Oncology and cardiovascular treatments were the mainstays, while rare disease therapies surged. Growth of the market is attributed to government healthcare initiatives, the rise in genomic testing and AI diagnostics adoption, and the overall increasing hospital infrastructure to support precision medicine in this region.

Middle East and Africa Precision Medicine Market Insights:

Middle East and Africa saw a patient pool of more than 0.95 million in 2025 including 0.40 million from UAE and 0.30 million from South Africa. Targeted therapies prevailed, and treatments for rare diseases surged. Growth will be supported by government healthcare initiatives, the development of genomic testing and AI diagnostics, and an increased number of hospitals and research facilities.

Precision Medicine Market Competitive Landscape:

Illumina, a U.S.-based genomics leader, dominates the precision medicine market through its next-generation sequencing technologies. By 2025, its next-generation sequencing platforms have empowered over 5 million genomic tests that have driven targeted therapies, companion diagnostics, and other forms of personalized medicine. The company’s extended range of products such as MiSeq and NovaSeq systems allows for applications in oncology, rare-disease diagnosis, and cardiovascular treatment. The reach, partnerships with hospitals and research institutions, and investment in genome-tools develop Illumina’s leadership.

-

In September 2025, Illumina partnered with pharmaceutical companies to develop KRAS companion diagnostics, aiming to improve personalized cancer therapies and accelerate targeted treatment adoption across oncology patients.

Thermo Fisher Scientific, the life sciences company, leads precision medicine with laboratory equipment, genomic solutions and diagnostic tools. By 2025, more than 4.5 million patients have had accessible benefits of its personalized therapeutic technologies in AI-assisted diagnostics and pharmacogenomics. Precision treatment adoption is furthered by strategic alliances with hospitals, research centers and biotechnology companies. Its extensive product portfolio, innovations and services offerings play role in driving market position.

-

In June 2025, Thermo Fisher launched its Orbitrap Astral Zoom and Excedion Pro mass spectrometers, providing higher speed and sensitivity for biopharma applications, omics research, and advanced diagnostic workflows.

Roche, a Swiss healthcare multinational, dominates precision medicine with its portfolio of targeted therapies, companion diagnostics, and genomic tests. Roche was able to serve more than 4 million patients in oncology, rare genetic diseases and cardiovascular medicine globally, in 2025. Innovation of personalized medicine, research organization collaboration, and diagnostic integration to patients’ care plans lead its management. Its patient-focused nature and on-going innovation in molecular diagnostics further establish Roche as a leader around the world.

-

In May 2025, Roche collaborated with Broad Clinical Labs to expand the adoption of SBX sequencing technology, enhancing genomic diagnostics and enabling broader implementation of precision medicine solutions globally.

Precision Medicine Market Key Players:

Some of the Precision Medicine Market Companies are:

-

Illumina

-

Thermo Fisher Scientific

-

Roche

-

Pfizer

-

Novartis

-

AstraZeneca

-

Johnson & Johnson

-

Merck & Co.

-

Abbott Laboratories

-

Medtronic

-

Qiagen

-

Guardant Health

-

Myriad Genetics

-

Foundation Medicine

-

Tempus Labs

-

Caris Life Sciences

-

Exact Sciences

-

Agilent Technologies

-

Siemens Healthineers

-

23andMe

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 118.69 Billion |

| Market Size by 2035 | USD 544.26 Billion |

| CAGR | CAGR of 16.45% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Targeted Therapy, Genomic Medicine, Pharmacogenomics, Companion Diagnostics, Others) • By Technology (Next-Generation Sequencing, PCR & qPCR, CRISPR, Bioinformatics, Others) • By Application (Oncology, Cardiovascular Diseases, Rare & Genetic Disorders, Neurological Disorders, Others) • By End User (Hospitals, Diagnostic Laboratories, Research Institutes, Pharmaceutical & Biotech Companies, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Illumina, Thermo Fisher Scientific, Roche, Pfizer, Novartis, AstraZeneca, Johnson & Johnson, Merck & Co., Abbott Laboratories, Medtronic, Qiagen, Guardant Health, Myriad Genetics, Foundation Medicine, Tempus Labs, Caris Life Sciences, Exact Sciences, Agilent Technologies, Siemens Healthineers, 23andMe |

Frequently Asked Questions

The Precision Medicine Market was valued at USD 118.69 billion in 2025.

The market is projected to reach USD 544.26 billion by 2035.

The market is expected to grow at a CAGR of 16.45% during the forecast period from 2026 to 2035.

Key growth drivers include advancements in genomics, rising adoption of personalized therapies, increasing prevalence of chronic diseases, and growth in companion diagnostics.

Technologies such as next-generation sequencing (NGS), artificial intelligence, biomarker-based diagnostics, and gene editing tools are significantly contributing to market growth.

Get in Touch