Prefabricated Panels Market Report Scope & Overview:

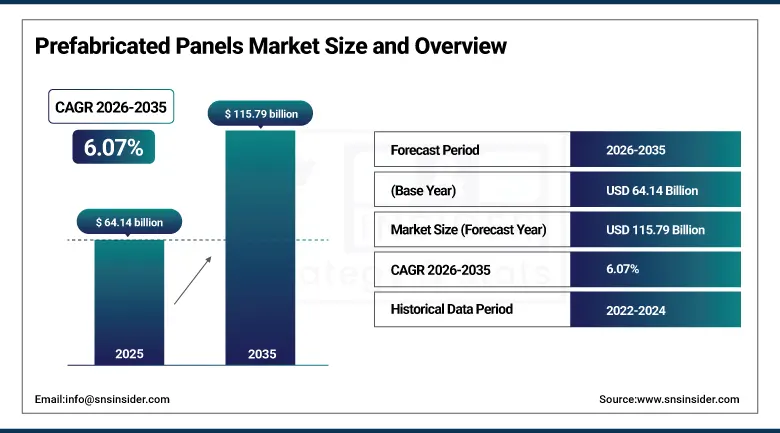

The Prefabricated Panels Market was valued at USD 64.14 Billion in 2025 and is expected to reach USD 115.79 Billion by 2035, growing at a CAGR of 6.07% from 2026–2035.

The Prefabricated Panels Market is growing strongly because of increasing demand for quick, cost-effective, and sustainable building options. Urbanization and infrastructure projects are speeding up the use of modular systems. Labor shortages in construction are prompting builders to turn to off-site production. Plus, new materials like insulated, composite, and eco-friendly panels make buildings more energy efficient and durable. Governments backing green buildings and smart cities are giving the market a boost too. Shorter construction times, less expensive projects, and better quality control are key drivers of global market growth.

According to the United Nations (UN DESA), 56% of the world’s population lives in urban areas in 2024, and this share is projected to reach 68% by 2050, significantly increasing demand for efficient housing and infrastructure solutions. According to the Global Alliance for Buildings and Construction (UNEP), the building sector accounts for around 37% of global CO₂ emissions, making construction efficiency improvements and low-carbon building technologies essential for achieving global decarbonization targets.

Key Market Size and Forecast

-

Market Size in 2026E: USD 68.03 Billion

-

Market Size by 2035: USD 115.79 Billion

-

CAGR: 6.07% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Prefabricated Panels Market - Request Free Sample Report

Key Market Trends

-

Rising demand for faster construction methods and reduced project timelines is driving the prefabricated panels market.

-

Growing adoption across residential, commercial, and industrial construction is boosting market growth.

-

Expansion of urbanization, infrastructure development, and housing projects is fueling panel deployment.

-

Increasing focus on cost efficiency, waste reduction, and sustainable construction practices is shaping adoption trends.

-

Advancements in insulation materials, lightweight composites, and modular panel systems are enhancing performance and durability.

U.S. Prefabricated Panels Market Outlook

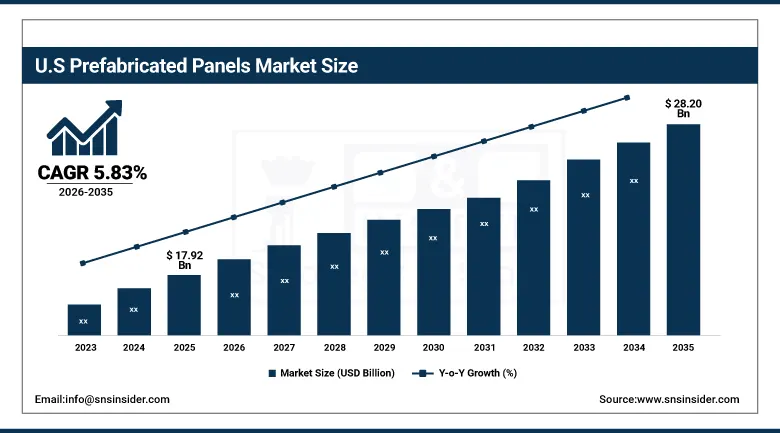

The U.S. Prefabricated Panels Market was valued at approximately USD 14.82 Billion in 2025 and is expected to reach approximately USD 28.51 Billion by 2035, growing at a CAGR of approximately 6.73%. The U.S. Department of Energy's USD 80 million investment announced in 2023 in intelligent building technologies including intelligent panel systems under the Inflation Reduction Act underscored the government's commitment to supporting advanced prefabricated construction methods as a component of energy-efficient building delivery.

The United States prefabricated panel market is driven by the acute shortage of skilled on-site construction labour whose progressive severity is making the labour-efficiency advantage of prefabricated panel construction economically compelling across residential, commercial, and industrial building categories. Multi-family residential construction, whose housing affordability crisis in major metropolitan areas creates political and economic motivation for cost and programme efficient construction methods, is progressively adopting prefabricated wall, floor, and facade panel systems whose factory production efficiency reduces per-unit construction cost and timeline.

Prefabricated Panels Market Segment Analysis

-

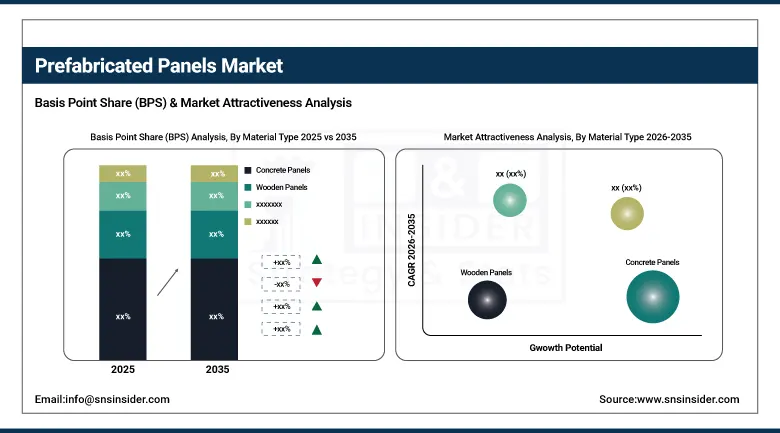

By Material Type, concrete panels segment dominated the prefabricated panels market in 2025 with 38% share; plastic & composite panels segment is the fastest growing segment.

-

By Construction Type, panelized construction segment dominated the market in 2025 with 36% share; volumetric modular construction segment is the fastest growing segment.

-

By Application, wall panels segment dominated the market in 2025 with 33% share; cladding & facade panels segment is the fastest growing segment.

-

By End-Use Industry, residential buildings segment dominated the market in 2025 with 40% share; infrastructure projects segment is the fastest growing segment.

By Material Type, concrete panels dominate the prefabricated panels market, plastic & composite panels are the fastest growing

Concrete panels dominated the Prefabricated Panels Market in 2025 because of their superior strength, durability, fire resistance, and long service life. Builders favored them for big residential, commercial, and infrastructure projects where load-bearing capacity and safety matter most. Their ability to handle rough conditions and need for little maintenance boosted their use too. Plus, well-established manufacturing processes and cost efficiency in making them in bulk supported their popularity in many construction areas.

Plastic and composite panels are the fastest growing segment because of their light weight, easy installation, and flexible designs. These materials provided great thermal and acoustic insulation, fitting perfectly in today's energy-efficient buildings. More people wanted sustainable and corrosion-resistant construction materials, which sped up the adoption of these panels. Advances in composite technology and increased use in modular and prefab structures also drove rapid growth in both residential and commercial sectors.

By Construction Type, panelized construction dominates the prefabricated panels market, volumetric modular construction is the fastest growing

Panelized construction dominated the market because of its perfect mix of speed, cost savings, and sturdy construction. This approach lets builders make parts in safe, controlled places before putting them together fast on site. This cuts down on labor costs and speeds up construction times too. It’s really popular for both homes and businesses since it allows for consistent results and easy scaling. Plus, its use of established building techniques keeps it very strong in the prefab panel world.

Volumetric modular construction is the fastest growing segment due to its high efficiency, shorter project times, and better quality control. Whole modules are built off-site and just need to be quickly assembled on-site. This major reduction in construction delays is awesome, especially with how cities are expanding and there's a big need for fast housing solutions. Also, labor shortages and more focus on green building practices are pushing developers to go modular, driving up the segment's growth.

By Application, wall panels dominate the prefabricated panels market, cladding & facade panels are the fastest growin

Wall panels dominated the market because they're vital structural and enclosure parts used in nearly every type of building. You can find them in residential, commercial, and industrial spaces since they offer strength, insulation, and design options. Plus, they're easy to put up and work well with different prefab systems, making life easier for builders. Cost-effectiveness and reliable performance in both interior and exterior settings also explain why they have such a big chunk of the market.

Cladding and facade panels are the fastest growing segment due to a rising need for stylish, energy-efficient exteriors. These panels boost a building's thermal performance, weather resilience, and overall look. Since there's more emphasis on eco-friendly building practices, this is boosting usage. Besides, new material innovations and design freedom help architects make custom facades. Because of this, these types of panels are super appealing in commercial and high-end homes.

By End-Use Industry, residential buildings dominate the prefabricated panels market, infrastructure projects are the fastest growing

Residential buildings dominated the market because of continuous urbanization, population growth, and the increasing demand for affordable housing. Plus, prefab panels are really popular in housing projects since they're cost-effective, speed up construction, and ensure better quality. With the government backing mass housing efforts, adoption just gets stronger. People also now prefer homes that are not only durable but energy-efficient too, which benefits prefab solutions in the residential market.

Infrastructure projects are the fastest growing segment due to investments in transport, smart cities, and public services. Bridges, railways, and large facilities rely more and more on prefab parts since they speed up building and ensure quality. With the government pushing infra projects and cities getting bigger, there’s a huge demand for prefab materials. Plus, everyone wants constructions that are tough and easy to maintain, which is why this area is growing so fast.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

28.5% |

|

Asia Pacific |

China |

42.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Prefabricated Panels Market Insights

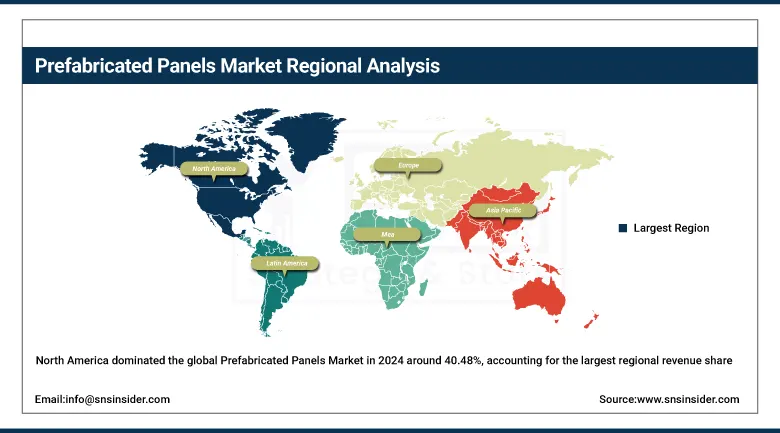

North America dominated the global Prefabricated Panels Market in 2024 around 40.48%, accounting for the largest regional revenue share. The United States accounts for approximately 82.5% of North American revenues through its combination of the world's most active hyperscale data centre construction programme creating large-scale insulated metal panel demand, the growing multi-family residential affordability housing programme's adoption of panelised construction, and the Inflation Reduction Act's clean manufacturing incentive-driven new industrial facility construction wave.

According to the United States Census Bureau, the United States issues approximately 1.4–1.6 million new housing permits every year, reflecting strong residential construction activity and supporting demand for faster, more efficient building and prefabrication methods across the housing sector.

According to the U.S. Department of Energy, buildings account for approximately 40% of total energy consumption, which is driving increased adoption of insulated prefabricated panels that improve energy efficiency and reduce overall heating and cooling demand in structures.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Prefabricated Panels Market Insights

Europe held a significant share of the global Prefabricated Panels Market in 2025. Germany, France, the United Kingdom, the Netherlands, and Scandinavia are the leading national markets whose advanced industrial construction cultures, stringent building energy performance requirements, and active social housing programmes create consistent and technically demanding prefabricated panel demand. Germany accounts for approximately 28.5% of European revenues through its large industrial building construction sector.

According to Eurostat, over 75% of buildings across the European Union are energy inefficient, significantly increasing large-scale retrofit demand and accelerating adoption of insulated prefabricated panels for improving thermal performance and reducing long-term energy consumption in existing building stock.

According to the European Commission Renovation Wave Strategy, supported by European Commission Energy, the European Union aims to double annual renovation rates by 2030, promoting deep energy retrofits and increased use of high-performance prefabricated insulated panels across residential and commercial buildings.

Asia Pacific Prefabricated Panels Market Insights

Asia Pacific is the fastest-growing regional Prefabricated Panels Market, driven by the world's largest construction markets in China and India whose urbanisation programmes, affordable housing ambitions, and rapidly expanding industrial and commercial construction sectors create enormous prefabricated panel demand. China accounts for approximately 42.8% of Asia Pacific revenues through the scale of its residential construction, industrial facility development, and government infrastructure investment whose adoption of prefabricated construction methods is progressively advancing from pilot programme to mainstream construction practice under national policy frameworks promoting building industrialisation.

According to the United Nations Economic and Social Commission for Asia and the Pacific UNESCAP, Asia is expected to add over 1 billion urban residents by 2050, driven by rapid urbanization, infrastructure expansion, and migration toward cities, significantly increasing long-term demand for residential and commercial construction.

China’s national policy targets over 30% prefabricated construction penetration in new buildings across many provinces, reflecting strong regulatory support for industrialized building methods, improved efficiency, reduced emissions, and faster delivery of large-scale infrastructure and housing projects.

MEA & Latin America Prefabricated Panels Market Insights

The UAE leads MEA revenues at approximately 38.4% of the regional total through its extraordinary construction pipeline whose NEOM, Red Sea Project, and Expo 2020 legacy development programmes require rapid building delivery at scales that conventional construction cannot achieve within the project timelines, creating large-scale prefabricated panel procurement at premium specifications. Saudi Arabia's Vision 2030 infrastructure and housing investment and Egypt's new administrative capital project create growing regional construction demand.

According to the World Bank World Bank, urban population in the Middle East exceeds 65%, accelerating infrastructure expansion and large-scale construction demand. This supports UAE-led megaproject pipelines and rapid prefabricated panel adoption across Saudi Arabia and Egypt.

Brazil leads Latin American revenues at approximately 44.2% of the regional total through its large residential construction market, the growing industrial and logistics real estate sector, and the Minha Casa Minha Vida affordable housing programme whose volume delivery requirements create adoption motivation for industrialised panel construction methods.

According to UN-Habitat UN Habitat, Latin America faces a significant urban housing deficit affecting tens of millions of people, increasing demand for faster construction methods and prefabricated solutions, with Brazil leading regional revenues and Mexico and Colombia expanding adoption.

Market Dynamics

Growth Drivers: Construction labor shortages globally are driving adoption of efficient panel construction and industrialized housing solutions.

The prefabricated panels market's growth is structurally driven by the convergence of a construction workforce shortage crisis and a housing affordability crisis that each independently create commercial motivation for industrialised building methods and whose simultaneous operation in major economies creates a compounding demand pull. The construction sector's documented workforce shortage, whose skills gap in developed economies reflects an ageing tradesperson workforce not being replaced at replacement rate by new entrants, creates labour cost inflation and programme delay risk that prefabricated panel systems mitigate by shifting 60 to 80% of construction activity from on-site labour to factory production whose controlled environment and manufacturing efficiency create more favourable labour economics.

Restraints: High initial capital investment and transportation cost constraints limit economic reach of prefabricated panel manufacturing facilities.

Prefabricated panel manufacturing facilities whose crane-serviced assembly halls, precision cutting equipment, and quality control infrastructure represent capital investments of tens to hundreds of millions of dollars create market entry barriers that limit supplier geographic distribution and create regional supply gaps in construction markets distant from established manufacturing concentrations. Panel transportation cost, whose sensitivity to distance from factory to site creates an economic radius of approximately 300 to 500 kilometres beyond which panel transportation cost erodes the labour efficiency advantage versus local in-situ construction, limits the commercial viability of prefabricated panel adoption in geographically remote construction projects whose site access and haul distance economics favour locally manufactured materials.

Opportunities: Mass timber innovation and digital fabrication integration enable customized panel production with standardized, scalable cost efficiency.

Mass timber prefabricated panel technology, encompassing cross-laminated timber, laminated veneer lumber, and nail-laminated timber structural panel systems whose carbon sequestration, renewable material content, and exposed timber aesthetic create a premium sustainable building material whose commercial adoption in mid-rise residential, commercial, and institutional construction is expanding rapidly under green building certification frameworks.

Each new building code amendment that extends permitted mass timber construction heights, as the IBC's 2021 edition did for the United States by creating tall mass timber building categories up to 18 storeys, expands the addressable market for mass timber prefabricated panel systems whose structural and sustainability advantages create competitive differentiation versus concrete and steel alternatives in the emerging premium sustainable construction market.

Recent Developments:

-

2025: Kingspan Group expanded insulated metal panel manufacturing capacity in North America through a new production facility investment targeting growing data centre, cold storage, and commercial industrial construction demand for high-performance building envelope systems.

-

2024: Nucor Corporation launched its new steel building systems division offering integrated prefabricated steel panel and structural systems for industrial and commercial construction, leveraging its domestic steel production advantage to provide integrated building envelope solutions to the growing U.S. industrial construction market.

-

2023: Godrej Construction built The Cocoon, a 500 square foot prefabricated office at its Khalapur campus in 40 hours using 3D-printing-integrated construction technology, demonstrating the commercial potential of next-generation integrated digital fabrication and prefabricated panel construction for programme-critical applications.

Key Market Players

-

Kingspan Group

-

Tata Steel Limited

-

Nucor Corporation

-

Algeco

-

Atco Ltd.

-

Metecno Group

-

EPACK Prefab

-

Lindab Group

-

Rauta

-

Ritz‑Craft Corporation

-

ArcelorMittal Construction

-

Assan Panel A.Ş.

-

BlueScope Buildings

-

DANA Group

-

Builders FirstSource

-

Fabcon Precast

-

Kingspan Timber Solutions

-

Robertson Group Ltd

-

Etex Building Performance

-

Hunter Douglas Group

Prefabricated Panels Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 64.14 Billion |

| Market Size by 2035 | USD 115.79 Billion |

| CAGR | CAGR of 6.07% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material Type- (Concrete Panels, Wooden Panels, Glass Panels, Metal Panels (e.g., steel, aluminium), Plastic & Composite Panels, Others (Gypsum panels, Fiber cement panels, and eco-friendly experimental materials)) • By Construction Type (Permanent Modular Construction (PMC), Relocatable/Temporary Buildings, Panelized Construction, Volumetric Modular Construction, Others (Hybrid construction systems, kit-of-parts systems, and custom prefab designs)) • By Application (Wall Panels, Roof Panels, Floor Panels, Ceiling Panels, Cladding & Facade Panels, Others (Partition panels and soundproof/acoustic panels)) • By End-Use Industry (Residential Buildings, Commercial Spaces, Industrial Facilities, Institutional Buildings, Infrastructure Projects, Others (Military housing, event pavilions, etc.)) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Kingspan Group, Tata Steel Limited, Nucor Corporation, Algeco, Atco Ltd., Metecno Group, EPACK Prefab, Lindab Group, Rauta, Ritz‑Craft Corporation, ArcelorMittal Construction, Assan Panel A.Ş., BlueScope Buildings, DANA Group, Builders FirstSource, Fabcon Precast, Kingspan Timber Solutions, Robertson Group Ltd, Etex Building Performance, Hunter Douglas Group |

Frequently Asked Questions

The Prefabricated Panels Market is expected to grow at a CAGR of 6.07% from 2026 to 2035.

The Prefabricated Panels Market was valued at USD 64.14 Billion in 2025.

Construction labour shortages, affordability pressures, data centre growth, green building mandates, and digital fabrication are driving prefabricated panel market expansion globally.

The Concrete segment dominated the Prefabricated Panels Market with the largest revenue share in 2025.

North America dominated the Prefabricated Panels Market in 2025.

Get in Touch