Polyetheramine Market Report Scope & Overview:

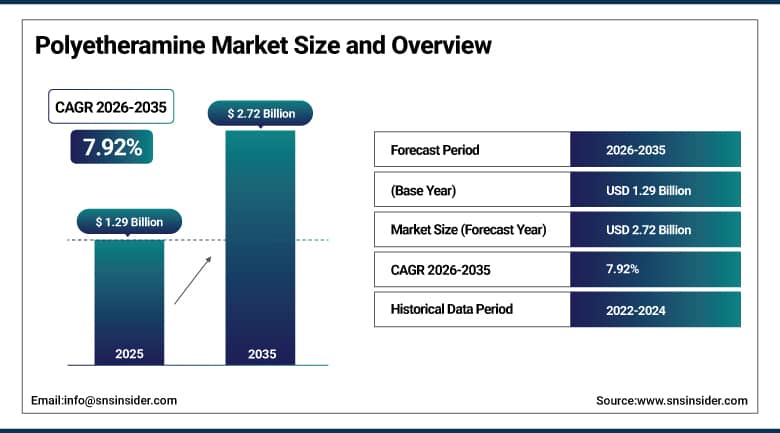

The Polyetheramine Market was valued at USD 1.29 Billion in 2025 and is expected to reach USD 2.72 Billion by 2035, growing at a CAGR of 7.92% from 2026–2035.

Polyetheramines are a class of specialty chemicals characterized by a backbone structure of polyether with terminal primary amine functional groups. The presence of the long chain segments of polyether within the cured epoxy resin matrix brings about increased flexibility, as opposed to other amine-based curing agents that lead to more brittle structures. Commercially, polyetheramines have a range of applications including as corrosion-resistant and toughened coating for construction infrastructure components; as toughened adhesives in the assembly of lightweight composite blades of wind turbines, thereby allowing rotor blades of increased sizes for greater energy capture; in automobile industry applications such as structural adhesive bonding between various materials; in aerospace applications where toughness, high tensile strength, and weight reduction properties are paramount; and in fuels as additives that confer detergency, corrosion protection, and lubricating qualities to gasoline and diesel fuels. The Huntsman Corporation product line known as JEFFAMINE pioneered the polyetheramine class commercially and is still widely specified today.

Huntsman Corporation introduced a new tri-functional polyetheramine product line under its JEFFAMINE brand in January 2025, designed for high-performance epoxy systems in aerospace and automotive composites. This product launch reflects active innovation investment by the leading global polyetheramine supplier in the fastest-growing end-user application categories for the product family.

Market Size and Forecast

-

Market Size in 2026E: USD 1.39 Billion

-

Market Size by 2035: USD 2.72 Billion

-

CAGR: 7.92% from 2026 to 2035

-

Fastest Growing Region: North America

-

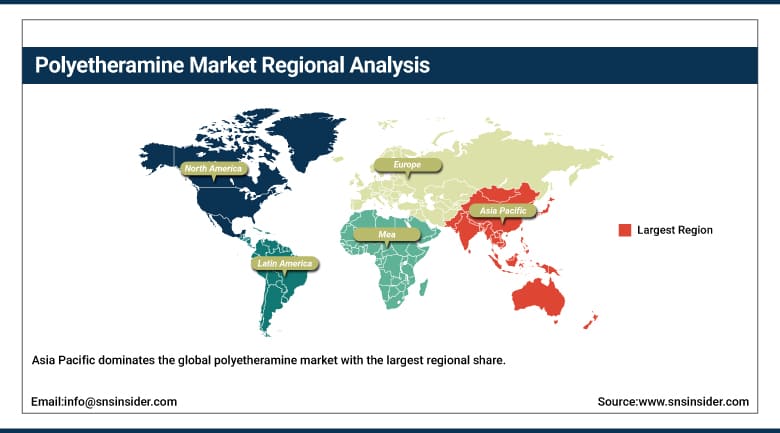

Largest Region: Asia Pacific

To Get More Information On Polyetheramine Market - Request Free Sample Report

Polyetheramine Market Trends

-

Blade manufacture for wind turbines is contributing to rising demand for polyetheramines in high-performance epoxy composites in the renewable energy sector.

-

Development of bio-derived polyetheramines is gaining traction as companies look for sustainable chemical alternatives without sacrificing performance.

-

Electric cars that are small and light in weight have increased the use of polyetheramines in composites and adhesives used in the automobile industry.

-

More and more use of low-VOC and water-based polyetheramines will help businesses abide by green building laws.

-

Polyurea coating has made use of polyetheramines for providing protective as well as waterproofing purposes to industrial structures.

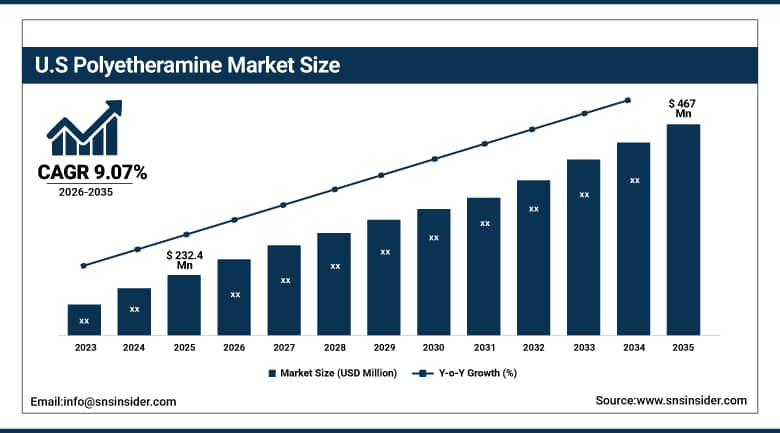

U.S. Polyetheramine Market Outlook

The U.S. Polyetheramine Market was valued at approximately USD 232.4 Million in 2025 and is expected to reach approximately USD 467 Million by 2035, growing at a CAGR of 9.07%.

The United States is the world's most commercially advanced polyetheramine market with a CAGR that exceeds the global average. The U.S. wind energy development is one of the most commercially significant polyetheramine demand drivers in North America. Offshore wind farms being developed along the Atlantic Coast, Great Lakes, and Pacific Coast use turbine blades whose composite manufacturing requires polyetheramine curing agents. Onshore wind energy additions across the Midwest, Great Plains, and Western states continue at substantial scale. Each megawatt of new wind capacity requires blade composite manufacturing with polyetheramine content, creating a direct link between U.S. energy policy and polyetheramine demand growth. The Inflation Reduction Act's extended production and investment tax credits for wind energy sustain the U.S. wind development pipeline that is one of the most commercially important drivers of U.S. polyetheramine market growth.

The U.S. Infrastructure Investment and Jobs Act's USD 1.2 trillion commitment to bridge, highway, port, and utility infrastructure rehabilitation is creating sustained demand for industrial protective coatings including polyetheramine-cured epoxy systems that provide the chemical resistance and mechanical durability required for infrastructure surface protection in corrosive and high-traffic environments.

Polyetheramine Market Segment Analysis

-

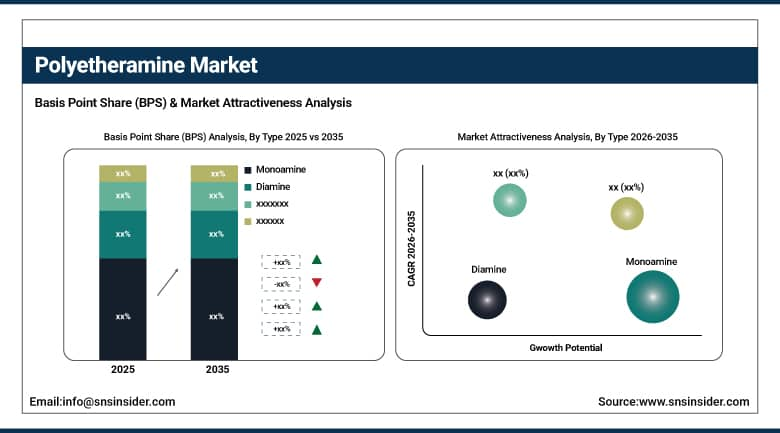

By Type, monoamine dominated the market with approximately 46% share in 2025; diamine is the fastest-growing type.

-

By Application, epoxy coatings held approximately 38% share in 2025; composites are the fastest-growing application.

-

By End User Industry, construction held the largest share in 2025; wind energy is the fastest-growing end user.

By Type, monoamine dominates, diamine grows fastest

Monoamine held approximately 46% of the polyetheramine market in 2025. Monoamines offer the simplest molecular architecture within the polyetheramine family, which translates into the most predictable reactivity, the easiest formulation integration, and the most cost-effective production. In fuel additive applications, monoamines provide the detergent, anti-corrosion, and lubricity functions that improve combustion efficiency, prevent injector deposits, and protect fuel system metal components. Their solubility in hydrocarbon fuel and their compatibility with other additive package components makes them the preferred polyetheramine type for this large-volume application.

Diamine is the fastest-growing polyetheramine type. With two reactive amine groups per molecule, diamines create higher crosslink density in cured epoxy matrices than monoamines, providing the mechanical strength, chemical resistance, and thermal stability that aerospace, wind blade, and automotive structural composite applications demand. The expansion of glass-fiber and carbon-fiber reinforced epoxy composite manufacturing for wind turbine blades is the most commercially significant growth driver for polyetheramine diamine demand. Blade manufacturers producing rotors exceeding 80 meters in length use diamine-cured epoxy systems as the matrix resin whose performance determines the structural reliability and operational lifetime of the entire blade assembly.

By Application, epoxy coatings dominate, composites grow fastest

Epoxy coatings held approximately 38% of the polyetheramine market in 2025. The commercial dominance of this application reflects the extraordinary scale of global infrastructure, industrial facility, marine vessel, and commercial building surface protection where polyetheramine-cured epoxy systems provide technically validated performance. The U.S. EPA and EU REACH regulations progressively restricting solvent content in commercial coatings are creating reformulation demand for waterborne and high-solids epoxy systems where polyetheramines provide the low-viscosity curing agent performance that enables VOC-compliant formulation at commercially acceptable application properties.

Composites are the fastest-growing application for polyetheramines. Wind turbine blade composite manufacturing is the most commercially significant driver, but aerospace structural composites and automotive body panel, floor system, and battery enclosure composite applications are also growing at above-average rates. The trend toward larger turbine rotor diameters to capture stronger winds at greater heights means that each successive turbine generation uses longer blades with higher polyetheramine content per unit than its predecessor, creating compound demand growth that exceeds the simple linear growth in turbine installation numbers.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

81.4% |

|

Europe |

Germany |

28.7% |

|

Asia Pacific |

China |

52.3% |

|

Middle East & Africa |

Saudi Arabia |

34.6% |

|

Latin America |

Brazil |

43.7% |

Asia Pacific Polyetheramine Market Insights

Asia Pacific dominates the global polyetheramine market with the largest regional share driven by China's extraordinary construction activity and epoxy coating consumption, India's growing industrial and infrastructure coating investment, South Korea's and Japan's advanced automotive and electronics manufacturing sectors, and the region's rapidly expanding wind energy development programmes. China accounts for approximately 52.3% of Asia Pacific revenues as the world's largest polyetheramine consuming nation by volume through its dominant construction, industrial coating, and wind energy manufacturing sectors. China's domestic polyetheramine production capacity has grown substantially, with companies including Wuxi Acryl Technology, Yangzhou Chenhua, and Yantai Minsheng operating at commercial scale alongside the global operations of Huntsman and BASF.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Polyetheramine Market Insights

North America is the fastest-growing regional polyetheramine market at a CAGR of 9.07%, driven by infrastructure investment, wind energy expansion, advanced aerospace and automotive composite manufacturing, and stringent VOC regulations driving low-emission coating formulation development. The United States accounts for approximately 81.4% of North American revenues as the home of Huntsman Corporation's global JEFFAMINE operations, the world's most active wind energy development programme, and the most technically demanding commercial polyetheramine applications in aerospace and advanced automotive manufacturing. The Infrastructure Investment and Jobs Act's multi-year commitment to bridge, highway, and utility infrastructure rehabilitation creates sustained demand for polyetheramine-cured protective coatings.

Canada is a growing polyetheramine market through its wind energy development programme, oil sands surface facility protective coating requirements, and the marine coating demand from its active shipbuilding and port infrastructure sectors. Canadian infrastructure investment in bridge and road rehabilitation alongside growing industrial facility protective coating demand sustains consistent polyetheramine consumption through construction and maintenance coating applications across the country's vast geography.

Europe Polyetheramine Market Insights

Europe is a large and sustainability-driven polyetheramine market where EU Green Deal initiatives, REACH chemical regulations, and growing renewable energy infrastructure investment are collectively shaping demand. Germany accounts for approximately 28.7% of European revenues through its position as the EU's largest wind energy market, its concentration of automotive composite manufacturing for BMW, Mercedes-Benz, Volkswagen, and Audi, and its chemical industry leadership through BASF and Evonik who are active polyetheramine producers and application developers. EU regulations restricting VOC content in industrial and decorative coatings are creating reformulation demand for low-VOC polyetheramine-compatible epoxy coating systems.

Offshore wind development in the North Sea and Celtic Sea is creating demand for polyetheramine-cured glass and carbon fiber composite turbine blades at scales that are driving capacity investment among European composite manufacturers. The EU taxonomy for sustainable activities and EU Green Deal investment frameworks is supporting renewable energy infrastructure investment that maintains European wind energy development momentum as a sustained driver of polyetheramine composite demand.

MEA & Latin America Polyetheramine Market Insights

The Middle East and Africa and Latin America are growing polyetheramine markets where oil and gas infrastructure coating, construction activity, and wind energy development are creating demand. Saudi Arabia leads MEA revenues at approximately 34.6% of the regional share through its extensive oil and gas infrastructure requiring high-performance anti-corrosion coating systems and its construction activity under Vision 2030 that uses polyetheramine-cured epoxy concrete protection systems. Brazil leads Latin American revenues at approximately 43.7% through its active wind energy development programme whose blade composite manufacturing is one of the fastest-growing polyetheramine applications in the region alongside infrastructure coating demand from Brazil's extensive port, bridge, and industrial facility maintenance programmes.

Market Dynamics

Growth Drivers: Wind energy composite demand from renewable capacity expansion and global infrastructure protective coating investment driving the polyetheramine market growth.

Wind energy infrastructure expansion is the most commercially dynamic driver of polyetheramine demand growth. Global wind energy capacity additions reached record levels in the past years as climate policy commitments, renewable energy economics, and energy security concerns collectively accelerated wind development in Europe, China, North America, and emerging markets. Each megawatt of new wind capacity requires composite blade manufacturing whose epoxy matrix systems use polyetheramine diamine curing agents. The trend toward larger turbines with longer blades means that per-turbine polyetheramine content is growing even as the manufacturing engineering of individual blade production becomes more sophisticated. Offshore wind development is particularly significant as offshore turbines are substantially larger than onshore units, using proportionally more composite materials per megawatt of installed capacity.

Global infrastructure protective coating investment is a large and growing polyetheramine end market. Bridge, pipeline, port, and industrial facility anti-corrosion coating systems represent one of the largest single application areas for polyetheramine-cured epoxy coatings globally. The ageing of infrastructure in North America and Europe, where much of the bridge, highway, and utility infrastructure was built in the mid-20th century, creates structural rehabilitation demand that generates protective coating procurement across public agency budgets. The Infrastructure Investment and Jobs Act in the U.S. and equivalent European and Asian infrastructure investment programmes create multi-year demand visibility for polyetheramine-cured protective coating systems.

Restraints: High raw material cost volatility from propylene oxide and ammonia feedstocks and market concentration among a small number of global polyetheramine producers are restraining the market growth.

Raw material cost volatility is the most commercially significant constraint on polyetheramine manufacturer margins and formulator product economics. Propylene oxide, the primary polyether backbone feedstock for most commercial polyetheramines, is derived from petroleum and subject to the price fluctuations of crude oil and refinery economics. Ammonia, required for the amination reaction that introduces amino groups into the polyether backbone, is influenced by natural gas prices through its production from steam methane reforming. When oil and gas prices spike, polyetheramine production costs rise substantially, creating margin pressure for producers and price increases for formulators that can reduce volume demand in price-sensitive application segments.

Market concentration among a small number of global polyetheramine producers creates supply chain risk for formulators dependent on secure, consistent supply of specific polyetheramine grades. Huntsman Corporation's JEFFAMINE line is specified in many formulations by name rather than specification, creating commercial dependency on a single supplier that creates risk if supply disruption occurs. Asian producers including Chinese manufacturers have expanded capacity and diversified the supply base for commodity grades, but for premium performance grades in demanding aerospace, wind energy, and advanced composite applications, formulation specifications often remain tied to specific established brands.

Opportunities: Renewable energy composite demand from offshore wind and solar tracking structures and polyurea infrastructure protection coating expansion represent the market growth opportunities.

Offshore wind energy development represents one of the largest near-term growth opportunities for the polyetheramine composite materials market. Offshore wind turbines use blades that are substantially longer than onshore equivalents and operate in salt spray environments that impose more demanding structural and corrosion resistance requirements. The scale of planned offshore wind development in the UK, Germany, Denmark, the Netherlands, U.S. Atlantic Coast, and Asian waters represent a large and commercially concentrated demand opportunity for the composite blade manufacturing industry whose epoxy matrix systems require polyetheramine curing agents. Each offshore turbine represents more blade composite material per unit than onshore equivalents, creating above-average polyetheramine content per turbine installed.

Bio-based polyetheramine development represents a commercially significant opportunity for producers who can achieve bio-based certification without compromising the performance characteristics that technically demanding applications require. Chemical companies including BASF and Evonik are investing in bio-based amine chemistry that could provide polyetheramine with partial or full bio-based content certification. Bio-based polyetheramines would support the green procurement requirements of construction companies, automotive manufacturers, and wind energy developers who are increasingly requiring sustainable material sourcing certification from their chemical suppliers as part of their own Scope 3 emission reduction programmes.

Recent Developments:

-

2025: Huntsman Corporation introduced a new tri-functional polyetheramine product line under its JEFFAMINE brand designed for high-performance epoxy systems in aerospace and automotive composites, targeting the fastest-growing segments of the polyetheramine application market.

-

2025: BASF SE expanded its polyetheramine product range for low-VOC waterborne epoxy coating formulations targeting the European and North American industrial and infrastructure coating markets where regulatory restrictions on solvent-based systems are accelerating demand for water-compatible curing agents.

-

2025: Evonik Industries advanced its VESTAMIN polyetheramine product line with new grades optimized for offshore wind blade composite manufacturing, addressing the technical specification requirements of offshore turbine blade producers for enhanced fatigue resistance and salt environment durability.

-

2025: Wuxi Acryl Technology expanded its polyetheramine production capacity in China, positioning to serve growing domestic construction coating and wind energy composite manufacturing demand as well as export markets in Southeast Asia and the Middle East.

Polyetheramine Market Key Players:

-

Huntsman Corporation

-

BASF SE

-

Evonik Industries AG

-

Clariant AG

-

Covestro AG

-

Stepan Company

-

Perstorp Holding AB

-

Wuxi Acryl Technology Co. Ltd.

-

Yangzhou Chenhua New Materials Co. Ltd.

-

Yantai Minsheng Chemicals Co. Ltd.

-

IRO Group Inc.

-

The Aurora Chemical Co. Ltd.

-

Yantai Dasteck Chemicals Co. Ltd.

-

Zibo Dexin Lianbang Chemical Industry Co. Ltd.

-

Solvay SA

-

Nanjing Sainuo Chemical Co. Ltd.

-

Qingdao IRO Surfactant Co. Ltd.

-

DuPont de Nemours Inc.

-

Ercros SA

-

Dow Chemical Company

Polyetheramine Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.29 Billion |

| Market Size by 2035 | USD 2.72 Billion |

| CAGR | CAGR of 7.92% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Monoamine, Diamine, Triamine) • By Application (Epoxy Coatings, Polyurea, Adhesives & Sealants, Composites, Fuel Additives, Others) • By End User Industry (Construction, Automotive, Wind Energy, Aerospace, Oilfield, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Huntsman Corporation, BASF SE, Evonik Industries AG, Clariant AG, Covestro AG, Stepan Company, Perstorp Holding AB, Wuxi Acryl Technology Co. Ltd., Yangzhou Chenhua New Materials Co. Ltd., Yantai Minsheng Chemicals Co. Ltd., IRO Group Inc., The Aurora Chemical Co. Ltd., Yantai Dasteck Chemicals Co. Ltd., Zibo Dexin Lianbang Chemical Industry Co. Ltd., Solvay SA, Nanjing Sainuo Chemical Co. Ltd., Qingdao IRO Surfactant Co. Ltd., DuPont de Nemours Inc., Ercros SA, Dow Chemical Company |

Frequently Asked Questions

Asia Pacific dominated the polyetheramine market in 2025.

Monoamine dominated with approximately 46% of revenues in 2025.

Wind energy composite demand from renewable capacity expansion and global infrastructure protective coating investment are the primary drivers.

The polyetheramine market was valued at USD 1.29 Billion in 2025.

The polyetheramine market is expected to grow at a CAGR of 7.92% from 2026 to 2035.

Get in Touch