Prenatal Care Market Report Scope & Overview:

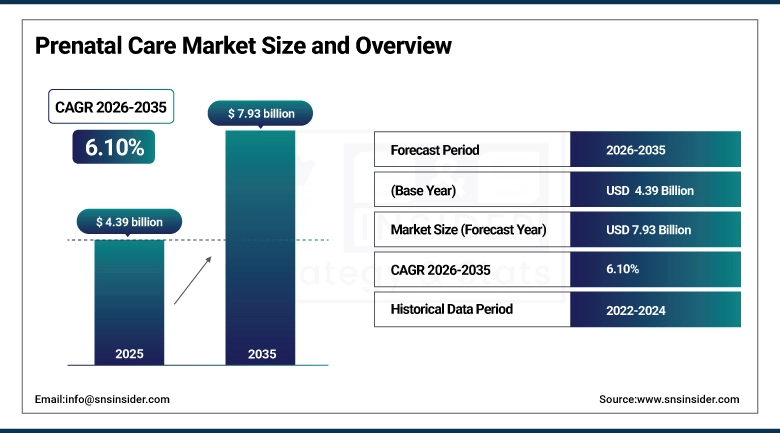

The Prenatal Care Market size was valued at USD 4.39 Billion in 2025 and is projected to reach USD 7.93 Billion by 2035, growing at a CAGR of 6.10% during 2026–2035.

Increasing awareness pertaining to maternal and fetal health, and high-risk pregnancies along with the growing accessibility towards the healthcare facilities are some factors that are propelling the growth of the prenatal care market. Market growth is also boosted by government initiatives and programs that encourage regular prenatal checkups. New diagnostic technologies such as ultrasound and genetic screening allow for the early detection of complications. In addition, increase in healthcare expenditure, increase in population in urban areas and an increase in preventive care market emphasizing on patients results in sustained market growth during the predicted time period in these developing regions.

Prenatal Care Market Size and Forecast:

- Market Size in 2025: USD 4.39 Billion

- Market Size by 2035: USD 7.93 Billion

- CAGR: 6.10% during 2026–2035

- Base Year: 2025

- Forecast Period: 2026–2035

- Historical Data: 2022–2024

To Get more information on Prenatal Care Market - Request Free Sample Report

Prenatal Care Market Key Trends:

- Rising awareness about maternal health and early diagnosis is encouraging expectant mothers to opt for regular prenatal monitoring and preventive care services.

- The integration of advanced technologies such as telehealth, AI-based diagnostics, and remote monitoring is transforming how prenatal care is delivered and accessed.

- Increasing demand for personalized and at-home prenatal care services is driving the growth of home-based testing kits and virtual consultations.

- Government initiatives and insurance coverage expansion for maternal healthcare are improving accessibility and affordability of prenatal services.

- Growing adoption of non-invasive prenatal testing (NIPT) and advanced screening methods is enhancing early detection of genetic abnormalities.

- The shift toward holistic prenatal care, including nutrition counseling, mental health support, and wellness programs, is reshaping patient-centered care approaches.

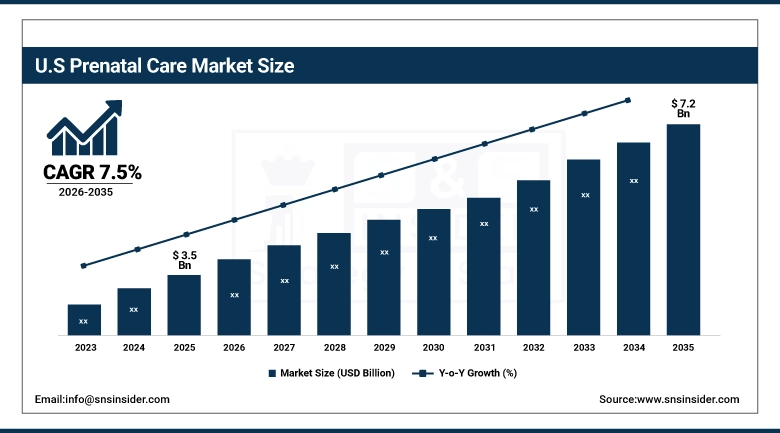

The U.S. Prenatal Care Market size was valued at USD 3.5 Billion in 2025 and is projected to reach USD 7.2 Billion by 2035, growing at a CAGR of 7.5% during 2025–2035. Growth in the U.S. prenatal care market is driven by rising maternal age, increasing high-risk pregnancies, strong healthcare infrastructure, and widespread insurance coverage. Technological advancements, including telehealth and genetic screening, along with growing awareness of early prenatal care, further support market expansion.

Prenatal Care Market Key Drivers:

- Increasing awareness of maternal health, rising high-risk pregnancies, and advancements in prenatal diagnostics are driving market demand.

The rise in maternal health awareness and early diagnosis will contribute immensely to the growth of the Prenatal Care Market. With the complications related to lifestyle becoming common along with rising maternal age, there is an increase in high-risk pregnancies contributing to the demand for its regular monitoring. The continuous evolution of prenatal diagnostics such as ultrasound and genetic basis, the existing healthcare infrastructure, the birth of initiatives by the government, are contributing towards the optimal healthcare and continuous growth in the market.

Prenatal Care Market Key Restraints:

- Increasing awareness of maternal health, rising high-risk pregnancies, and advancements in prenatal diagnostics are driving market demand.

The high cost of healthcare and inequality in access to prenatal services a restraint for the Prenatal Care Market. This makes affordable options a huge issue in low- and middle-income territories where few specialists will actually be stationed. Cultural factors and ignorance of the importance of early prenatal visits may delay the care. Various factors such as differences in healthcare infrastructure have contributed to inconsistent widespread market growth and have prevented both from reaching their full market potential.

Prenatal Care Market Key Opportunities:

- Technological advancements, telehealth expansion, and growing demand for personalized prenatal care are creating new growth opportunities.

Telehealth, AI-based monitoring, and personalized prenatal care solutions are all on the rise the type of trends that can lead to meaningful market growth. Access and convenience are increasing, especially in remote areas, where digital health platforms and at-home testing kits are providing much-needed solutions. The combination of initiatives to shift towards preventive care, new integrations with mental health, and insurance expansion are facilitating service uptake, empowering providers to expand new segments to drive improved outcomes with new sources of revenue.

Prenatal Care Market Segments:

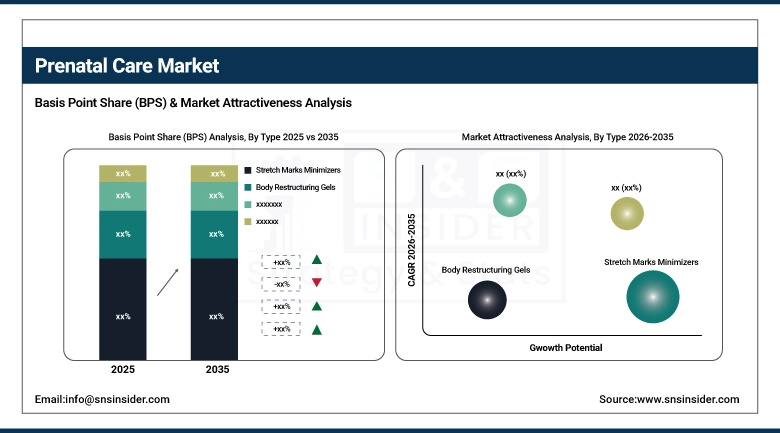

- By Type: In 2025, Stretch Marks Minimizers dominated with 36% share; Body Restructuring Gels fastest growing segment during 2026–2035

- By Equipment: In 2025, Ultrasound and Ultrasonography Devices dominated with 41% share; Fatal Monitors fastest growing segment during 2026–2035

- By Supplements: In 2025, Vitamins dominated with 39% share; Essential Fatty Acids fastest growing segment during 2026–2035

- By Distribution Channel: In 2025, Hospital Pharmacies dominated with 46% share; Online Pharmacies fastest growing segment during 2026–2035

Prenatal Care Market Segments Analysis:

By Type, Stretch Marks Minimizers Dominate While Body Restructuring Gels Expand Rapidly:

The Stretch Marks Minimizers segment was the largest compared to other categories in the market as it is the most common concern related to during pregnancy, this will continue to drive the demand of preventive and corrective skin care product markets. Adoption is further supported by increased awareness and availability of dermatologically tested formulations. Reaching for 2025, this type represented a sizable section of total product usage.

The Body Restructuring Gels are expected to be the fastest growing segment as an increase in the requirement for post pregnancy body care and recovery is also for concrete body restructuring gels. The growing interest in aesthetic wellness is fueling a concerted push from consumers toward products that can enhance skin with better elasticity and firmness. Restructuring gels experienced an uptick in demand, particularly in urban markets in 2025.

By Equipment, Ultrasound and Ultrasonography Devices Dominate While Fetal Monitors Expand Rapidly:

Ultrasound and Ultrasonography Devices is the most prominent type of product segment owing to its key role in routine prenatal screening and monitoring fetal development. Due to their availability and non-invasiveness, they are a routine modality in prenatal care. These devices made up the biggest portion of diagnoses performed in 2025.

Fetal Monitors held the largest market share and is projected to register the highest CAGR owing to increase adoption of continuous fetal health monitoring, particularly in high-risk pregnancies. With technological growth and convergence with digital health platforms, they are gaining even more traction. Fetal monitoring solution delivery grew considerably within both hospitals and clinics during 2025.

By Supplements, Vitamins Dominate While Essential Fatty Acids Expand Rapidly:

The largest share of the market came from the vitamins segment because prenatal vitamins such as folic acid and iron are frequently advised taking during pregnancy in order to contribute to fetal development and maternal health. Behind it, strong clinical support and regular prescription practices create stable demand. Prenatal supplements were predominately consumed in the form of vitamin supplements in 2025.

Essential fatty acids segment, which is the fastest growing segment due to increasing awareness related to importance of essential fatty acids in fetal brain and eye development. Demand is also being driven by the growing recommendations from healthcare professionals and growing awareness about the importance of prebiotics. This segment experienced swift expansion until 2025 around developed, as well as growing economies.

By Distribution Channel, Hospital Pharmacies Dominate While Online Pharmacies Expand Rapidly:

By type, the market is divided into Retail Pharmacies, Hospital Pharmacies and Online Pharmacies: Hospital Pharmacies remained prominent in the market as they are the foremost source for prescribed prenatal supplements, medications, and diagnostics. It has a good market position as healthcare professionals trust this brand and all the products are readily available on the shelf. The hospital-based distribution held the largest revenue share in 2025.

The fastest growing segment is Online Pharmacies, due to the increase in digital adoption, convenience, and availability of various prenatal products. Several factors, including home delivery services, competitive pricing, and rising trust in e-commerce applications, are increasing the rate of growth. This significant growth occurred in 2025, when online sales of prenatal care products expanded.

Prenatal Care Market Regional Analysis:

North America Prenatal Care Market Insights:

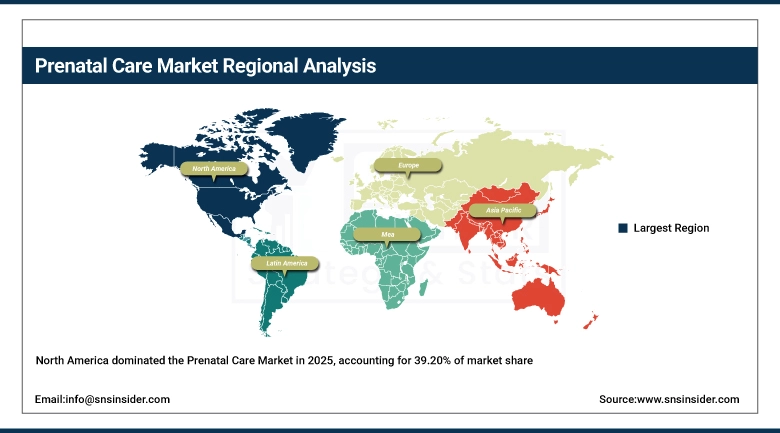

In 2025, North America accounted for the largest Prenatal Care Market share of 39.20%, which is attributed to an established healthcare framework along with significant knowledge of maternal health and adequate insurance coverage. The rise in demand can be attributed to the presence of leading healthcare providers in the region and due to high prevalence of advanced prenatal diagnostics, alongside high maternal age. The regional strengths are even more reinforced by technological integration like telehealth and AI-based monitoring.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia-Pacific Prenatal Care Market Insights:

Between 2026 and 2035, the fastest growth of the prenatal care market would be recorded in the Asia-Pacific region, with a 7.80% CAGR. ACG will continue propelled by higher births, higher healthcare spending, and a greater awareness of prenatal health across nations like China, India, and Japan. The regional market growth is being fueled by widening healthcare infrastructure, favorable government policies, and increasing adoption of digital health solutions.

Europe Prenatal Care Market Insights:

Europe Prenatal Care Market (it covers the Countries as UK, Germany, France, Italy, Norway) is benefitted by the availability of well structured healthcare systems, robust regulatory frameworks and increasing interest in maternal health. Some nations, like Germany, the U.K., and France, are at the vanguard of adopting state-of-the-art prenatal screening tech. The increasing focus on preventive care and the government-assisted healthcare programs aid in stable market growth regionally.

Latin America Prenatal Care Market Insights:

The Latin America Prenatal Care Market is likely to increase due to advances in healthcare infrastructure, rising maternal health awareness and growing government initiatives. Expecting parents in countries including Brazil and Mexico are getting more prenatal services. Increasing private health care institutions and growing availability of diagnostics space have also been beneficial for market growth.

Middle East & Africa (MEA) Prenatal Care Market Insights:

With improving access for maternal care services, increasing birth rate, and healthcare investments, the prenatal care market is also growing in the Middle East, and Africa region. The growth of the prenatal vitamins market can be mainly attributed to the healthcare reforms led by the governments, continuous expansion of hospitals infrastructure, and increasing awareness of prenatal health. Regional development is being led by key markets like the UAE, Saudi Arabia and South Africa.

Prenatal Care Market Competitive Landscape:

Clarion Medical Technologies, Canadian manufacturer of advanced medical technologies and healthcare solutions focusing on diagnostic imaging, surgical systems, and aesthetic medicine devices. Through the distribution of high-quality ultrasound systems and imaging solutions, the company promotes adequate prenatal care, allowing for correct monitoring and diagnosis of the baby as early as possible. Along with the robust partnerships with manufacturers across the globe, customer-focused service, and focus on innovation, it helps in expanding the motherhood healthcare markets footprint.

- In recent developments, Clarion Medical Technologies has focused on expanding its diagnostic imaging portfolio and strengthening partnerships with leading equipment manufacturers to enhance access to advanced prenatal imaging solutions across healthcare facilities.

Siemens Healthineers, headquartered in Erlangen, Germany, is a global leader in medical technology, offering a wide range of solutions including diagnostic imaging, laboratory diagnostics, and digital health services. In prenatal care, Siemens Healthineers provides advanced ultrasound systems and fetal imaging technologies that support early and accurate detection of pregnancy-related conditions. Its strong R&D capabilities, global presence, and integration of AI-driven diagnostics position it as a key player in the prenatal care ecosystem.

- In June 2025, Siemens Healthineers introduced enhanced AI-powered ultrasound solutions aimed at improving prenatal diagnostics, enabling faster image processing, higher accuracy, and improved workflow efficiency for healthcare professionals.

Prenatal Care Market Key Players:

-

Clarion Medical Technologies

-

Siemens Healthineers

-

Vyaire Medical

-

Laboratoires Expanscience

-

GE Healthcare

-

Getinge AB

-

Medtronic plc

-

Natus Medical Incorporated

-

Atom Medical Corporation

-

Philips Healthcare

-

Fujifilm Healthcare

-

Canon Medical Systems Corporation

-

Samsung Medison

-

Hologic Inc.

-

Mindray Medical International Limited

-

Koninklijke Philips N.V.

-

CooperSurgical Inc.

-

PerkinElmer Inc.

-

Abbott Laboratories

-

Hoffmann-La Roche Ltd

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.39 Billion |

| Market Size by 2035 | USD 7.93 Billion |

| CAGR | CAGR of 10.89% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Type (Body Restructuring Gels, Stressed Legs Products, Stretch Marks Minimizers, Dark Spots Treatment Creams, Skin Toning Lotions) •By Equipment (Ultrasound and Ultrasonography Devices, Fetal Dopplers, Fetal Monitors, Fetal Magnetic Resonance Imaging) •By Supplements (Minerals, Vitamins, Essential Fatty Acids, Others) •By Distribution Channel (Hospital Pharmacies, Online Pharmacies, Supermarkets, Drug Stores) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Clarion Medical Technologies, Siemens Healthineers, Vyaire Medical, Laboratoires Expanscience, GE Healthcare, Getinge AB, Medtronic plc, Natus Medical Incorporated, Atom Medical Corporation, Philips Healthcare, Fujifilm Healthcare, Canon Medical Systems Corporation, Samsung Medison, Hologic Inc., Mindray Medical International Limited, Koninklijke Philips N.V., CooperSurgical Inc., PerkinElmer Inc., Abbott Laboratories, F. Hoffmann-La Roche Ltd |

Frequently Asked Questions

The Prenatal Care Market is expected to grow at a CAGR of 6.10% during 2026–2035.

The Prenatal Care Market size was valued at USD 4.39 Billion in 2025 and is projected to reach USD 7.93 Billion by 2035.

The key drivers of the Prenatal Care Market include increasing awareness of maternal and fetal health, rising prevalence of high-risk pregnancies, growing healthcare expenditure, government initiatives promoting prenatal check-ups, and advancements in diagnostic technologies such as ultrasound and genetic screening.

The Ultrasound and Ultrasonography Devices segment dominated the Prenatal Care Market during the projected period.

North America dominated the Prenatal Care Market in 2025.

Get in Touch