Price Comparison Websites (PCWs) Market Report Scope & Overview:

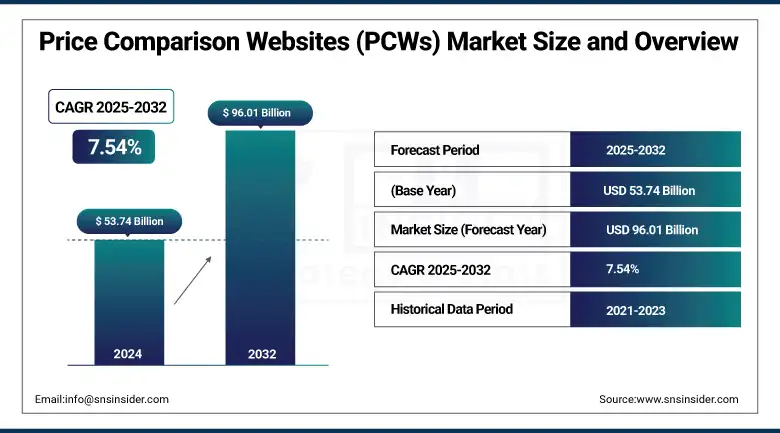

The Price Comparison Websites (PCWs) Market size was valued at USD 53.74 billion in 2024 and is expected to reach USD 96.01 billion by 2032, expanding at a CAGR of 7.54% over the forecast period of 2025-2032.

The Price Comparison Websites (PCWs) market has been expanding rapidly as more and more consumers seek to use digital aids to make well-informed purchase decisions. These applications provide price, feature, and review comparisons across the various store options, adding some measure of transparency and convenience to the shopping process. Commission, subscription, and hybrid are the key revenue models. Key service categories include general merchandise, travel, electronics, and financial services. Consumers are the overwhelming users, with increasing take-up among students and businesses. Retailer websites, user reviews, and AI-processed data all serve as the underpinning of these platforms. With the US at the front, APAC is analogously placed, and North America has a similar prospect of growth. PWcs are so important in the emergent e-commerce facility.

According to research, AI-powered PCWs enhance product match accuracy by 28%, while machine learning-driven personalization boosts repeat visits by 25%. Additionally, chatbot integration improves conversion rates by 12–15% for complex service comparisons, collectively driving stronger user engagement and platform efficiency.

To Get more information On Price Comparison Websites (PCWs) Market - Request Free Sample Report

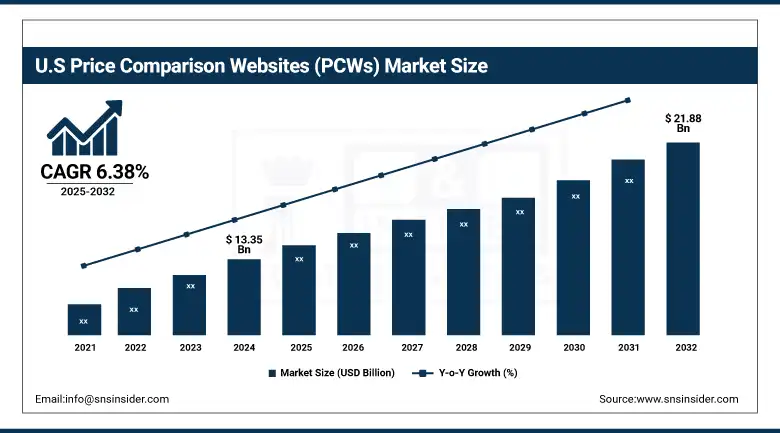

The U.S Price Comparison Websites (PCWs) market size reached USD 13.35 billion in 2024 and is expected to reach USD 21.88 billion in 2032 at a CAGR of 6.38% from 2025 to 2032.

The U.S. dominates the global Price Comparison Websites (PCWs) market due to its advanced digital infrastructure, widespread internet and smartphone usage, and a highly mature e-commerce ecosystem. Consumers in the U.S. are accustomed to leveraging PCWs for making value-driven decisions, particularly in sectors like electronics, travel, and insurance. Market penetration is distributed from key retailers like Google Shopping and Amazon. Major growth drivers are surging need for transparent pricing, AI-driven personalization, and growing online retail activities. These factors and tech-savvy consumers with a high level of digital integration further establish the United States of America as the dominant force of the global PCWs market.

Market Dynamics

Drives:

-

Rising Adoption of AI and Personalized Recommendations Enhances Consumer Engagement and Conversion Rates.

One of the lead factors behind the Price Comparison Websites (PCWs) market growth is the rapid adoption of artificial intelligence (AI) and machine learning in price comparison platforms. These features allow for highly personalized experiences that suggest products, dynamically track prices and tailor content to individual users. It is a big part of the reason customers feel happy and engaged, and those feelings often mean more conversions. And now the most recent innovations include AI-driven chatbots for instant service, predictive pricing algorithms, and super-personalized shopping experiences that are tailored to what are we have been looking at and how we have been behaving.. Major players are pouring money into data analysis to improve algorithms that allow faster, more precise comparisons. It’s not just that these advances are facilitating ease of use but they are driving competitive distinction.

Restraints:

-

Data Privacy and Regulatory Concerns Impede Platform Scalability and User Trust Across Regions.

Increasing data privacy and compliance laws act as a significant inhibitor for these platforms to scale. As personalization and performance are dependent on user data, managing compliance with regulations such as the GDPR, CCPA and other regional data protection laws has become cumbersome and cost-intensive. Consumers are also becoming more concerned with the misuse of data and are becoming less inclined to exchange any personal details. It’s becoming difficult for businesses to remain transparent in data-gathering amidst multiple jurisdictions.” In addition, recent focus on big tech platforms’ privacy breaches have ensured that the demand for strict data governance increases, stalling the quick growth of data-driven innovations.

Opportunities:

-

Expansion into Niche Markets and Localized Platforms Opens New Avenues for Growth and Monetization.

A significant opportunity lies in targeting niche markets and developing region-specific platforms tailored to local preferences and languages. As consumer demand diversifies beyond mainstream retail categories, price comparison tools can tap into segments like sustainable products, healthcare, education services, and regional goods. Recent developments also indicate an increasing number of hyperlocal PCWs that provide comparisons in local currency and vendor networks. This contextual approach not only increases user adoption in emerging markets, but also generates new revenue streams through local partnerships with merchants and fee-based access to premium features.

Challenges:

-

Maintaining Real-Time Accuracy Across Thousands of Retailers Presents a Major Operational and Technical Hurdle.

One of the biggest challenges when it comes to price comparison platforms is that of maintaining the real-time accuracy of the information across a large & ever-changing universe of retailers and products. Keeping price, inventory, and features up-to-date requires integrated flows with a variety of data sources and sophisticated, high-performance infrastructure. The smallest delay, the slightest mistake, and all the user's trust is gone, and so is the brand's credibility! The Bottom Line The needs of all those APIs have driven us to integrate with many web scraping tools as well as multiple payment gateways, discount rules, etc. The technical complexity and expense of this approach make scalability and dependability significant barriers.

Segment Analysis

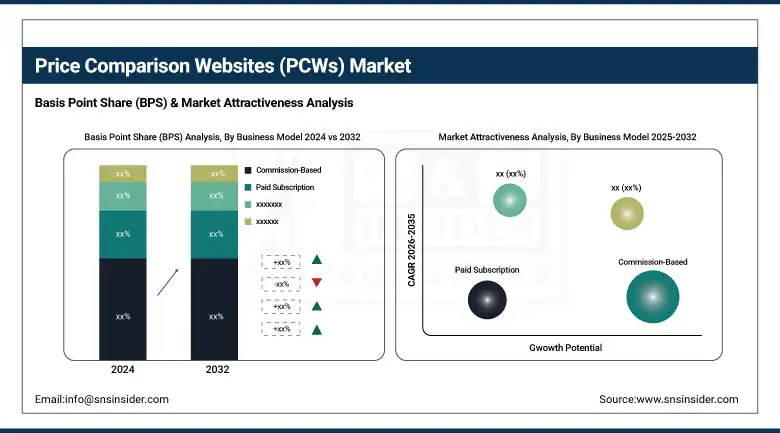

By Business Model

The Commission-Based segment holds the highest revenue share at 41.25% in 2024 because of its performance fee-based model, where the platform gets a cut when users make a transaction via referral links. This appeals to merchants and advertisers because it translates into something quantifiable. Price Comparison Websites (PCWs) market companies such as Priceline and Expedia have extended this business model with better partner integration and revenue-cascading commission models. One major catalyst is the growing need for transparent pricing and up-to-the-minute deal alerts. Enhancements like affiliate API optimization and increased product categories are improving platform functionality to underscore the increasing importance of this model in today’s e-commerce world.

The Hybrid model is growing rapidly at a CAGR of 8.60%. This flexibility allows platforms to monetize through multiple streams, appealing to both budget-conscious users and premium service seekers. Hybrid-model platforms, such as Shopzilla and Google Shopping, have even started to emerge, opening honest subscription access options, while taking their dues in commissions. The main motivation is the increasing demand for multiple sources of monetization due to fierce competition and high user requirements. New products have appeared, such as the tiered membership plan with value-added services and the performance-based merchant’s integration, so that hybrid models are now found to be easier and more efficient in the PCWs ecosystem

By Service Scope

General Merchandise accounts for the largest revenue share at 40.17% in 2024, driven by high consumer demand for everyday items, from clothing to home goods. Price comparison sites like Amazon and Yahoo Shopping have capitalized on this with broad inventories and dynamic pricing tools. The main driver is the increased online shopping frequency and consumer preference for real-time deal hunting across various product categories. Product developments include personalized catalogs and predictive pricing alerts. With large SKUs and competitive pricing, general merchandise continues to attract repeat visitors, reinforcing its dominance within the PCWs landscape.

The Travel and Hospitality segment is experiencing the highest growth rate at a CAGR of 8.75%, a rebound in international travel, and a growing appetite for transparent travel pricing.’ KAYAK, Expedia, or Booking Holdings are other platforms that have also optimised their services by incorporating hotel reviews, flight insights, or AI-generated recommendations. The desire to compare fares in real time and to compare fares with bundled travel is major trigger. Recent features such as mobile-first design, virtual trip planner, and loyalty integration with air and hotel, continue to make travel price comparison easier and more intuitive for the user.

By Target Audience

Consumers remain the dominant segment in the PCWs market, accounting for 70.12% of the total revenue in 2024. The increasing reliance on digital tools for informed purchasing decisions across retail, electronics, and travel is a key driver. Services like Google Shopping and Bing Shopping are always driving a better-experience mentality with AI-driven recommendations. Recent releases that increase user engagement include custom dashboards and real-time deal notifications. This segment is the spine of PCW platform income, because the post-pandemic future of more price-conscious consumers requires comparison tools for well-informed choices.

The student segment is growing at a CAGR of 9.28%, driven by increased digital usage among younger users and their propensity for value shopping. Platforms appealing to this demographic, such as UNiDAYS and Student Beans, are combining price comparison with student discounts. The ultimate motivator is cost, backed by unique promotions and editorial product lists. Recent Price Comparison Websites market trends have seen student-only portals, subscription bundles, and AI-curated comparisons of academic software emerge. This tech-savvy generation now turns to PCWs to discover the best value deals, particularly for books, electronics, and course tools.

By Data Source

Retailer websites are the primary data source for PCWs, contributing 43.47% of market revenue in 2024. These sites provide real-time product availability, pricing, and promotions. Major platforms like Amazon and Walmart support rich data feeds that PCWs tap into for accurate comparisons. The main driver is consumer demand for up-to-date, retailer-verified pricing. Product developments include real-time inventory sync and automated discount tracking. As retailers become more open to third-party integrations, this data source ensures reliability and enhances user trust in comparison results.

AI-based data sources are growing at a CAGR of 10.52%, due to their capacity to deliver dynamic, predictive, and personalized feedback. Marketplaces such as Google Shopping can take advantage of AI to sort products intelligently, analyze sentiment in customer reviews, and apply dynamic pricing. The predominant motivation is the requirement of high-precision intelligence and improved user experience. New developments include natural language search, image-based product recognition, and AI-driven competitor benchmarking. These attributes not only increase data quality but also cast AI as a change agent for the PCW ecosystem.

By Value-Added Services

Personalized Shopping Experience has the largest revenue share at 11.92% in 2024. Sites such as Shopzilla and Amazon offer personalized product recommendations based on a user's behavior and interests. The primary motivator is increased consumer demand for timely and relevant product offerings. New developments involve preference learning with AI and cross-device personalization integrated into the framework. These tools boost user experience and satisfaction, which has a direct impact on conversion rates. As personalization is now the norm, its effect on user loyalty and average order value further solidifies its stronghold.

Loyalty Programs are growing at a CAGR of 9.35% due to the urgency for improving customer retention and lifetime value. Market leaders like Expedia Group and Booking Holdings have rewards systems as part of their comparison features. The primary catalyst is user affinity towards cumulative saving and personalized benefits. Recent developments involve gamified loyalty functionality, tiered membership, and cross-platform point redemption. These programs not only differentiate platforms in a competitive environment but also establish repeat engagement, serving as a means for sustaining long-term user acquisition efforts.

Regional Analysis

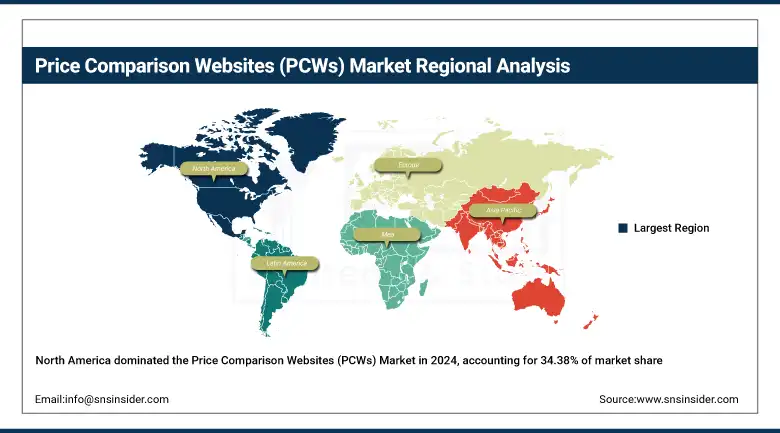

North America, holding the dominant position with a 34.38% Price Comparison Websites (PCWs) market share in 2024, leads the global PCWs market due to advanced digital infrastructure, high penetration of the Internet, and an established e-commerce ecosystem. Being aware of price transparency, consumers increasingly use the AI technologies adopted by the retail comparison platforms. Besides, Google Shopping and Amazon hugely reinforce the PCWs market as the leading market players.

Get Customized Report as per Your Business Requirement - Enquiry Now

The U.S. dominates the North American market, driven by high consumer demand for competitive pricing, robust e-commerce penetration, and technological advancements like AI-based comparison engines.

Europe exhibits steady growth in the PCWs market, supported by consumer preference for informed buying and regulatory encouragement for transparency in digital markets. Countries like Germany, the UK, and France are major contributors due to their mature online retail and travel sectors.

The UK dominates the European market owing to its highly developed online shopping ecosystem and strong presence of PCW platforms across finance, insurance, and retail sectors.

Asia Pacific is the fastest-growing region in the market, projected to expand at a CAGR of 8.87% during the forecast period. This growth is fueled by increasing internet and smartphone usage, an expanding middle class, and rising online retail penetration. Increasing consumer need for deal comparison and mobile-first shopping behavior is a crucial market accelerator in all emerging economies.

China leads the Asia Pacific market due to its massive e-commerce ecosystem, strong digital adoption, and government support for digital economy initiatives, which fuel demand for PCWs across categories.

Middle East & Africa and Latin America are expected to grow at a constant pace in the PCWs market as a result of digital transformation, enhanced payment infrastructure, high e-commerce presence, and the rising trend of online price comparison. The UAE and Brazil are front-runners in the regions, with strong internet penetration, supportive steps by governments, and localized comparison platforms taking out.

Key Players

The major key players of the Price Comparison Websites (PCWs) Market are Shopzilla, Priceline, Kayak, Expedia, Orbitz, Travelocity, Google, Yahoo, Bing, Booking Holdings, and others.

Key Developments

-

In April 2025, Expedia unveiled enhanced “Bundle & Save” features, allowing travelers to combine flights, hotels, and car rentals for up to 10% savings. The update includes flexible payment options, aiming to boost booking convenience and value.

-

In April 2025, Kayak debuted Kayak.ai, an AI-driven, chat-first interface offering real-time pricing from over 400 providers and conversational travel planning. They also appointed a dedicated CTO to accelerate their AI capabilities, signaling a strong focus on innovation.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 53.74 Billion |

| Market Size by 2032 | USD 96.01 Billion |

| CAGR | CAGR of 7.54% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Business Model (Free Service, Paid Subscription, Commission-Based, Hybrid (Combination of Models)) • By Service Scope (General Merchandise, Travel and Hospitality, Financial Services, Electronics, Software and Technology) • By Target Audience (Consumers, Businesses, Students, Senior Citizens, Budget-Conscious Individuals) • By Data Source (Retailer Websites, Manufacturer Data, User Reviews, Crowdsourced Data, Artificial Intelligence (AI)) • By Value-Added Services (Product Recommendations, Price Alerts, Loyalty Programs, Exclusive Deals, Personalized Shopping Experiences) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Shopzilla, Priceline, Kayak, Expedia, Orbitz, Travelocity, Google, Yahoo, Bing, Booking Holdings. |

Frequently Asked Questions

North America dominated the Price Comparison Websites (PCWs) Market in 2024 with a 34.38% market share, driven by advanced digital infrastructure, high internet penetration, and a mature e-commerce ecosystem.

By Business Model, the Commission-Based segment held the highest revenue share at 41.25% in 2024, making it the dominant type throughout the projected years.

The major growth factor is the rising adoption of AI and personalized recommendations, which enhances consumer engagement and conversion rates through features like dynamic pricing, AI-driven chatbots, and tailored content.

The market size was USD 53.74 billion in 2024.

The market is projected to expand at a CAGR of 7.54% from 2025 to 2032.

Get in Touch