Professional Services Automation Software Market Analysis & Overview:

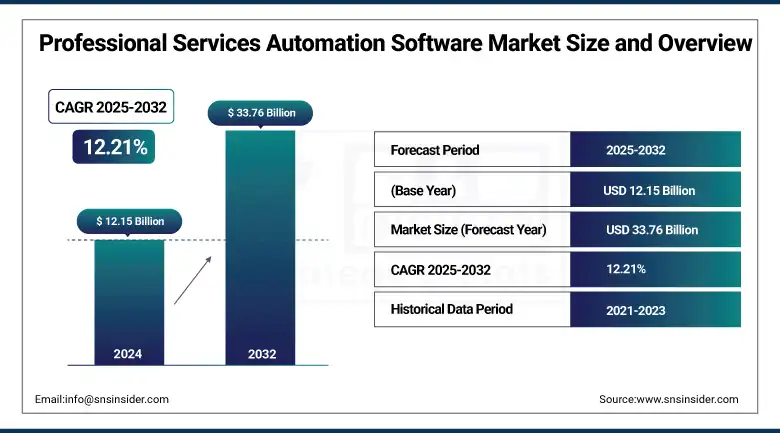

Professional Services Automation Software Market size was valued at USD 12.15 billion in 2024 and is expected to reach USD 33.76 billion by 2032, growing at a CAGR of 12.21% from 2025-2032.

The Professional Services Automation Software Market is growing due to rising demand for efficient project management, resource utilization, and real-time analytics in enterprises. The adoption of cloud-based solutions and the use of AI for improved forecasting and decision-making further increase market growth, particularly among IT, consulting, and engineering companies.

To Get more information On Professional Services Automation Software Market - Request Free Sample Report

As of 2024, 94% of businesses use cloud services, and 73% implement hybrid cloud systems to increase flexibility and scalability.

For instance, as of October 2024, SAP Business Technology Platform (BTP) is used by over 27,000 customers and over 2,800 partners globally.

In 2024, Procore introduced Procore AI with Agents, Insights, and Copilot to simplify construction management. They automate work, provide data-backed insights, and increase productivity, with additional feature rollouts on the horizon during 2025.

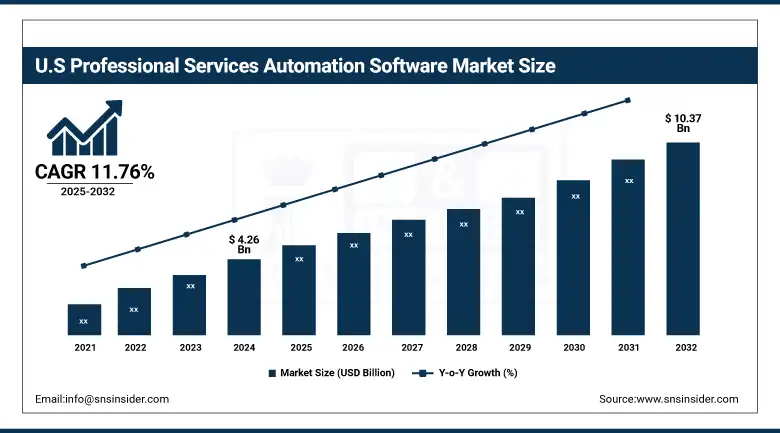

U.S. Professional Services Automation Software Market size was valued at USD 4.26 billion in 2024 and is expected to reach USD 10.37 billion by 2032, growing at a CAGR of 11.76% from 2025-2032.

U.S. Professional Services Automation Software Market growth is expanding due to rising demand for effective management of resources, tracking of projects in real-time, and automation of service delivery. Implementation of cloud-based solutions and AI-powered tools also drives the market faster.

In the U.S., federal agencies are increasingly adopting cloud solutions, with 24 major agencies having set policies and guidance to ensure secure and cost-effective cloud services.

The U.S. Census Bureau's Business Trends and Outlook Survey indicates that AI adoption among U.S. businesses increased from 3.7% in fall 2023 to 5.4% by February 2024, with expectations to reach 6.6% by early fall 2024.

Professional Services Automation Software Market Dynamics

Drivers

• Growing emphasis on real-time analytics and project visibility is accelerating software investments among enterprise service providers globally

As more service-based businesses emerge, project visibility and real-time information spur investments. PSA software provides consolidated dashboards to track project milestones, financial metrics, and resource allocations, facilitating smart decision-making, cost control, and increased client satisfaction. Flexibility and transparency of PSA platforms are necessary for business development and managing multiple engagements. This is particularly important for multinational organizations needing standardized control across geographies, necessitating analytics-driven PSA solutions as a means to operational management and strategic forecasting.

As per studies, the report unfolds that 85% of most successful organizations adopting PSA software avail advantages, including 14% boost in billable utilization, 9% higher rate of realization, 50% quickening of project sourcing, and as much as 24% better EBITDA.

Replicon's Polaris PSA software has been used by more than 7,800 clients, including Fujitsu and the USDA. The system provides a 10% boost in closed revenue leakages, a 90% reduction in administrative overhead, and a 5 to 10% boost in utilization of resources, as stated on the company's website.

Restraints

• Concerns around data privacy, compliance, and vendor lock-in discourage enterprises from fully committing to PSA platforms

Enterprise clients are reluctant to embrace PSA solutions post full because of data security concerns over third party or cloud based platforms. For firms which operate across multiple jurisdictions, regulatory compliance such as GDPR starts complicating things further. Additionally, there is apprehension about vendor lock-in, switching providers or integrating alternative systems â both of which dissuade adoption. The lack of transparency in contract terms, scalability and future-proofing has made enterprises wary of vendor-locked solutions. Such issues restrict growth of market, particularly for large, risk averse organizations.

Opportunities

• Growing adoption of AI and automation capabilities within PSA platforms is unlocking new strategic and operational efficiencies

Integration of machine learning and AI in PSA solutions is transforming predictive planning and automation. Machine learning and AI enable smart forecasting, proactive risk management, and self-scheduling resources, streamlining administrative burdens. Service organizations are now more focused on using AI-driven platforms for searching historical information, creating usable insights to help drive profit margins and client success. This movement puts into focus the growing demand for strategic automation, positioning PSA vendors to respond to the needs of an aggressive, high-velocity professional services marketplace through fact-based decision-making.

The ServiceNow AI Platform freed up 3 million employee hours, worth $325 million each year. It lowered IT help desk resolution time by 37%, accelerated payroll questions from 4 days to 8 seconds, and enhanced software development productivity with a 52% AI code acceptance rate.

Forecast App leverages AI for real-time visibility into project performance, resource utilization, and finances to allow customers to realize 65% margin targets, prevent scope and cost creep, and deliver 50% top-line and headcount growth.

Challenges

• Lack of standardization in workflows and service delivery models complicates software customization and cross-organizational implementation

Professional services firms have variable project flows, billing models, and delivery structures, which create a challenge for implementing traditional PSA software in these firms. Traditional PSA software vendors cannot create elastic, scalable platforms to accommodate this variability without deep customization. This non-standardization makes it harder to onboard, lengthens deployment times, and costs more. User adoption across departments with varying processes throws in an added barrier. These issues impact software scalability, especially when dealing with multinational clients with region-specific operational requirements and compliance requirements.

Professional Services Automation Software Market Segmentation Analysis

By Component

The Solutions segment dominated the Professional Services Automation Software Market share of 69% in 2024, owing to its wide-ranging offerings that bring together project management, resource planning, and time tracking on a single platform. Businesses prefer these solutions because of their ability to scale, be customized, and simplify operations making them a strategic investment for workflow optimization as well as gaining visibility in complicated, client-centric service environments.

Services segment is expected to grow at the fastest rate, with a growth CAGR of 14.06% during 2025-2032, as the need for implementation, integration, and training assistance increases. As companies utilize more sophisticated automation solutions, professional services are essential to enable seamless onboarding, maximize ROI, and tailor solutions according to specific operational needs especially for organizations with limited in-house IT capabilities or undergoing digital transformation.

By Deployment

The On-premise segment accounted for the largest revenue share of 24% in 2024, primarily because of its popularity among organizations having stringent data security policies, regulatory compliance requirements, or legacy platforms. Many large enterprises and government agencies still rely on on-premise deployments to exercise greater control over sensitive information, in addition to maintaining internal governance standards across their professional service operations.

The Cloud segment is projected to expand at the fastest CAGR of 13.08% during the period 2025-2032, driven by its lower initial costs, scalability, and convenience of remote access. As more businesses adopt distributed and hybrid work patterns, cloud-based PSA solutions offer rapid deployment cycles and real-time collaboration highly desirable for growing businesses that seek agility, reduced IT overhead, and easy software updates within a dynamic marketplace.

By Enterprise Size

Large Enterprises dominated the market with 56% of overall revenue in 2024, propelled by their sophisticated business operations, high volumes of clients, and more significant budgetary investment in digital transformation. Large enterprises gain the most from PSA tools that consolidate processes, enhance billing accuracy, and provide resource optimization for varied departments and international projects making automation an essential part of their strategic service delivery.

Small and Medium Enterprises are expected to advance at the fastest CAGR of 13.38% from 2025 to 2032, due to growing awareness of how automation can increase profitability and efficiency. As PSA solutions come down in price and are available across a broader range, SMEs increasingly adopt these solutions to improve resource planning, track time, and streamline processes allowing them to compete on a level playing field in client-oriented service sectors without the cost of enterprise IT investment.

By Application

Technology Companies led the PSA software market in 2024 with a 32% revenue share, as their inherent dependence on project-based work, agile methods, and high need for resource visibility drives them to be early adopters of PSA tools to improve service delivery, handle cross-functional teams, and synchronize financial performance with technical output—requiring automation to ensure competitiveness and operational scalability in a technology-driven environment.

Marketing and Communication are anticipated to expand at a CAGR of 14.05% from 2025 to 2032, with increasing client demands for transparency, quicker turnaround for campaigns, and measurable ROI fueling expansion. PSA software helps these companies to manage timelines, monitor budgets, and build client relationships by providing rich reporting and live project tracking critical drivers in an industry where possessing multiple accounts accurately impacts profitability.

Professional Services Automation Software Market Regional Outlook

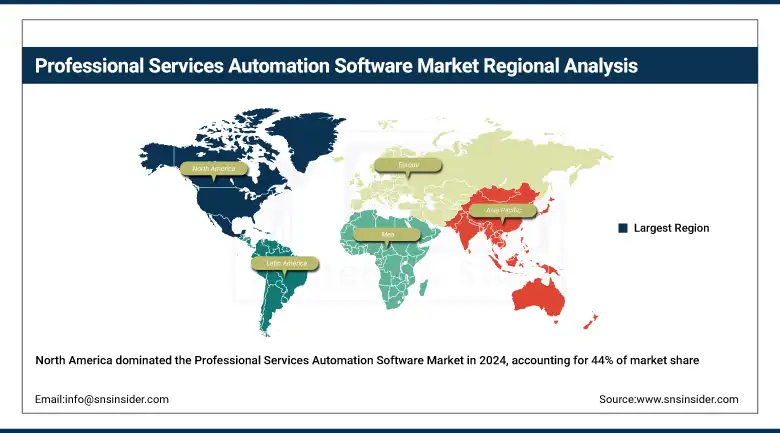

North America led the Professional Services Automation Software Market with the largest revenue share of approximately 44% in 2024 because of the intense presence of top software vendors, early technology adoption, and maximum demand for automation of consulting, IT, and legal services. The region's mature digital base and concentration on driving labor productivity by means of integrated project and resource management software also drove leadership in the market.

Get Customized Report as per Your Business Requirement - Enquiry Now

The U.S. had a market leadership position due to early technology adoption, strong established presence of leading vendors, and high demand for automation in professional service markets.

Asia Pacific will expand at the fastest CAGR of 14.51% over 2025-2032, driven by rapid digitalization, increase in IT services and increased awareness of efficiency due to automation. The higher market growth in the region is driven by the rapid adoption of cloud solutions by small and medium-sized businesses, high investment in professional services, and technology ecosystem development in the regional markets including China and India.

China is leading the Professional Services Automation Software Market in Asia Pacific with its fast-growing technological developments, extensive digital transformations, and heavy investments in automation across sectors.

Europe is well established in the Professional Services Automation Software Market with its mature IT infra, strong focus on digital transformation, and extensive use of automation solutions to enhance operation efficiency and service quality across sectors.

Germany is leading the Professional Services Automation Software Market because of its robust industrial base, sophisticated digital infrastructure, and high rate of adoption of enterprise automation solutions.

Middle East & Africa and Latin America are experiencing growth in the Professional Services Automation Software Market because of growing demand for digital transformation, rising technology adoption, and the necessity to automate business processes across industries, especially in emerging economies.

Key Players

Professional Services Automation Software Market companies include Autotask Corporation, Atlassian, BMC Software, Inc., ConnectWise, Inc., Deltek, Inc., FinancialForce.com, Kimble Apps, Klient, Inc., Microsoft Corporation, NetSuite OpenAir, Inc., Oracle Corporation, Planview, PROJECTOR PSA, SAP SE, Upland Software, Inc., Workday, Inc.

Recent Developments:

-

Jan 2025, NetSuite rebranded OpenAir to SuiteProjects Pro with the 2025.1 release, adding homepage charts, improved global search, and a collaboration tool to streamline PSA project management.

-

Jul 2024, NetSuite OpenAir 2024.2 introduced the Redwood design system, a refreshed homepage, and enhanced global search, delivering a modernized and intuitive PSA experience for project and resource management teams.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 12.15 Billion |

| Market Size by 2032 | USD 33.76 Billion |

| CAGR | CAGR of 12.21% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Component (Solutions, Services) •By Deployment (Cloud, On-premise) •By Enterprise Size (Large Enterprises, Small & Medium Enterprises) •By Application (Consulting Firms, Marketing and Communication Companies, Technology Companies, Architecture, Engineering, and Construction Companies, Audit and Accounting Firms, Scientific Research and Development Companies, Legal Services, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Autotask Corporation, Atlassian, BMC Software, Inc., ConnectWise, Inc., Deltek, Inc., FinancialForce.com, Kimble Apps, Klient, Inc., Microsoft Corporation, NetSuite OpenAir, Inc., Oracle Corporation, Planview, PROJECTOR PSA, SAP SE, Upland Software, Inc., Workday, Inc. |

Get in Touch