Programmatic Advertising Market Report Scope & Overview:

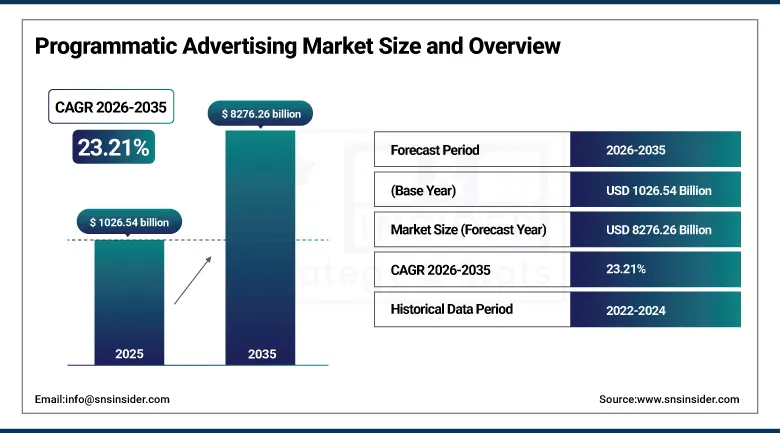

The Programmatic Advertising Market was valued at USD 1,026.54 billion in 2025 and is expected to reach USD 8,276.26 billion by 2035, growing at a CAGR of 23.21% from 2026–2035.

The global Programmatic Advertising Market represents one of the most consequential structural transformations in the entire media and advertising industry, as the systematic replacement of manual insertion order-based media buying with automated, data-driven, real-time auction systems is compressing the human decision cycle in advertising from weeks of planning and negotiation to milliseconds of algorithmic optimisation at the moment of each individual ad impression opportunity. Programmatic advertising encompasses all forms of automated digital media buying and selling, including real-time bidding auctions where supply-side platforms and demand-side platforms exchange thousands of simultaneous bid requests and responses within the fraction of a second between a webpage loading and the ad slot rendering, programmatic direct deals where guaranteed inventory is transacted at agreed rates through automated workflows without the operational complexity of traditional insertion orders, and private marketplace environments where premium publishers invite selected buyers to compete for exclusive inventory in controlled auction environments.

The Programmatic Advertising Market's extraordinary 23.21% CAGR from 2026 to 2035 reflects the compounding commercial momentum of a market where every major digital media channel is progressively adopting programmatic buying mechanisms, every major brand advertiser is increasing the programmatic share of its media budget, and the technology infrastructure that makes programmatic advertising possible is continuously improving in sophistication, scale, and intelligence. Meta Platforms' 2025 announcement of plans to roll out fully autonomous AI-powered ad creation across Facebook and Instagram by 2026 and Google's generative AI feature expansion at DMEXCO 2024 confirm that the world's two largest digital advertising platforms are investing in programmatic automation that will accelerate market growth through the forecast period.

Programmatic Advertising Market Size and Forecast

-

Market Size in 2025: USD 1,026.54 Billion

-

Market Size by 2035: USD 8,276.26 Billion

-

CAGR: 23.21% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Programmatic Advertising Market - Request Free Sample Report

Programmatic Advertising Market Trends

-

Rapid expansion of programmatic advertising into Connected Television, where major streaming platforms including Netflix, Disney Plus, Hulu, and Peacock are integrating programmatic ad sales infrastructure enabling advertisers to reach targeted television audiences through the same audience data and campaign management systems used for digital advertising, bridging the historic gap between TV brand building and digital performance marketing.

-

Growing adoption of privacy-first programmatic solutions in response to third-party cookie deprecation, where advertisers and platforms are investing in first-party data infrastructure, contextual targeting algorithms, data clean room technology, and privacy-preserving identity solutions that maintain targeting effectiveness while complying with GDPR, CCPA, and emerging global privacy regulations.

-

Accelerating integration of generative AI into programmatic creative development, where AI systems automatically generate multiple ad creative variants optimised for different audience segments, device types, and campaign contexts, enabling dynamic creative optimisation at a scale and speed impossible through traditional creative production workflows.

-

Rising adoption of retail media networks, where major retailers including Amazon, Walmart, Target, and Kroger monetise their first-party shopper data and owned digital touchpoints through programmatic advertising platforms that enable consumer goods brands to reach shoppers with high purchase intent at or near the point of sale.

-

Growing development of programmatic audio advertising across music streaming, podcast, and internet radio platforms, where Spotify, iHeartRadio, and podcast networks are implementing programmatic ad insertion technology enabling real-time, audience-targeted audio ad placement within streamed content.

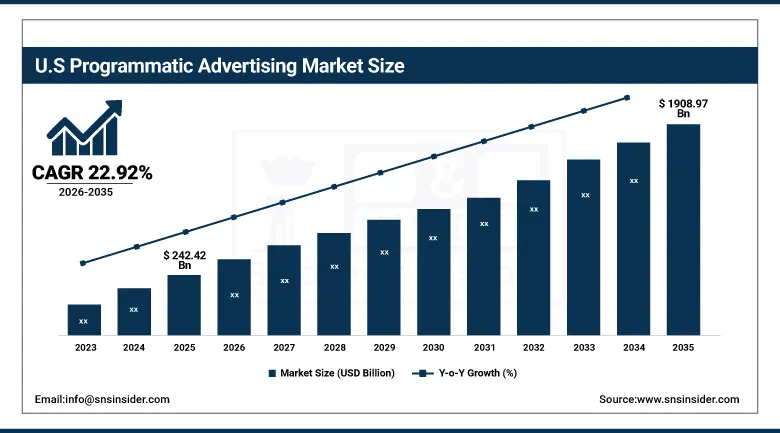

U.S. Programmatic Advertising Market was valued at USD 242.42 billion in 2025 and is expected to reach USD 1,908.97 billion by 2035, growing at a CAGR of 22.92% during 2026–2035.

The United States dominates the global Programmatic Advertising Market as the world's most commercially advanced and technically sophisticated programmatic advertising ecosystem, where programmatic buying mechanisms now account for the overwhelming majority of all digital advertising transactions and are progressively extending into Connected TV, digital audio, and addressable traditional television channels that represent the largest remaining opportunities for programmatic market expansion. U.S. market leadership is sustained by the commercial headquarters of the world's dominant programmatic platform operators including The Trade Desk, Google Display and Video 360, Amazon DSP, Meta Ads Manager, and Adobe Advertising Cloud, combined with the most developed supply-side platform ecosystem, the deepest first-party data infrastructure from the world's most data-rich consumer economy, and the most sophisticated brand advertiser digital marketing capabilities that continuously push programmatic technology innovation at the commercial frontier. The U.S. programmatic advertising market's size reflects the comprehensive digital advertising infrastructure investment of every major consumer-facing industry sector, from the largest retail and consumer goods advertisers whose programmatic retargeting and prospecting campaigns constitute a foundational revenue stream for all major programmatic platforms, to the rapidly growing pharmaceutical and healthcare programmatic adoption enabled by HIPAA-compliant audience targeting solutions.

Meta Platforms' 2025 announcement of plans to roll out fully autonomous AI-powered ad creation across Facebook and Instagram by 2026, enabling campaigns to be set up with minimal inputs such as images and budgets, represents the most significant single programmatic automation advance by any platform in the industry's history. This AI-driven creative automation, combined with Meta's already sophisticated algorithmic campaign optimisation, will further consolidate Meta's position as a leading programmatic advertising destination while raising the baseline automation expectations that advertisers bring to all programmatic platforms through the 2026 to 2035 forecast period.

Programmatic Advertising Market Segment Insights

-

According to Ad Format, Video dominated with approximately 24% revenue share in 2025, driven by immersive storytelling capability, higher engagement rates, and strong brand recall relative to static display formats; Others (smart TVs, wearables, voice assistants) is the fastest-growing format category at approximately 25.15% CAGR from 2026 to 2035 driven by emerging device ecosystem expansion.

-

In terms of Device Type, Mobile and Tablets dominated with approximately 50% revenue share in 2025, driven by widespread smartphone penetration and mobile-first content consumption enabling location-aware, hyper-targeted ad delivery; Connected TV is the fastest-growing device segment through the extraordinary expansion of streaming platform programmatic ad sales.

-

By Transaction Model, Real-Time Bidding dominated as the largest transaction model; Programmatic Direct is the fastest-growing transaction model driven by premium publisher preference for guaranteed revenue at premium pricing with greater brand safety control than open RTB environments.

-

By End-User Industry, Retail and Consumer Goods dominated with approximately 34% revenue share in 2025 through high consumer engagement, purchase intent targeting, and real-time campaign optimisation for e-commerce conversion; Media and Entertainment is the fastest-growing end-user industry at approximately 25.95% CAGR from 2026 to 2035.

Programmatic Advertising Market Segment Analysis

By Ad Format: Video dominates, Others (Emerging Devices) grows fastest

Video Ad Format retained the dominant position in the Programmatic Advertising Market in 2025 with approximately 24% of revenues, reflecting the advertising industry's fundamental commercial conviction that video creative delivers the most emotionally resonant, brand-building advertising experiences available in digital media, combined with the technical maturity of programmatic video infrastructure including video SSPs, DSP video bidders, VAST and VPAID ad serving standards, and server-side ad insertion technology for streaming environments. Programmatic video encompasses pre-roll, mid-roll, and post-roll in-stream video placements across YouTube, social media video feeds, Connected TV streaming environments, and mobile app video interstitials, each offering distinct audience reach, engagement, and pricing characteristics that advertisers optimise across through unified programmatic buying platforms. The shift from traditional television to streaming media consumption is progressively migrating television advertising budgets from upfront guaranteed broadcast placements into programmatic CTV and digital video buying, creating a convergence of television-scale brand investment with digital precision targeting that is the programmatic advertising market's most commercially significant near-term growth driver.

The Others segment, encompassing smart TV app advertisements, wearable device notifications, voice assistant ad integrations, and emerging programmatic format categories, is projected to grow at the fastest CAGR of approximately 25.15% through 2035, driven by the progressive proliferation of internet-connected devices beyond the smartphone and computer screens that currently dominate programmatic media consumption. Smart TV app environments, where streaming content is consumed on the largest screens in the home with the most attentive viewing contexts, represent the highest-value emerging programmatic inventory frontier, attracting premium CPMs from brand advertisers seeking high-impact brand awareness placements at television-equivalent audience scale with digital targeting precision.

By Device Type: Mobile and Tablets dominate, Connected TV grows fastest

Mobile and Tablets retained the dominant device type position with approximately 50% of Programmatic Advertising Market revenues in 2025, reflecting the global consumer transition to mobile-first digital content consumption where the smartphone has become the primary access point for social media, search, video streaming, e-commerce, news, and entertainment that collectively constitute the most commercially valuable programmatic advertising inventory categories. Mobile programmatic advertising benefits from the richest location awareness, enabling geotargeted and proximity-based advertising execution that desktop environments cannot replicate, from the deepest individual user behavioural data generated through continuous mobile device usage throughout the day, and from the highest time-spent engagement rates that make mobile inventory the most competitively priced and performance-validated format in the programmatic ecosystem. The ubiquity of programmatic-enabled mobile advertising SDKs within app monetisation frameworks has created a vast supply of mobile programmatic inventory across gaming, utility, social, and entertainment applications that sustains mobile's dominant market position.

Connected TV is projected to be the fastest-growing device segment through 2035, as the global acceleration of linear television audience migration to streaming platforms is creating the most commercially significant expansion opportunity in the programmatic advertising industry since mobile programmatic emerged a decade ago. CTV programmatic advertising combines the brand-building creative impact of traditional television with the audience targeting, campaign measurement, and real-time optimisation capabilities of digital programmatic buying, creating a unique media category that is attracting both television-focused brand advertising budgets migrating from linear and digital-focused performance budgets extending into premium video environments. The Netflix, Disney Plus, and Peacock advertising tier launches combined with Hulu's mature programmatic advertising infrastructure collectively represent a premium CTV programmatic inventory expansion that is enabling the largest brand advertisers to reach streaming audiences at scale through programmatic buying workflows.

By Transaction Model: Real-Time Bidding dominates, Programmatic Direct grows fastest

Real-Time Bidding retained the dominant transaction model position in the Programmatic Advertising Market in 2025, reflecting its status as the foundational infrastructure through which the vast majority of programmatic advertising inventory is transacted in open auction environments where DSP buyers compete for each individual impression opportunity in millisecond-duration auctions. RTB's dominance is sustained by the extraordinary scale of the open web's programmatic inventory, where hundreds of thousands of publisher websites and apps make billions of daily impression opportunities available through SSP connections to the major ad exchanges, enabling advertisers to reach target audiences across the long tail of internet content at the CPMs that open auction competitive dynamics produce. RTB's operational efficiency for advertisers seeking reach and scale at competitive pricing, combined with its compatibility with sophisticated audience data activation and bid optimisation algorithms, makes it the default transaction mechanism for programmatic media buyers pursuing awareness and retargeting campaign objectives.

Programmatic Direct is the fastest-growing transaction model through 2035, driven by brand advertisers' increasing preference for guaranteed impressions at agreed CPMs with premium publishers whose content environments and audience quality meet the brand safety and context standards that large-brand programmatic programmes require. Programmatic Direct enables automated execution of reservation-based advertising deals that would otherwise require manual trafficking, creative management, and billing reconciliation through traditional direct sales workflows, providing efficiency gains for both advertisers and publishers while maintaining the predictability of guaranteed impression delivery that performance-critical campaigns require.

By End-User: Retail and Consumer Goods dominates, Media and Entertainment grows fastest

Retail and Consumer Goods retained the dominant end-user industry position in 2025 with approximately 34% of Programmatic Advertising Market revenues, reflecting the retail industry's foundational commercial reliance on digital advertising for customer acquisition, product discovery, cart abandonment recovery, and loyalty re-engagement that collectively make programmatic advertising the primary revenue driver for the world's largest retail and consumer goods companies. Retail programmatic advertising encompasses the full consumer purchase funnel from awareness campaigns targeting broad demographic audiences for new product launches through retargeting campaigns reaching consumers who have previously visited product pages or abandoned shopping carts, with campaign performance measured at the individual sale or revenue attribution level that enables continuous algorithmic optimisation against commercial outcomes. The rise of retail media networks operated by Amazon, Walmart, Kroger, and Target is creating a premium, closed-loop programmatic advertising ecosystem where brands can reach verified shoppers with high purchase intent within the retailer's owned inventory and measure campaign outcomes through transaction data that provides the most commercially validated advertising attribution available anywhere in digital advertising.

The Media & Entertainment industry will grow at the highest rate of approximately 25.95% CAGR between 2022 and 2035 due to the massive amount of content consumption on OTT platforms, games, streaming, and social media that results in a highly growing pool of programmable advertising inventory along with growing advertiser need to connect to target audiences while consuming digital entertainment content. Streaming Media sector's adoption of an advertising-based model with Netflix Standard with Ads, Disney Plus Basic, and Peacock ad-supported tier resulting in adding tens of millions of ad-viewers to their user base since 2022 is giving rise to premium programmable CTV inventory and changing the very fabric of Television Advertiser Market Structure. Gaming programmatic advertising is one of the fastest-growing sectors of programmatic advertising which consists of ad placement in game environment on mobile, consoles, and PC, where gamer audience provides some of the best engagement in the digital advertising ecosystem.

Programmatic Advertising Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

~84% |

|

Europe |

United Kingdom |

~30% |

|

Asia Pacific |

China |

~43% |

|

Middle East & Africa |

UAE |

~30% |

|

Latin America |

Brazil |

~44% |

North America Programmatic Advertising Market Insights

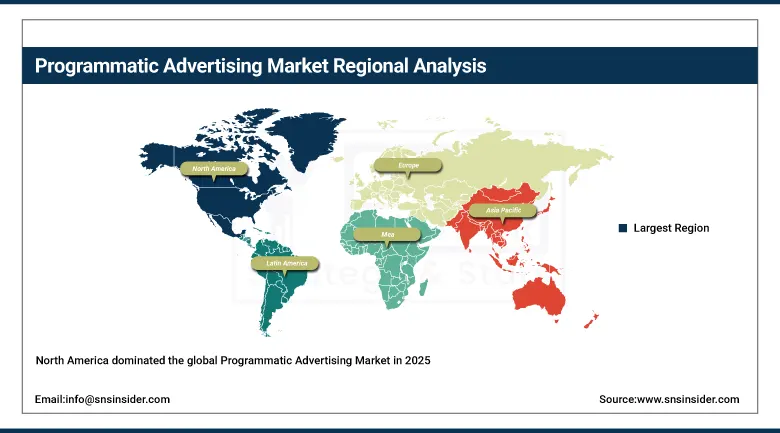

North America dominated the global Programmatic Advertising Market in 2025, led by the United States which accounted for approximately 84% of North American revenues. U.S. market leadership is anchored by the commercial headquarters of the world's dominant programmatic platforms including The Trade Desk, Google DV360, Amazon DSP, Meta Ads Manager, and the major independent DSP and SSP ecosystems, combined with the world's highest programmatic adoption rate among brand advertisers and the most advanced first-party data infrastructure supporting privacy-compliant programmatic targeting. The U.S. market's scale and sophistication set global programmatic standards that are progressively adopted across international markets.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Programmatic Advertising Market Insights

Asia Pacific is the fastest-growing regional programmatic advertising market, driven by China's massive digital advertising ecosystem encompassing Alibaba's digital media network, Baidu's search and display programmatic infrastructure, and ByteDance's TikTok and Douyin programmatic capabilities, combined with India's rapidly expanding mobile digital advertising market as smartphone internet adoption creates one of the world's largest and fastest-growing digital media audiences. Japan, South Korea, and Southeast Asian markets are each building sophisticated programmatic advertising ecosystems, with regional DSPs and SSPs serving local publisher and advertiser needs alongside the global platform participants.

Europe Programmatic Advertising Market Insights

Europe represents a sophisticated and commercially significant programmatic advertising market, shaped by GDPR's stringent consent requirements that have accelerated European investment in contextual targeting, first-party data infrastructure, and privacy-preserving audience solutions that are progressively influencing global programmatic technology development. The UK leads European programmatic adoption through its world-class digital advertising industry, followed by Germany, France, and the Netherlands as major European programmatic markets. European programmatic growth is additionally driven by the rapid expansion of Connected TV programmatic as major streaming platforms launch advertising tiers across European markets.

Middle East & Africa and Latin America Programmatic Advertising Market Insights

MEA and Latin America are rapidly growing programmatic advertising markets, driven by accelerating digital media adoption and brand advertising budget migration from traditional to digital channels. The UAE leads MEA adoption through its sophisticated digital media culture and high concentration of global brand regional marketing headquarters investing in programmatic efficiency. Brazil leads Latin American programmatic revenues at approximately 44% of regional share through its advanced digital advertising ecosystem, high mobile internet penetration, and sophisticated advertiser community that has been among the earliest emerging market adopters of programmatic buying technology.

Programmatic Advertising Market Growth Drivers:

-

AI-powered automation and data-driven precision targeting delivering demonstrably superior advertising ROI creating systematic digital media budget migration toward programmatic channels

The primary structural growth driver for the Programmatic Advertising Market is the documented and consistently validated ability of programmatic advertising to deliver superior return on advertising spend relative to manual media buying through continuous real-time campaign optimisation, precise audience targeting against behavioural and contextual signals unavailable in traditional media, and the operational efficiency of automated buying that concentrates advertiser resources on strategy and creative rather than media transactional administration. The systematic extension of programmatic buying mechanisms into every digital media channel, from its established dominance in display and mobile through its rapid expansion in CTV, digital audio, digital out-of-home, and gaming, creates a compounding market expansion dynamic where each new channel adoption by programmatic buying technology expands the total addressable market for the entire programmatic ecosystem.

Meta Platforms' 2025 announcement of fully autonomous AI-powered ad creation across Facebook and Instagram by 2026, combined with Google Ads' DMEXCO 2024 generative AI feature introduction enabling enhanced campaign customisation through AI, collectively represent the most advanced programmatic automation milestone in the industry's history. These developments confirm that the world's two largest digital advertising platforms are converging toward a model where the entire advertising creative-to-placement-to-optimisation workflow is automated through AI, progressively reducing the human time investment required to run sophisticated programmatic campaigns while simultaneously improving campaign performance through continuous algorithmic improvement. This automation deepening sustains the Programmatic Advertising Market's exceptional 23.21% CAGR through the 2026 to 2035 forecast period.

Programmatic Advertising Market Restraints

-

Third-party cookie deprecation creating targeting signal disruption, ad fraud reducing budget efficiency, and privacy regulation compliance complexity constraining data-driven audience activation

A significant restraint on the Programmatic Advertising Market is the progressive deprecation of third-party cookies across major web browsers, led by Google Chrome's phased removal plan that eliminates the primary audience identification mechanism used for cross-site retargeting and frequency capping in the open web programmatic ecosystem, requiring the industry to develop and adopt alternative identity solutions including first-party data matching, privacy-preserving audience cohort technologies, and contextual targeting approaches that maintain audience relevance without individual user cross-site tracking. Ad fraud, encompassing bot traffic, domain spoofing, ad stacking, and other techniques that generate fraudulent impressions billed to advertisers without delivering genuine human audience exposure, represents a persistent cost drain from programmatic advertising budgets that industry estimates place between 5 and 15% of programmatic spend depending on channel and measurement methodology, reducing the net ROI that advertisers realise from programmatic investment. The complexity of privacy regulation compliance across GDPR, CCPA, and the growing number of national and state privacy laws requires advertisers and platforms to invest substantially in consent management infrastructure, data governance frameworks, and legal compliance capabilities that increase the operational cost of programmatic advertising programme management.

Programmatic Advertising Market Opportunities

-

Connected Television programmatic expansion, retail media network development, and AI-native programmatic campaign management

The transition of linear television viewership to streaming platforms creates a transformative programmatic advertising expansion opportunity, as the remaining USD 60 to 80 billion U.S. television advertising market progressively migrates from guaranteed upfront buying to programmatic CTV transactional models that enable the audience precision, measurement, and real-time optimisation capabilities that streaming environments uniquely support. Retail media networks, combining retailer first-party shopper data with owned digital touchpoints and programmatic buying infrastructure, represent the fastest-growing premium programmatic advertising category and offer consumer goods brands the most commercially validated advertising attribution available through closed-loop purchase measurement. AI-native programmatic campaign management platforms that automate the entire campaign lifecycle from audience strategy through creative generation, bid optimisation, pacing management, and performance reporting with minimal human intervention represent the programmatic market's ultimate commercial evolution, enabling small and mid-size advertisers to access enterprise-grade campaign management capabilities at accessible self-serve price points.

Recent Developments:

-

2025: Meta Platforms announced plans to roll out fully autonomous AI-powered ad creation across Facebook and Instagram by 2026, enabling campaigns to be launched with minimal inputs such as images and budgets, representing the most advanced advertiser-facing programmatic automation milestone in platform advertising history.

-

2024: Google Ads introduced new generative AI features at DMEXCO 2024, offering enhanced campaign insights and creative customisation tools that give advertisers greater control over AI-driven programmatic campaign execution across Google's Search, Display, and YouTube advertising products.

-

2025: The Trade Desk advanced its Kokai AI-powered DSP platform with enhanced predictive audience modelling, cross-channel measurement, and Unified ID 2.0 integration, maintaining its position as the world's leading independent DSP serving premium programmatic brand advertisers.

-

2025: Amazon Ads expanded its DSP capabilities with enhanced retail audience signal integration, enabling consumer goods advertisers to activate Amazon's first-party shopper data across programmatic inventory beyond Amazon-owned properties for the first time at scale.

-

2025: Magnite extended its streaming media programmatic SSP with enhanced CTV supply curation and audience verification capabilities, supporting the growing programmatic CTV market by improving inventory transparency and brand safety assurance for premium streaming inventory buyers.

Programmatic Advertising Market Key Players

-

The Trade Desk Inc.

-

Google LLC (DV360, Google Ads)

-

Meta Platforms Inc. (Meta Ads Manager)

-

Amazon Advertising (Amazon DSP)

-

Adobe Inc. (Adobe Advertising Cloud)

-

Microsoft Corporation (Microsoft Advertising)

-

AppNexus (Xandr by Microsoft)

-

Magnite Inc.

-

PubMatic Inc.

-

Index Exchange Inc.

-

OpenX Technologies Inc.

-

Criteo SA

-

LiveRamp Holdings Inc.

-

DoubleVerify Holdings Inc.

-

Integral Ad Science Inc.

-

Verizon Media (Yahoo DSP)

-

Basis Technologies Inc.

-

StackAdapt Inc.

-

Simpli.fi LLC

-

NextRoll Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1026.54 Billion |

| Market Size by 2035 | USD 8,276.26 Billion |

| CAGR | CAGR of 23.21% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Ad Format (Video, Display, Audio, Native, Others) • By Device Type (Mobile and Tablets, Desktop, Connected TV, Others) • By Transaction Model (Real-Time Bidding, Programmatic Direct, Private Marketplace) • By End-User Industry (Retail and Consumer Goods, BFSI, Media and Entertainment, Telecom, Healthcare, Automotive, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | The Trade Desk Inc., Google LLC (DV360, Google Ads), Meta Platforms Inc. (Meta Ads Manager), Amazon Advertising (Amazon DSP), Adobe Inc. (Adobe Advertising Cloud), Microsoft Corporation (Microsoft Advertising), AppNexus (Xandr by Microsoft), Magnite Inc., PubMatic Inc., Index Exchange Inc., OpenX Technologies Inc., Criteo SA, LiveRamp Holdings Inc., DoubleVerify Holdings Inc., Integral Ad Science Inc., Verizon Media (Yahoo DSP), Basis Technologies Inc., StackAdapt Inc., Simpli.fi LLC, NextRoll Inc. |

Get in Touch