Mainframe Modernization Market Report Scope & Overview

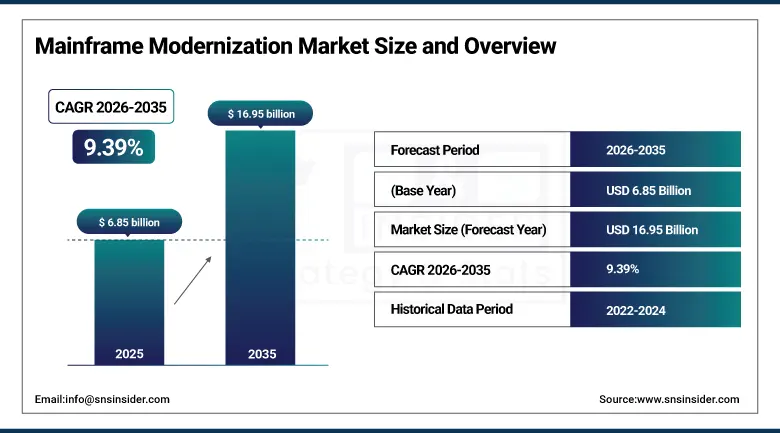

The Mainframe Modernization Market was valued at USD 6.85 billion in 2025 and is expected to reach USD 16.95 billion by 2035, growing at a CAGR of 9.39% from 2026–2035.

The global mainframe modernization market is at an inflection point as decades of accumulated technical debt in legacy computing infrastructure collides with the immediacy of cloud-native digital transformation requirements, generative AI integration imperatives, and the talent scarcity crisis created by the retirement of the COBOL-literate workforce that has historically maintained mainframe application estates across the world’s largest financial institutions, government agencies, healthcare systems, and retail conglomerates. Mainframes process an estimated 30 billion transactions per day globally, underpinning virtually every major financial exchange, airline reservation, insurance claims processing operation, and government benefit disbursement system in existence, which means modernization programmes are not optional infrastructure refreshes but existential risk management exercises for organisations whose operational continuity depends on systems whose age, proprietary vendor lock-in, and specialist skill dependencies are creating compounding vulnerabilities as the global technology landscape accelerates away from the architectural assumptions on which mainframe-centric operating models were built. The market’s commercial landscape is being shaped by the progressive maturity of cloud migration tooling, AI-assisted code analysis and translation platforms, and hybrid cloud architectures that allow organisations to pursue modernization incrementally rather than through the risky big-bang replacement programmes that earlier migration approaches required, substantially expanding the population of organisations willing to initiate modernization journeys that their risk appetite previously prevented.

IBM’s March 2025 generative AI-powered mainframe code conversion announcement, demonstrating automated COBOL-to-Java translation that compresses multi-year manual migration programmes into months through AI-assisted code analysis, dependency mapping, and automated refactoring, represents a genuine commercial breakthrough that is reducing the risk, cost, and duration barriers that have historically prevented organisations from initiating large-scale mainframe modernization despite recognising the strategic necessity of reducing their legacy dependency.

Market Size and Forecast

- Market Size In 2026E: USD 7.49 Billion

- Market Size By 2035: USD 16.95 Billion

- CAGR: 9.39% From 2026 To 2035

- Fastest Growing Region: Asia Pacific

- Largest Region: North America

To Get more information on Mainframe Modernization Market - Request Free Sample Report

Mainframe Modernization Market Trends

- Accelerating deployment of AI-powered code analysis, automated COBOL-to-Java translation, and intelligent dependency mapping tools that compress multi-year manual mainframe migration programmes into dramatically shorter timelines by automating the discovery, documentation, and translation of legacy application code at a throughput and accuracy level that human developer-led migration approaches cannot achieve at comparable cost or speed, fundamentally improving the economic and risk calculus of large-scale mainframe modernization programmes.

- Growing adoption of hybrid cloud architectures that enable progressive mainframe workload migration by connecting mainframe environments to public cloud platforms through secure API layers, allowing organisations to move individual application components and data streams to cloud environments while retaining mission-critical core processing on mainframe infrastructure until sufficient confidence in cloud-native equivalents is established.

- Rising enterprise interest in containers and microservices as the target architecture for modernized mainframe workloads, as the decomposition of monolithic COBOL and assembler application codebases into independently deployable microservices running on Kubernetes platforms enables the development agility, independent scaling, and cloud provider optionality that mainframe-centric architectures fundamentally cannot provide regardless of hardware investment.

- Growing regulatory compliance pressure in BFSI and healthcare sectors whose ageing mainframe application estates contain the core systems of record for regulatory reporting, transaction processing, and patient data management, creating both the compliance risk that makes modernization urgent and the regulatory scrutiny of data migration processes that makes careful, audited, and reversible modernization approaches essential for regulated entities.

- Expanding talent market crisis as the global population of COBOL-literate developers ages toward retirement faster than educational institutions and enterprises are training replacements, creating an escalating operational risk for organisations whose mainframe application maintenance skill dependency is becoming an increasingly expensive and fragile competitive liability as specialist availability declines and compensation expectations rise.

U.S. Mainframe Modernization Market Outlook

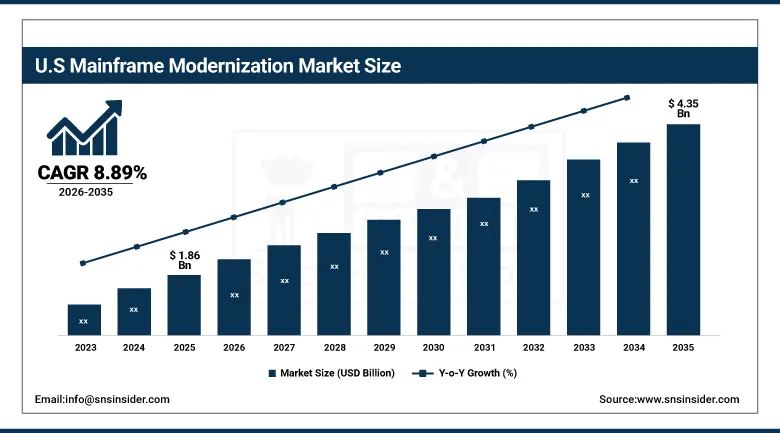

The U.S. mainframe modernization market was valued at approximately USD 1.86 billion in 2025 and is expected to reach approximately USD 4.35 billion by 2035, growing at a CAGR of 8.89%, driven by the world’s largest concentration of mainframe-dependent financial institutions, government agencies, and healthcare systems whose combined legacy application estate represents the most commercially valuable and technically complex mainframe modernization opportunity in the global market, attracting the deepest ecosystem of modernization solution providers, systems integrators, and specialist consulting firms.

The United States mainframe modernization market is defined by the extraordinary scale and commercial sophistication of its BFSI sector, which hosts the world’s largest mainframe-dependent banks including JPMorgan Chase, Bank of America, Wells Fargo, and Citibank, whose combined mainframe estate processes the majority of U.S. domestic financial transactions and whose modernization programmes represent multi-billion dollar investment commitments that are reshaping the commercial landscape for IBM, Kyndryl, Broadcom, and specialist modernization vendors competing for programme engagement. The U.S. government represents a distinctive and growing modernization demand category, as federal agencies including the Social Security Administration, IRS, and Department of Defense are operating mainframe systems whose age and maintenance cost burden have been identified by the Government Accountability Office as significant operational risks warranting prioritised modernization investment.

The Department of Homeland Security’s 2025 report identifying mainframe modernization as a top-ten federal cybersecurity priority has elevated the national security dimension of legacy system dependency above the operational efficiency framing that previously dominated federal IT modernization discussions, creating bipartisan policy consensus around increased modernization appropriations that is expanding the government vertical’s contribution to total U.S. modernization market demand.

Mainframe Modernization Market Segment Analysis

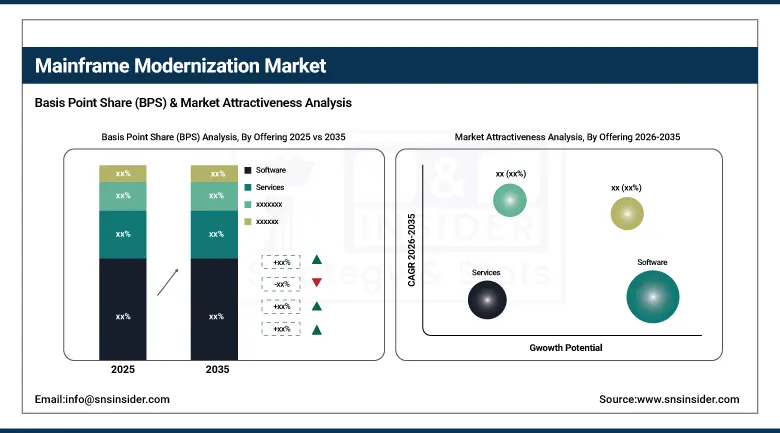

- By offering, software dominated with approximately 59% revenue share in 2025 as enterprises prioritise modernization platforms offering migration, integration, and application reengineering capabilities; services is the fastest-growing offering segment at a CAGR of approximately 10.64% driven by enterprise demand for consulting, implementation, and managed services that minimise migration risks and provide specialist expertise that internal teams cannot rapidly develop.

- By modernization type, rehosting led with approximately 30% share in 2025 as enterprises prefer cost-effective approaches migrating workloads to cloud or modern environments without major code changes; rearchitecting is the fastest-growing type at a CAGR of approximately 11.15% as organisations pursue deeper architectural transformation delivering the development agility and cloud-native operating model that rehosting alone cannot achieve.

- By organization size, large enterprises dominated with approximately 70% share in 2025 due to heavy reliance on mission-critical mainframes for banking, insurance, and government operations; small and medium enterprises are the fastest-growing organisation size at a CAGR of approximately 11.50% as cloud-based modernization platforms make legacy transformation accessible at investment levels fitting SME constraints.

- By vertical, BFSI led with approximately 32% share in 2025 driven by extraordinary mainframe dependency for core banking, payment processing, and regulatory compliance; healthcare is the fastest-growing vertical at a CAGR of approximately 12.09% as providers modernize legacy systems to enable digital health integration, EHR interoperability, and telehealth platform connectivity.

Software Leads Offering Segment, Services Grows Fastest

Software retained the dominant offering position with approximately 59% of the mainframe modernization market in 2025, reflecting enterprises’ prioritisation of the automated migration, code analysis, testing, and application reengineering platforms that make large-scale legacy workload transformation technically feasible without the prohibitive manual developer investment that unassisted migration programmes historically required. The software segment encompasses a growing portfolio of AI-powered capabilities including automated COBOL and assembler code scanning and documentation tools, dependency graph generation platforms mapping application-to-application interactions across decades of accumulated integration points, automated code translation engines converting legacy language code to Java or Python with varying degrees of structural fidelity, and testing automation platforms that validate functional equivalence between legacy and modernized application versions. IBM’s watsonx Code Assistant for Z, Broadcom’s Application Performance Analyzer, and Micro Focus’s Enterprise Suite represent the established enterprise software leaders, while emerging specialist vendors including CloudFrame, TSRI, and Mechanical Orchard are competing with purpose-built AI-powered conversion tools demonstrating higher automated translation fidelity for specific language and architecture patterns.

Services is the fastest-growing offering at a CAGR of approximately 10.64% through 2035, driven by enterprises’ recognition that mainframe modernization is fundamentally an organisational transformation programme requiring deep mainframe domain expertise, cloud architecture design authority, application testing strategy, change management, and risk mitigation planning that software platforms alone cannot provide without human expert guidance. The managed services component within the broader services segment is growing particularly rapidly as organisations seek to transfer ongoing mainframe modernization execution responsibility to specialist service providers including Kyndryl, Accenture, Capgemini, and Cognizant whose dedicated modernization practices combine proprietary tooling, factory-based delivery models, and deep COBOL architecture expertise with the financial capacity to absorb programme risk through outcome-based commercial arrangements that align provider incentives with client modernization success.

Rehosting Leads Modernization Type, Rearchitecting Grows Fastest

Rehosting retained the leading modernization type position with approximately 30% share in 2025, reflecting the commercial reality that lift-and-shift migration to cloud-compatible runtime environments represents the lowest-risk, fastest-execution, and most immediately cost-reducing modernization approach available to organisations seeking to reduce mainframe hardware and software licensing costs without the application code re-engineering investment that deeper transformation requires. Rehosting’s dominance reflects both its practicality as a first modernization step for organisations with limited internal cloud expertise and its genuine commercial value in reducing IBM zSeries hardware refresh, software licence, and operational staff costs that make mainframe total cost of ownership burdensome, even if rehosting alone does not deliver the development agility and cloud-native operational model that more ambitious approaches ultimately achieve.

Rearchitecting is the fastest-growing modernization type at a CAGR of approximately 11.15% through 2035, propelled by the growing proportion of enterprises that have completed initial rehosting phases and are now pursuing the deeper architectural transformation required to achieve genuine cloud-native agility, microservices decomposition, and the ability to leverage modern DevOps tooling and development frameworks that fundamentally change how application teams build, test, and deploy new features. The rearchitecting segment is specifically accelerated by AI-powered code transformation tools including IBM’s watsonx Code Assistant for Z and emerging specialist platforms that automate significant portions of the structural refactoring process, making conversion of monolithic COBOL applications into independently deployable Java or Python services economically viable at application sizes that would have required unacceptable manual developer investment without AI assistance.

BFSI Dominates Vertical Segment, Healthcare Grows Fastest

BFSI retained the dominant vertical position with approximately 32% of the mainframe modernization market in 2025, a dominance reflecting the financial services sector’s extraordinary historical investment in mainframe infrastructure for core banking, payment processing, card transaction authorisation, regulatory reporting, and risk management workloads whose transaction volumes, reliability requirements, and regulatory auditability standards historically made mainframe the only commercially viable platform architecture. The BFSI sector’s modernization motivation is equally strong on both cost and capability dimensions: on cost, IBM’s MLC pricing that scales with workload volume is consuming growing proportions of IT budgets at major banks as digital transaction volumes grow; on capability, mainframe architectures’ inability to natively support real-time API integration, event-driven processing, and AI model inference is creating competitive disadvantage relative to fintech challengers built on cloud-native foundations.

Healthcare is the fastest-growing vertical at a CAGR of approximately 12.09% through 2035, propelled by the sector’s urgent need to modernize aging administrative and clinical information systems that cannot support electronic health record interoperability, telehealth platform integration, population health analytics, and AI-powered clinical decision support that contemporary healthcare delivery models demand. The U.S. healthcare sector’s particular modernization motivation is driven by CMS regulatory requirements for interoperability and patient data access under the 21st Century Cures Act, which mandate API-based health data exchange capabilities that mainframe-centric systems cannot natively provide, creating both a regulatory compliance driver and a quality improvement imperative for healthcare system CIOs whose legacy application estates are preventing compliance with federal interoperability standards.

Regional Analysis

|

Region |

Major Country |

Share Within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

61.7% |

|

Middle East & Africa |

Saudi Arabia |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Mainframe Modernization Market Insights

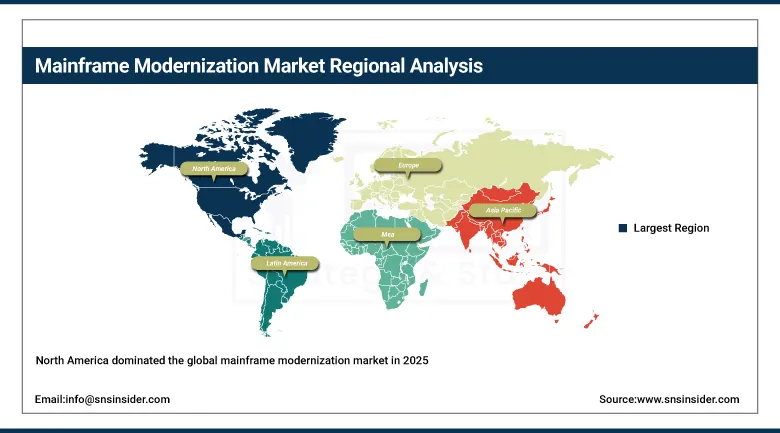

North America dominated the global mainframe modernization market in 2025 with the United States accounting for approximately 87.4% of North American revenues, driven by the world’s deepest concentration of mainframe-dependent Fortune 500 financial institutions, government agencies at federal and state levels, and healthcare systems whose combined legacy application estate represents the most commercially valuable modernization opportunity in the global market. The U.S. market benefits from the world’s most developed mainframe modernization professional services ecosystem, with Kyndryl’s dedicated mainframe modernization practice, Accenture’s Federal Services mainframe capability, and dozens of specialist boutique firms collectively providing the expertise depth required for the complex multi-year programmes that major bank and government agency modernization represent. Canada contributes approximately 12.6% of North American revenues through a financial services sector whose major banks including RBC, TD, and Scotiabank are executing cloud migration programmes that include mainframe workload modernization as a component of broader digital transformation strategies.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Mainframe Modernization Market Insights

Europe is the world’s second-largest mainframe modernization market, characterised by a sophisticated and technically conservative financial services and government sector whose large mainframe estates in Germany, the United Kingdom, France, and the Benelux countries represent the primary demand pool for modernization solutions. Germany accounts for approximately 22.3% of European revenues as the region’s largest national market, where major banks including Deutsche Bank and Commerzbank, large insurance groups, and federal government agencies are executing modernization programmes that reflect German IT’s characteristic emphasis on risk management rigour and incremental migration validation. The EU’s Digital Operational Resilience Act requirements are creating additional compliance motivation for European BFSI organisations whose mainframe dependency on IBM creates concentration risk exposures that DORA’s IT service provider management requirements are pushing financial institutions to address through diversification and modernization programmes.

Asia Pacific Mainframe Modernization Market Insights

Asia Pacific is the fastest-growing regional market for mainframe modernization, driven by rapidly expanding financial services sectors in China, India, Japan, Australia, and Southeast Asian markets where the combination of growing transaction volumes, digital banking competitive pressure, and increasing cloud infrastructure adoption is creating modernization demand among a regional banking and insurance sector whose mainframe dependency is growing in absolute commercial value as Asia Pacific financial markets expand. China accounts for approximately 61.7% of Asia Pacific revenues through the modernization programmes of major state-owned banks including ICBC, China Construction Bank, and Bank of China, whose legacy system modernization is a stated component of China’s broader financial technology infrastructure agenda. India represents the most commercially dynamic secondary market, as the country’s large IT services industry’s COBOL and mainframe expertise is being applied to both domestic bank modernization programmes and offshore delivery for North American and European clients.

Latin America and MEA Mainframe Modernization Market Insights

Latin America and the Middle East and Africa are emerging mainframe modernization markets where the rapid digitalisation of financial services, government operations, and telecommunications sectors is creating growing pressure to modernize the legacy mainframe systems underpinning core processing in the largest financial institutions and government agencies. Brazil accounts for approximately 44.2% of Latin American revenues through the modernization programmes of major Brazilian banks including Itau Unibanco, Bradesco, and Banco do Brasil, whose cloud migration strategies are progressively incorporating mainframe workload modernization as a component of broader digital banking transformation. Saudi Arabia leads Middle East and Africa revenues at approximately 38.4% of the regional total, driven by Vision 2030’s financial sector digitalisation agenda creating modernization investment across Saudi commercial banks and government ministries with legacy system estates.

Market Dynamics

Growth Drivers: Escalating mainframe maintenance cost burden and COBOL talent scarcity driving modernization urgency, AI-powered code translation reducing migration risk and cost, and cloud architecture requirements that legacy systems cannot natively meet

The primary structural growth drivers for the mainframe modernization market are the convergent pressures of escalating mainframe total cost of ownership, accelerating talent scarcity as the COBOL developer population ages toward retirement, and the growing competitive disadvantage of being unable to deploy modern cloud-native capabilities including real-time API integration, AI model inference, and DevOps deployment velocity on infrastructure architectures never designed to support these operational models. The IBM MLC pricing model’s volume-correlated licence cost structure creates a compounding financial pressure as digital transaction volumes grow, with major banks reporting annual mainframe software licence cost increases consuming growing proportions of IT budgets and creating a direct financial motivation for reducing mainframe compute consumption through workload migration that operates independently of strategic cloud adoption goals. AI’s role in reducing modernization risk is transforming enterprise willingness to initiate programmes: when COBOL-to-Java migration required proportionally larger manual developer investment with proportionally higher technical risk, risk-averse organisations deferred programmes indefinitely; as AI-assisted automated translation demonstrates reliable fidelity at scale, the risk-adjusted cost-benefit of initiating modernization improves sufficiently to convert previously reluctant organisations into active programme buyers.

Restraints: Mission-critical application risk aversion delaying programme initiation, organisational change management complexity of multi-year transformation programmes, and data migration complexity for decades of accumulated structured and unstructured mainframe data

A significant restraint on the mainframe modernization market is the profound organisational risk aversion surrounding the systems of record at the heart of enterprise operations, where the cost of even a brief operational disruption during migration significantly exceeds the annual savings that modernization delivers, creating a risk calculus that favours programme delay or extreme caution in execution that prolongs programme timelines and increases total programme investment. The organisational change management complexity of mainframe modernization programmes that simultaneously touch application code, database architecture, integration patterns, operational procedures, regulatory compliance frameworks, and development team skill profiles represents an execution challenge that many organisations underestimate, with the result that programmes initiated with confidence in their technical feasibility encounter cultural and stakeholder management obstacles that extend timelines beyond initial estimates.

Opportunities: AI code conversion platform maturation enabling automated large-scale migration, government-mandated modernization investment creating public sector programme pipeline, and cloud vendor incentive programmes reducing migration financial barriers

The AI code conversion platform opportunity is the most commercially transformative near-term development in the mainframe modernization market, as the demonstrable performance of tools including IBM’s watsonx Code Assistant for Z in automating COBOL analysis and Java conversion at enterprise banking system scale is creating a genuine shift in the risk and cost parameters that define programme feasibility, expanding the population of organisations for whom initiating a modernization programme is commercially rational from the subset with the highest cost pressure to virtually every mainframe-dependent enterprise whose strategic direction includes cloud adoption, AI integration, or development agility improvement.

Recent Developments

- 2025: IBM announced its watsonx Code Assistant for Z with enhanced generative AI capabilities that automate COBOL-to-Java code conversion at scale, demonstrating the ability to analyse and document millions of lines of legacy code while generating functionally equivalent Java equivalents with reduced manual developer review requirements.

- 2025: Kyndryl expanded its mainframe modernization practice with new AI-enhanced migration factory capabilities combining proprietary code analysis tooling with structured delivery methodology and cloud partner integrations across AWS, Azure, and Google Cloud, enabling enterprise clients to access factory-based programme delivery compressing timelines and improving quality consistency.

- 2025: Broadcom introduced updated modernization capabilities within its Mainframe Software Portfolio, adding AI-assisted application performance analysis and workload optimisation tools that help enterprises identify the most commercially viable workloads for cloud migration based on actual usage patterns, dependencies, and cost contribution.

Mainframe Modernization Market Key Players are:

- IBM Corporation

- Kyndryl Holdings Inc.

- Broadcom Inc.

- Micro Focus International plc (OpenText)

- Accenture plc

- Cognizant Technology Solutions

- Capgemini SE

- DXC Technology

- Infosys Limited

- Tata Consultancy Services

- Wipro Limited

- HCL Technologies

- Amazon Web Services (AWS)

- Microsoft Azure

- Rocket Software Inc.

- Fujitsu Limited

- CloudFrame Inc.

- TSRI Inc.

- TmaxSoft Co., Ltd.

- Mechanical Orchard

Mainframe Modernization Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 6.85 Billion |

| Market Size by 2035 | USD 16.95 Billion |

| CAGR | CAGR of 9.39% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Offering (Software, Services) •By Modernization Type (Rehosting, Refactoring, Rearchitecting, Replatforming, Others) •By Organization Size (Large Enterprises, Small & Medium Enterprises) •By Vertical (BFSI, Healthcare, IT & Telecom, Government, Retail & Commerce, Media & Entertainment, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | IBM Corporation, Kyndryl Holdings Inc., Broadcom Inc., Micro Focus International plc (OpenText), Accenture plc, Cognizant Technology Solutions, Capgemini SE, DXC Technology, Infosys Limited, Tata Consultancy Services, Wipro Limited, HCL Technologies, Amazon Web Services (AWS), Microsoft Azure, Rocket Software Inc., Fujitsu Limited, CloudFrame Inc., TSRI Inc., TmaxSoft Co., Ltd., and Mechanical Orchard |

Frequently Asked Questions

Get in Touch