Psychedelic Drugs Market Report Scope and Overview:

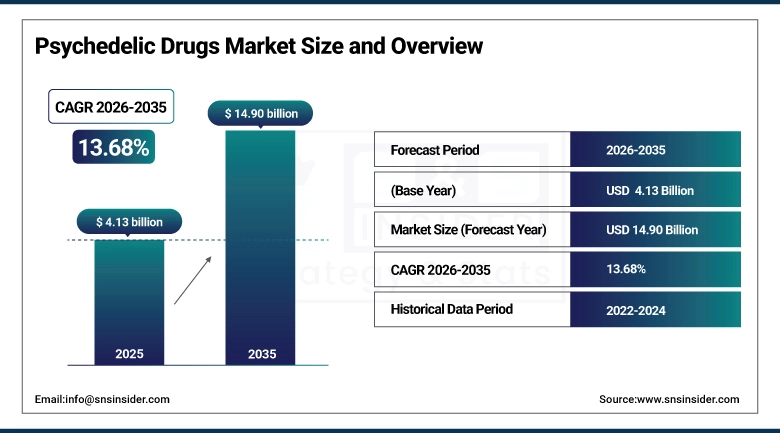

The Psychedelic Drugs Market was estimated at USD 4.13 billion in 2025 and is expected to reach USD 14.90 billion by 2035 and grow at a CAGR of 13.68% over the forecast period of 2026-2035.

Few areas within global medicine have undergone as dramatic a transformation as psychedelic assisted therapy over the past decade. Once dismissed as a relic of counterculture experimentation, compounds such as psilocybin, ketamine, MDMA, and LSD are now at the center of one of the most energetically funded and scientifically productive waves of psychiatric research in modern history. The global Psychedelic Drugs Market is expanding rapidly because the underlying need it addresses - effective treatment for conditions like treatment resistant depression, post-traumatic stress disorder, severe anxiety, and substance use disorders - remains one of the most unmet in all of healthcare. Traditional pharmacological options have not meaningfully improved outcomes for hundreds of millions of people living with these conditions, and that gap is precisely what is driving policymakers, investors, clinicians, and patients toward psychedelic medicine as a credible next frontier.

The WHO estimates that over 970 million people worldwide live with a mental or substance use disorder. Of those, a substantial proportion fail to achieve adequate relief from currently approved medications or psychotherapy. That reality has created both the moral urgency and the commercial rationale for the surge in psychedelic drug research now visible across North America, Europe, Australia, and rapidly emerging markets in Asia. Regulatory agencies have taken notice. The U.S. FDA has awarded Breakthrough Therapy designation to psilocybin and MDMA candidates, compressing trial timelines and signaling institutional acceptance that would have seemed inconceivable a generation ago.

Market Size and Forecast

-

Market Size in 2025: USD 4.13 Billion

-

Market Size by 2035: USD 14.90 Billion

-

CAGR: 13.68% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026 to 2035

-

Historical Data: 2022 to 2024

To Get more information on Psychedelic Drugs Market - Request Free Sample Report

Psychedelic Drugs Market Trends

-

Rapidly growing number of global clinical trials focused on psychedelic drugs, with the total number surpassing 400 trials in progress at the current time, registered by authorities in North America, Europe, and Asia Pacific.

-

Australia emerges as the world’s first officially legalized jurisdiction for MDMA and psilocybin therapies, an event that is currently receiving keen attention among regulators in the UK, Canada, and European Union countries.

-

Increasing trend of investment capital being channeled to psychedelic biotech companies, resulting in sector investments exceeding billions of dollars in cumulative value.

-

The proliferation of ketamine infusion centers and psychedelic therapy clinics in key metro markets in both the United States and Canada.

-

The development of technologies integrating with psychedelic therapy sessions, such as remote monitoring services, biofeedback devices, and AI guided session preparations.

-

Military and veteran healthcare organizations becoming increasingly interested in psychedelic treatments for PTSD suffered due to military combat situations, driven by promising initial findings from VA related research projects.

-

An emerging public and policy consensus towards psychedelic decriminalization laws, with multiple states in the United States adopting legal frameworks where there are no criminal penalties for personal usage of psychedelics.

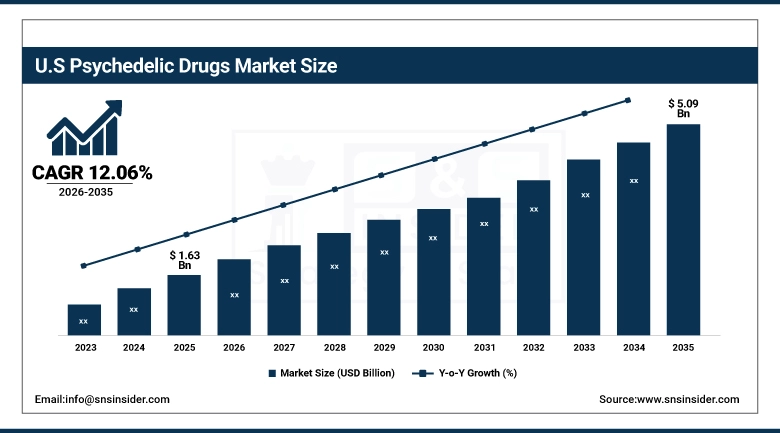

The U.S. Psychedelic Drugs Market was valued at USD 1.63 billion in 2025 and is expected to reach USD 5.09 billion by 2035, registering a CAGR of 12.06% during 2026 to 2035.

The United States sits at the epicenter of the global psychedelic medicine movement. It is home to the highest concentration of active clinical trials, the most heavily funded psychedelic biotech companies, and the most developed network of private ketamine and emerging psilocybin therapy clinics in the world. The FDA's willingness to grant Breakthrough Therapy designations to multiple psychedelic compounds has been a landmark development, not just for the U.S. market, but for the global trajectory of psychedelic medicine as a category. American academic institutions - including NYU, Johns Hopkins, and the University of California system - have established dedicated psychedelic research centers that are generating a steady stream of high-quality clinical evidence supporting therapeutic applications across depression, addiction, end of life anxiety, and eating disorders.

State level legislative activity has added another dimension to U.S. market development. Oregon became the first state to establish a regulated psilocybin services framework, and Colorado followed with a broader natural medicine program. These programs, while still nascent, are creating the world's first regulated non clinical psychedelic therapy infrastructure and providing important real-world data that will inform both federal regulatory pathways and international policy development. Insurance coverage discussions are also beginning, with employer sponsored mental health platforms showing early interest in subsidizing psychedelic therapy access for eligible employees.

Psychedelic Drugs Market Segment Analysis

-

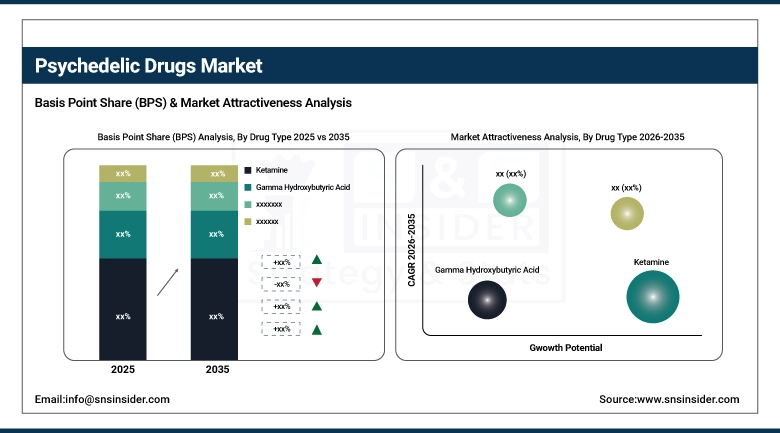

Based on Drug Type, Ketamine accounted for the largest market share of approximately 42% in 2025 due to its established FDA approved status. Psilocybin is expected to register the fastest CAGR through 2035.

-

Based on Source, Synthetic compounds accounted for the largest market share of approximately 55% in 2025 due to scalability and regulatory compatibility. Naturally derived compounds are gaining ground as research into plant medicine expands.

-

Based on Application, Treatment Resistant Depression accounted for the largest market share in 2025. PTSD is expected to be the fastest growing application segment through 2035.

-

Based on Route of Administration, Intravenous accounted for the largest share in 2025 given ketamine infusion clinic prevalence. Intranasal and oral routes are expected to grow rapidly as new drug formulations receive approval.

-

Based on End Use Setting, Specialized Psychedelic Clinics accounted for the largest share in 2025. Research and Academic Institutes are expected to register the fastest CAGR, driven by expanding clinical pipeline activity.

By Drug Type, Ketamine segment dominates the Psychedelic Drugs Market, Psilocybin segment expected to grow fastest

Ketamine holds the commanding share of the psychedelic drugs market in 2025, accounting for approximately 42% of total revenue. Its position rests on a foundation that no other psychedelic compound currently enjoys: formal FDA approval. Esketamine, the nasal spray formulation developed for treatment resistant depression, entered the U.S. market in 2019 and legitimized an entire category overnight. Since then, the number of ketamine infusion centers in North America has grown from a few hundred to several thousand, serving patients who have exhausted conventional antidepressant regimens. Ketamine's rapid onset of action, often producing measurable mood improvements within hours rather than the weeks required by SSRIs, has made it particularly compelling for patients in acute psychiatric distress. Its established safety profile in anesthetic medicine provides an additional layer of clinical familiarity that accelerates adoption in outpatient psychiatric settings.

Psilocybin is positioned to record the fastest CAGR in the drug type segment from 2026 through 2035. The data emerging from Phase 2 and Phase 3 trials across multiple indications - treatment resistant depression, major depressive disorder, alcohol use disorder, and end of life existential anxiety - has been consistently impressive, with some studies reporting remission rates that would be extraordinary by any conventional psychiatric standard. COMPASS Pathways has reported statistically significant improvements in depression severity scores that have attracted attention far beyond the psychedelic research community. Australia's formal scheduling of psilocybin for therapeutic use in 2023 created the world's first national precedent for its medical availability, and regulatory dossiers are advancing in the UK, Canada, and the EU. As commercial approval materializes in these markets, psilocybin revenue is expected to scale rapidly.

By Source, Synthetic segment dominates the Psychedelic Drugs Market, Naturally Derived segment expected to grow rapidly

Synthetic psychedelic compounds held approximately 55% of the market in 2025 and represent the dominant source category for clinically developed psychedelic medicine. Ketamine, MDMA, and LSD are all synthetically produced, and their standardized chemical consistency makes them far more amenable to the rigorous quality control, pharmacokinetic profiling, and regulatory dossier requirements expected by agencies like the FDA, EMA, and Health Canada. Pharmaceutical companies operating in this space rely on synthetic production not merely for practical reasons, but because the reproducibility of synthetic compounds is a prerequisite for the clinical trial standards that translate into market approval. The scalability of synthetic manufacturing also allows production volumes to be expanded in line with anticipated commercialization demand, which is a critical operational advantage as pipeline candidates approach approval.

Naturally derived compounds, including plant based psilocybin, mescaline from the peyote cactus, and DMT derived from ayahuasca plant sources, are gaining growing research interest and cultural legitimacy - particularly in the context of indigenous healing traditions that are increasingly recognized as valid therapeutic frameworks. Oregon's and Colorado's regulated natural medicine programs are creating formal infrastructure for the delivery of naturally sourced psychedelic experiences under supervised clinical and wellness settings. As quality standardization and regulatory frameworks for natural compounds mature, this segment is expected to register meaningful growth through the forecast period, particularly in markets with more permissive frameworks for plant medicine.

By Application, Treatment Resistant Depression dominates the Psychedelic Drugs Market, PTSD segment expected to grow fastest

Treatment resistant depression represents the largest application segment in the psychedelic drugs market in 2025, a position it occupies by virtue of both epidemiological magnitude and clinical evidence depth. An estimated 100 million people globally are classified as having treatment resistant depression, meaning they have failed to achieve adequate response from at least two adequately dosed antidepressant regimens. This is the patient population for whom the urgency of new options is most acute, and the one for which the most advanced psychedelic clinical programs have been designed. The ketamine and esketamine commercial programs, the COMPASS Pathways psilocybin trials, and the Johnson and Johnson Spravato platform are all fundamentally oriented around this indication.

Post traumatic stress disorder is the fastest growing application segment, driven by the exceptional clinical signal that MDMA has demonstrated in Phase 3 trials. The MAPS sponsored MDMA assisted therapy program generated response rates in PTSD patients that clinical psychiatry has not historically achieved with any available treatment. The veteran and military healthcare community in North America has been particularly engaged with this research, given the scale of combat related PTSD in this population and the limitations of existing pharmacological options. Even though the FDA declined initial approval in 2024 pending additional data, the program continues advancing, and multiple countries are watching the regulatory outcome closely as they assess their own frameworks for MDMA in psychiatric medicine.

By End Use Setting, Specialized Psychedelic Clinics hold the largest share, Research and Academic Institutes expected to grow fastest

The development of specialized psychedelic clinics is the most popular end-use application for psychedelics in 2025, making up the majority of the revenue in this industry. This is consistent with the current reality of delivering psychedelics in medicinal applications; namely, most psychedelic treatments currently on the market require a more controlled environment, integration, and supervision by professional therapists in private clinics. The ketamine treatment clinic business model, which has existed for years already, paved the way for other models being replicated by psilocybin and MDMA treatment clinics across the country. Companies such as Numinus, Field Trip, and other independent entities have formed networks of clinics across the country.

Research and academic institutes are expected to grow at the fastest CAGR through 2035. The sheer volume of active clinical trials, the expansion of dedicated psychedelic research programs at universities in the U.S., UK, Netherlands, and Australia, and the growing pipeline of investigational new drug applications being developed at academic centers collectively underpin this trajectory. Government funded research into psychedelics at institutions like Johns Hopkins, NYU, and Imperial College London is producing data that informs both regulatory submissions and the broader scientific community, creating a feedback loop that accelerates commercialization timelines.

Regional Insights

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

~79% |

|

Europe |

Germany |

~27% |

|

Asia Pacific |

Australia |

~38% |

|

Middle East and Africa |

Israel |

~29% |

|

Latin America |

Brazil |

~44% |

North America Psychedelic Drugs Market Insights

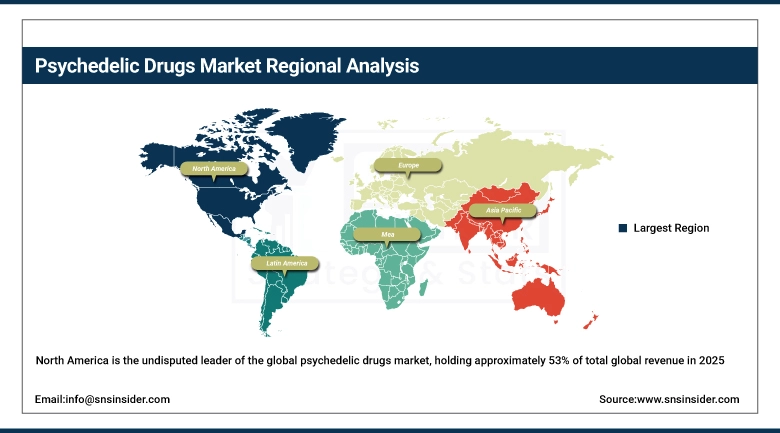

North America is the undisputed leader of the global psychedelic drugs market, holding approximately 53% of total global revenue in 2025. The United States accounts for the overwhelming majority of this share. What makes the U.S. particularly dominant is not just market size but the concentration of enabling infrastructure: the highest number of FDA approved and IND authorized clinical trials, the deepest pool of psychedelic biotech venture funding, the largest network of operating ketamine therapy clinics, and the most active legislative environment for psychedelic decriminalization and therapeutic framework development. Canada has been an important contributor as well, with Health Canada granting an increasing number of Section 56 exemptions allowing seriously ill patients to access psilocybin therapy outside of formal clinical trials.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Psychedelic Drugs Market Insights

Asia Pacific is expected to register the highest CAGR among all regions from 2026 through 2035. Australia has already distinguished itself as the global regulatory pioneer, becoming the first country in the world to formally schedule MDMA and psilocybin as controlled substances approved for therapeutic use in 2023. Australian psychiatric clinics offering these therapies represent a first of their kind commercial model that is being closely studied by regulators and operators in the UK, Canada, and continental Europe. Japan, South Korea, and Singapore are at earlier stages of research and policy development, but growing rates of depression, anxiety, and burnout in these markets are creating strong public health rationale for exploring novel treatment options. India and China represent large potential markets where mental health awareness is rising rapidly alongside economic development.

Europe Psychedelic Drugs Market Insights

Europe holds a significant share of the global psychedelic drugs market, with the United Kingdom, Germany, the Netherlands, and Switzerland as the leading national markets for both research and early commercial activity. The UK's Medicines and Healthcare products Regulatory Agency has granted several psychedelic drug candidates Promising Innovative Medicine designation, a precursor to an accelerated review pathway. Clinical research at institutions like Imperial College London and King's College London is producing internationally recognized evidence on psilocybin's efficacy in depression and addiction. The Netherlands has a long standing legal framework for psilocybin truffles that has enabled a growing network of therapeutic retreat centers operating in a regulatory gray zone that is increasingly attracting international clients seeking legal psychedelic experiences.

Middle East and Africa and Latin America Psychedelic Drugs Market Insights

The Middle East and Africa and Latin America regions represent earlier stage but genuinely promising markets for psychedelic medicine. Israel has been particularly notable in the global context, with its national health system authorizing compassionate use of MDMA and psilocybin for specific patient populations and with Ben Gurion University conducting active psychedelic research. Brazil has a unique cultural and legal relationship with ayahuasca, a DMT containing brew with deep indigenous roots that is legally consumed in religious contexts. This tradition is increasingly attracting scientific research and clinical interest, with Brazilian researchers publishing peer reviewed studies on ayahuasca's antidepressant properties. Both regions are expected to grow meaningfully through 2035 as global regulatory norms evolve and healthcare systems engage more formally with psychedelic medicine.

Psychedelic Drugs Market Growth Drivers:

Surging global mental health burden and the failure of conventional treatments driving urgent demand for psychedelic medicine

The single most powerful structural driver of the psychedelic drugs market is a healthcare system reality that conventional psychiatry has struggled to solve: the enormous global burden of mental illness and the inadequacy of current treatments for a large proportion of patients. The WHO ranks depression as a leading cause of disability globally, and rates of anxiety, PTSD, addiction, and eating disorders are rising in virtually every major market. The pharmacological tools available to clinicians - primarily SSRIs, SNRIs, benzodiazepines, and antipsychotics - have not changed fundamentally in decades, and for the populations most severely affected, their effectiveness is modest at best. This is the unmet need that psychedelic medicine is being developed to address, and it is large enough to sustain a market growing at double digit rates for a decade or more. Every clinical trial that reports positive outcomes adds to the evidence base that is incrementally shifting clinical practice, regulatory interpretation, and investor confidence in favor of psychedelic therapeutics as a legitimate and scalable treatment category.

Industry and academic data consistently show that for patients with treatment resistant depression, the response rates achieved by ketamine and emerging psilocybin protocols significantly exceed those of any available pharmacological alternative. This efficacy signal is the foundation upon which an entire commercial ecosystem of clinics, insurers, digital health companies, and pharmaceutical developers is now being built.

Psychedelic Drugs Market Restraints

Regulatory uncertainty and stigma presenting barriers to mainstream clinical adoption and commercial scale

Despite the progress made in recent years, the psychedelic drugs market continues to face meaningful structural restraints. The regulatory pathway for psychedelic medicines - while more defined than it was a decade ago - remains uncertain, lengthy, and expensive. The FDA's 2024 decision to decline initial approval of MDMA assisted therapy, citing the need for additional data on therapist certification and standardized protocol adherence, demonstrated that even well funded and well executed programs can face unexpected setbacks at the regulatory finish line. Cultural stigma around the word 'psychedelic' persists in parts of the medical establishment, creating friction in prescriber adoption, hospital formulary inclusion, and insurance reimbursement discussions. The training and certification requirements for therapists who administer psychedelic assisted therapy add complexity to scale, since the availability of qualified practitioners is a genuine bottleneck in markets where clinical programs are advancing faster than training infrastructure.

Psychedelic Drugs Market Opportunities

Expansion of insurance coverage, digital therapy integration, and decriminalization creating new pathways for market growth

The psychedelic drugs market stands at the threshold of several developments that could meaningfully accelerate its growth trajectory through 2035. Insurance coverage is the most transformative near term opportunity. Currently, most psychedelic therapies are paid out of pocket, limiting access to wealthier patients and suppressing the total addressable market substantially. As clinical approvals materialize and cost effectiveness data accumulates, private insurers and government healthcare systems will come under increasing pressure to cover psychedelic assisted therapy for approved indications. Oregon's regulated psilocybin services framework is already providing the insurance and reimbursement research community with real world utilization and outcome data that could accelerate this transition. Digital health integration represents another significant opportunity: platforms that provide remote preparation, session monitoring, and post session integration support can dramatically improve therapy scalability and outcomes consistency, potentially making psychedelic therapy accessible to patient populations that cannot access specialized in person clinics. The convergence of these factors creates a market that could be substantially larger by 2035 than any current projection would suggest if the enabling conditions align.

Recent Developments:

-

2026: Multiple MDMA and psilocybin assisted therapy programs advanced through late stage clinical trials globally, with Health Canada approving expanded compassionate access for psilocybin therapy. The number of specialized psychedelic therapy clinics operating in North America crossed the 5,000 mark as the ketamine therapy market continued its rapid expansion alongside emerging psilocybin service frameworks in Oregon and Colorado.

-

August 2025: SNS Insider confirmed global Psychedelic Drugs Market valuation of USD 3.63 billion for 2024, projecting growth to USD 10.11 billion by 2032 at a CAGR of 13.68%. The report highlighted ketamine as the dominant drug type at 42% share and North America as the leading regional market with 53% global share, driven by progressive regulatory reforms and expanding clinical trial networks.

-

August 2024: COMPASS Pathways reported positive Phase 2b clinical trial results for COMP360 psilocybin therapy in treatment resistant depression, demonstrating statistically significant and clinically meaningful reductions in depression severity scores at three weeks post treatment. The results reinforced the company's Phase 3 development program and attracted renewed investor and regulatory attention to the psilocybin therapeutic platform.

Psychedelic Drugs Market Key Players

-

COMPASS Pathways plc

-

MindMed Inc.

-

Cybin Inc.

-

Atai Life Sciences N.V.

-

GH Research PLC

-

Seelos Therapeutics Inc.

-

Beckley Psytech Ltd.

-

Field Trip Health and Wellness Ltd.

-

Numinus Wellness Inc.

-

Mydecine Innovations Group Inc.

-

Small Pharma Inc.

-

Awakn Life Sciences Corp.

-

Filament Health Corp.

-

Tryp Therapeutics Inc.

-

Psyence Group Inc.

-

Entheon Biomedical Corp.

-

Delic Holdings Corp.

-

PharmAla Biotech Holdings Inc.

Psychedelic Drugs Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.13 Billion |

| Market Size by 2035 | USD 14.90 Billion |

| CAGR | CAGR of 13.68% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Drug Type (Gamma Hydroxybutyric Acid, Ketamine, Psilocybin, Lysergic Acid Diethylamide, MDMA, Dimethyltryptamine, Ibogaine, Mescaline, Others) • By Source (Naturally Derived, Synthetic) • By Application (Treatment Resistant Depression, Major Depressive Disorder, Post Traumatic Stress Disorder, Substance and Opiate Addiction, Anxiety and Panic Disorders, Narcolepsy and Sleep Disorders, Alcohol Use Disorder, Others) • By Route of Administration (Oral, Intranasal, Intravenous, Sublingual and Buccal, Transdermal and Others) • By End Use Setting (Specialized Psychedelic Clinics, Hospitals, Research and Academic Institutes, Homecare Settings) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Johnson and Johnson, Jazz Pharmaceuticals plc, COMPASS Pathways plc, MindMed Inc., Cybin Inc., Atai Life Sciences N.V., GH Research PLC, Seelos Therapeutics Inc., Beckley Psytech Ltd., Field Trip Health and Wellness Ltd., Numinus Wellness Inc., Mydecine Innovations Group Inc., Small Pharma Inc., Awakn Life Sciences Corp., Filament Health Corp., Tryp Therapeutics Inc., Psyence Group Inc., Entheon Biomedical Corp., Delic Holdings Corp., PharmAla Biotech Holdings Inc. |

Frequently Asked Questions

Ans: The Psychedelic Drugs Market is expected to grow at a CAGR of 13.68% from 2026 to 2035.

Ans: The Psychedelic Drugs Market was valued at USD 4.13 billion in 2025.

Ans: The surging global burden of mental illness and the documented failure of conventional psychiatric treatments for a large patient population, combined with expanding clinical trial evidence, evolving regulatory pathways, and growing institutional investment in psychedelic assisted therapy platforms.

Ans: The Ketamine segment dominated the Psychedelic Drugs Market in 2025, accounting for approximately 42% of total market revenue, driven by its FDA approved status and the rapid expansion of ketamine infusion clinic networks globally.

Ans: Research and Academic Institutes are expected to grow at the fastest CAGR from 2026 to 2035, driven by the expanding global pipeline of psychedelic clinical trials and growing government and institutional funding for psychedelic medicine research programs.

Get in Touch