Quantum Computing Market Report Scope & Overview:

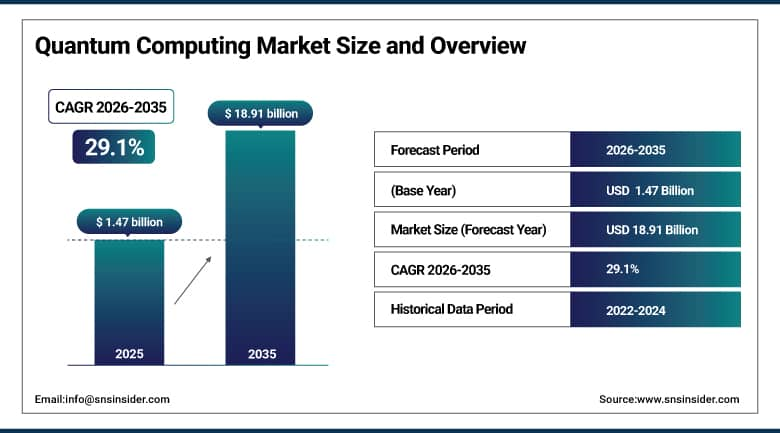

The Quantum Computing Market was valued at USD 1.47 billion in 2025 and is expected to reach USD 18.91 billion by 2035, growing at a CAGR of 29.1% from 2026-2035.

Quantum Computing (QC) is a quantum-mechanical computation model that promises to dramatically outperform classical computation commanding attention in the industry as well. The quantum computing market has been booming in the past couple of years, thanks to hardware and software advances, as well as increased computational demand as companies use QCs to address real-world problems such as health care, finance, aerospace and energy. This market is ripe for serious growth, as governments, both big tech, and startups are investing heavily in the future of technology.

Quantum Computing Market Size and Forecast:

-

Market Size in 2025: USD 1.47 Billion

-

Market Size by 2035: USD 18.91 Billion

-

CAGR: 29.1% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On Quantum Computing Market - Request Free Sample Report

Quantum Computing Market Trends:

-

Rising demand for high-performance computing and complex problem-solving is driving the quantum computing Quantum Computing Market.

-

Adoption across finance, healthcare, defense, and logistics sectors is boosting growth.

-

Advancements in qubit technologies, error correction, and quantum algorithms are enhancing computing power and reliability.

-

Expansion of cloud-based quantum services is increasing accessibility and scalability.

-

Focus on cryptography, material science, and AI applications is shaping adoption trends.

-

Government initiatives and research funding are accelerating development and commercialization.

-

Collaborations between tech companies, startups, and academic institutions are fostering innovation and deployment.

Quantum Computing Market Growth Drivers:

-

Increasing Demand for Advanced Computational Power Drives Growth in Quantum Computing Market

With increasing complexity of data and computing power and growing requirement from industries, we see the rise of quantum computers in enterprises. Conventional computing infrastructure is limited in its ability to solve complex problems associated with artificial intelligence (AI), machine learning, drug development, and climate simulation. Quantum computing provides unparalleled abilities to solve these complex problems by using quantum bits (qubits) that can process information in multiple states at the same time. This enables quantum systems to solve optimization problems, simulate molecular structures, and enhance decision-making processes at speeds that classical computers cannot match. Several sectors, including healthcare, energy, aerospace, and finance, are particularly interested in these capabilities to improve efficiency and innovation.

In healthcare, quantum computing can accelerate drug discovery and personalized medicine, while in finance, it can help optimize portfolio management and risk assessment. As more industries understand the potential of quantum computing to transform their operations and solve problems that were previously thought to be unsolvable, the demand for quantum computing continues to increase. The advancements in quantum hardware and software are just adding to the momentum in this market.

-

Significant Investments and Collaborations Fuel Expansion of Quantum Computing Capabilities

The fact that the private sector as well as governments have made significant investments in the development of quantum computing technology has played a critical role in the fast evolution of quantum computing technology. The likes of IBM, Google, Microsoft, and Amazon have invested billions of dollars in R&D to advance quantum computing. The investments made are not only in the development of hardware but also in software platforms that can harness the power of quantum computing.

In addition, governments around the world are ramping up their efforts to support quantum research, such as the U.S. National Quantum Initiative, which was established to accelerate quantum technologies with investments of hundreds of millions of dollars. Public-private partnerships also add to these efforts, with companies coming together to speed the commercialization of quantum computing and make it more accessible to everyone. These developments are helping to mitigate the existing challenges in hardware development, error correction, and scalability. With further investment, quantum computing is expected to become more advanced and accessible.

Quantum Computing Market Restraints:

-

High Costs and Lack of Scalability Pose Challenges to Widespread Adoption of Quantum Computing

Despite the promising advancements in quantum computing, the high costs of quantum hardware and the current limitations in scalability present significant challenges to the widespread adoption of the technology. Quantum computers have highly complex hardware, such as qubits that have to be protected from environmental interference, which requires complex and costly cryogenic solutions. This makes it very difficult to scale up quantum computing technology and restricts its use only to large corporations that have the resources to invest in R&D. Moreover, the fact that scalability is the challenge facing the technology today means that while quantum computers are able to solve some problems faster than classical computers, the technology is still in its infancy. Until significant breakthroughs are made in qubit coherence, error correction, and the overall size of the quantum system, the technology will remain in its current form. This means that for many companies, particularly small and medium-sized enterprises, the cost of adoption is prohibitive, and the immediate return on investment remains uncertain. While solutions to these challenges are being actively explored, it will take time for quantum computing to reach a level where it can be widely and cost-effectively deployed across various industries.

Quantum Computing Market Segment Analysis:

By Component, System segment dominates the market, Services are expected to grow fastest

In 2025, the System segment of the quantum computing market accounted for the largest share, with an estimated revenue of 64%. This dominance may be due to the emergence of strong progress in implementation issues regarding quantum hardware, quantum processors or quantum computers that are at the heart of any quantum system. There are already vast strides under the belt of companies like IBM, Google and D-Wave. For example, IBM’s Quantum System One has defined the standard in quantum systems that integrate with hardware, software and a cloud-based QaaS (Quantum as a Service) offering.

The Services segment in the quantum computing market would witness the highest CAGR of 30.29% during period 2026–2035, owing to a surge in demand for Quantum-as-a-Service (QaaS) and cloud-based quantum computing platforms. Quantum computing as a service gives your business access to quantum resources without the need for heavy investment in hardware. Leading firms like IBM, Microsoft, and Amazon Web Services (AWS) are expanding their service offerings.

By End-User, BFSI leads the quantum computing market, Healthcare is projected to grow fastest

In 2025, the BFSI (Banking, Financial Services, and Insurance) segment accounted for the largest market share of the quantum computing market, contributing approximately 25% of the total revenue. This is mainly due to the industry’s requirement for increased computing power in order to maximize risk-management, portfolio-optimization, fraud detection and cryptography. Quantum computing can disrupt the BFSI sector by offering quicker and accurate answers to both complex financial modeling, and data handling processes. Organizations such as IBM and Microsoft are the front runners to put in place quantum solutions targeted for BFSI.

The Healthcare segment is expected to witness the largest CAGR of 31.74% during the forecasted period 2026-2035, primarily driven by the growing interest in utilizing quantum computing for drug discovery, genomics, and personalized medicine. Quantum computing’s capacity to simulate molecular structures and unravel hard biological problems more effectively than traditional computers represents a tremendous opportunity for healthcare innovation. IBM has introduced its Quantum for Life Sciences program to enable drug companies to revolutionise how molecules interact at a quantum level.

Quantum Computing Market Regional Analysis:

North America Quantum Computing Market Insights

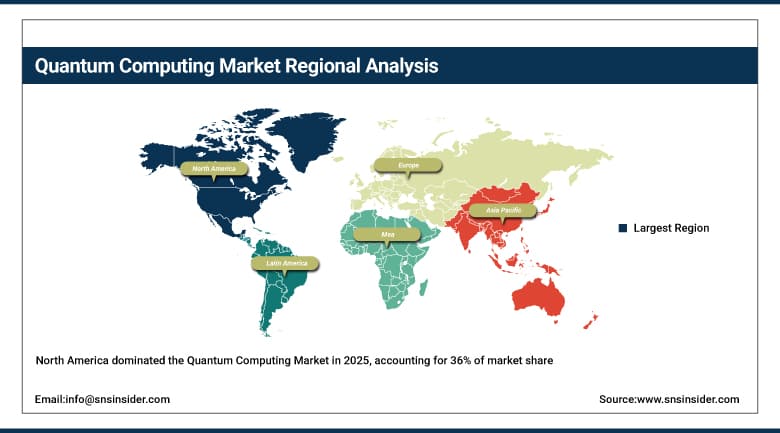

In 2025, North America was the leading region in the quantum computing market, due to large investments in research and development, a strong presence of key players, and government support. The market share of North America in the quantum computing market was estimated to be around 36%. This is because the United States is at the forefront of quantum research in both the public and private sectors. The U.S. National Quantum Initiative Act has provided large amounts of funding to speed the development and application of quantum technology.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific Quantum Computing Market Insights

The Asia Pacific (APAC) region was the fastest-growing region in the quantum computing market in 2025, with an estimated CAGR of around 31.93%. There are several reasons that have led to this swift expansion, including growing government support, technological developments, and the rising interest in innovation. Regions such as China and Japan have made considerable progress in the field of quantum research, with China taking the lead in quantum communication and cryptography initiatives. In addition to this, India has also been actively pursuing quantum computing research and development through its National Mission on Quantum Technologies and Applications (NM-QTA). The major companies, including Fujitsu and Hitachi, are leading the way in quantum computing developments.

Europe Quantum Computing Market Insights

The quantum computing market of Europe is progressing at a high pace due to heavy investments undertaken by government, research efforts and interaction between industry and academia. This article highlights quantum hardware, software platforms and quantum cryptography solutions. The UK, France and Germany lead innovation which encourages startups and tech relationships. In addition, quantum applications in finance, health care and logistics are driving adoption, as are regulations that support the growth of quantum research from policymakers who understand its importance to global commerce for years to come.

Middle East & Africa and Latin America Quantum Computing Market Insights

The Middle East & Africa and Latin America quantum computing markets are still in the budding stage due to the rising interest in adopting cutting-edge technology. The governments and various organizations in these regions are encouraging innovation through research institutions, startups, and partnerships with world-leading technology companies. The major use cases for quantum computing in these regions are finance, healthcare, logistics, and the military. Even though the adoption rate is in the early stages, awareness programs, funding, and technology collaborations are expected to boost the growth of the market.

Quantum Computing Market Competitive Landscape:

D-Wave Systems Inc.

D-Wave, founded in 1999 and headquartered in Burnaby, Canada, is a pioneer in quantum computing, focusing on the development of quantum annealing processors and hybrid quantum-classical systems. The company provides cloud-based access to quantum hardware and solvers, enabling businesses and researchers to tackle complex optimization, machine learning, and simulation problems. D-Wave emphasizes scalable quantum technology, real-time cloud integration, and practical applications to accelerate innovation in computational science and industrial problem-solving.

-

February 2024: D-Wave introduced its 1,200+ qubit Advantage prototype through the Leap real-time quantum cloud service. Existing Leap subscribers gain immediate access, while new users can receive up to one minute of free usage of the Advantage2 prototype, alongside other quantum processing units (QPUs) and solvers on the platform.

Rigetti Computing

Rigetti Computing, founded in 2013 and headquartered in Berkeley, California, is a leading provider of full-stack quantum computing systems. The company develops superconducting quantum processors, integrated quantum-classical platforms, and cloud-based quantum software to solve complex computational problems. Rigetti focuses on scalable architectures, benchmarking, and hybrid algorithms, enabling businesses, researchers, and government agencies to advance quantum applications in optimization, cryptography, and machine learning, bridging theoretical research with practical deployment of quantum computing solutions.

-

November 2023: Rigetti received Phase 2 funding from DARPA, totaling up to USD 1.5 million, to support the creation of benchmarks evaluating large-scale quantum computer performance in real-world applications.

IBM Quantum

IBM Quantum, part of IBM Corporation founded in 1911 and headquartered in Armonk, New York, is a global leader in quantum computing research and development. The division provides cloud-based quantum hardware, software tools, and educational initiatives to advance quantum science and workforce development. IBM Quantum focuses on practical applications, partnerships with academia, and large-scale education programs to cultivate the next generation of quantum scientists and engineers while expanding access to cutting-edge quantum technologies.

-

December 2023: IBM partnered with Keio University, The University of Tokyo, Yonsei University, Seoul National University, and The University of Chicago to advance quantum education in Japan, Korea, and the U.S., aiming to train up to 40,000 students over the next decade.

Key players:

Some of the major players in the Quantum Computing Market are

-

IBM (IBM Quantum System One, Qiskit)

-

D-Wave Quantum Inc. (Advantage Quantum Processor, Leap Quantum Cloud Service)

-

Microsoft (Azure Quantum, Quantum Development Kit (Q#))

-

Amazon Web Services (Amazon Braket, Quantum Solutions Lab)

-

Rigetti Computing (Aspen Series Quantum Processors, Forest Development Kit)

-

Fujitsu (Digital Annealer, Quantum-Inspired Optimization Services)

-

Hitachi (Quantum Annealing System, CMOS-Based Quantum Computing)

-

Toshiba (Quantum Key Distribution (QKD) System, Quantum Cryptography Solutions)

-

Google (Sycamore Processor, Quantum AI Platform)

-

Intel (Horse Ridge Cryogenic Controller, Quantum Dot Qubits)

-

Quantinuum (H-Series Ion Trap Processors, Quantum Origin (QKD))

-

Huawei (HiQ Cloud Quantum Computing Service, Quantum Computing Simulator)

-

NEC (Quantum Annealing Cloud Service, Quantum Neural Network Solutions)

-

Accenture (Quantum Computing Consulting Services, Quantum Impact Simulation Tool)

-

Nippon Telegraph and Telephone (NTT QKD Platform, Quantum Node Integration)

-

Bosch (Quantum Sensing Devices, Quantum-Inspired Optimization Tools)

-

Quantum Computing Inc. (Qatalyst Software, Entropy Quantum Computing Platform)

-

PsiQuantum (Photon-Based Quantum Processors, Quantum Foundry Services)

-

Alpine Quantum Technologies GmbH (Ion Trap Qubit Solutions, Quantum Research Platform)

-

Xanadu (Borealis Quantum Processor, PennyLane Software)

-

Zapata Computing (Orquestra Platform, Quantum Workflow Automation Tools)

-

Northrop Grumman (Quantum Sensor Technologies, Advanced Quantum Communication Systems)

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.47 Billion |

| Market Size by 2035 | USD 18.91 Billion |

| CAGR | CAGR of 29.1 % From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (System, Services) • By Deployment (On-Premises, Cloud) • By Application (Optimization, Simulation, Machine Learning, Others) • By End-user (Aerospace & Defense, BFSI, Healthcare, Automotive, Energy & Power, Chemical, Government, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | IBM, D-Wave Quantum Inc., Microsoft, Amazon Web Services, Rigetti Computing, Fujitsu, Hitachi, Toshiba, Google, Intel, Quantinuum, Huawei, NEC, Accenture, Nippon Telegraph and Telephone, Bosch, Quantum Computing Inc., PsiQuantum, Alpine Quantum Technologies GmbH, Xanadu, Zapata Computing, Northrop Grumman. |

Frequently Asked Questions

Ans: North America dominated the Quantum Computing Market in 2025, led by technology investments, research initiatives, and early enterprise adoption of quantum solutions.

Ans: The System segment dominated the Quantum Computing Market, while Services are expected to grow fastest due to rising Quantum-as-a-Service (QaaS) adoption.

Ans: Increasing demand for advanced computational power, complex problem-solving, and adoption across BFSI, healthcare, logistics, and AI applications is driving market growth.

Ans: In 2024, the Quantum Computing Market was valued at USD 1.47 billion, driven by early adoption in finance, healthcare, and defense sectors.

Ans: The Quantum Computing Market is expected to grow at a CAGR of 29.1% from 2025 to 2035, reflecting rapid adoption across industries.

Get in Touch