Radioimmunoassay Market Report Scope & Overview:

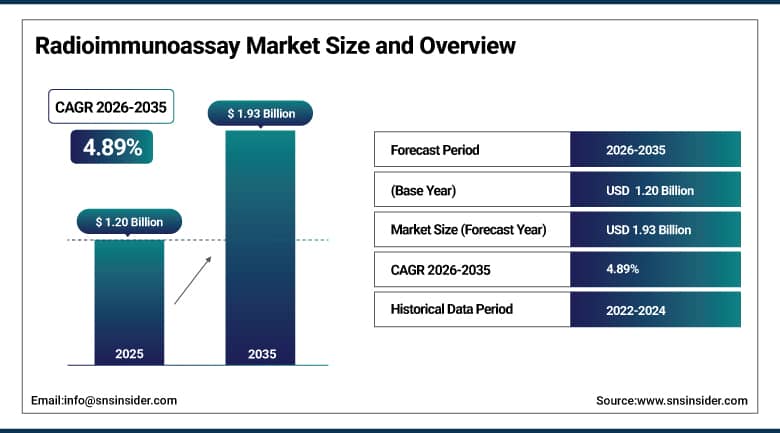

The Radioimmunoassay Market is valued at USD 1.20 Billion in 2025 and is expected to reach USD 1.93 Billion by 2035, growing at a CAGR of 4.89% from 2026-2035.

The Radioimmunoassay (RIA) Market is growing due to increasing demand for precise and sensitive diagnostic testing in endocrinology, oncology, and infectious diseases. Rising prevalence of hormonal disorders, cancers, and chronic illnesses is driving the need for accurate biomarker detection. Advancements in automated RIA systems, improved assay sensitivity, and growing adoption in clinical and research laboratories are further fueling market expansion. Additionally, increasing healthcare awareness and rising diagnostic testing volumes globally are supporting steady market growth.

In 2024, RIA usage grew by 7.5% globally, with clinical and research labs conducting over 135 million assays driven by rising demand for precise hormone, cancer antigen, and therapeutic drug monitoring, particularly in aging and high-burden chronic disease populations.

Radioimmunoassay Market Size and Forecast:

-

Market Size in 2025: USD 1.20 Billion

-

Market Size by 2035: USD 1.93 Billion

-

CAGR: 4.89% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Radioimmunoassay Market - Request Free Sample Report

Radioimmunoassay Market Trends:

-

Rising adoption of radioimmunoassay for highly sensitive detection of hormones, cancer biomarkers, and infectious diseases

-

Increasing demand for advanced RIA kits driven by chronic disease prevalence and expanding diagnostic laboratory workloads

-

Growth in endocrinology and reproductive health testing fueling frequent usage of RIA for accurate hormone quantification

-

Advancements in radioisotope labeling and assay automation improving precision, throughput, and reproducibility of diagnostic outcomes

-

Expanding usage of RIA in pharmaceutical research for drug development, pharmacokinetics, and therapeutic monitoring applications

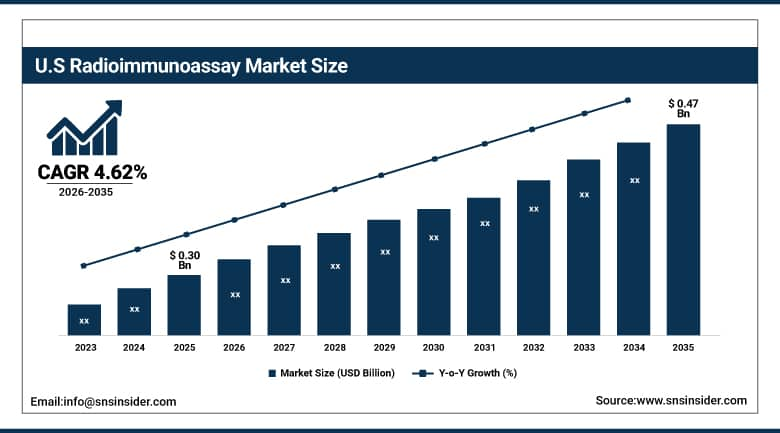

U.S. Radioimmunoassay Market is valued at USD 0.30 billion in 2025 and is expected to reach USD 0.47 billion by 2035, growing at a CAGR of 4.62% from 2026-2035.

Growth in the U.S. Radioimmunoassay Market is driven by rising prevalence of hormonal and metabolic disorders, increasing demand for accurate diagnostic testing, and growing adoption of automated and sensitive RIA systems in clinical and research laboratories. Expanding healthcare infrastructure further supports market growth.

Radioimmunoassay Market Growth Drivers:

-

Increasing prevalence of chronic and endocrine disorders is driving demand for radioimmunoassay techniques for highly sensitive hormone, drug, and biomarker detection in clinical diagnostics

The rising global burden of chronic diseases, including diabetes, thyroid disorders, infertility, metabolic dysfunctions, and cancer, is significantly increasing demand for sensitive diagnostic technologies. Radioimmunoassay remains one of the most accurate techniques for quantifying hormones, antigens, and drugs at extremely low concentrations. Hospitals and clinical laboratories rely on RIA for early disease detection, treatment monitoring, and therapeutic decision-making. Growing emphasis on precision diagnostics and the need for reliable quantification of biomarkers continue to drive adoption of RIA, especially in endocrinology, oncology, and toxicology applications despite competition from newer methods.

In 2024, rising cases of diabetes, thyroid disorders, and other endocrine conditions drove a 21% increase in radioimmunoassay (RIA) use for ultrasensitive hormone and biomarker testing, particularly in clinical labs managing chronic disease diagnostics.

-

Rising adoption of advanced laboratory automation and research activities in pharmaceutical and biotechnology industries boosts the need for accurate radioimmunoassay-based quantitative analysis

The growing pace of drug discovery, immunology studies, and biomedical research is driving laboratories to adopt highly precise and reproducible testing methods. Radioimmunoassay continues to be a preferred platform for accurate quantitative analysis in preclinical and clinical research, particularly for pharmacokinetics and toxicology studies. Laboratory automation further enhances efficiency, throughput, and assay consistency, strengthening the applicability of RIA systems in high-volume research environments. Increasing collaborations between pharmaceutical companies, CROs, and academic institutes support investments in advanced RIA instruments and reagents, contributing to sustained market growth across research-driven settings.

In 2024, 55% of pharmaceutical and biotech labs integrated radioimmunoassay (RIA) into automated workflows, driving a 19% increase in demand for RIA-based quantitative analysis to support drug development and biomarker validation.

Radioimmunoassay Market Restraints:

-

Stringent regulatory guidelines for radioactive materials and disposal create operational challenges, increasing compliance costs and limiting market adoption across smaller laboratories

Radioimmunoassay requires the use of radioactive isotopes that are subject to strict regulations governing procurement, handling, storage, waste disposal, and personnel safety. Compliance demands specialized infrastructure, radiation-shielded facilities, trained staff, and licensing procedures, which significantly increase operational expenses. These requirements limit adoption in small diagnostic laboratories and in developing regions with limited regulatory and financial support. Additionally, concerns over occupational exposure and environmental safety further discourage routine deployment. As regulatory frameworks continue to tighten, many laboratories prefer alternative non-radioactive immunoassay methods, restraining broad-based market expansion for RIA systems.

In 2024, 65% of small and mid-sized laboratories avoided radioimmunoassay (RIA) due to stringent regulations on radioactive material handling, with compliance and disposal costs adding 27% to operational expenses, limiting broader adoption.

-

Availability of alternative diagnostic techniques like ELISA and chemiluminescent immunoassays reduces dependency on radioimmunoassay and restrains overall market growth

Technological progress has introduced highly sensitive non-radioactive diagnostic platforms such as ELISA, CLIA, and fluorescence-based assays, offering faster turnaround times and simpler operational requirements compared with RIA. These techniques do not involve radioisotope handling and require minimal compliance documentation, making them more attractive for large-scale clinical laboratories. As healthcare facilities prioritize automation, cost-efficiency, and worker safety, many are transitioning to modern immunoassay systems for routine diagnostics. The availability of diverse test panels, improved sensitivity, and reduced maintenance requirements in alternative platforms continues to challenge the adoption rate of radioimmunoassay across multiple regions.

In 2024, over 60% of clinical labs shifted from radioimmunoassay (RIA) to ELISA and chemiluminescent immunoassays due to easier handling, lower regulatory burden, and comparable sensitivity slowing RIA market growth by an estimated 9%globally.

Radioimmunoassay Market Opportunities:

-

Growing investments in personalized medicine and precision diagnostics create opportunities for RIA applications in targeted biomarker detection and therapeutic monitoring

The shift toward personalized healthcare is increasing demand for highly sensitive diagnostic techniques capable of measuring subtle biomarker variations to support individualized treatment decisions. Radioimmunoassay is uniquely positioned to quantify extremely low-concentration analytes that other methods may fail to detect, making it valuable in monitoring hormone therapy, drug metabolism, immune response, and cancer biomarkers. As healthcare providers adopt precision-based treatment strategies, the need for accurate RIA-based profiling continues to rise. Increasing funding for translational research and biomarker discovery further strengthens the market opportunity for advanced RIA tools and reagents.

In 2024, RIA adoption in personalized medicine grew by 22%, with 35% of precision diagnostics labs using RIA for sensitive biomarker quantification and therapeutic drug monitoring in oncology, endocrinology, and autoimmune disorders.

-

Expansion of diagnostic infrastructure in emerging economies and increasing availability of research funding support wider adoption of radioimmunoassay technologies globally

Developing economies are increasing investments in healthcare modernization, laboratory automation, and disease surveillance programs, creating a conducive environment for the adoption of advanced immunoassay platforms. Academic and government-funded research institutions are expanding capabilities in endocrinology, toxicology, and drug discovery, generating demand for accurate biomarker analysis tools. International organizations offering grants and funding for disease research also support the installation of RIA systems. As laboratory capacity strengthens across Asia Pacific, Latin America, and the Middle East & Africa, radioimmunoassay adoption is expected to grow, opening new revenue streams for reagent and instrument manufacturers.

In 2024, diagnostic infrastructure expansion in emerging economies led to a 28% increase in radioimmunoassay (RIA) adoption, supported by a 20% rise in government and institutional research funding for endocrinology and infectious disease testing.

Radioimmunoassay Market Segment Highlights:

-

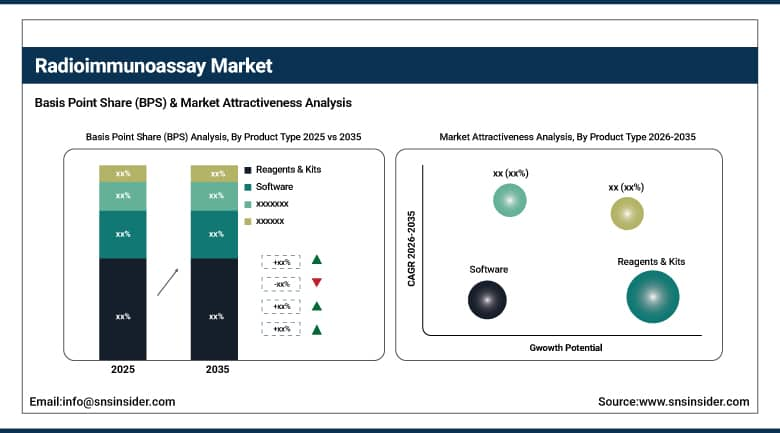

By Product Type: Reagents & Kits led with 44.8% share, while Software is the fastest-growing segment with CAGR of 7.9%.

-

By Radioisotope: Iodine-125 led with 41.2% share, while Indium-111 is the fastest-growing segment with CAGR of 8.1%.

-

By Application: Endocrinology led with 46.5% share, while Drug Testing & Pharmacokinetics is the fastest-growing segment with CAGR of 7.6%.

-

By End User: Clinical Laboratories led with 42.7% share, while Pharmaceutical & Biotechnology Companies are the fastest-growing segment with CAGR of 7.4%.

Radioimmunoassay Market Segment Analysis:

By Product Type: Reagents & Kits led, while Software is the fastest-growing segment.

Reagents & Kits dominate the market as they are essential for performing accurate and sensitive radio immunoassays. Their wide applicability in clinical diagnostics, research laboratories, and pharmaceutical studies ensures recurring demand. They are compatible with various analytes, cost-effective, and provide high reproducibility, making them the preferred choice for hospitals and labs. Their consistent supply, regulatory compliance, and role in enabling critical hormone, biomarker, and drug-level measurements maintain their leading position in the market.

Software is the fastest-growing segment as laboratories increasingly adopt digital tools for automated data acquisition, analysis, and reporting in radioimmunoassays. Cloud-based platforms, AI-enabled quantification, and workflow management solutions improve accuracy, reduce human error, and accelerate results. Growing demand from research and clinical laboratories, integration with instruments, and the need for regulatory-compliant reporting are driving adoption. These tools support efficient data handling, trend analysis, and quality control, making software a rapidly expanding segment.

By Radioisotope: Iodine-125 led, while Indium-111 is the fastest-growing segment.

Iodine-125 dominates due to its optimal half-life, high sensitivity, and broad compatibility with various immunoassay applications. It is widely used in hormone analysis, tumor marker detection, and therapeutic drug monitoring, providing accurate and reproducible results. Its availability, cost-effectiveness, and established safety protocols make it the isotope of choice for clinical and research laboratories. High adoption in both routine diagnostics and preclinical studies ensures that Iodine-125 maintains the leading position in the radioimmunoassay market.

Indium-111 is the fastest-growing radioisotope segment due to its expanding use in targeted receptor-binding studies, cell tracking, and immunoassay research. Its high specificity and suitability for labeling antibodies and peptides make it ideal for drug development and preclinical testing. Increasing demand from pharmaceutical and biotechnology companies, coupled with improvements in handling safety, imaging, and detection technologies, is driving adoption. Indium-111 supports precise analytical applications, making it a rapidly emerging segment in the market.

By Application: Endocrinology led, while Drug Testing & Pharmacokinetics is the fastest-growing segment.

Endocrinology leads the application segment as radioimmunoassay provides highly sensitive detection of hormones and endocrine biomarkers. Its ability to quantify minute concentrations makes it indispensable for diagnosing endocrine disorders, monitoring treatment efficacy, and guiding clinical decisions. Hospitals and clinical laboratories rely on RIA for routine hormone testing, contributing to its dominant position. The well-established protocols, accuracy, and reliability in both clinical and research settings ensure that endocrinology remains the largest application area.

Drug Testing & Pharmacokinetics is the fastest-growing application due to increasing demand for precise pharmacokinetic profiling, therapeutic drug monitoring, and preclinical testing. Pharmaceutical and biotechnology companies are adopting RIA to analyze drug absorption, distribution, metabolism, and excretion efficiently. Regulatory emphasis on bioanalytical validation, coupled with the rising development of biologics and small-molecule drugs, is fueling market expansion. The need for accurate, reproducible, and high-throughput testing supports rapid growth in this segment.

By End User: Clinical Laboratories led, while Pharmaceutical & Biotechnology Companies are the fastest-growing segment.

Clinical Laboratories dominate the end-user segment because they perform high-volume, routine testing requiring accuracy and validated RIA protocols. Equipped with advanced instruments, trained staff, and automated systems, these labs ensure high throughput and reliable results for diagnostics and research. Their central role in hospitals and private testing centers, combined with adoption of quality control and standardization practices, reinforces their market dominance. Demand from both diagnostic and research workflows sustains their leadership position.

Pharmaceutical & Biotechnology Companies are the fastest-growing end-user segment due to the increasing use of radioimmunoassays in drug development, biomarker quantification, and pharmacokinetic studies. The rising investment in biologics, targeted therapies, and precision medicine drives adoption. These companies require high-accuracy, reproducible, and regulatory-compliant assays for R&D and clinical trial monitoring. As personalized medicine and innovative therapeutics expand globally, the need for RIA applications in research pipelines accelerates growth, making this the fastest-growing end-user category.

Radioimmunoassay Market Regional Analysis:

North America Radioimmunoassay Market Insights

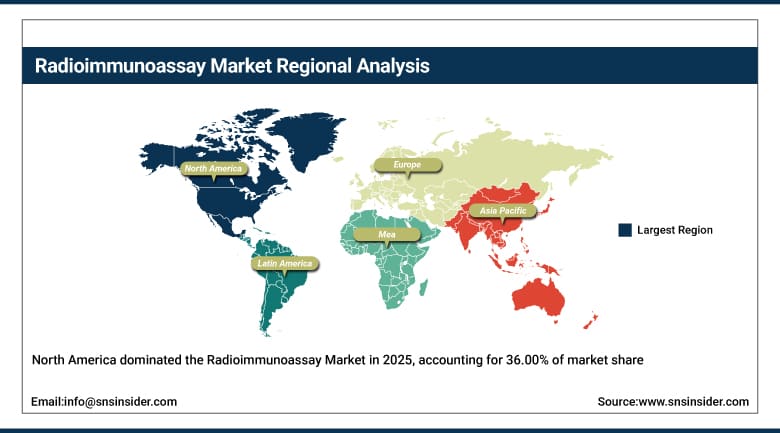

North America dominated the Radioimmunoassay Market with the highest revenue share of about 36.00% in 2025 due to the strong presence of advanced diagnostic infrastructure, significant healthcare expenditure, and high adoption of radioimmunoassay in endocrinology, oncology, and drug testing. The region also benefits from well-established laboratory networks, continuous research funding, and early availability of innovative radioisotope-based diagnostic solutions.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Radioimmunoassay Market Insights

Asia Pacific is expected to grow at the fastest CAGR of about 6.73% from 2026–2035 due to the rapid expansion of healthcare facilities, increasing rate of chronic and hormonal disorders, and rising adoption of advanced laboratory diagnostics. Growing investments in nuclear medicine, government support to strengthen diagnostic laboratories, and improving patient access to specialized testing further accelerate market growth in the region.

Europe Radioimmunoassay Market Insights

Europe holds a significant position in the Radioimmunoassay Market owing to its strong clinical research environment, high diagnostic testing volume, and early adoption of nuclear medicine-based assays. The presence of well-established pathology laboratories, supportive reimbursement policies for diagnostic procedures, and substantial investments in oncology and endocrinology research further fuel widespread use of radioimmunoassay. Increasing collaborations between hospitals, academic institutions, and biotechnology companies continue to enhance technology adoption across Western and Central European countries.

Middle East & Africa and Latin America Radioimmunoassay Market Insights

Middle East & Africa and Latin America collectively exhibit steady growth in the Radioimmunoassay Market driven by increasing incidence of chronic diseases, expanding laboratory capabilities, and growing demand for accurate hormonal and metabolic disorder diagnostics. Investments in oncology and infectious disease testing, government initiatives to strengthen nuclear medicine departments, and rising collaborations with global diagnostic players are improving access to radioimmunoassay services. Gradual development of healthcare infrastructure and training programs for laboratory professionals further support market expansion across these regions.

Radioimmunoassay Market Competitive Landscape:

Berthold Technologies GmbH & Co. KG, headquartered in Germany, is a leading provider of innovative measurement and detection systems, including radioimmunoassay (RIA) instruments. The company focuses on precision, reliability, and advanced technology to support clinical diagnostics, research, and life sciences applications. Its RIA solutions are designed to deliver highly accurate results for hormone, drug, and biomarker analysis. Berthold Technologies combines robust instrumentation with user-friendly interfaces to optimize laboratory workflows and ensure consistent, high-quality outcomes.

-

2024, Berthold Technologies launched the RIAStar, a fully automated radioimmunoassay workstation designed to modernize RIA workflows in clinical and research labs.

IBL International, based in Germany, specializes in producing high-quality immunoassays, including radioimmunoassay kits, for clinical diagnostics and research purposes. The company is known for its focus on accuracy, reproducibility, and sensitivity in hormone, tumor marker, and autoimmune testing. IBL International emphasizes innovation in assay development and quality control, offering standardized, reliable RIA solutions for laboratories worldwide. Its products support efficient workflows while ensuring precise measurement and robust performance across diverse medical and research applications.

-

2024, IBL International launched RIA Connect, a cloud-based digital platform designed to enhance quality control and data management for radioimmunoassay users.

DRG International, Inc., headquartered in the USA, is a prominent provider of diagnostic products, including radioimmunoassay kits for clinical and research use. The company offers a wide range of RIA solutions for endocrinology, oncology, and therapeutic drug monitoring. DRG International focuses on high sensitivity, accuracy, and user-friendly design, enabling laboratories to achieve reliable and reproducible results. By integrating innovative assay technologies with rigorous quality standards, DRG supports global healthcare and research institutions in advancing diagnostics and patient care.

-

2024, DRG International introduced a reformulated Iodine-125 (I-125) Cortisol RIA Kit that delivers the same analytical sensitivity with 30% lower radioactivity per test.

Radioimmunoassay Market Key Players:

-

DIAsource ImmunoAssays SA

-

Danaher Corporation (Beckman Coulter, Inc.)

-

Berthold Technologies GmbH & Co. KG

-

IBL International

-

DRG International, Inc.

-

PerkinElmer, Inc.

-

MP Biomedicals, LLC

-

Cisbio

-

Euro Diagnostica AB

-

DiaSorin S.p.A.

-

EMD Millipore (Merck KGaA)

-

Izotop / Institute of Isotopes

-

Stratec Biomedical AG

-

Tecan Group Ltd.

-

Creative Biolabs

-

Biosigma S.p.A.

-

Revvity, Inc.

-

Montreal Biotech

-

Shenzhen New Industry Biomedical Engineering Co., Ltd.

-

Siemens Healthineers AG

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.20 Billion |

| Market Size by 2035 | USD 1.93 Billion |

| CAGR | CAGR of 4.89% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Reagents & Kits, Instruments/Analyzers, Consumables & Accessories, Software, Services) • By Radioisotope (Iodine-125, Cobalt-60, Indium-111, Tritium, Other Radioisotopes) • By Application (Endocrinology, Oncology, Toxicology, Drug Testing & Pharmacokinetics, Clinical Diagnostics) • By End User (Hospitals, Clinical Laboratories, Research & Academic Institutes, Pharmaceutical & Biotechnology Companies, Contract Research Organizations) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | DIAsource ImmunoAssays SA, Danaher Corporation (Beckman Coulter, Inc.), Berthold Technologies GmbH & Co. KG, IBL International, DRG International, Inc., PerkinElmer, Inc., MP Biomedicals, LLC, Cisbio, Euro Diagnostica AB, DiaSorin S.p.A., EMD Millipore (Merck KGaA), Izotop / Institute of Isotopes, Stratec Biomedical AG, Tecan Group Ltd., Creative Biolabs, Biosigma S.p.A., Revvity, Inc., Montreal Biotech, Shenzhen New Industry Biomedical Engineering Co., Ltd., Siemens Healthineers AG |

Frequently Asked Questions

North America dominated with 36% revenue share in 2025, attributed to advanced diagnostic infrastructure, high RIA adoption, and strong healthcare expenditure.

Reagents & Kits led the Radioimmunoassay Market, owing to their essential role, reproducibility, cost-effectiveness, and wide application in diagnostics and research.

Growth is driven by rising prevalence of endocrine disorders, cancers, chronic diseases, and increasing adoption of automated, precise RIA systems.

The market was valued at USD 1.20 billion in 2025, supported by growing clinical and research laboratory adoption of RIA systems.

The market is projected to grow at a CAGR of 4.89% from 2026–2033, driven by rising demand for sensitive diagnostics globally.

Get in Touch