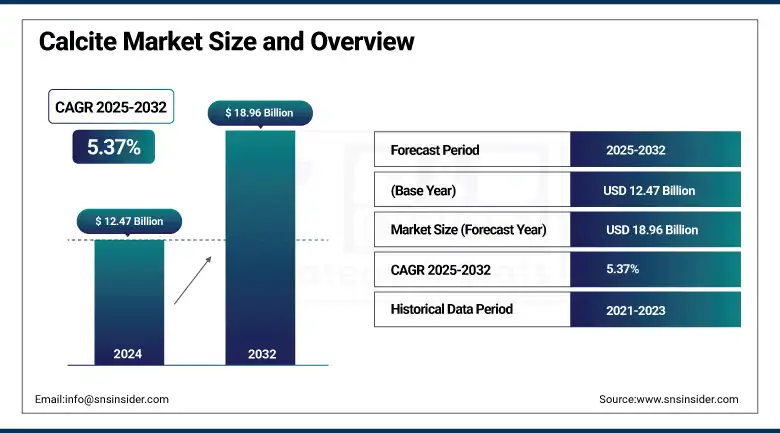

Calcite Market Size Analysis:

The Calcite Market size was USD 12.47 billion in 2024 and is expected to reach USD 18.96 billion by 2032 and grow at a CAGR of 5.37% % over the forecast period of 2025-2032.

Calcite market analysis reveals that increasing construction activities significantly contribute to the market's growth trajectory. It is due to the growing use of calcite in several building materials in construction activities is responsible for boosting the calcite market growth chart, as revealed through an analysis of the calcite market. Ground Calcium Carbonate (GCC) is an extensive form of filler used in cement, concrete, asphalt, and other construction products. These properties make it useful for the improvement of the strength, durability finish of these materials, due to its whiteness, chemical purity, and reinforcement ability.

To Get more information On Calcite Market - Request Free Sample Report

According to the U.S. Census Bureau, it is estimated that the total construction put in place during March 2025 was at a seasonally adjusted annual rate of USD 2,196.1 billion, a 2.8% increase from March 2024.

According to the Indian Ministry of Finance, the increase in public infrastructure investment made it a boon for the calcite market in demand as well. With infrastructure investments growing too quickly. USD 208 billion in FY 2023–2024, representing 5.87% of India’s GDP, which reflects an impressive growth in construction activities in India.

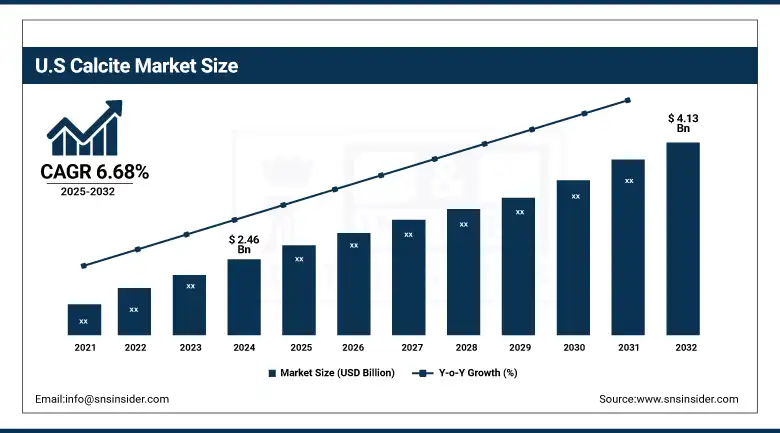

The U.S calcite market size was worth USD 2.46 billion in 2024 and is expected to reach USD 4.13 billion by 2032 growing at a CAGR of 6.68% over the forecast period of 2025-2032. It is attributed to a healthy industrial base in the region, growing infrastructure development, and strong demand from the construction, plastics, paper, and healthcare sectors. Calcite in the U.S. construction is an important contributor to the overall increase in calcite consumption as calcite is used in cement, paint, and floor-related products. Additionally, large-scale production and technology adoption in the country support the production of high-quality grade calcite for specialty applications such as food processing and fermentation.

Calcite Market Dynamics:

Drivers:

-

Growth in Cold Chain Logistics and Food Storage Drives Market Growth

The growing need for freezer warehouse infrastructure and temperature-controlled transport systems has emerged as increasing demand for perishable food products, dairy, meat, and pharmaceuticals globally. Efficient and durable refrigeration oils are used by these systems, but the bulk of demand lies with the refrigeration systems themselves, as they are integral to the quality and safety of the product being stored in these facilities. Meanwhile, with the rapid development of e-commerce in the grocery and pharmaceutical fields, the cold chain logistics globally are developing even faster.

For instance, in April 2023, Omya India made a USD 25 million investment in the Gujarat expansion of a strategically located advanced calcium carbonate plant. The expansion is intended for capacity expansion and boosting efficiency in light of rising demand across the adhesive and sealant industries.

Restraints:

-

High Transportation Costs May Hamper Market Growth

The large bulkiness and heaviness of calcite lead to high transportation costs, which is a major component of the cost structure leading to potential inhibition of the growth of the calcite market. Calcite is commonly produced in defined geographic locations and shipped to industrial centers great distances away for use or processing, so the long-distance freight, especially by land or sea, represents a significant cost. Rising fuel prices, along with higher freight tariffs and underdeveloped infrastructure in emerging markets, multiply these costs. Hence, for manufacturers and end-users in cost-sensitive industries, such as construction or plastics, there are new costs that might further squeeze margins and deter the use of calcite in favor of indigenous or lighter materials.

Opportunities:

-

Technological Advancements in Mining and Processing Create Opportunity for Market Expansion

The growing mining and processing technology is presenting a strong impetus for development in the calcite market due to its contributing factors in operational efficiency, product quality, and application. Newer extraction techniques including precision blasting and use of automated machinery have greatly improved overall calcite recovery with lesser environmental impacts. Moreover, ultrafine calcite particles, calcite crystals, and calcite powder with consistent morphology and width, used to be impossible to prepare in the past, are now easily preparable via advanced grinding and micronization technologies.

The U.S. Geological Survey (USGS) has made a special effort to synergize machine learning and remote sensing data to improve mineral resource information. It forms assistance for better knowledge of mineral distributions, such as calcite, and a more effective mining process. Apart from that, governmental initiatives such as the Thermally Induced Calcium Carbonate Precipitation (TICP) project, headed by the U.S. Department of Energy (DOE), which explores processes for calcite precipitation, also reveal a shift towards novel mineral processing methods.

Additionally, the calcite companies focused on the partnership strategy to expand their business in the market. In September 2022, Omya and IFG agreed to a strategic R&D partnership to investigate the incorporation of calcium carbonate into fibres at IFG's Fibers Research Center in Linz, Austria. The partnership will develop new fiber products that will improve performance and fiber product characteristics, and drive the calcite market trends.

Calcite Market Segmentation Analysis:

By Type

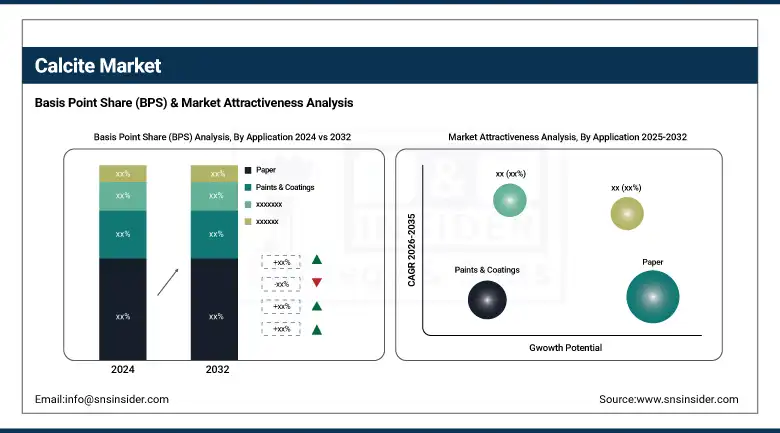

Ground calcium carbonate held the largest calcite market share, around 67%, in 2024 owing to its variety of applications, coupled with the economic advantage it provides the ground calcium carbonate form. GCC is obtained from very pure limestone and is an important raw material in construction, paints, plastics, paper, and adhesives. The reason for its high demand is that it improves the physical properties of the products by improving the strength, whiteness, and opacity in coatings and paints.

Precipitated calcium carbonate held a significant market share owing to its high quality and unique properties, which make PCC highly demanded in several industrial applications. PCC is produced via a controlled chemical process, unlike ground calcium carbonate (GCC), resulting in a finer particle, higher purity, and consistency. Thus, PCC is particularly important in the sectors of paper, plastics, rubber, and pharmaceuticals for the supply of white fillers and additives of the highest quality.

By Application

In 2024, the paper segment held the largest market share, which is approximately 28%. Calcium carbonate is a widely used functional filler in the paper industry, which is an important aspect of value-added value, because it provides necessary convenience such as brightness, opacity, and smoothness. It improves the printability and durability of the finished paper product, allowing a wider variety of paper grades, including coated, uncoated, and specialty paper to be manufactured using it.

Paints & Coatings held a significant market share due to the importance of calcium carbonate in improving the performance and cost-efficiency of paint formulations. Ground Calcium Carbonate (GCC) and Precipitated Calcium Carbonate (PCC) are two of the most extensively employed fillers in paints and coatings due to their traditional role in enhancing opacity, body, durability, and coverage in dried films. The viscosity of paint is controlled with calcium carbonate, which prevents slippage and improves the rheological properties for paint efficiency on application, which gives a smooth and even surface.

Regional Insights:

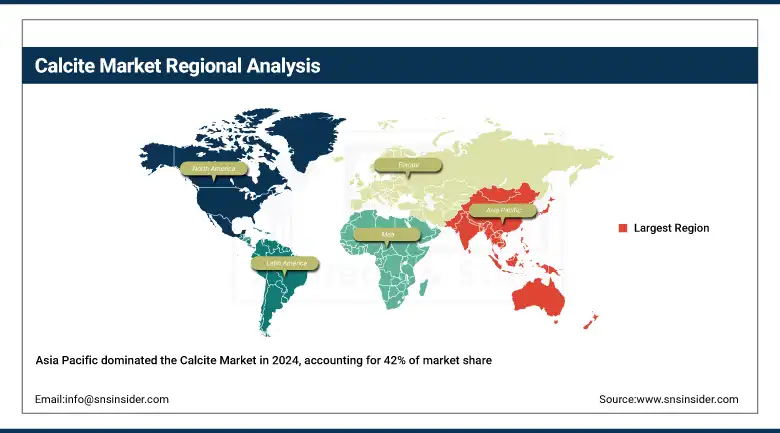

Asia Pacific held the largest market share, around 42%, in 2024. It is due to the expanding construction, plastics, and paper sectors, which are the key end-use industries of calcite, that are expected to boost the market growth in the region. With significant infrastructural growth, urbanization, and industrialization, economies, such as China, India, and Japan have been an important market for calcite as a coater and filler material. Also, the natural calcite available in the region at a cheap cost of production, and the government policy to grow the manufacturing area in the region. Factors including the presence of the leading domestic manufacturers and easy availability of raw materials have further solidified the region’s position in the global calcite market.

Get Customized Report as per Your Business Requirement - Enquiry Now

For instance, in October 2022, JSW Cement acquired Springway Mining, a subsidiary of India Cements, to gain access to 106 million tonnes of limestone reserves, a key raw material for calcite production. This production helps the company to increase its revenue in the market.

North America held a significant market share and is the fastest-growing segment during the forecast period owing to the extensive construction, plastics, and paper industries that are consumers of calcite products in the region. The growing construction infrastructure renovation and demand for residential houses in the U.S. and Canada are further expected to surge the product demand. This will in turn, contribute toward steady utilization of calcite in paints, cement, and coatings over the forecast period. Moreover, the country gains from cutting-edge manufacturing technologies and demanding quality criteria, which lead to high calcium carbonate usage in pharmaceutical, food additives, and solid polymer applications.

In 2023, the U.S. Department of Energy created USD 32 million in funding for research, development, and deployment of monitoring, measurement, and mitigation technology. This is in line with initiatives related to the elimination of Hydrofluorocarbons and the promotion of eco-friendly Calcites, and helps in reducing greenhouse gas emissions. As noted in the U.S. Geological Survey's Mineral Commodity Summaries 2025, calcite is one of the nonmetallic minerals in which the U.S recorded significant production in 2024. A wide range of increased mineral production extends through many components, the largest consumer of calcite being the construction industry.

Europe held a significant market share during the forecast period owing to an advanced industrial base, high-end use demand in key industries such as paper, plastics, construction, and paints, and an established system for sustainability and recycling. Nations including Germany, the U.K., France, and Italy have sturdy development and automobile sectors that take full advantage of using calcite as filler and coating materials. Calcite, a naturally occurring mineral, also plays a key role in the European trend toward more eco-friendly and energy-efficient building materials, as these are being developed in response to demand for greener and non-toxic building materials.

Calcite Market Key Players:

The leading players operating in the market are Imerys, Omya AG, Minerals Technologies Inc., Nordkalk Corporation, Huber Engineered Materials, Wolkem, Gulshan Polyols Ltd., Jay Minerals, Ashirwad Minerals, and Zantat Sdn Bhd.

Recent Developments:

-

In 2024, Gulshan Polyols has undertaken the expansion of production facilities for calcite-based products in response to the rising demand in the plastics and paints sector.

-

In 2024, ASEC Company for Mining invested in upgrading its calcite processing facilities to enhance product quality and expand market share in the Middle East and North Africa region.

| Report Attributes | Details |

| Market Size in 2024 | USD 12.47 Billion |

| Market Size by 2032 | USD 18.96 Billion |

| CAGR | CAGR of5.37% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Type (Ground Calcium Carbonate, Precipitated Calcium Carbonate) • By Application (Paper, Paints & Coatings, Construction, Plastics, Adhesives & Sealants, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Imerys, Omya AG, Minerals Technologies Inc., Nordkalk Corporation, Huber Engineered Materials, Wolkem, Gulshan Polyols Ltd., Jay Minerals, Ashirwad Minerals, Zantat Sdn Bhd |

Get in Touch