Hydroxyethyl Cellulose Market Report Scope and Overview:

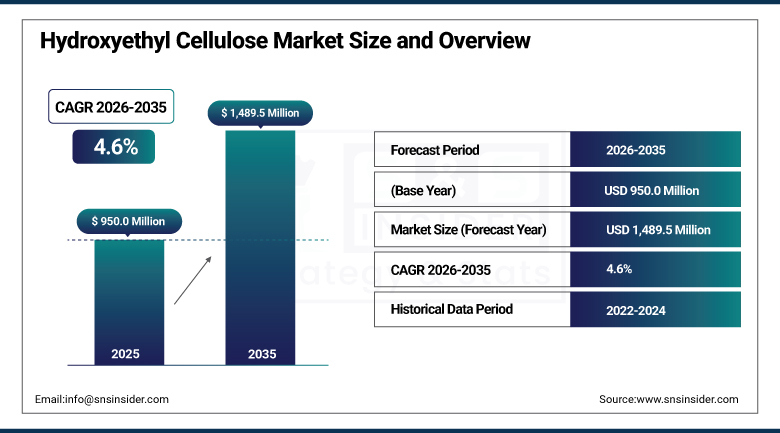

The Hydroxyethyl Cellulose Market was valued at USD 950.0 Million in 2025 and is projected to reach USD 1,489.5 Million by 2035, registering a CAGR of 4.6% from 2026 to 2035.

Hydroxyethyl cellulose is a non-ionic water-soluble polymer, produced by cellulose through etherification process using ethylene oxide, known for its excellent thickening, binding, film forming and water retaining characteristics within an incredibly wide variety of applications in industry, pharmaceuticals, and consumer goods manufacturing. Hydroxyethyl cellulose raw materials are crucial specialty chemicals, which help to reach the optimal product properties without any complicated synthetic substitutes, usually demonstrating good thickening and rheological properties similar to synthetic polymers, along with the bio-based sustainability and regulatory benefits. The above materials have significant benefits, such as natural nature, proven properties and environmental friendliness, being necessary for waterborne coatings, personal care formulations and many other applications in industry.

Under India's Smart Cities Mission, more than 6,000 construction projects worth approximately USD 30 billion had been initiated by the end of 2024, directly influencing demand for building materials where hydroxyethyl cellulose is commonly used to enhance workability and extend open time in cement-based formulations.

Market Size and Forecast

- Market Size in 2026E: USD 993.7 Million

- Market Size by 2035: USD 1,489.5 Million

- CAGR: 4.6% from 2026 to 2035

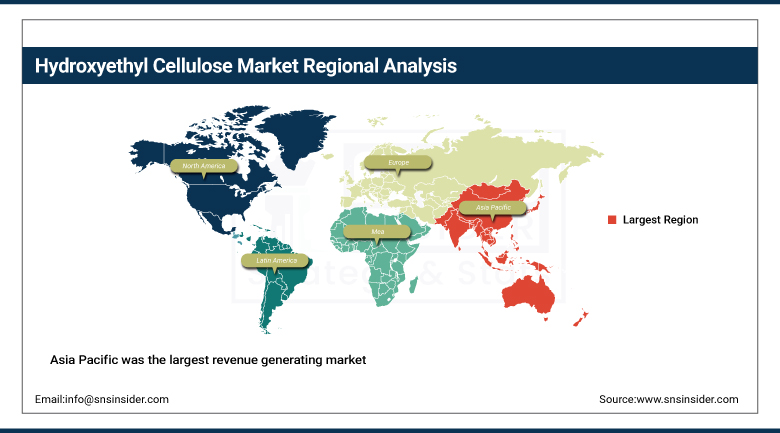

- Fastest Growing Region: Asia Pacific

- Largest Region: Asia Pacific

To Get more information On Hydroxyethyl Cellulose Market - Request Free Sample Report

Hydroxyethyl Cellulose Market Trends

- Increasing consumer preference for clean-label and plant-based ingredients continues significantly influencing hydroxyethyl cellulose demand across food industry applications.

- Increasing adoption of low-VOC and waterborne coating systems continues strengthening demand for cellulose ether thickeners in architectural paints.

- Supply chain volatility in dissolving wood pulp and refined cotton continues accelerating vertical integration strategies among HEC producers.

- Growth in hydraulic fracturing activity and shale gas exploration continues expanding demand for high-purity HEC drilling fluid additives.

- Governments continue investing in green buildings and sustainable construction methods that rely on additive-enhanced formulations incorporating cellulose-based rheology modifiers.

The US Hydroxyethyl Cellulose Market Outlook

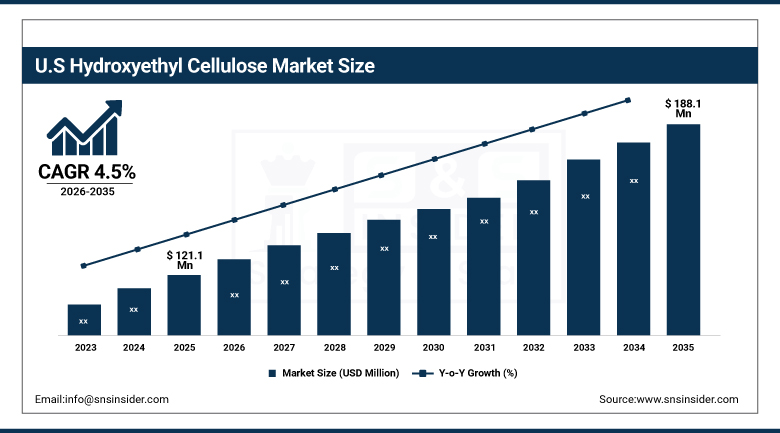

The US Hydroxyethyl Cellulose Market was valued at approximately USD 121.1 Million in 2025 and is projected to reach approximately USD 188.1 Million by 2035, registering a CAGR of approximately 4.5% from 2026 to 2035.

The overall demand in the U.S. was still being fueled by the demand from different industries like construction, personal care, and pharmaceuticals. The growing regulatory compliance requirements and consumers’ inclination toward sustainable products helped fuel market growth, whereas increased use of hydraulic fracturing techniques and exploration of shale gas fueled the demand for high-purity HEC drilling fluid additives among domestic oilfield services providers. Growing usage of waterborne coatings systems fueled the demand for cellulose ethers thickener in architectural paints, whereas the growth in infrastructural developments further strengthened the demand for construction grade hydroxyethyl cellulose in the U.S.

Ashland continued expanding its cellulose ether production capacity throughout 2025, targeting personal care, pharmaceutical, and construction chemical manufacturers seeking reliable, high-purity hydroxyethyl cellulose supply for increasingly demanding formulation and regulatory compliance requirements across the American market.

Hydroxyethyl Cellulose Market Segment Analysis

- By Application, waterborne paints and coatings led the market with an approximate 34.7% share in 2025, while pharmaceuticals is the fastest-growing application, tracking rising generic pharmaceutical and ophthalmic formulation demand.

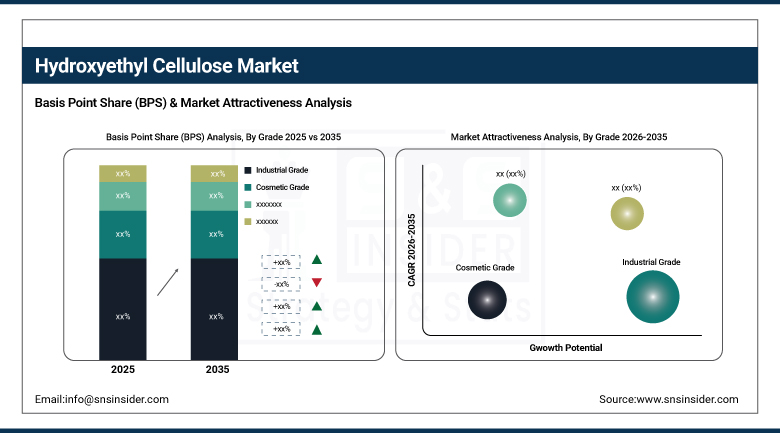

- By Grade, industrial grade led the market with an approximate 43% share in 2025, while pharmaceutical grade is the fastest-growing grade, tracking a projected 6.8% CAGR.

By Application, Waterborne Paints and Coatings led the market, Pharmaceuticals grew fastest

Waterborne paints and coatings held the market leadership position in 2025, at approximately 34.7% of total consumption, stemming from hydroxyethyl cellulose's critical functional role providing excellent thickening efficiency while maintaining superior leveling properties and brush drag characteristics across all waterborne formulation systems. Increasing environmental regulations and growing consumer preference for low-VOC coatings continued reinforcing this application category's dominant position by a considerable margin.

Pharmaceuticals is projected to grow at the fastest CAGR among applications, at approximately 6.8% through the forecast period. Aging global demographics, expansion of the global generic pharmaceutical market, and growing demand for preservative-free ophthalmic formulations in developed markets continue driving this growth, as hydroxyethyl cellulose serves as a key excipient in controlled-release tablets and topical gels where its water-retention and film-forming properties genuinely matter.

By Grade, Industrial Grade led the market, Pharmaceutical Grade grew fastest

Industrial grade HEC dominated the market, holding approximately 43% of total market share, due to its widespread use in building materials and oilfield applications. With the growing demand for high-quality building materials and increased oil exploration activity, this grade category continued reinforcing its dominant position across the broadest range of industrial applications this market serves, benefiting from stable supply from key cellulose derivative manufacturers and genuine ease of formulation.

Pharmaceutical Grade HEC is projected to grow at the fastest CAGR during the forecast period, at approximately 6.8%. Rising demand for controlled-release drug delivery systems and topical pharmaceutical formulations continues driving this growth, as pharmaceutical manufacturers increasingly specify the higher purity and consistency standards this grade delivers relative to industrial or cosmetic-grade alternatives, keeping this segment's growth rate well ahead of the broader, still-dominant industrial grade category.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|

Asia Pacific |

China |

34.20% |

|

North America |

United States |

80.30% |

|

Europe |

Germany |

24.05% |

|

Middle East and Africa |

UAE |

26.55% |

|

Latin America |

Brazil |

34.85% |

North America Hydroxyethyl Cellulose Market Insights

North America held a substantial share of global revenue, supported by strong demand across construction, personal care, and pharmaceutical applications. Growth in hydraulic fracturing activity and shale gas exploration continued expanding demand for high-purity HEC drilling fluid additives across the region's oilfield service sector throughout the year.

The United States accounted for roughly 80.30% of regional revenue, anchored by strong demand across construction, personal care, and pharmaceutical manufacturing sectors. Canada added further regional demand through its own growing construction and industrial materials sector, and that combined strength kept the continent a genuinely significant contributor to global hydroxyethyl cellulose revenue.

Europe Hydroxyethyl Cellulose Market Insights

Europe held a meaningful share of global revenue, supported by stringent regulatory standards and growing demand for sustainable, bio-based rheology modifiers across the region's construction, coatings, and personal care industries. Continued emphasis on low-VOC coating formulations kept reinforcing steady European demand throughout the year.

Germany led demand at roughly 24.05% of European revenue, supported by its substantial construction and industrial chemicals manufacturing base. The UK and France contributed substantial additional demand, and continued European regulatory emphasis on sustainable, bio-based formulations should keep regional demand climbing through the forecast period.

Asia Pacific Hydroxyethyl Cellulose Market Insights

Asia Pacific was the largest revenue generating market and continued registering the fastest growth trajectory in the global hydroxyethyl cellulose market. The growth in urban housing and infrastructure development, especially in fast-growing economies including India, China, and Brazil, continued pushing up demand for construction-grade HEC, keeping the region firmly positioned as the market's clear leader on both dominance and growth simultaneously.

China led the region and was projected to lead the global market in terms of revenue, supported by its massive construction and industrial manufacturing base. India and Southeast Asian economies contributed meaningful additional demand, with rapid urban housing development and expanding personal care and pharmaceutical manufacturing continuing to reinforce Asia Pacific's structural leadership in both production and consumption.

Get Customized Report as per Your Business Requirement - Enquiry Now

MEA and Latin America Hydroxyethyl Cellulose Market Insights

The Middle East and Africa and Latin America both showed steady growth, driven by expanding construction and infrastructure investment, growing personal care manufacturing activity, and rising oilfield exploration activity across both areas. As these markets continued building out modern construction and industrial manufacturing infrastructure, hydroxyethyl cellulose demand grew correspondingly from a considerably smaller base than in more mature markets.

The UAE led Middle East and Africa demand, supported by growing construction and oilfield exploration activity tied to the region's infrastructure investment agenda. Saudi Arabia contributed further demand through its own construction and petrochemical development programs. In Latin America, Brazil accounted for the largest share of regional revenue, with growing urban housing development continuing to anchor regional demand for hydroxyethyl cellulose.

Market Dynamics

Growth Drivers: Construction Sector Expansion and Sustainable Rheology Modifier Demand

The growth in urban housing and infrastructure development, especially in fast-growing economies like India, China, and Brazil, continues pushing up demand for construction-grade hydroxyethyl cellulose. HEC's water-retention and thickening properties help improve workability and extend open time, which remains genuinely crucial in large-scale construction projects relying on cement-based products including tile adhesives, self-leveling compounds, and plasters.

The increasing demand for sustainable rheology modifiers and bio-based alternatives continues reinforcing this driver, as hydroxyethyl cellulose provides efficient thickening and rheology control comparable to synthetic polymers while delivering genuine bio-based sustainability credentials and regulatory acceptance. Increasing consumer preference for clean-label and plant-based ingredients continues significantly influencing demand across food industry applications as well, and that combination of construction-sector scale and cross-industry sustainability appeal is exactly what keeps demand climbing at such a sustained pace.

Restraints: Raw Material Supply Volatility and Synthetic Alternative Competition

Supply chain volatility in dissolving wood pulp and refined cotton, the primary cellulose feedstocks for hydroxyethyl cellulose production, continues posing a genuine restraint on stable margin planning across the industry. That volatility continues accelerating vertical integration strategies among HEC producers seeking to secure reliable, cost-predictable raw material supply.

Competition from lower-cost synthetic rheology modifiers continues posing a further restraint in certain price-sensitive industrial applications, where cheaper alternatives can deliver adequate, if not equivalent, thickening performance. That cost sensitivity keeps some manufacturers weighing hydroxyethyl cellulose's genuine sustainability and performance advantages against synthetic alternatives' typically lower upfront material cost.

Opportunities: Pharmaceutical Excipient Expansion and Clean-Label Food Formulation Growth

Rising demand for controlled-release drug delivery systems and preservative-free ophthalmic formulations represents a genuinely significant opportunity, as this pharmaceutical application's fastest-growing status among all categories tracked in this market reflects genuine demand for the water-retention and film-forming properties hydroxyethyl cellulose delivers as a key pharmaceutical excipient. Vendors offering genuinely pharmaceutical-grade, consistently specified HEC stand to capture meaningful share of this expanding, higher-value application category.

Growing consumer preference for clean-label and plant-based ingredients offers a second substantial opportunity, as food manufacturers increasingly seek cellulose-based viscosifiers and stabilizers that satisfy clean-label expectations without compromising product performance. Vendors that can deliver genuinely food-grade, regulatory-compliant hydroxyethyl cellulose stand to capture meaningful share as clean-label formulation trends continue expanding across baked goods, beverages, and processed food categories worldwide.

Recent Developments:

- 2025: Dow continued expanding its cellulose ether product portfolio, targeting construction chemical and personal care manufacturers seeking reliable, sustainably sourced hydroxyethyl cellulose supply for demanding formulation applications.

- 2025: Shin-Etsu Chemical continued advancing its cellulose derivative manufacturing capability, targeting pharmaceutical and personal care customers seeking high-purity, consistently specified hydroxyethyl cellulose grades.

- 2024: AkzoNobel continued expanding its specialty cellulose chemicals production capacity, targeting coatings and construction chemical manufacturers seeking sustainable, bio-based rheology modifier alternatives.

Hydroxyethyl Cellulose Market key players are:

- Ashland Inc.

- Dow Inc.

- Shin-Etsu Chemical Co., Ltd.

- AkzoNobel N.V.

- Henkel AG & Co. KGaA

- DAICEL Corporation

- Chemcolloids Group

- Zhejiang Haishen New Materials Co., Ltd.

- Anhui Yillong Chemical Co., Ltd.

- Wuxi Sanyou Cellulose Technology Co., Ltd.

- Lamberti S.p.A.

- CP Kelco U.S., Inc.

- J.M. Huber Corporation

- Sinocmc Chemical Co., Ltd.

- Jiangsu Haixiang Chemical Co., Ltd.

- Shandong Head Group Co., Ltd.

- Shanghai Chemical Reagent Co., Ltd.

- Nippon Shokubai Co., Ltd.

- Nouryon Holding B.V.

- San-Ei Kagaku Corporation

Hydroxyethyl Cellulose Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 950.0 Million |

| Market Size by 2035 | USD 1,489.5 Million |

| CAGR | CAGR of 4.6% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application (Waterborne Paints and Coatings, Construction Chemicals, Personal Care and Cosmetics, Pharmaceuticals, Food) • By Grade (Industrial Grade, Cosmetic Grade, Pharmaceutical Grade, Food Grade) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Ashland Inc., Dow Inc., Shin-Etsu Chemical Co., Ltd., AkzoNobel N.V., Henkel AG & Co. KGaA, DAICEL Corporation, Chemcolloids Group, Zhejiang Haishen New Materials Co., Ltd., Anhui Yillong Chemical Co., Ltd., Wuxi Sanyou Cellulose Technology Co., Ltd., Lamberti S.p.A., CP Kelco U.S., Inc., J.M. Huber Corporation, Sinocmc Chemical Co., Ltd., Jiangsu Haixiang Chemical Co., Ltd., Shandong Head Group Co., Ltd., Shanghai Chemical Reagent Co., Ltd., Nippon Shokubai Co., Ltd., Nouryon Holding B.V., and San-Ei Kagaku Corporation |

Frequently Asked Questions

The Hydroxyethyl Cellulose Market was valued at approximately USD 950.0 Million in 2025, based on triangulation across multiple independent research sources.

The Hydroxyethyl Cellulose Market is expected to grow at a CAGR of approximately 4.6% from 2026 to 2035, based on triangulated secondary research estimates.

Asia Pacific dominated the Hydroxyethyl Cellulose Market in 2025, serving as both the largest and fastest-growing regional market.

The Waterborne Paints and Coatings segment dominated the Hydroxyethyl Cellulose Market by application, representing an estimated 34.7% of consumption in 2025.

The major growth factor is growth in urban housing and infrastructure development combined with increasing demand for sustainable, bio-based rheology modifiers.

Get in Touch