Rare Earth Metals Market Report Scope & Overview:

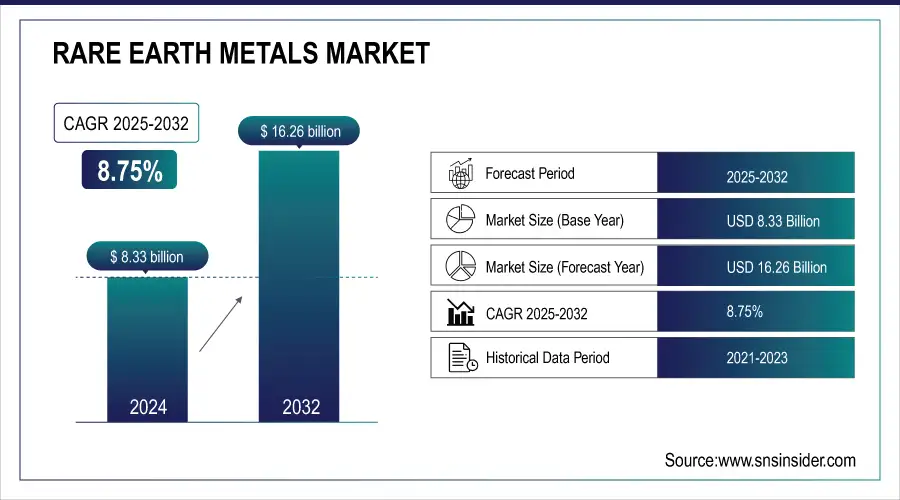

Rare Earth Metals Market was valued at USD 9.06 billion in 2025 and is expected to reach USD 21.03 billion by 2035, growing at a CAGR of 8.75% from 2026-2035.

The Rare Earth Metals Market is experiencing consistent growth because of increasing demand from various clean energy technologies, electric cars, and high-tech electronics. These metals play a critical role in the production of magnets that are required in wind power systems and electric car engines. Growing investment in renewable energy sources, military systems, and electronic devices is further fueling demand. Furthermore, initiatives to ensure diversity in supply chain management have led to increased exploration and mining activities, boosting market growth.

Supporting this market, the U.S. Geological Survey (USGS) classifies rare earth elements as critical minerals designation that triggers federal government programs for supply chain diversification, domestic production investment, and strategic stockpiling.

The USGS's 2023 Mineral Commodity Summaries report identifies China as the source of approximately 60% of global rare earth mine production and an even higher share of global processing capacity, highlighting the supply concentration risk that is motivating allied nations to invest in alternative supply chains.

In addition, the U.S. Department of Defense (DoD) has designated rare earth elements as critical to national security and has funded domestic rare earth processing capability development through the Defense Production Act (DPA) Title III program, committing hundreds of millions of dollars to support domestic mining, separation, and magnet manufacturing projects that reduce U.S. military dependence on foreign rare earth supply chains.

Rare Earth Metals Market Size and Forecast

-

Market Size in 2025: USD 9.06 Billion

-

Market Size by 2035: USD 21.03 Billion

-

CAGR: 8.75% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Rare Earth Metals Market - Request Free Sample Report

Rare Earth Metals Market Trends

-

Rising demand for advanced electronics, electric vehicles, and renewable energy technologies is driving the rare earth metals market.

-

Growing adoption in permanent magnets, batteries, wind turbines, and consumer electronics is boosting market growth.

-

Expansion of mining and refining activities to secure supply chains is fueling production.

-

Increasing focus on strategic resource security and reducing dependency on limited supply sources is shaping market trends.

-

Advancements in extraction, separation, and recycling technologies are enhancing efficiency and sustainability.

-

Rising government initiatives, stockpiling strategies, and investments in critical minerals are supporting market expansion.

-

Collaborations between mining companies, technology manufacturers, and governments are accelerating innovation and global supply diversification.

U.S. Rare Earth Metals Market was valued at USD 0.91 billion in 2025 and is expected to reach USD 2.10 billion by 2035, growing at a CAGR of 8.75% from 2026-2035.

Rising demands for rare earth metals in the use of electric cars, renewable energy applications, and defense equipment have increased the market growth rate in the U.S. The government is taking initiatives to increase the availability of domestic sources, decrease the reliance on imports, and enhance the mining capacity.

The U.S. Department of Energy's (DOE) Critical Materials Institute and its successor programs have invested over USD 400 million in rare earth supply chain research and development, including rare earth separation technologies, magnet recycling processes, and alternative material development.

The DOE's Industrial Demonstrations Program has additionally funded commercial-scale rare earth processing projects as part of the broader critical materials supply chain strengthening agenda mandated by executive orders on domestic supply chain resilience.

Rare Earth Metals Market Segment Highlights

-

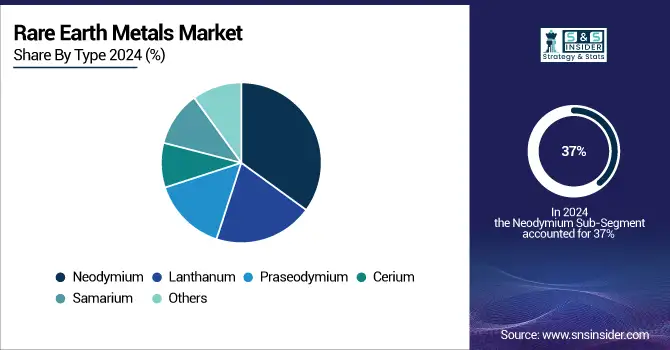

By Type, Cerium dominated with ~33% share in 2025; Neodymium fastest growing.

-

By Application, Magnets dominated with ~38% share in 2025; Catalysts fastest growing.

-

By End-Use Industry, Electronics dominated with ~29% share in 2025; Energy fastest growing.

Rare Earth Metals Market Segment Analysis

By Type, Cerium segment dominates the Rare Earth Metals Market, Neodymium segment expected to grow fastest

The Cerium segment accounted for the largest share of around 33% in the Rare Earth Metals Market in 2025. Cerium is extensively utilized in the production of catalysts, glass polishing, and metallurgy because of its oxidizing capability and low price relative to other rare earth metals. Due to wide usage of cerium in automotive catalytic converters and glass manufacturing industries, it accounts for high consumption worldwide. Furthermore, its availability and low-cost extraction add to its market dominance.

The Neodymium segment is projected to record the highest growth rate in the coming decade till 2035 owing to the rapidly growing requirement for powerful neodymium-based permanent magnets utilized in electric automobiles, wind power generators, and cutting-edge electronic gadgets. NdFeB or neodymium iron boron magnets provide efficient magnetic performance, which makes them indispensable for clean energy applications and future-generation transportation systems.

By Application, Magnets segment dominates the Rare Earth Metals Market, Catalysts segment expected to grow fastest

The Magnets segment held the largest market share of about 38% in 2025 because of their importance in many growing sectors such as consumer electronics, automotive, and renewable energy industries. Rare earth magnets help achieve smaller sizes and better performance in various products including smartphones, electric motors, and wind turbine generators. Electric cars and sustainable energy technologies are contributing further to the supremacy of this sector.

Catalysts represented the fastest-growing segment during 2026-2035 due to the strict emission standards and demand for cleaner energy sources. Rare earth elements play a huge role in the production of automotive catalysts and refining crude oil into different fuels. The rising awareness of environmental issues is increasing the use of catalytic technology worldwide.

By End-Use Industry, Electronics segment dominates the Rare Earth Metals Market, Energy segment expected to grow fastest

The Electronics segment held the dominant share of approximately 29% in 2025, due to the widespread use of rare earth elements in semiconductor components, display screens, batteries, and other components of electronics. The increase in the demand for smartphones, consumer electronics, and computing devices across the world contributes to the rise in consumption. Rare earth materials provide the required performance enhancements in electronic devices., supporting sustained market leadership.

The Energy segment is anticipated to witness the highest growth during 2026-2035, due to the rapid shift towards renewable energies such as wind and solar, and electric vehicles. Rare earth elements are used in wind turbine generators and electric vehicles due to their ability to create permanent magnets. There has been increased investment in clean energy infrastructure across the globe.

Rare Earth Metals Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

Asia Pacific |

China |

78% |

|

North America |

United States |

82% |

|

Europe |

Germany |

22% |

|

Middle East & Africa |

South Africa |

35% |

|

Latin America |

Brazil |

45% |

Asia Pacific Rare Earth Metals Market Insights

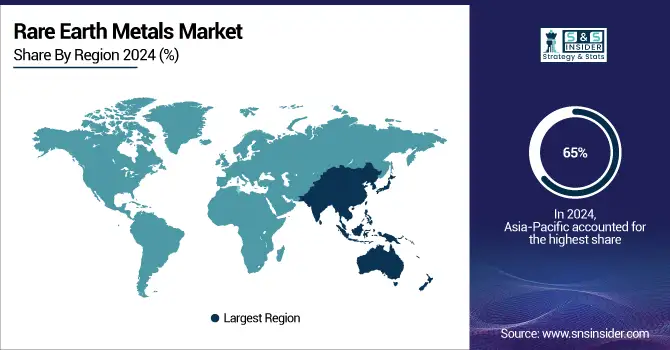

The Asia Pacific region led the global market for Rare Earth Metals, earning approximately 65% of revenues in 2025 due to China's dominance in rare earth mining and downstream processing, separation, and magnet production. The Bayan Obo mine in Inner Mongolia, China, holds the highest known reserve of rare earth minerals globally, producing the most heavy rare earths on the planet.

Beyond China, Australia's Lynas Rare Earths operating the Mt. Weld mine and a processing facility in Malaysia is the world's largest rare earth producer outside China, with a growing U.S. processing footprint.

China's Ministry of Industry and Information Technology (MIIT) administers strict production quotas and export controls on rare earth mining, smelting, and separation under the Rare Earths Management Regulations, maintaining the government's strategic oversight of the world's most concentrated rare earth supply.

China's periodic adjustment of export restrictions on rare earth materials most recently in 2023-2024 highlights the geopolitical leverage this supply concentration affords and directly stimulates foreign government investment in alternative supply chains.

North America Rare Earth Metals Market Insights

The region of North America represents one of the most rapidly developing segments of the Rare Earth Metals Market from the perspective of supply development, where the US and Canada are actively promoting their supply chain development programs. The Mountain Pass facilities owned by MP Materials are increasing their capacity for producing oxides and metals, and its Fort Worth facility located in Texas is planning to manufacture NdFeB magnets in the US for the first time in decades. Several rare earth developments in the US and Canada are supported by the US Department of Energy and Defense funding programs.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Rare Earth Metals Market Insights

In 2025, the European region is estimated to have a market share of around 12%, which is based on demand from major European markets such as the automobile sector, electronic industry, wind power generation, and the defense electronics sector, with less emphasis on production. The countries that make up the main market include Germany, France, Sweden, and the United Kingdom.

The EU Critical Raw Materials Act adopted in 2024 establishes binding targets for domestic EU production of strategic raw materials including rare earth elements, mandating that at least 10% of EU consumption be sourced from domestic production by 2030, directly stimulating European mine development and processing investment.

The European Commission's Critical Raw Materials Act sets strategic autonomy targets requiring at least 10% of the EU's annual consumption of strategic raw materials to be extracted domestically and at least 40% to be processed within the EU by 2030.

For rare earth elements, this creates direct policy pressure to develop domestic European supply including projects in Sweden (LKAB), Greenland (Greenland Minerals), and Finland and to build European rare earth processing and magnet manufacturing capacity, stimulating upstream market investment.

Middle East & Africa and Latin America Rare Earth Metals Market Insights

The Middle East & Africa (MEA) region presents immense rare earth resource opportunity, especially in South Africa, Namibia, Tanzania, Malawi, and Kenya, where explorations and development initiatives have intensified amid attempts by Western firms and administrations to secure alternative sources outside China. Projects nearing production status include Longonjo project by Pensana and Vital Metals’ initiatives in Tanzania.

In Latin America, Brazil has the second largest rare earth deposits globally, as stated by the USGS, with firms such as Serra Verde starting production from their ionic clay ore deposits rich in heavy rare earth elements like dysprosium and terbium.

Rare Earth Metals Market Growth Drivers:

-

Accelerating global electric vehicle production and renewable energy capacity expansion driving unprecedented structural demand growth for neodymium, dysprosium, and praseodymium in permanent magnet applications

The growth of electric vehicles and the shift towards clean energy worldwide is leading to a substantial increase in demand for rare earth permanent magnets. These magnets offer high energy density, efficiency, and compactness, being key to the design of EV traction motors, which consume 1-2 kilograms per unit. For offshore wind turbines – especially the direct-drive variety – the consumption is higher, at 600-800 kilograms per megawatt. The International Energy Agency forecasts that demand will quadruple by 2040.

The International Energy Agency (IEA) Net Zero by 2050 report identifies rare earth elements as among the most critical materials for the clean energy transition, projecting that demand for neodymium and praseodymium for permanent magnets will need to grow 40 times above 2020 production levels by 2040 under an accelerated energy transition scenario highlighting the extraordinary scale of supply development required to meet demand and underpinning long-term market growth projections.

Rare Earth Metals Market Restraints:

-

High geographic concentration of rare earth production and processing in China creating strategic supply chain vulnerability and price volatility that constrains market stability and downstream investment

The high degree of geographic concentration associated with rare earths mining and processing, whereby China produces around 60% of the world's total mined rare earths and almost 90% of the world's total separation and processing, constitutes the largest structural weakness within the rare earth value chain. Such concentration increases the risk of supply interruptions due to potential restrictions by China on rare earths exports, production quotas, or any form of geopolitics that may cause an unexpected surge in prices and supply insecurity to manufacturers relying on rare earths minerals. The long time required to set up new mines and processing plants between 10-15 years means that any efforts towards diversifying sources will take considerable time.

Rare Earth Metals Market Opportunities:

-

Massive global investment in domestic rare earth supply chains, recycling infrastructure, and processing technology creating transformative opportunities for non-Chinese producers and technology developers

With global efforts at diversifying rare earth sourcing becoming an issue of national security and industry strategy, there are huge opportunities that come with investment into rare earth mining, processing, and magnet production for countries other than China. With governments in the U.S., EU nations, Australia, Canada, and Japan investing in their ability to produce their own rare earth materials, there are great growth opportunities associated with rare earth recycling and recovery operations for neodymium and dysprosium from electric vehicle motors and wind turbine generators.

Recent Developments:

-

2025: MP Materials commenced commercial production of NdFeB permanent magnets at its Fort Worth, Texas manufacturing facility the first U.S.-produced rare earth magnets in decades under a long-term supply agreement with General Motors for EV traction motor magnets, marking a landmark milestone in U.S. rare earth supply chain independence.

-

2025: Lynas Rare Earths completed construction of its Texas rare earth processing facility under a DoD-funded agreement, adding U.S.-based heavy rare earth separation capacity to complement its existing Australian mining and Malaysian processing operations.

-

2024: Energy Fuels Inc. advanced rare earth oxide production at its White Mesa Mill in Utah, processing rare earth-bearing monazite sands into separated rare earth oxides including neodymium, praseodymium, and dysprosium products as part of its DOE-supported rare earth supply chain development program.

-

2023: Serra Verde commenced commercial production from its ionic clay rare earth deposit in Goias, Brazil, producing a mixed rare earth carbonate concentrate with favorable heavy rare earth content, establishing Brazil as an emerging source of heavy rare earth supply to complement Chinese production.

Rare Earth Metals Market Key Players

Some of the Rare Earth Metals Market Companies

-

MP Materials

-

China Northern Rare Earth High-Tech

-

Iluka Resources

-

China Minmetals Rare Earth

-

Jiangxi Ganzhou Rare Earth Group

-

Shenghe Resources

-

Neo Performance Materials

-

Avalon Advanced Materials

-

Texas Mineral Resources Corp

-

American Rare Earths

-

Energy Fuels

-

AEM REE

-

Rare Element Resources

-

Mkango Resources

-

USA Rare Earth

-

Materion Advanced Materials

-

Idaho Strategic Resources

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 9.06 Billion |

| Market Size by 2035 | USD 21.03 Billion |

| CAGR | CAGR of 8.75% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Type (Lanthanum, Praseodymium, Cerium, Neodymium, Samarium, Others) •By Application (Magnets, Catalysts, Metallurgy, Phosphors, Ceramics, Polishing, Others) •By End-Use Industry (Electronics, Automotive, Energy, Defense & Aerospace, Healthcare, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles |

MP Materials, China Northern Rare Earth High-Tech, Lynas Rare Earths, Iluka Resources, China Minmetals Rare Earth, Jiangxi Ganzhou Rare Earth Group, Shenghe Resources, Arafura Resources, Neo Performance Materials, Avalon Advanced Materials, Texas Mineral Resources Corp, Ucore Rare Metals, American Rare Earths, Energy Fuels, AEM REE, Rare Element Resources, Mkango Resources, USA Rare Earth, Materion Advanced Materials, Idaho Strategic Resources. |

Frequently Asked Questions

Asia Pacific dominated the Rare Earth Metals Market in 2025.

The Magnets segment dominated the Rare Earth Metals Market with approximately 40% share in 2025.

The Neodymium segment dominated the Rare Earth Metals Market with approximately 37% share in 2025.

The Rare Earth Metals Market was valued at USD 9.06 billion in 2025.

The Rare Earth Metals Market is expected to grow at a CAGR of 8.75% from 2026 to 2035.

Get in Touch