Renal Medical Devices Service Market Report Scope & Overview:

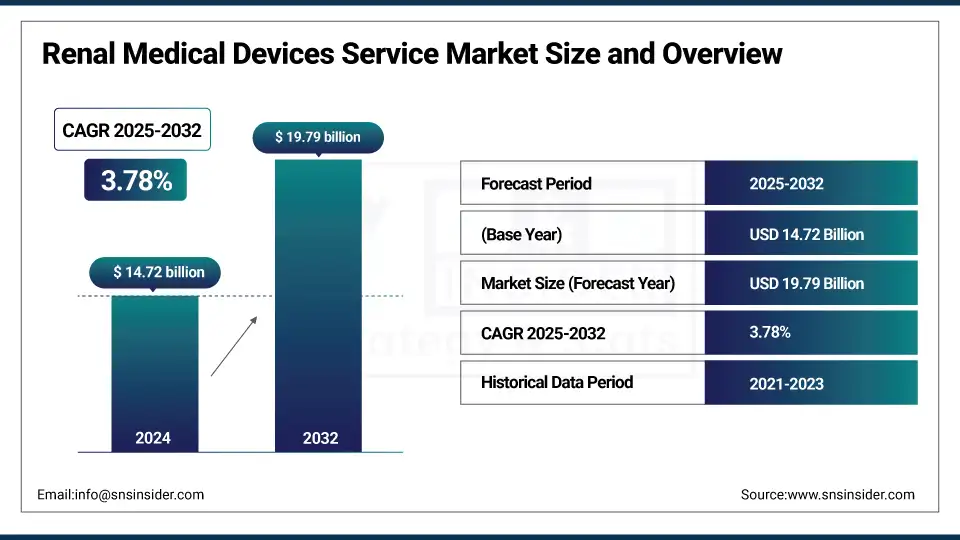

The renal medical devices service market size was valued at USD 14.72 billion in 2024 and is expected to reach USD 19.79 billion by 2032, growing at a CAGR of 3.78% over 2025-2032.

The renal medical devices service market is growing rapidly due to an increase in the incidence of renal disorders. More than 850 million people globally have kidney diseases, and, as of 2015, approximately 10% of the worldwide population was affected by chronic kidney disease (CKD). With an ageing global population and lifestyle-related diseases, such as diabetes and hypertension, the main drivers of CKD, there is a need for dialysis and renal monitoring, and kidney support equipment to be ever-increasing. The global renal medical devices services market is also growing as hospital groups shift toward home dialysis and/or interventional renal treatment. Since 2023, over 30% of the dialysis treatments have been held at home in the U.S. and Japan due to improvements in compact and wearable dialysis systems.

To Get more information On Renal Medical Devices Service Market - Request Free Sample Report

Supply-side expansion is driven by investment in new production capacity and regional supply chain localization among key players, such as Fresenius, Baxter, and Nipro, which are building production capacity in both the Asia Pacific and North America regions. Between 2020-2024, IHIH investors have invested over USD 2.3 billion in venture capital funds and in IPOs in renal device start-ups, which include AI-powered monitoring devices, wearable filters fetching kidneys, and RD devices. R&D is alive and well due to the R&D from Medtronic, DaVita, and Asahi Kasei Medical in the next-gen renal platform. There are also increased innovation-friendly regulatory environments, including the U.S. FDA has provided breakthrough device designations to several wearable, artificial kidney technologies and offered new fast-track review pathways under the “Kidney Health Initiative”. In Europe, however, CE-marked home dialysis equipment has witnessed increased clinical uptake with the release of revised EUDAMED guidelines.

In addition, government-sponsored programmes, including the KidneyX Innovation Accelerator and EU Horizon Health 2024, have pledged over USD 300 million of R&D support to renal device technologies together. These developments are creating good investment opportunities and promoting innovation in an active ecosystem, and are contributing to the renal medical devices service market growth.

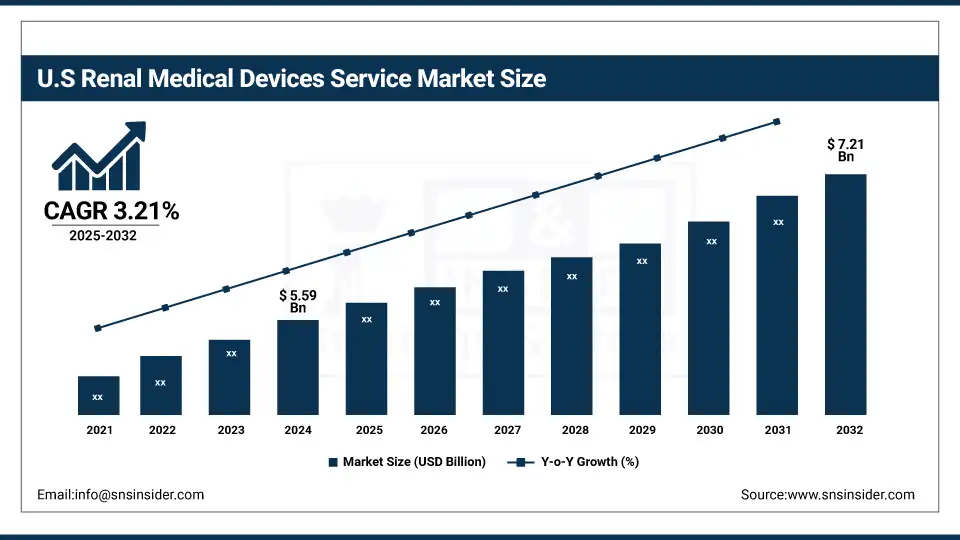

The U.S. renal medical devices service market size was valued at USD 5.59 billion in 2024 and is expected to reach USD 7.21 billion by 2032, growing at a CAGR of 3.21% over 2025-2032. The area has contributed to more than 38% of the global market. The U.S. accounted for the largest share, owing to approximately 90% of the country’s dialysis being covered by Medicare, a well-developed network of dialysis centers, and high investments in AI-based renal monitoring and wearable dialysis devices. More than 500,000 patients in the U.S. undergo dialysis every year. Canada is also increasing the use of home dialysis due to publicly funded pilots and increasing R&D collaborations between the government and private organizations.

Market Dynamics:

Drivers:

-

Rising Disease Burden, Technological Advancements, and Favorable Policies Fuel Market Expansion

The global renal medical devices services market is primarily being influenced by a growing prevalence of chronic and acute kidney disorders, which is highly associated with the increasing global prevalence of type 2 diabetes, obesity, and hypertension. According to the International Society of Nephrology, more than 1.2 million people die each year as a result of kidney failure, and that number is expected to rise based on increased life expectancies and unhealthy dietary practices. Such health trends are creating a lot of traction for dialysis machines, wearable kidney devices, and renal monitoring devices.

On the innovation side of things, companies, such as AWAK Technologies and Outset Medical, are focusing on portable and compact dialysis, with total R&D expenditure surpassing USD 450 million in 2023. In addition, supportive reimbursement changes, including CMS's ESRD Treatment Choices Model, are driving growth in home-based therapies and new device types. Regulatory authorities, including the U.S. FDA, have approved various AI-powered kidney monitoring solutions through fast-track channels. Improving access to cloud-connected systems and remote monitoring platforms is also enabling greater adoption among providers and patients. These factors together are contributing to the continued renal medical device service market growth, given active investment pipelines and policy environments.

Restraints:

-

High Cost, Device Complexity, and Limited Skilled Workforce Propel Market Growth

Despite technological advances, the global renal medical devices service market share has significant constraints, such as high initial and maintenance costs of advanced renal devices. The expenses could be prohibitive for health-care providers and patients, especially in low- and middle-income countries, as a wearable artificial kidney, for instance, may cost more than USD 20,000 apiece without taking account of consumables and ongoing service charges. Furthermore, the more complex devices, such as automated dialysis systems, need trained personnel from the nephrology team and technical personnel for setting up and maintaining such devices.

According to WHO, more than half of the nations globally suffer from inadequately trained nephrologists, leading to significant difficulty in deploying devices in under-resourced or remote areas. Moreover, many of the existing healthcare IT infrastructures in multiple geographies struggle to technically integrate cloud-based diagnostics and AI algorithms, and therefore, adoption has been slow. Fecal occult blood estimates were unreliable for all years from 2022 onward due to supply-side issues with semiconductors and polymers that disrupted production cycles of renal devices, which in turn led to delays and price hikes. Regulation is still a roadblock with devices needing to comply with a wide range of fast-changing standards in different regions, including the EU MDR, which has held up the rollout of some products. These are all barriers to the rapid rollout and availability of novel renal care technologies.

Segmentation Analysis:

By Device Type

Dialysis devices held the dominating position in 2024 with 38.6% of the renal medical devices service market share, as high prevalence of CKD and ESRD requires day-to-day hemodialysis and peritoneal dialysis. Their ongoing uses in both clinical and non-clinical settings make SWDs maintain a position in the lead.

The fastest growth segment was wearable artificial kidney devices, driven by growing R&D success and patient demand for mobility and flexibility in home treatment. These devices provide continuous renal replacement therapy with more freedom for patients, reducing the need for complications and hospital visits to comply with value-based care organizations.

By Application

In 2024, chronic kidney disease (CKD) was the major application, with a renal medical devices service market share of 34.2%, owing to a relatively high incidence and early-stage treatment by renal monitoring and dialysis devices.

The diabetes-related kidney complications were the fastest-growing application and were propelled by the growing global diabetes prevalence and the demand for persistent monitoring of kidney function and early intervention applications using advanced diagnosis coupled with integrated renal support devices.

By Technology

Conventional dialysis technologies accounted for the largest share in 2024, due to the availability of infrastructure, familiarity of the products from the providers, and insurance coverage.

The fastest growing was innovative dialysis technologies, as adoption of sorbent-based systems, portable home-use units, and AI-integrated platforms grows, resulting in better patient outcomes and less reliance on hospitals.

By Patient Demographics

Adult patients led the share in 2024, accounting for 65.1% as most of the population is affected by lifestyle-related kidney diseases, such as hypertension and diabetes.

The most rapidly expanding demographic was geriatric patients, with a rapidly aging global population, and increasing age-related renal dysfunctions augmenting the demand for chronic dialysis and home-based care technologies.

By End-User

Hospitals controlled the market in 2024 with a 43.5% share owing to the presence of advanced renal infrastructure, critical-care power, and inpatient dialysis reimbursement compatibility.

On the other hand, home healthcare providers were the fastest-growing end-user segment, owing to the rising demand for home-based treatment options, growing regulatory pressure for at-home dialysis, and growing patient preference for remote care with the help of telemedicine and wearable renal devices.

Regional Analysis:

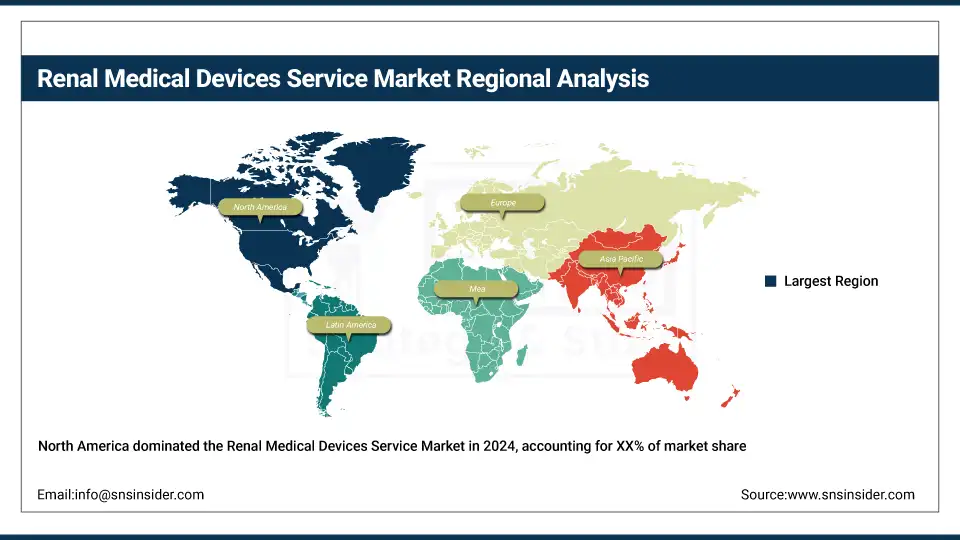

The renal medical devices service market analysis in North America was the largest in 2024, owing to the high prevalence of diseases along with high adoption of technology and reimbursement.

Get Customized Report as per Your Business Requirement - Enquiry Now

The Asia Pacific is the fastest-growing region in the global renal medical devices service market analysis, driven by CKD and ESRD prevalence, improving healthcare access, and higher investments in medical devices. The market for renal disease is rapidly evolving with China at the forefront, pressing ahead on aggressive expansion of dialysis centers and also cloud-connected renal monitoring systems. The number of ESRD patients in China exceeded 800,000 in 2024, and it aims to induce the use of domestically developed dialysis systems for low-cost treatment. High growth in India is driven by public-private partnerships, such as the Pradhan Mantri National Dialysis Program, which has enabled scaling access to rural areas. Having one of the most advanced medical infrastructures, Japan has an over 35% home dialysis penetration rate, and thus is one of the key adopters for wearable devices.

Key Players:

Notable renal medical devices service companies in the market include Fresenius Medical Care, DaVita Inc., Baxter International Inc., B. Braun Melsungen AG, Nipro Corporation, Medtronic plc, Asahi Kasei Medical Co., Ltd., NxStage Medical Inc., Rockwell Medical Inc., Dialyze Direct, Kawasumi Laboratories Inc., Sorene, HillRom Holdings Inc., Sandoz, Renal Ventures Management LLC, Abbott Laboratories, BD (Becton, Dickinson and Company), Boston Scientific Corporation, Poly Medicure Ltd., and Infomed SA.

Recent Developments:

In June 2024, Baxter International launched an upgraded version of its HomeChoice Claria automated peritoneal dialysis (APD) system, featuring enhanced Sharesource connectivity that enables real-time physician monitoring, catering to the rising demand for at-home treatment solutions among patients.

In April 2024, Medtronic initiated a global trial of its Symplicity Spyral renal denervation system, designed to manage resistant hypertension associated with renal dysfunction. The move highlights a shift toward integrated kidney-cardiovascular treatment pathways, underscoring evolving renal medical devices service market trends.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 14.72 billion |

| Market Size by 2032 | USD 19.79 billion |

| CAGR | CAGR of 3.78% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Device Type [Dialysis Devices, Catheters, Renal Monitoring Devices, Renal Denervation Devices, Wearable Artificial Kidney Devices, Kidney Transplant Devices, Distal Embolic Protection Devices, Renal Replacement Therapy Devices, Others (Portable dialysis units, home-use dialysis accessories, and device consumables)] • By Application [Chronic Kidney Disease (CKD), Acute Kidney Injury (AKI), End-Stage Renal Disease (ESRD), Kidney Failure, Renal Stone Disease, Hypertension-related Kidney Disorders, Diabetes-related Kidney Complications, Kidney Transplantation, Others (Polycystic kidney disease, lupus nephritis, and glomerulonephritis)] • By Technology [Conventional Dialysis Technologies, Innovative Dialysis Technologies, Minimally Invasive Technologies] • By Patient Demographics [Pediatric Patients, Adult Patients, Geriatric Patients] • By End User [Hospitals, Dialysis Centers, Home Healthcare Providers, Research & Academic Institutions, Others (Ambulatory surgical centers (ASCs), and specialized kidney clinics)] |

| Regional Analysis/Coverage | North America (U.S., Canada), Europe (Germany, France, UK, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America) |

| Company Profiles | Fresenius Medical Care, DaVita Inc., Baxter International Inc., B. Braun Melsungen AG, Nipro Corporation, Medtronic plc, Asahi Kasei Medical Co., Ltd., NxStage Medical Inc., Rockwell Medical Inc., Dialyze Direct, Kawasumi Laboratories Inc., Sorene, HillRom Holdings Inc., Sandoz, Renal Ventures Management LLC, Abbott Laboratories, BD (Becton, Dickinson and Company), Boston Scientific Corporation, Poly Medicure Ltd., and Infomed SA. |

Frequently Asked Questions

They include diagnostics, dialysis, and monitoring services used to manage kidney diseases like CKD and ESRD.

Rising CKD prevalence, aging population, and demand for home-based dialysis are key growth drivers.

Wearable dialysis, AI-based monitoring, and cloud-integrated remote care are revolutionizing renal treatment.

North America leads due to high CKD rates, advanced healthcare infrastructure, and favorable reimbursement.

High costs, limited access in low-income regions, and skilled workforce shortages hamper market growth.

Get in Touch