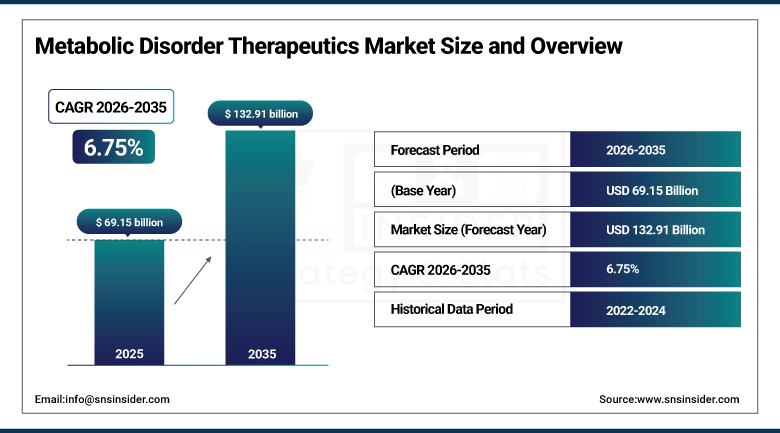

Metabolic Disorder Therapeutics Market Report Scope & Overview:

The Metabolic Disorder Therapeutics Market was valued at USD 69.15 Billion in 2025 and is expected to reach USD 132.91 Billion by 2035, growing at a CAGR of 6.75% from 2026 to 2035.

The development of metabolic disorder drugs is evolving from chronic symptom management to disease modification, obesity-focused, and cardiometabolic risk management, with current market driven by diabetes, obesity, dyslipidemia, metabolic dysfunction-associated steatohepatitis, rare metabolic diseases and their complications like kidney and cardiovascular disorders. The growth in demand is fueled by epidemiological evidence provided by the WHO, which states that there are over a billion obese individuals in the world in 2022, while diabetes is prevalent among around 830 million people worldwide in the same year. The increasing prevalence of metabolic problems is continuing to create growing clinical and commercial significance for GLP-1 agonists, dual/triple incretin mimetics, SGLT2 inhibitors, lipid modulating drugs, RNA therapy, and precision medicine.

Novo Nordisk continued advancing its GLP-1 receptor agonist portfolio in 2025, reinforcing its position as a global leader in diabetes and obesity therapeutics through sustained clinical development and manufacturing capacity expansion supporting rising global demand for incretin-based treatments.

Market Size and Forecast

- Market Size in 2026E: USD 73.82 Billion

- Market Size by 2035: USD 132.91 Billion

- CAGR: 6.75% from 2026 to 2035

- Fastest Growing Region: Asia Pacific

- Largest Region: North America

To Get more information Metabolic Disorder Therapeutics Market - Request Free Sample Report

Metabolic Disorder Therapeutics Market Trends

- Metabolic disorders therapeutics continue moving from chronic symptom control toward disease-modifying, weight-centric treatment strategies.

- Growing recognition that obesity, diabetes, liver disease, kidney disease, and cardiovascular risk are connected conditions continues shaping treatment approaches.

- Increasing adoption of precision medicine continues supporting more targeted, individualized metabolic disorder treatment protocols.

- Government policies supporting development of therapies for rare metabolic disorders continue fostering innovation across the pharmaceutical industry.

- Growing investments in biotechnology and pharmaceutical research continue accelerating the pace of novel metabolic therapeutic development.

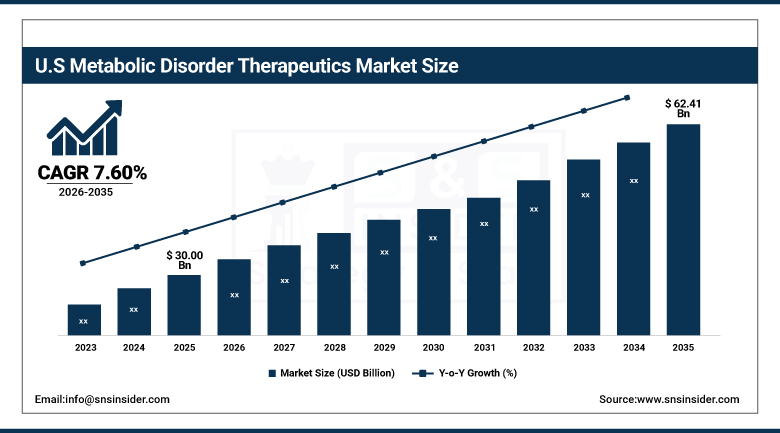

The United States Metabolic Disorder Therapeutics Market Outlook

The United States Metabolic Disorder Therapeutics Market was valued at USD 30.00 Billion in 2025 and is expected to reach USD 62.41 Billion by 2035, growing at a CAGR of 7.60% from 2026 to 2035.

The United States constituted nearly ninety percent of the value of the North American regional market, given the prevalence of major pharmaceutical producers and full coverage healthcare reimbursement system for metabolic disorder treatments in the country. Diabetes remained the disease category with the highest revenue generation, while the growing uptake of GLP-1 receptor agonists for both diabetes and obesity became an important driving factor for the market growth in the country.

Eli Lilly continued expanding its incretin therapy manufacturing capacity in 2025, strengthening its position serving American patients requiring GLP-1 and dual GIP/GLP-1 receptor agonist therapies for diabetes and obesity management amid sustained demand growth.

Metabolic Disorder Therapeutics Market Segment Analysis

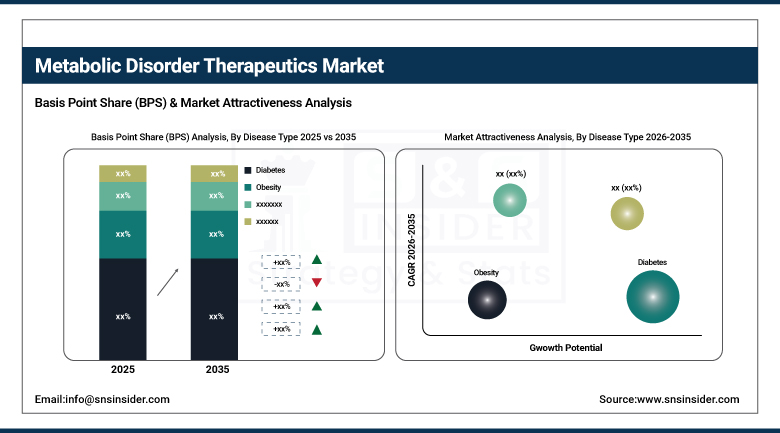

- By Disease Type, the diabetes segment held the largest share in 2025, while the lysosomal storage diseases segment is the fastest growing.

- By Treatment Class, the enzyme replacement therapy segment held approximately 30.60% share in 2025, while the gene therapy segment is the fastest growing, with a CAGR of approximately 9.70%.

- By Route of Administration, the parenteral segment held approximately 50.00% share in 2025, while the oral segment is the fastest growing, with a CAGR of approximately 8.20%.

- By Distribution Channel, the hospital pharmacies segment held the largest share in 2025, while the online pharmacies segment is the fastest growing.

By Disease Type, diabetes segment dominates the metabolic disorder therapeutics market, lysosomal storage diseases grow fastest

The diabetes segment held the largest share of the disease type segmentation in 2025, generating substantially more revenue than any other individual disease category given diabetes affecting approximately eight hundred thirty million people worldwide. That massive, sustained global patient population, combined with increasing adoption of insulin analogs and GLP-1 receptor agonists, continues keeping diabetes firmly at the top of the broader disease type segmentation, with obesity and dyslipidemia continuing to represent substantial additional revenue categories.

The lysosomal storage diseases segment is projected to grow at the fastest rate during the forecast period, as government policies supporting development of therapies for rare metabolic disorders continue fostering innovation within this specialized pharmaceutical category. Rising diagnosis rates and expanding reimbursement programs for these rare, inherited conditions continue pushing this disease type category's growth rate ahead of the broader disease type segmentation.

By Treatment Class, enzyme replacement therapy segment dominates the metabolic disorder therapeutics market, gene therapy grows fastest

The enzyme replacement therapy segment held approximately 30.60% of total market revenue in 2025, targeting the fundamental enzyme deficiencies associated with lysosomal storage disorders and significantly improving patient health and quality of life. That established clinical effectiveness continues keeping enzyme replacement therapy firmly at the top of the broader treatment class segmentation, with small-molecule and substrate reduction therapies continuing to represent meaningful additional treatment categories.

The gene therapy segment is projected to grow at the fastest CAGR of approximately 9.70% during the forecast period, holding significant potential to offer curative solutions for inherited metabolic diseases with limited treatment options. Rising clinical pipeline investment in gene therapy approaches for rare metabolic conditions continues pushing this treatment class category's growth rate ahead of the broader treatment class segmentation.

By Route of Administration, parenteral segment dominates the metabolic disorder therapeutics market, oral segment grows fastest

The parenteral segment held approximately 50.00% of total market revenue in 2025, aided by rapid onset of action and high bioavailability that continues making this route essential for medications with poor oral absorption. Parenteral administration effectively bypasses the gastrointestinal tract, avoiding first-pass metabolism crucial for immediate therapeutic effects, keeping this route firmly at the top of the broader route of administration segmentation.

The oral segment is projected to grow at the fastest CAGR of approximately 8.20% during the forecast period, driven by increasing patient preference and continued oral formulation innovation that continues improving treatment adherence relative to injectable alternatives. Rising development of oral GLP-1 and other oral metabolic therapeutics continues pushing this route of administration category's growth rate ahead of the broader route of administration segmentation.

By Distribution Channel, hospital pharmacies segment dominates the metabolic disorder therapeutics market, online pharmacies grows fastest

The hospital pharmacies segment held the largest share of the distribution channel segmentation in 2025, anchored by the clinical supervision that complex metabolic disorder treatment protocols, particularly for rare inherited conditions, continue requiring. That established clinical infrastructure requirement continues keeping hospital pharmacies firmly at the top of the broader distribution channel segmentation, with retail pharmacies continuing to represent a meaningful additional distribution category.

The online pharmacies segment is projected to grow at the fastest CAGR during the forecast period, as patients increasingly seek convenient, recurring access to chronic metabolic disorder medications including diabetes and obesity treatments through digital pharmacy platforms. Rising direct-to-consumer pharmacy adoption continues pushing this distribution channel category's growth rate ahead of the broader distribution channel segmentation.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

85.30% |

|

Europe |

Germany |

27.20% |

|

Asia Pacific |

China |

36.30% |

|

Middle East & Africa |

UAE |

26.40% |

|

Latin America |

Brazil |

37.20% |

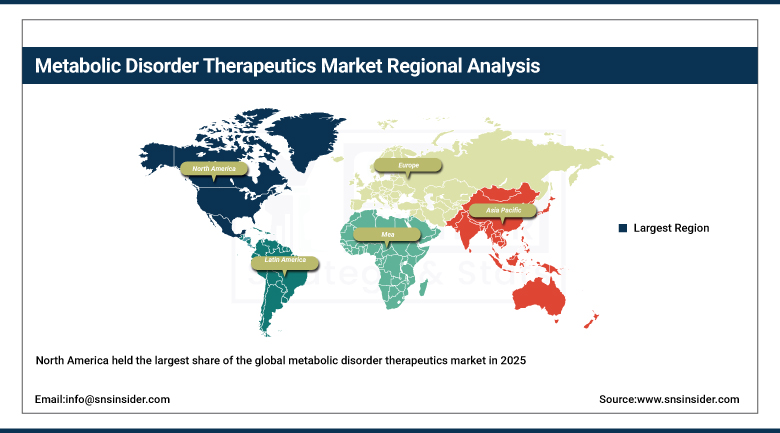

North America Metabolic Disorder Therapeutics Market Insights

North America held the largest share of the global metabolic disorder therapeutics market in 2025, supported by high prevalence of diabetes and obesity alongside comprehensive healthcare reimbursement infrastructure across the region. Continued GLP-1 receptor agonist adoption and rising diagnosis rates for rare metabolic disorders continued reinforcing this leadership position throughout the year.

The U.S. represented around 85.30% of regional revenues owing to its high number of top pharmaceutical companies along with the strong healthcare reimbursement system. The Canadian share in regional revenues was comparatively smaller but increased with time due to an increase in the use of metabolic disorders therapies in the country, thus positioning North America above all other regions in the market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Metabolic Disorder Therapeutics Market Insights

Europe held a substantial share of the global metabolic disorder therapeutics market in 2025, with reports indicating that approximately twenty-five percent of adults are afflicted by metabolic syndrome across the region. Germany accounted for roughly 27.20% of regional revenue, supported by its concentration of pharmaceutical manufacturers and comprehensive national health insurance coverage.

The United Kingdom, expected to register the highest country-level CAGR in the region, along with France and Italy, followed a broadly similar trajectory, as continued healthcare access expansion extended metabolic disorder therapeutics demand across the continent's largest healthcare markets. Continued regulatory support for rare disease therapeutics is expected to keep supporting steady European demand through the remainder of the forecast period.

Asia Pacific Metabolic Disorder Therapeutics Market Insights

Asia Pacific was the fastest-growing region in the global metabolic disorder therapeutics market, supported by rapidly rising diabetes and obesity prevalence, expanding healthcare infrastructure investment, and growing government-backed disease screening programs across the region's largest and most populous economies. Rising healthcare access continued driving regional demand at a pace considerably faster than more mature Western markets.

China accounted for roughly 36.30% of regional revenue, supported by expanding domestic healthcare infrastructure and growing oral therapeutic access. Japan and South Korea contributed significant additional regional demand through their own advanced healthcare technology adoption, reinforcing Asia Pacific's position as the clear growth leader in this market.

MEA & Latin America Metabolic Disorder Therapeutics Market Insights

The Middle East and Africa region recorded steady growth in metabolic disorder therapeutics adoption in 2025, with metabolic syndrome prevalence rates of approximately 29.2% reported in South Africa reflecting substantial unmet treatment need across the broader region. The UAE accounted for roughly 26.40% of regional revenue, supported by national healthcare modernization strategies and rising demand for advanced metabolic disorder treatment.

Latin America expanded at a comparable pace, led by Brazil at roughly 37.20% of regional revenue, where metabolic syndrome prevalence of approximately 25.2% continued to support category growth. Mexico and Argentina followed a similar trajectory as regional healthcare infrastructure investment expanded further through the remainder of the forecast period.

Growth Drivers: Rising Global Obesity and Diabetes Prevalence

Demand is supported by verified epidemiology, with more than one billion people living with obesity in 2022 and diabetes affecting approximately eight hundred thirty million people worldwide, continuing to be the central force behind metabolic disorder therapeutics market growth. Rising incidences of diabetes, obesity, and hypercholesterolemia continue driving sustained demand across nearly every major healthcare market worldwide, with prevalence expected to double in the coming two decades in the United States and Asian and Latin American countries in particular.

Increasing awareness regarding early diagnosis and disease management, combined with continuous advancements in therapeutic development, continues reinforcing structural demand growth. Increasing adoption of precision medicine, growing investments in biotechnology and pharmaceutical research, and rising demand for effective long-term management solutions continue establishing metabolic disorder therapeutics as essential components of modern healthcare.

Restraints: High Treatment Costs and Rare Disease Diagnosis Gaps

Even the exorbitant costs of the more advanced therapies designed to treat metabolic disorders, including enzyme replacement therapy and gene therapy treatment for rare lysosomal storage disorders, remains a hindrance to adoption in health care systems and patients that are sensitive to prices. Cost considerations have meant that such more advanced treatments continue to be confined to the wealthier markets and insured patients.

Gaps in the diagnosis of rare inborn errors of metabolism continue to constrain the patient population eligible for treatment, with many patients continuing to go through long periods without proper diagnosis and treatment. This gap continues to necessitate investments to increase the number of patients receiving treatment.

Opportunities: Oral Formulation Innovation and Gene Therapy Pipeline Expansion

Continued oral formulation innovation presents substantial opportunity for manufacturers positioned to serve patients seeking improved treatment adherence relative to injectable alternatives, particularly for chronic conditions requiring long-term management. Manufacturers capable of delivering effective oral GLP-1 and other oral metabolic therapeutics stand to capture a growing share of demand as this technology continues maturing.

Continued gene therapy pipeline expansion presents a further significant growth avenue, as these approaches hold significant potential to offer curative solutions for inherited metabolic diseases with limited treatment options. Manufacturers capable of successfully commercializing gene therapy treatments for rare metabolic disorders stand to capture meaningful new revenue streams through 2035.

Recent Developments:

- 2025: Amgen continued advancing its metabolic disorder therapeutic pipeline, targeting obesity and cardiometabolic risk reduction through novel treatment approaches in clinical development.

- 2025: AstraZeneca continued expanding its SGLT2 inhibitor and cardiometabolic therapeutic portfolio, strengthening its position serving patients with diabetes and related renal and cardiovascular complications.

- 2025: BioMarin Pharmaceutical continued advancing its enzyme replacement therapy and gene therapy programs, targeting patients with rare lysosomal storage disorders and other inherited metabolic conditions.

Metabolic Disorder Therapeutics Market key players are:

- Novo Nordisk A/S

- Sanofi S.A.

- Boehringer Ingelheim GmbH

- Eli Lilly and Company

- Merck KGaA

- Amgen, Inc.

- AstraZeneca PLC

- Actelion Pharmaceuticals Ltd.

- Shire PLC

- AbbVie, Inc.

- Biocon Ltd.

- BioMarin Pharmaceutical, Inc.

- Bristol-Myers Squibb Company

- Cipla, Inc.

- CymaBay Therapeutics, Inc.

- Pfizer Inc.

- Johnson & Johnson

- Roche Holding AG

- Regeneron Pharmaceuticals, Inc.

- Vertex Pharmaceuticals Incorporated

Metabolic Disorder Therapeutics Market Report Scope :

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 69.15 Billion |

| Market Size by 2035 | USD 132.91 Billion |

| CAGR | CAGR of 6.75% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Disease Type (Diabetes, Obesity, Dyslipidemia, Lysosomal Storage Diseases) • By Treatment Class (Enzyme Replacement Therapy, Small-Molecule Therapy, Substrate Reduction Therapy, Gene Therapy) • By Route of Administration (Parenteral, Oral) • By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Novo Nordisk A/S, Sanofi S.A., Boehringer Ingelheim GmbH, Eli Lilly and Company, Merck KGaA, Amgen, Inc., AstraZeneca PLC, Actelion Pharmaceuticals Ltd., Shire PLC, AbbVie, Inc., Biocon Ltd., BioMarin Pharmaceutical, Inc., Bristol-Myers Squibb Company, Cipla, Inc., CymaBay Therapeutics, Inc., Pfizer Inc., Johnson & Johnson, Roche Holding AG, Regeneron Pharmaceuticals, Inc., Vertex Pharmaceuticals Incorporated |

Frequently Asked Questions

The Metabolic Disorder Therapeutics Market is expected to grow at a CAGR of 6.75% from 2026 to 2035.

The Metabolic Disorder Therapeutics Market was valued at USD 69.15 Billion in 2025.

Rising global obesity and diabetes prevalence combined with continuous advancements in therapeutic development is the major growth factor.

The Enzyme Replacement Therapy segment held approximately 30.60% share in 2025.

North America held the largest share of the Metabolic Disorder Therapeutics Market in 2025.

Get in Touch