Resuscitation Devices Market Report Scope & Overview:

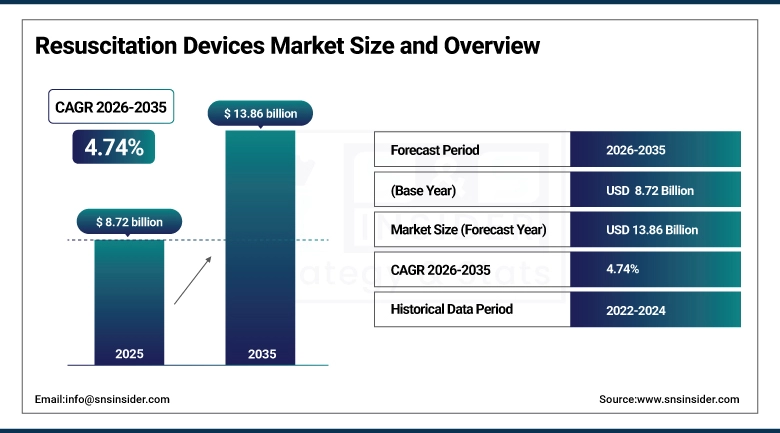

The Resuscitation Devices Market size was valued at USD 8.72 Billion in 2025 and is expected to reach USD 13.86 Billion by 2035, growing at a CAGR of 4.74% over the forecast period of 2026-2035.

The growth of the global resuscitation devices market is driven by factors like an increase in the incidence of sudden cardiac arrest, respiratory failures, and trauma-related emergencies. In addition, the need for immediate interventions in the treatment of patients experiencing life-threatening situations is also a major factor. Resuscitation devices like airway management devices, ventilators, and external defibrillators play an important role in the treatment of patients experiencing critical care situations. The increasing incidence of cardiovascular diseases, the aging population, and an increase in the incidence of respiratory disorders have significantly contributed to the growth of the global resuscitation devices market.

The incorporation of advanced technologies like automated defibrillation, portable ventilation devices, and advanced airway management devices has significantly improved the survival rate of patients experiencing critical care situations. In addition, the increasing need for improving the infrastructure of the ambulance services and the increasing need for advanced life support equipment in the healthcare sector have significantly contributed to the growth of the global resuscitation devices market. The need for wearable cardioverter-defibrillator devices is also increasing in the global market.

In March 2025, global emergency medical organizations reported that the adoption of automated external defibrillators (AEDs) in public access programs increased by nearly 28% compared to the previous year, highlighting the expanding role of rapid-response resuscitation equipment in improving survival rates for sudden cardiac arrest cases.

Resuscitation Devices Market Size and Forecast:

-

Market Size in 2025: USD 8.72 Billion

-

Market Size by 2035: USD 13.86 Billion

-

CAGR: 4.74% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Resuscitation Devices Market - Request Free Sample Report

Resuscitation Devices Market Trends:

-

Increasing deployment of automated external defibrillators (AEDs) in public spaces, airports, corporate offices, and sports facilities to improve response time during cardiac emergencies.

-

Growing demand for portable ventilators and compact airway management devices designed for emergency transport and pre-hospital care settings.

-

Expansion of wearable cardioverter defibrillators for patients at high risk of sudden cardiac arrest who require continuous cardiac monitoring outside hospital environments.

-

Advancements in laryngoscopy technology, including video laryngoscopes, improving the success rate of airway intubation procedures.

-

Rising focus on pediatric resuscitation equipment specifically designed to support neonatal and child emergency care.

-

Integration of digital monitoring systems with defibrillators and ventilators to enable real-time patient data analysis during emergency interventions.

-

Increasing government initiatives promoting CPR awareness and AED accessibility across public healthcare systems.

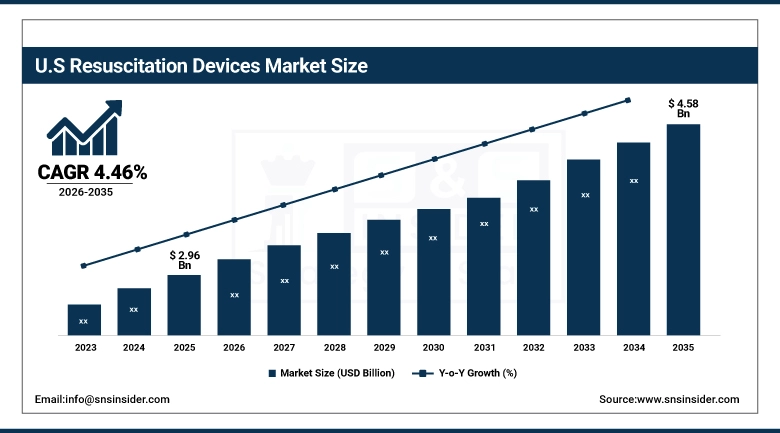

The U.S. Resuscitation Devices Market is estimated at USD 2.96 Billion in 2025 and is expected to reach USD 4.58 Billion by 2035, growing at a CAGR of 4.46% from 2026-2035. The country holds a significant position in the world market due to its well-developed emergency medical services infrastructure, high healthcare expenditure, and widespread use of defibrillation devices in healthcare and community healthcare programs. Moreover, strict regulations for emergency equipment in healthcare settings, high awareness about sudden cardiac arrest treatment, and the presence of well-known manufacturers in this market are some of the important factors that contribute to the growth of this market. The need for training in cardiopulmonary resuscitation and public access defibrillation is also contributing to the rapid adoption of resuscitation devices in healthcare settings and public places.

Resuscitation Devices Market Growth Drivers:

-

Rising Incidence of Sudden Cardiac Arrest and Cardiovascular Diseases Driving Market Growth

The rising number of cases of cardiovascular diseases and sudden cardiac arrest is one of the major factors propelling the growth of the global resuscitation devices market. Cardiovascular diseases are the major cause of death across the world. Therefore, there is a constant and increasing need for emergency resuscitation equipment that has the potential to restore heartbeats and respiratory functions in the case of sudden cardiac arrest. Automated external defibrillators, ventilators, and airway management devices are extremely important for the stabilization of patients with heart problems or respiratory problems.

In this regard, healthcare providers are investing in advanced resuscitation technologies to help increase survival rates and prevent any complications that may arise as a result of delayed medical care. The expansion of pre-hospital emergency care services is also contributing to the increased use of resuscitation equipment in healthcare facilities worldwide.

For example, in February 2025, emergency medical response units across several developed healthcare systems reported that the availability of automated external defibrillators in ambulances improved survival rates from out-of-hospital cardiac arrest by more than 30%, demonstrating the life-saving importance of early defibrillation.

Resuscitation Devices Market Restraints:

-

High Equipment Costs and Training Requirements Restricting Market Expansion

The high costs involved in the usage of advanced resuscitation equipment and the need for training of the health care personnel may prove to be a major restraint for the growth of the resuscitation devices market. The advanced equipment, including ventilators, wearable cardioverter defibrillators, and advanced airway management devices, demands a high amount of investment from the health care sector. Also, the usage of advanced equipment demands training of the health care personnel in the field of emergency health care and resuscitation procedures.

In the case of the health care sector of developing countries, the low funding and infrastructure in the field of emergency health care may prove to be a restraint for the growth of the resuscitation devices market. The different regulations in the different regions may result in a time lag in the approval of the products.

Resuscitation Devices Market Opportunities:

-

Expansion of Pre-Hospital Emergency Care and Public Access Defibrillation Programs

The growth of pre-hospital emergency care infrastructure and the increasing trend of public access defibrillation offer a significant opportunity for the portable resuscitation devices market. The governments and health organizations worldwide are encouraging the installation of automated external defibrillators in public areas like transportation centers, schools, shopping centers, and sports arenas. This will help in the immediate response to any cardiac arrest situation in public areas.

Innovations in portable resuscitation devices, including lightweight ventilators and wearable cardiac monitors, have enabled the growth of the portable resuscitation devices market. The recent advancements in the development of portable and easy-to-use devices, even for non-medical personnel, have provided an opportunity to improve the accessibility of these devices in public areas. This will play a major role in improving the survival rates and enhancing the emergency health infrastructure in the world.

For instance, in January 2025, several public health authorities launched nationwide AED accessibility programs aimed at increasing the number of publicly available defibrillators by more than 40% within five years, further accelerating the adoption of resuscitation technologies.

Resuscitation Devices Market Segment Analysis:

-

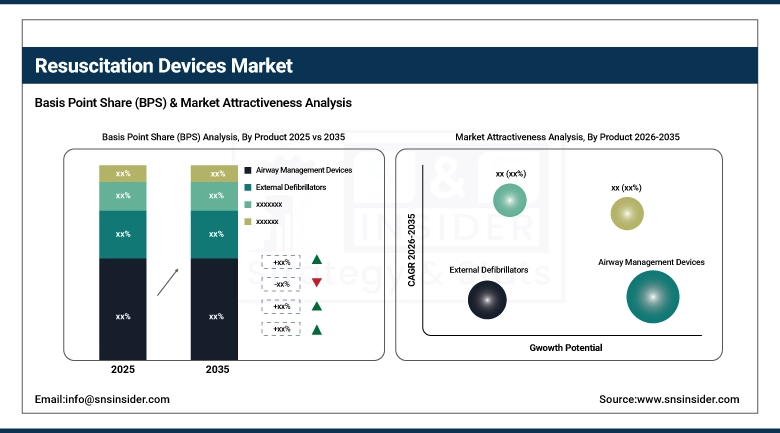

By product, airway management devices accounted for the largest share of approximately 39.64% in 2025, while the external defibrillators segment is anticipated to exhibit the fastest growth with a CAGR of 5.26% over the forecast period.

-

By patient type, adult patients represented the highest market share of around 78.21% in 2025, while the pediatric patients segment is expected to grow at a CAGR of 5.12% during the forecast period.

-

By end user, hospitals, ambulatory surgical centers, and cardiac centers held the dominant market share of nearly 61.37% in 2025, while the pre-hospital care settings segment is projected to register the fastest growth at a CAGR of 5.43%.

By Product, Airway Management Devices Dominate, While External Defibrillators Show Strong Growth

The airway management devices segment had the highest share of the market for resuscitation devices in 2025, given the critical importance of airway patency during emergency procedures. Various devices such as ventilators, endotracheal tubes, resuscitators, tracheostomy tubes, laryngeal mask airways, and laryngoscopes have found extensive use in emergency rooms and ICUs to manage respiratory failure. In addition, the prevalence of respiratory disorders, trauma, and surgery complications is a major driver of growth for airway management devices.

The external defibrillators market is expected to grow at the highest rate during the forecast period, considering the increasing prevalence of sudden cardiac arrests. Automated external defibrillators and wearable cardioverter defibrillators have found critical importance in emergency response situations, both in hospitals and community settings, because of their ability to restore a normal heart rhythm during cardiac arrests.

By Patient Type, Adult Patients Segment Leads the Market

The adult patients segment held the maximum share in the resuscitation devices market in 2025, which is about 78.21% of the total revenue generated. The high prevalence rate of cardiovascular diseases, respiratory disorders, and age-related medical conditions in adult patients has increased the demand for resuscitation devices in healthcare facilities. On the other hand, the pediatric segment is likely to grow as medical equipment for children and neonates is advancing.

By End Use, Hospitals Lead While Pre-Hospital Care Settings Grow Rapidly

Hospitals, ambulatory surgery centers, and cardiac centers were the major resuscitation devices market share in 2025, with a share of almost 61.37% of the overall market share. These centers are the primary providers of emergency services and are equipped with advanced equipment for life support. However, the pre-hospital care settings segment is expected to witness the highest growth rate in the forecast period. This is because of the increasing need to improve the response time of emergency services. Ambulance services and response teams are a part of the pre-hospital care settings segment.

Resuscitation Devices Market Regional Highlights:

North America Resuscitation Devices Market Insights:

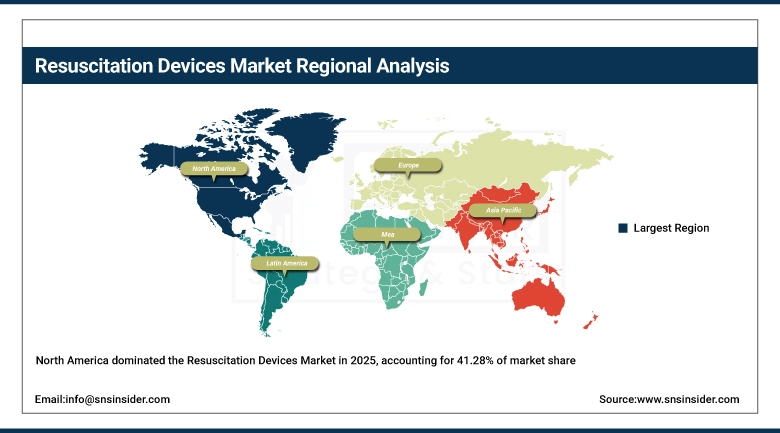

The highest market revenue share was reported by the North American market with a revenue share of around 41.28% in 2025. This is because the healthcare infrastructure is well developed in the region, and the focus is given to the development of emergency medical response systems. The availability of automated external defibrillators in hospitals, airports, schools, and workplaces has improved the quality of emergency care for patients with heart problems.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Resuscitation Devices Market Insights:

The Asia Pacific market for resuscitation devices is expected to witness the highest growth and is anticipated to expand at a CAGR of around 5.36% during the forecast period. Urbanization and investments in healthcare infrastructure are the major growth drivers for the resuscitation devices market. Cardiovascular diseases are also prevalent in countries such as China and India. Governments in the Asia Pacific are investing more in healthcare services such as emergency healthcare services and ambulance services. This is also increasing the demand for resuscitation equipment.

Europe Resuscitation Devices Market Insights:

The second-largest market for resuscitation devices is the European market. The healthcare infrastructure and government regulations for medical devices are well developed in the region. Initiatives are being taken by the government to improve the availability of defibrillators and emergency medical training programs.

Latin America (LATAM) and Middle East & Africa (MEA) Resuscitation Devices Market Insights:

The resuscitation devices market in Latin America and the Middle East & Africa is experiencing gradual growth due to increasing healthcare investments and the development of emergency medical services infrastructure. The growing adoption of portable medical equipment and improvements in hospital facilities are expected to support market expansion in these regions over the coming years.

Resuscitation Devices Market Competitive Landscape:

Medtronic plc utilizes its strong expertise in cardiovascular and critical care technologies to develop advanced ventilators, airway management systems, and emergency cardiac devices designed to improve patient survival during life-threatening medical emergencies.

-

In February 2025, the company introduced an upgraded portable ventilator platform designed for emergency transport and intensive care settings, offering improved oxygen delivery precision and enhanced patient monitoring capabilities.

Koninklijke Philips N.V. focuses on providing innovative resuscitation and emergency response solutions, particularly automated external defibrillators and patient monitoring systems integrated with digital healthcare platforms.

-

In January 2025, the company launched a next-generation automated external defibrillator featuring real-time CPR guidance and wireless connectivity for emergency medical response teams.

Stryker Corporation specializes in life-saving emergency medical equipment, including defibrillation systems and advanced patient monitoring solutions designed for both hospital and pre-hospital emergency care environments.

-

In December 2024, the company expanded its automated external defibrillator portfolio with a lightweight portable model designed for public access defibrillation programs.

Resuscitation Devices Market Key Players:

-

Medtronic plc

-

Koninklijke Philips N.V.

-

Stryker Corporation

-

ZOLL Medical Corporation

-

GE Healthcare

-

Drägerwerk AG & Co. KGaA

-

Smiths Medical

-

Fisher & Paykel Healthcare

-

Ambu A/S

-

Getinge AB

-

Mindray Medical International Limited

-

Nihon Kohden Corporation

-

Asahi Kasei Medical

-

Laerdal Medical

-

Teleflex Incorporated

-

Becton, Dickinson and Company

-

Spacelabs Healthcare

-

Schiller AG

-

Intersurgical Ltd.

-

Allied Healthcare Products

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 8.72 Billion |

| Market Size by 2035 | USD 13.86 Billion |

| CAGR | CAGR of 4.74% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Airway Management Devices (Ventilators, Endotracheal Tubes, Resuscitators, Tracheostomy Tubes, Laryngeal Mask Airways, Laryngoscopes, Nasopharyngeal Airways, and Oropharyngeal Airways), External Defibrillators (Semi-automated External Defibrillators, Fully Automated External Defibrillators, Wearable Cardioverter Defibrillators), Convective Warming Blankets, and Other Resuscitation Devices) • By Patient Type (Adult Patients, Pediatric Patients) • By End User (Hospitals, Ambulatory Surgical Centers, and Cardiac Centers, Pre-hospital Care Settings, and Other End Users) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Medtronic plc, Koninklijke Philips N.V., Stryker Corporation, ZOLL Medical Corporation, GE Healthcare, Drägerwerk AG & Co. KGaA, Smiths Medical, Fisher & Paykel Healthcare, Ambu A/S, Getinge AB, Mindray Medical International Limited, Nihon Kohden Corporation, Asahi Kasei Medical, Laerdal Medical, Teleflex Incorporated, Becton, Dickinson and Company, Spacelabs Healthcare, Schiller AG, Intersurgical Ltd., Allied Healthcare Products |

Frequently Asked Questions

The global Resuscitation Devices Market was valued at USD 8.72 billion in 2025 and is projected to reach USD 13.86 billion by 2035.

The market is expected to grow at a CAGR of 4.74% during the forecast period from 2026 to 2035.

Key growth drivers include the rising incidence of sudden cardiac arrest, increasing cardiovascular and respiratory diseases, expansion of emergency medical services, and growing adoption of automated defibrillators and portable ventilation systems.

Airway management devices held the largest share in 2025, accounting for approximately 39.64% of the global market.

North America dominates the global market, accounting for around 41.28% of total revenue in 2025, driven by advanced healthcare infrastructure and widespread deployment of defibrillation devices.

Get in Touch