Rutile Market Report Scope & Overview:

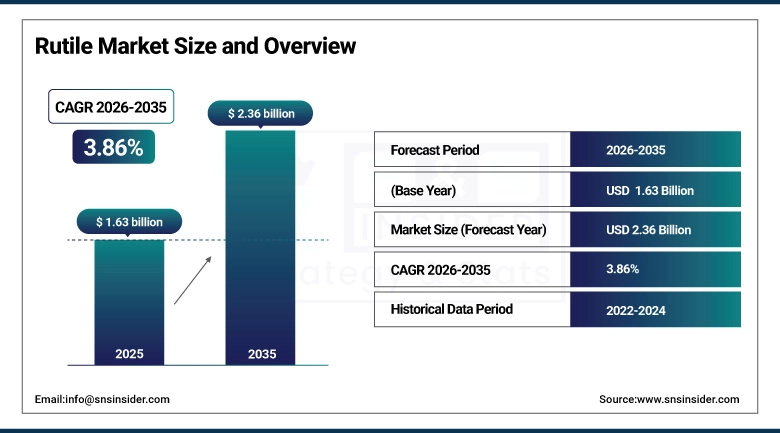

The Rutile Market was valued at USD 1.63 Billion in 2025 and is expected to reach USD 2.36 Billion by 2035, growing at a CAGR of 3.86% from 2026-2035.

Growth in Rutile Market has been attributed to increased demand for quality-grade titanium dioxide in paints, coatings, plastic, and ceramic industries, apart from its growing use in electronics, personal care, and welding sectors. Increased industrial activities, infrastructural developments, and automobile manufacturing have played an important role in driving the consumption of rutile. Progress in terms of high purity and artificial rutile manufacturing, together with increasing consciousness about sustainable materials, has been contributing to market growth.

For instance, China’s titanium dioxide production reached 4.72 million tons in 2025, down 1% year-over-year, with rutile-type TiO₂ accounting for 4.103 million tons, or 86.9% of total output from 36 full-process enterprises.

Market Size and Forecast:

- Market Size in 2025: USD 1.63 Billion

- Market Size by 2035: USD 2.36 Billion

- CAGR: 3.86% from 2026 to 2035

- Base Year: 2025

- Forecast Period: 2026–2035

- Historical Data: 2022–2024

To Get more information on Rutile Market - Request Free Sample Report

Rutile Market Trends:

- Rising demand for titanium dioxide production in paints, coatings, and plastics is driving the rutile market.

- Growing use in welding electrodes, ceramics, and refractory applications is boosting market growth.

- Expansion of construction, automotive, and packaging industries is fueling rutile consumption.

- Increasing focus on high-purity rutile for specialty applications is shaping adoption trends.

- Advancements in mining, processing, and pigment-grade rutile production are enhancing quality and efficiency.

- Rising global infrastructure development and industrialization are supporting market expansion.

- Collaborations between mineral producers, pigment manufacturers, and end-use industries are accelerating innovation and market penetration.

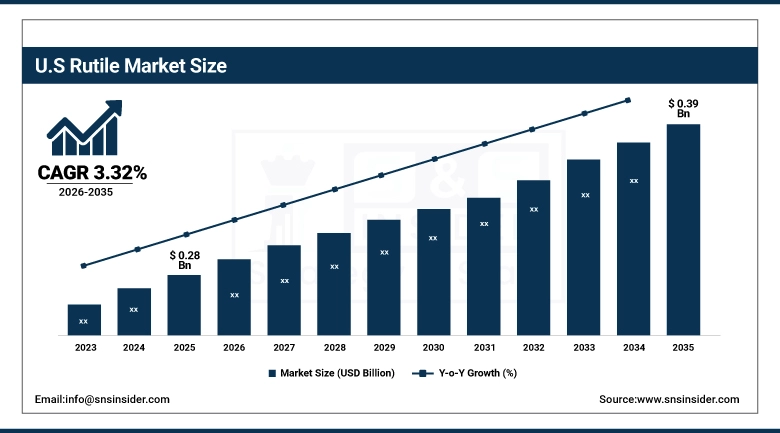

The U.S. Rutile Market was valued at USD 0.28 billion in 2025 and is expected to reach USD 0.39 billion by 2035, growing at a CAGR of 3.32% from 2026-2035.

Rutile market in the U.S. is expanding owing to increased consumption from paints, coating, plastic, and electronics sectors, aided by sophisticated manufacturing facilities, extensive use of high purity rutile, and growing usage in personal care and specialized industrial goods.

Rutile Market Growth Drivers:

- Increasing demand for high-quality titanium dioxide in paints and coatings is fueling significant growth in the global Rutile Market

Rising usage of titanium dioxide extracted from rutile in paints, coatings, and plastics will be an important contributing factor behind the expansion of the market. Rutile offers improved luminosity, hardness, and chemical stability which is vital for its utilization across industries as well as for consumers. The increased number of construction work, automobile manufacturing, and use of high-performance plastic products have resulted in higher consumption of rutile. Also, preference for paints that are eco-friendly and durable in nature will contribute to the usage of rutile.

In the U.S., in 2024, one company produced ilmenite and rutile from surface deposits at Nahunta, Georgia, and Starke, Florida, whereas another produced ilmenite from tailings, meeting more than 95 percent of demand for TiO₂ pigment manufacturers.

Titanium mineral concentrate production by U.S. facilities, which includes rutile, increased to 300,000 metric tons in 2022 compared to 200,000 tons in 2021, mainly used as feedstock for TiO₂.

Rutile Market Restraints:

- Volatility in raw material availability and limited high-grade rutile deposits restricts market growth potential globally

An unequal availability of natural rutile resources and dependence on only specific mining locations results in problems with supply chains. Inadequate availability of quality rutile leads to increased costs of titanium dioxide and its derivatives production. Geopolitical issues, restrictions on mining activities, and environmental considerations may contribute to additional limitations to rutile extraction. Changes in price that are associated with supply difficulties or increased costs of extraction will negatively affect industrial use and development of rutile-related applications. The requirement for complicated processes of processing inferior grades of rutile or manufacturing substitutes creates extra difficulties for producers and limits rutile market expansion.

Rutile Market Opportunities:

- Expanding application of rutile in advanced electronics, personal care, and cosmetic industries opens new growth avenues

The unique optical attributes of rutile, together with its ability to resist UV rays and its chemical stability, make it an ideal choice for use in electronics, sunscreens, and cosmetics. Rising demand from consumers of quality and long-lasting personal care products provides new directions for exploiting the benefits of rutile. The rise of semiconductors and optoelectronics further propels innovation in applying the material. Furthermore, the move towards multi-functional materials for paints, pigments, and nanomaterials provides companies with new options to broaden their range of products. R&D activities aimed at producing improved rutile derivatives for the above applications can lead to lucrative opportunities.

Rutile Market Segment Highlights:

- By Particle Size, Medium Particle Size dominated the Rutile Market with ~36% share in 2025; Fine Particle Size fastest growing (CAGR).

- By Application, Paints & Coatings dominated the Rutile Market with ~30% share in 2025; Personal Care fastest growing (CAGR).

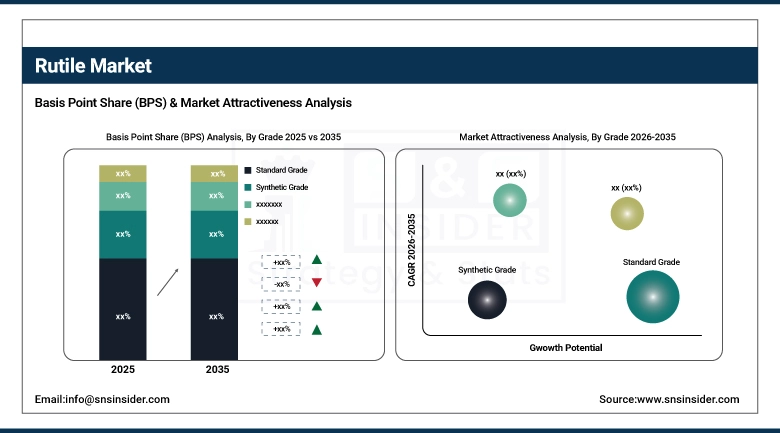

- By Grade, Standard Grade dominated the Rutile Market with ~31% share in 2025; Synthetic Grade fastest growing (CAGR).

- By Level, High Purity dominated the Rutile Market with ~39% share in 2025; High Purity fastest growing (CAGR).

- By Source, Titanium Ore dominated the Rutile Market with ~40% share in 2025; Titanium Ore fastest growing (CAGR).

Rutile Market Segment Analysis:

By Grade, Standard Grade segment dominates the Market, Synthetic Grade segment expected to grow fastest

Segment Standard Grade led the market in terms of revenue share during 2025, owing to its affordability and versatile uses in paints, coatings, ceramics, and welding operations. The overall performance of the product grade is satisfactory for industry needs without any specific treatment process. The high availability, lower manufacturing cost, and application in traditional processes have made it the top choice among companies globally. The Synthetic Grade segment is forecasted to exhibit the highest CAGR between 2026-2035 owing to the increasing use of high-grade, quality, and superior-performance rutile in various industries. The product grade's stable chemical composition and superior qualities make it suitable for advanced electronics, coatings, and other applications.

By Source, Titanium Ore segment dominates the Market, Titanium Ore segment expected to grow fastest

Titanium Ore Segment emerged as the most dominant in the Rutile Market with the largest market share revenue-wise in 2025 since it provides the primary feedstock for the manufacture of titanium dioxide, and it is highly available and affordable. The Titanium Ore segment is projected to record the highest growth rate during the forecast period of 2026-2035 due to growing industrialization, rising demand from paints and coatings applications, and automotive applications, and increased exploration of titanium ore reserves.

By Particle Size, Medium Particle Size segment dominates the Market, Fine Particle Size segment expected to grow fastest

The Medium Particle Size section held the largest share of revenue in the Rutile Market in 2025 because of its broad range of applications in the paints, coating, ceramic, and welding industries. The particle size is distributed evenly and delivers excellent performance and efficiency. Companies favor this segment due to its ease of manufacturing, processing, and handling.

The Fine Particle Size market segment will register the highest CAGR during the forecast period of 2026-2035 due to increasing application demand for high technology, personal care, and electronics. The increased surface area and high reactivity improve the optical and UV protective characteristics of zinc oxide particles. Thus, it is widely used in premium products and applications.

By Application, Paints & Coatings segment dominates the Market, Personal Care segment expected to grow fastest

The Paints & Coatings category accounted for the largest market share in terms of revenue generation in 2025 owing to the excellent reflective ability, opacity, and durability offered by rutile. Its chemical stability improves paint quality and ensures color integrity. The extensive use of rutile in building coatings, vehicle coatings, and industrial coatings contributes to its dominance in the market.

The Personal Care segment is forecast to experience the highest CAGR from 2026-2035 due to the growing demand for sunscreens, UV blockers, and cosmetics. Due to the chemical stability and optics of rutile, its application in the Personal Care industry is quite promising for skin, hair, and personal care applications. The growing consumer interest in functional and premium personal care products will drive its growth.

By Level, High Purity segment dominates the Market, High Purity segment expected to grow fastest

High Purity held the largest share of the Rutile Market with maximum revenues in 2025 on account of its excellent chemical stability and minimum amount of impurities, making it suitable for use in advanced industry. Due to its high purity attributes, the product has immense potential for application in industries like electronics, coatings, and ceramics. High Purity is set to have the highest CAGR from 2026-2035 owing to the increasing requirements of premium quality products in advanced industries around the globe.

Regional Analysis:

Asia Pacific Rutile Market Insights

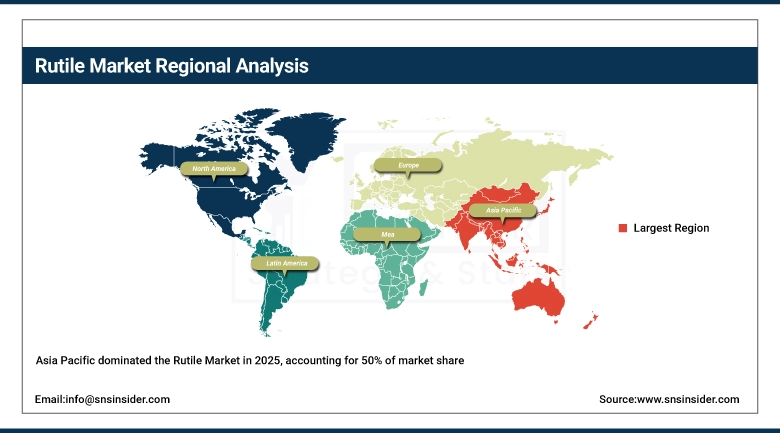

In terms of revenue generation, the Asia Pacific region emerged as the dominant player in the Rutile Market, contributing up to 50% of the global market revenue in 2025. This is attributed to the availability of significant amounts of natural deposits of rutile and large-scale mining activities in countries such as Australia and India. Additionally, the fast pace of industrialization, increased demand for construction materials, automobiles, paints, and coatings, and increased production and demand for high-quality titanium dioxide have contributed to market growth.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Rutile Market Insights

North America in the Rutile Market is driven by strong demand from the paints, coatings, and automotive industries. The region benefits from established manufacturing infrastructure, high adoption of advanced technologies, and growing applications in electronics and personal care products. Availability of high-quality rutile and synthetic alternatives, coupled with regulatory support for industrial development, ensures steady consumption, making North America a significant contributor to the global rutile market growth.

Europe Rutile Market Insights

The Europe region is predicted to exhibit the highest CAGR of around 5.58% during the forecast period of 2026-2035 due to higher industrialization, increased demand for pure rutile in electronic products, specialty coatings, and automobiles, and more focus on advanced manufacturing techniques. The rise in end-user sectors, sustainable and high-performance material usage, and R&D investments is driving the market. This makes the Europe region one of the fast-growing regions in terms of rutile consumption and applications.

Middle East & Africa and Latin America Rutile Market Insights

Steady growth is seen in Middle East & Africa and Latin America because of factors such as rising industrialization, development in the building and automobile industry, and high demands in the paint and coating sector, among others. The existence of mineral sands and rutile ores in some countries also plays an important role in their production. In addition, increased investment in infrastructure, among others, is also boosting rutile consumption in these regions.

Competitive Landscape:

Iluka Resources is one of the most dominant firms in the minerals sands industry, with an emphasis on the production of zircon, rutile, and synthetic rutile. The firm serves as a major supplier of feedstock material for titanium dioxide pigments, welding, ceramics, and advanced technologies. Sustainability is one of Iluka’s key areas of focus, along with efficiency and project development.

- 2024: Iluka’s production reached 496 kt; Balranald project construction progressed with commissioning planned in H2 2025, supporting future synthetic rutile supply expansion.

- 2025: Iluka suspended Cataby and SR2 synthetic rutile production due to weak demand, with existing inventories sufficient to satisfy customer requirements.

Tronox Holdings is an integrated manufacturer of titanium dioxide pigments and mineral sands feedstocks such as rutile. It is a leading supplier in the global coating, plastic, and industrial market sectors. The company strives towards sustainable business practices through renewable energy use, process efficiencies, and environmental conservation. Tronox continuously improves its mining and pigment manufacturing processes without compromising the quality of the titanium feedstock that supports pigment manufacturing and other industrial uses.

- 2023: No specific rutile-focused news was released; Tronox’s operations continued producing titanium feedstocks across its mining and pigment facilities.

- 2024: Tronox signed a ~200 MW wind and solar energy agreement to reduce emissions across mining and mineral sands operations.

Rio Tinto is an international mining group that produces a range of commodities, such as mineral sand products including ilmenite, zircon, and rutile. It emphasizes efficiency, sustainability, and projects at strategic sites, such as Richards Bay Minerals. Innovation and environmental management are part of Rio Tinto’s mining operations, which also provides high-grade titanium products used as pigments, in industrial products, and other specialty uses. Rutile output supplements the diverse sources of TiO₂.

- 2024: Richards Bay Minerals plans to resume Zulti South mineral sands expansion producing ilmenite, zircon, and rutile, pending updated feasibility studies.

Chemours Produces titanium dioxide pigments, which include rutile and anatase types of TiO2 products. The company has sustainability in its manufacturing processes, carbon footprint reduction in product development, and regulatory adherence. Innovation is incorporated by Chemours in pigment manufacturing, providing a variety of special TiO2 types with enhanced performances. Chemours produces TiO2 pigments globally and for different markets that range from industrial to decorative to specialty markets.

- 2023: Chemours introduced a lower-carbon Ti-Pure sustainability grade TiO₂ pigment, improving processing efficiency and reducing carbon footprint for rutile applications.

- 2024: Chemours paused TiO₂ production at Altamira, Mexico, due to regional drought, impacting supply continuity for rutile pigment customers.

- 2025: Chemours launched Ti-Pure TS-6706 TMP/TME-free rutile TiO₂ pigment, addressing regulatory and customer demands in coatings applications.

Kronos Worldwide is a pigment company producing rutile and anatase titanium dioxide pigments for use in coatings and plastics. They have their chloride and sulfate production plants, and they emphasize quality and innovation in their operations. The company prioritizes efficiency and the management of its production capacities to ensure the sustainability of pigment supply chain systems worldwide. Their rutile titanium dioxide pigments are suitable for high performance in coating and industrial uses.

- 2023: Kronos’ annual report confirmed ongoing production and sales of rutile and anatase TiO₂ pigments and operation of the Lake Charles rutile slurry facility.

- 2024: Kronos’ 10-K details ownership of Louisiana Pigment Company and continued rutile TiO₂ production via chloride and sulfate processes.

ISK Corporation is a Japanese manufacturer that produces rutile titanium dioxide used in coatings and electronics. Innovation, consistency, and flexibility are the primary values of ISK in the titanium dioxide industry. The company employs cutting-edge technology and sustainable practices in manufacturing TiO2 products. Rutile TiO2 products of the company cater to industrial and electronic materials customers.

- 2023: No specific rutile-focused press; ISK’s TiO₂ product portfolio supports industrial and electronic applications.

- 2024: ISK raised TIPAQUE TiO₂ product prices in Asia-Pacific, reflecting regional TiO₂ market dynamics.

- 2025: High-purity TiO₂ development highlighted in Chemical Industry Daily, demonstrating ISK’s continued focus on rutile applications in electronics.

Rutile Market Key Players:

-

Iluka Resources Limited

-

Tronox Holdings plc

-

Rio Tinto Group

-

Kenmare Resources plc

-

Base Resources Limited

-

Sierra Rutile Limited

-

Kerala Minerals & Metals Ltd.

-

V V Mineral

-

TiZir Limited

-

Chemours Company

-

Lomon Billions Group

-

Kronos Worldwide, Inc.

-

Venator Materials PLC

-

ISK (Ishihara Sangyo Kaisha)

-

CNNC Hua Yuan Titanium Dioxide Co., Ltd.

-

Shandong Doguide Group

-

Group DF

-

Tayca Corporation

-

East Minerals

-

IREL (India) Limited

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.63 Billion |

| Market Size by 2035 | USD 2.36 Billion |

| CAGR | CAGR of 3.86% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Grade (Standard Grade, Synthetic Grade, Natural Grade, High Grade, Low Grade, AR Grade) • By Source (Titanium Ore, Ilmenite Ore, Rutile Sand) • By Application (Welding and Cutting, Glass and Ceramics, Paints and Coatings, Electronics, Personal Care, Foundry Industry, Refractories) • By Level (High Purity, Medium Purity, Low Purity, Ultra High Purity) • By Particle Size (Fine Particle Size, Medium Particle Size, Coarse Particle Size, Ultrafine Particle Size) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Iluka Resources Limited, Tronox Holdings plc, Rio Tinto Group, Kenmare Resources plc, Base Resources Limited, Sierra Rutile Limited, Kerala Minerals & Metals Ltd., V V Mineral, TiZir Limited, Chemours Company, Lomon Billions Group, Kronos Worldwide, Inc., Venator Materials PLC, ISK (Ishihara Sangyo Kaisha), CNNC Hua Yuan Titanium Dioxide Co., Ltd., Shandong Doguide Group, Group DF, Tayca Corporation, East Minerals, IREL (India) Limited |

Frequently Asked Questions

The Rutile Market is expected to reach USD 2.36 Billion by 2035.

The Rutile Market was valued at USD 1.63 Billion in 2025.

The Rutile Market is projected to grow at a CAGR of 3.86% from 2026 to 2035.

The market is anticipated to grow by approximately USD 0.73 Billion between 2025 and 2035.

Growth is driven by rising demand for titanium dioxide pigments, welding electrodes, and aerospace-grade titanium products.

Get in Touch