SaaS-based Core Banking Software Market Report Scope & Overview:

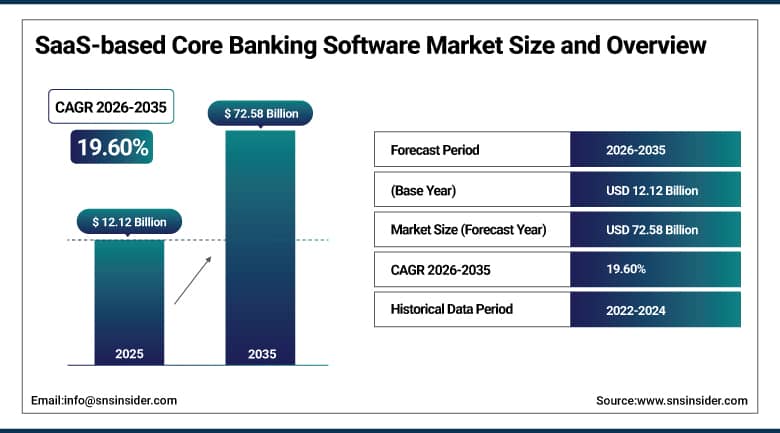

The SaaS-based Core Banking Software Market was valued at USD 12.12 Billion in 2025 and is expected to reach USD 72.58 Billion by 2035, growing at a CAGR of 19.60% from 2026 to 2035.

The SaaS-based Core Banking Software Market is experiencing significant growth owing to digital transformation among financial institutions and high demands for cloud-enabled core banking platforms. Financial institutions and service providers are leveraging SaaS core banking software to cut down on operational expenses, make their operations scalable, quicken the time to market for their offerings, and provide a better customer experience. High demand for payments processing in real-time, open banking, APIs and artificial intelligence-based banking services is fueling the growth of the market. Moreover, increased adoption of fintech, higher regulatory compliance, and remote accessibility for banking is fostering steady market growth.

78% of banks deployed SaaS-based core banking platforms leveraging AI, real-time data, and cloud scalability to cut operating costs by 30%, reflecting how quickly cloud-native infrastructure has moved from experimental pilot to mainstream operating model across the banking sector.

Market Size and Forecast

-

Market Size in 2026E: USD 14.50 Billion

-

Market Size by 2035: USD 72.58 Billion

-

CAGR: 19.60% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On SaaS-based Core Banking Software Market - Request Free Sample Report

SaaS-based Core Banking Software Market Trends

-

Rising digital transformation initiatives across the banking sector are pushing institutions toward scalable, flexible, and cost-effective SaaS-based core banking platforms.

-

Cloud-based platforms are increasingly the default choice for banks looking to boost operational efficiency, sharpen customer experience, and enable real-time data access.

-

Growing demand for mobile and online banking keeps expanding the addressable market for cloud-native core banking infrastructure.

-

Integration of AI and analytics into core banking platforms is enabling increasingly personalized services, from tailored product recommendations to proactive fraud detection.

-

Regulatory compliance pressure continues pushing banks toward platforms that can demonstrate auditable, real-time reporting without heavy manual overhead.

The U.S. SaaS-based Core Banking Software Market Outlook

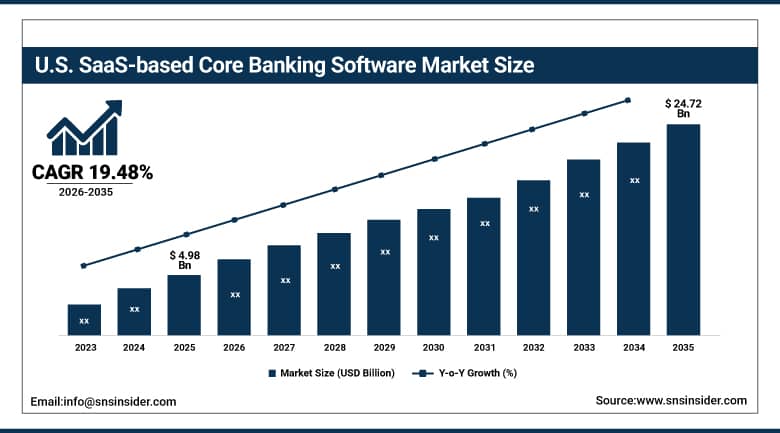

The U.S. SaaS-based Core Banking Software Market was valued at approximately USD 4.98 Billion in 2026 and is expected to reach approximately USD 24.72 Billion by 2035, growing at a CAGR of approximately 19.48%.

The U.S. market is being driven by banks' increasing focus on digital transformation, cloud adoption, and cost-efficient infrastructure that can flex with changing transaction volumes without requiring a multi-year hardware refresh cycle. Rising demand for real-time banking services, mobile and online platforms, and AI-powered analytics for enhanced customer experience keeps accelerating market growth across both large national banks and smaller regional institutions. The rapid shift toward digital banking and online financial services has meaningfully increased demand for flexible, scalable core banking systems, and American institutions in particular have been quick to treat cloud migration as a genuine competitive necessity rather than a discretionary IT upgrade.

Fiserv announced the general availability of its Digital Core Banking SaaS Platform in February 2025, unifying account processing, payments, and digital engagement into a single cloud-native stack designed to help U.S. banks modernize without the disruption of a traditional core replacement.

SaaS-based Core Banking Software Market Segment Analysis

-

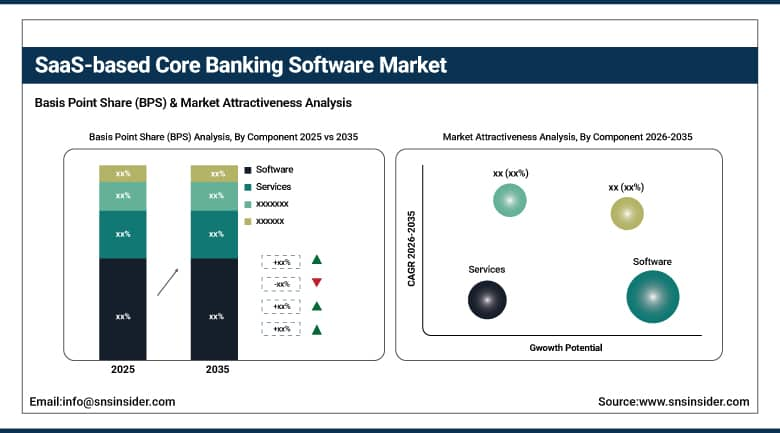

By Component, Software segment dominated the SaaS-based Core Banking Software Market in 2025 with 67% share; Services segment is the fastest growing segment.

-

By Deployment Mode, Public Cloud segment dominated the market in 2025 with 49% share; Hybrid Cloud segment is the fastest growing segment.

-

By Application, Retail Banking segment dominated the market in 2025 with 35% share; Digital Banking segment is the fastest growing segment.

-

By End User, Banks & Financial Institutions segment dominated the market in 2025 with 58% share; FinTech Companies segment is the fastest growing segment.

By Component, Software segment dominates the SaaS-based Core Banking Software Market, Services segment expected to grow fastest

The Software segment dominated the SaaS-based Core Banking Software Market in 2025 owing to growing preference for cloud-native core banking software that makes banking operations more efficient and improves the customer experience. There was a need for scalable software products to update legacy systems, ensure compliance with regulations, and facilitate real-time transactions. Innovations in artificial intelligence, analytics, open banking APIs, and cybersecurity further drove the need for software, which became the biggest revenue contributor in the market.

The Services segment is the fastest-growing because of the growing demand for implementation, integration, consulting, migration, and managed services offered by SaaS-based core banking software providers to their customers. Financial institutions sought help from specialized service providers for a seamless transition to cloud computing, cybersecurity, and optimal performance of systems.

By Deployment Mode, Public Cloud segment dominates the SaaS-based Core Banking Software Market, Hybrid Cloud segment expected to grow fastest

The Public Cloud segment dominated the SaaS-based Core Banking Software Market in 2025 owing to its cost-effectiveness in deployment, scalability, availability, and lesser infrastructure management. The rising usage of public cloud by banks for faster digital transformation and improved efficiency in launching new products has helped the segment grow. Moreover, innovations in cloud security, compliance, disaster recovery, and artificial intelligence-powered banking applications have contributed towards the growing popularity of public clouds.

The Hybrid Cloud segment is the fastest-growing due to growing needs of flexibility in banking operations by combining both public and private clouds. It enables banks to maintain their sensitive workloads on secure private cloud infrastructure while scaling up customer-focused applications through the public cloud. Rising regulatory requirements, data sovereignty, and business continuity needs are fueling the need for hybrid cloud solutions.

By Application, Retail Banking segment dominates the SaaS-based Core Banking Software Market, Digital Banking segment expected to grow fastest

The Retail Banking segment dominated the SaaS-based Core Banking Software Market in 2025 as a result of the huge numbers of customer accounts, transactions, loans, and payments processed by the retail banks. More and more banks started to implement SaaS-based core banking systems in order to offer personalized digital solutions, increase operational efficiencies, and facilitate omnichannel banking services. Customer demands for mobile banking, fast payments, and account management became the key drivers of the adoption of core banking software solutions among retail banks.

The Digital Banking segment is the fastest-growing due to the growing preference of consumers towards mobile and online banking solutions. Banks have been spending more money on implementing cloud-native solutions that allow instant account opening, digital lending, artificial intelligence-based customer service, and real-time payment features. Expansion of open banking, fintech partnerships, and personalized financial services became the main driver of digital banking adoption.

By End User, Banks & Financial Institutions segment dominates the SaaS-based Core Banking Software Market, FinTech Companies segment expected to grow fastest

Banks & Financial Institutions dominated the SaaS-based Core Banking Software Market in 2025 owing to the fact that banks use the core banking platform to manage deposits, loans, payments, customer accounts, and regulatory requirements. Increased spending on digital transformation, efficiency improvement, cyber security, and cloud migration drove the adoption of SaaS-based solutions. The increasing need for scalable, secure, and real-time core banking systems was another factor driving the growth of this market segment.

The FinTech Companies segment is the fastest-growing as financial services providers use SaaS-based core banking software to roll out innovative solutions at reduced infrastructure costs. Cloud-native solutions help in scaling operations, API integrations, embedded finance, and providing digital customer experience. The rising investment in digital payments, neobanking, lending platform, and Banking-as-a-Service (BaaS) models drive the adoption of core banking software solutions in FinTech companies.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.30% |

|

Europe |

United Kingdom |

25.40% |

|

Asia Pacific |

China |

29.85% |

|

Middle East & Africa |

UAE |

27.60% |

|

Latin America |

Brazil |

37.20% |

North America SaaS-based Core Banking Software Market Insights

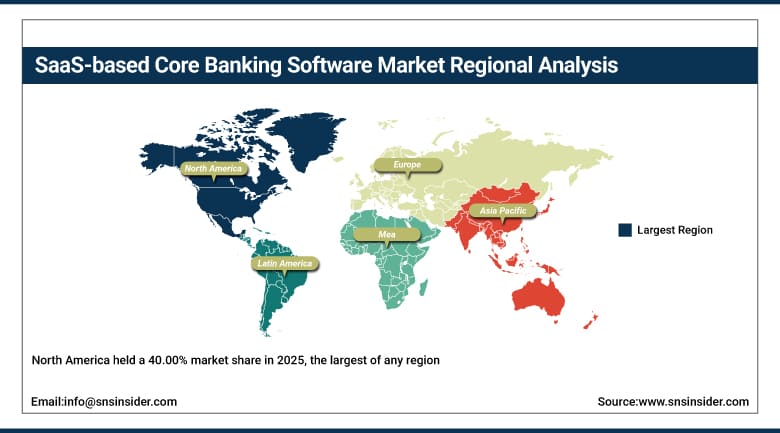

North America held a 40.00% market share in 2025, the largest of any region, attributed to its advanced financial services industry, prevalence of digitized banking solutions, and presence of key SaaS core banking service providers. The domination of this region was further reinforced due to increasing demand for automated and scalable cloud core banking systems that are able to serve both big national and small community banks that modernize their IT infrastructure at the same time.

About 82.30% of total revenue comes from the US region, driven by its advanced financial services sector, technological developments, and regulatory landscape that has been favorable for cloud transition. Banks migrate to cloud systems from traditional on-premise solutions in order to meet regulations and provide improved customer experience, scalability, and cost-efficiency, while Canada contributes to the demand in the region through its development in banking industry that transitions to cloud-native solutions.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe SaaS-based Core Banking Software Market Insights

In 2025, Europe accounted for an important share of the market for core banking software based on SaaS technology because of the development of its banking sector infrastructure, regulation, and digital banking solutions adoption across its leading economies. The growing interest in cloud core banking solutions, fintech solutions implementation, and banking process automation have made the Europe region one of the real contributors to market revenue growth.

The United Kingdom is a leader in regional demand accounting for around 25.40% of the European revenue, due to London being the global financial center and relatively dynamic fintech environment that has forced banks to adopt cloud solutions faster than in other neighboring countries. Germany and France are important contributors in terms of demand as well, and further regulation harmonization in the EU will make European demand for cloud core banking grow constantly throughout the forecast period.

Asia Pacific SaaS-based Core Banking Software Market Insights

The Asia Pacific region will witness the fastest CAGR of around 21.90% during the forecast period from 2025 to 2035 on account of quick digital transformation in the region's banking sector, high adoption of financial technology that is cloud-based, and increase in demand for core banking software that is scalable and efficient in the largest economies of the region.

China has the highest share of the regional revenue, which is around 29.85%, as a result of quick digital transformation in the banking industry in China and development in the fintech industry backed by the government. The other regions are India, Japan, and South Korea, where India, in particular, is poised to be a growth engine for cloud-native core banking software adoption.

MEA & Latin America SaaS-based Core Banking Software Market Insights

Middle East & Africa and Latin America both recorded healthy gains within the SaaS-based core banking software market in 2025, thanks to the growth of the banking industry, increasing investments in cloud and digital technology solutions for finance infrastructure, and increased governmental efforts towards the transformation of financial services. Being still in the early stages of establishing digital banking solutions, cloud native platforms are found to be a cost-effective method of bypassing investments into legacy IT infrastructure.

In the Middle East & Africa region, the UAE dominates the market share, accounting for around 27.60%, due to the governmental efforts to establish itself as a financial center and the ambitions to build a state-of-the-art financial infrastructure. Saudi Arabia and South Africa help to drive regional demand through the efforts of modernizing their economies. In Latin America, Brazil remains the biggest contributor of regional revenues with a share of around 37.20%.

Market Dynamics

Growth Drivers: Digital transformation and demand for scalable banking infrastructure

Increasing digital transformation initiatives across the banking sector, combined with rising need for scalable, flexible, and cost-effective banking solutions, sit at the core of this market's growth. Banks and financial institutions are adopting cloud-based platforms specifically to enhance operational efficiency, improve customer experience, and enable real-time data access, and that combination of operational and customer-facing benefit has made cloud migration a genuinely strategic priority rather than a back-office IT decision. Growing demand for mobile and online banking is reinforcing this shift further, as customer expectations around instant, always-available service have made legacy batch-processing infrastructure increasingly untenable.

Regulatory compliance requirements and the integration of AI and analytics for personalized services are adding a second, reinforcing layer of demand behind this transformation. Banks need platforms that can demonstrate auditable, real-time compliance reporting without heavy manual overhead, and the same cloud-native architecture that enables that reporting also makes it far easier to layer in AI-driven personalization, fraud detection, and predictive analytics. That dual benefit, compliance efficiency paired with customer-facing intelligence, is exactly what's kept SaaS-based core banking adoption climbing so quickly across institutions of every size.

Restraints: Data security concerns and legacy system migration complexity

Migrating decades-old core banking infrastructure to a cloud-native platform is a genuinely complex undertaking, and that complexity remains one of the more persistent restraints on faster market adoption. Banks carry enormous volumes of sensitive customer and transaction data, and moving that data to cloud infrastructure raises legitimate security and data-sovereignty concerns that risk-averse institutions, particularly larger, more heavily regulated banks, are often reluctant to move past quickly.

The technical complexity of migrating away from legacy mainframe systems without disrupting live banking operations adds a further layer of restraint, since even a brief service interruption during a core banking migration can carry real reputational and regulatory consequences. Smaller institutions with limited IT resources often find this migration risk particularly daunting, which helps explain why adoption, while accelerating, hasn't moved uniformly fast across every tier of the banking industry.

Opportunities: FinTech partnerships and AI-driven personalization

Growing collaboration between traditional banks and fintech companies represents a genuinely significant opportunity for SaaS-based core banking providers, as banks increasingly look to fintech partnerships to accelerate their own digital transformation rather than building every capability from scratch internally. Cloud-native core banking platforms are proving to be the natural connective tissue for these partnerships, since they're built with the API-driven architecture fintechs already expect.

Deeper integration of AI-driven personalization represents a second substantial opportunity, as banks increasingly compete on the quality of customer experience rather than product features alone. Vendors that can help institutions deliver genuinely tailored product recommendations, proactive fraud alerts, and predictive service offerings stand to capture real advantage as banks consolidate around fewer, more capable core banking platforms in the years ahead.

Recent Developments:

-

2025: Fiserv announced the general availability of its Digital Core Banking SaaS Platform, unifying account processing, payments, and digital engagement in a single cloud-native stack.

-

2025: nCino, Inc. announced the acquisition of Sandbox Banking, aiming to offer digital banking solutions with improved data connections and streamlined operational capability.

-

2024: Oracle launched its Digital Core for Banking as a fully managed SaaS solution on Oracle Cloud Infrastructure, targeting retail, corporate, and digital banks.

SaaS-based Core Banking Software Market key players are:

-

Oracle Corporation

-

Fiserv Inc.

-

TEMENOS AG

-

Q2 Holdings Inc.

-

nCino Inc.

-

MeridianLink Inc.

-

Alkami Technology Inc.

-

Backbase

-

Mambu B.V.

-

MX Technologies Inc.

-

Thought Machine Group Limited

-

Finxact LLC

-

Alacriti Infosystems Private Limited

-

Hyland Software Inc.

-

Antier Solutions Private Limited

-

Itexus LLC

-

Apiture Inc.

-

Advapay OU

-

Dashdevs LLC

-

Vine Financial Inc.

SaaS-based Core Banking Software Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 12.12 Billion |

| Market Size by 2035 | USD 72.58 Billion |

| CAGR | CAGR of 19.60% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Software, Services) • By Deployment Mode (Public Cloud, Private Cloud, Hybrid Cloud) • By Application (Retail Banking, Corporate Banking, Digital Banking, Wealth Management, Payment & Transaction Processing) • By End User (Banks & Financial Institutions, Credit Unions, Microfinance Institutions, Non-Banking Financial Companies (NBFCs), FinTech Companies) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Oracle Corporation, Fiserv Inc., TEMENOS AG, Q2 Holdings Inc., nCino Inc., MeridianLink Inc., Alkami Technology Inc., Backbase, Mambu B.V., MX Technologies Inc., Thought Machine Group Limited, Finxact LLC, Alacriti Infosystems Private Limited, Hyland Software Inc., Antier Solutions Private Limited, Itexus LLC, Apiture Inc., Advapay OU, Dashdevs LLC, Vine Financial Inc. |

Frequently Asked Questions

The SaaS-based Core Banking Software Market is expected to grow at a CAGR of 19.60% from 2026 to 2035.

The SaaS-based Core Banking Software Market was valued at USD 12.12 Billion in 2025.

The major growth factor is increasing digital transformation initiatives in the banking sector and rising demand for scalable, flexible, and cost-effective banking solutions.

The Software segment dominated the SaaS-based Core Banking Software Market with a 67% share by component in 2025.

North America dominated the SaaS-based Core Banking Software Market in 2025 with a 40.00% share of total global market revenue.

Get in Touch