Satellite Antenna Market Report Scope & Overview:

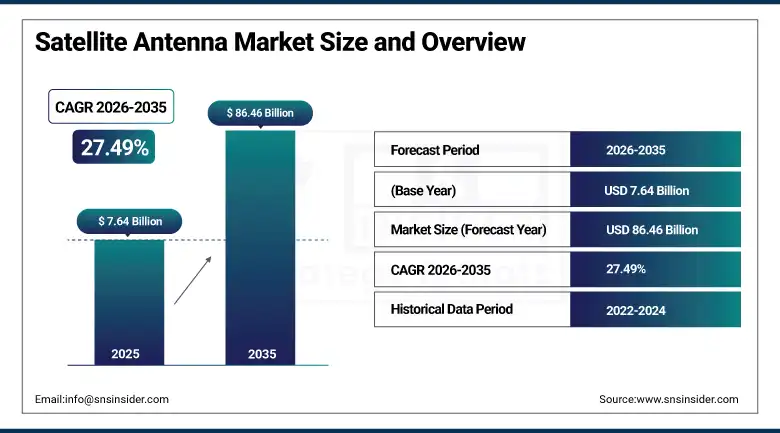

The Satellite Antenna Market was valued at USD 7.64 Billion in 2025 and is expected to reach USD 86.46 Billion by 2035, growing at a CAGR of 27.49% from 2026–2035.

The adoption of satellite communications is rapidly increasing in remote and underdeveloped regions. Digital connectivity gaps are being narrowed down with government policies around the world. The military use of satellite communication technology is driving regional developments, particularly in North America and Asia-Pacific. Modernization and need for defense are some other factors behind this development. The use of satellite IoT technologies is increasing in sectors like agriculture, marine, and logistics. With these technologies, remote monitoring and operation can be performed efficiently. Increased demand for satellite broadband has resulted in the installation of antennas in rural areas. Countries that do not have much fiber optic technology are relying on satellite communication technology. Every year, innovative products continue to enter the market.

According to a recent announcement from the United States’ Space Force in December 2024, the U.S. space force has plans to develop some antennas in view of upgrading the old satellite control network. This will be accomplished before the close of 2025 in order to meet increased demand. It is part of a trend that has been observed all over the world. Defense organizations everywhere are competing to ensure that their satellite communications are up to date.

Market Size and Forecast

-

Market Size in 2026E: USD 9.74 Billion

-

Market Size by 2035: USD 86.46 Billion

-

CAGR: 27.49% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Satellite Antenna Market - Request Free Sample Report

Satellite Antenna Market Trends

-

Low Earth Orbit satellite constellations from Starlink and Project Kuiper are improving global broadband penetration fast.

-

Phased array antenna technology is replacing traditional dish antennas for better mobile connectivity performance.

-

Satellite-enabled IoT applications are expanding rapidly across agriculture, maritime, and logistics tracking systems.

-

5G backhaul integration is creating new demand for satellite antennas in remote network areas.

-

Defense modernization programs are driving steady antenna upgrade cycles across military communication systems.

The U.S. Satellite Antenna Market Outlook

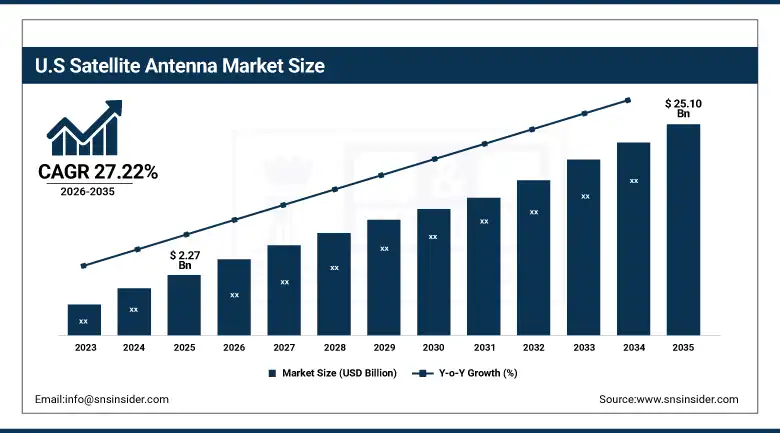

The U.S. Satellite Antenna Market was valued at approximately USD 2.27 Billion in 2025. It is expected to reach approximately USD 25.10 Billion by 2035. The market is growing at a CAGR of approximately 27.22%.

Development of satellites continues to fuel growth in the U.S. market. Increasing requirements for broadband Internet connectivity remain among the key factors contributing to this trend. The adoption rate of satellite communications in defense, telecommunications, and commercial segments increases. The rollout of 5G technology is likely to further contribute to it. The integration of satellite technology into IoT ecosystems also gains momentum. Manufacturers from different industries increasingly invest in the development of antenna technology.

In February 2024, C-COM Satellite Systems obtained the Eutelsat Type Approval for the iNetVu Ka-74G Antenna system. The approval enables the system to operate on Eutelsat’s broadband service portfolio. The approval process guarantees that the system meets all performance and safety requirements. The certification provides new opportunities for business growth for the manufacturer of satellite antennas. It demonstrates a close cooperation between satellite operators and antenna manufacturers.

Satellite Antenna Market Segment Analysis

-

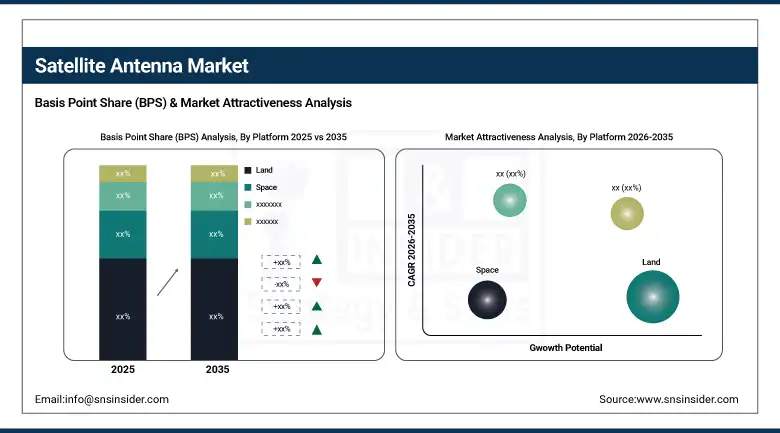

By Platform, land segment dominated the satellite antenna market with approximately 28% share in 2025. The airborne segment is growing fastest, driven by rising in-flight connectivity demand.

-

By Frequency, the Ku-band segment dominated the satellite antenna market with the largest share in 2025. The Ka-band segment is growing fastest, driven by high-throughput satellite demand.

-

By Technology, the SATCOM-On-the-Move segment dominated the satellite antenna market with approximately 59% share in 2025. The SATCOM On-the-Pause segment is growing fastest, driven by temporary field deployment needs.

By Platform, land dominates, airborne grows fastest

Land-based antennas have dominated the platform market share since 2025, accounting for around 28% of the market. The demand for better internet services in both cities and remote regions is what leads the pack. Communication infrastructure robustness has become increasingly important over time. Increasing smart city implementations and expanding IoT connectivity contribute to growth in this segment. Governments and firms continue their investments in the ground-based satellite network. Investments in ground-based satellite network infrastructure help bridge the connectivity gap in regions where fiber network connectivity is not possible. They are often more affordable compared to air- and sea-based connectivity solutions. They represent an economically sound choice for many connectivity initiatives. Telecom firms often deploy land-based terminals to expand their rural connectivity footprint.

Antennas that operate through airborne platforms are expanding at a much faster rate than other platform categories. The increasing demand for improved communication in the skies is the primary reason behind this growth. Aircraft used by commercial airlines, military aircrafts, and unmanned aerial vehicles all use satellite antenna systems. Every year there is a consistent rise in the number of passengers demanding for Wi-Fi and live television from airline flights. The airlines view this as one of the main areas to make their services stand out. For military aircrafts, reliable and secure communication is essential while performing their operations.

By Frequency, Ku-band dominates, Ka-band grows fastest

Ku-band held the largest frequency share in 2025. Widespread acceptance and established infrastructure both support this lead. Direct-to-home television services rely heavily on Ku-band technology. The 12 to 18 GHz frequency range offers reliable, high-quality communication. This makes it popular for broadcasting, maritime, and aeronautical services alike. Ku-band also offers strong resistance to weather-related signal disruption. Cost-effectiveness compared to higher frequency bands adds further appeal. Many established satellite networks were built around Ku-band from the start. This installed base gives Ku-band a durable advantage that newer bands will take years to match.

Ka-band is the fastest-growing frequency segment today. Better bandwidth and rising demand for high-throughput satellites both drive this growth. The 26.5 to 40 GHz range supports high-data-rate applications effectively. High-speed internet and high-definition video streaming both benefit from Ka-band capacity. Satellite operators are increasingly designing new systems around Ka-band technology. This shift reflects growing consumer and enterprise demand for faster data speeds. Enterprise customers requiring large data transfers are particularly drawn to Ka-band’s expanded capacity. As more high-throughput satellites launch in coming years, Ka-band adoption should keep accelerating well past the broader market average.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

24.6% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Satellite Antenna Market Insights

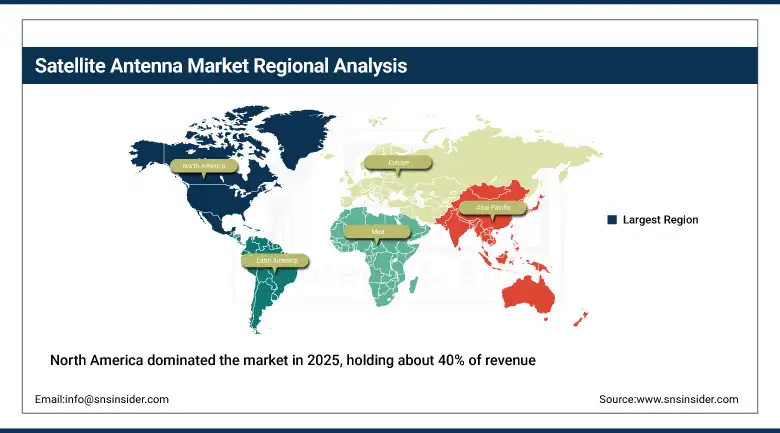

North America dominated the market in 2025, holding about 40% of revenue. Advances in high-throughput satellites and phased array antennas both support this lead. These technologies have improved system functioning and capability significantly. Satellite TV and direct-to-home services remain popular across the region. Defense procurement budgets in the United States and Canada also add steady regional demand.

The United States accounts for approximately 82.5% of North American revenue. Consumers continue seeking wide channel selection and varied content options. Major defense contractors and satellite operators are both based here. This concentration of expertise helps maintain regional leadership. Ongoing investment in next-generation satellite constellations should keep this advantage intact.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Satellite Antenna Market Insights

Europe is a significant satellite antenna market today. Strong aerospace manufacturing and growing defense modernization both support this position. Airbus SE runs major satellite communication operations across the continent. Germany accounts for approximately 24.6% of European revenue. France and the United Kingdom also host substantial satellite manufacturing capacity.

Rising demand for rural broadband connectivity is also boosting regional growth. The EU’s digital connectivity initiatives are pushing antenna adoption in underserved areas. Several European nations are investing in next-generation satellite infrastructure. This investment should sustain steady growth through the forecast period. Cross-border defense cooperation programs are also adding fresh procurement demand.

Asia Pacific Satellite Antenna Market Insights

Asia Pacific is expected to grow at the fastest CAGR through 2035. Rapid urbanization and rising demand for high-speed internet both drive this growth. Urban and rural areas alike need reliable connectivity solutions. Bridging the digital divide remains a key regional priority.

China accounts for approximately 44.8% of Asia Pacific revenue. Government-backed digital infrastructure programs keep adding new capacity. India’s satellite communication sector is also expanding quickly. This regional growth should keep outpacing the global average for years.

MEA & Latin America Satellite Antenna Market Insights

The UAE leads MEA revenue through strong government investment in satellite infrastructure supports this position. Defense and commercial broadcasting both contribute to regional demand. Saudi Arabia is also investing heavily in satellite connectivity for remote desert regions.

Brazil leads Latin American revenue through rural connectivity needs and growing defense spending both drive this lead. Mexico and Argentina contribute secondary demand through their own expanding satellite programs. Vast rural geography across the region keeps satellite connectivity a practical necessity.

Market Dynamics

Growth Drivers: Rising LEO satellite deployment and growing high-speed internet demand fueling antenna installations worldwide

Rising demand for high-speed internet is a major growth driver. Remote and rural areas especially need better connectivity for streaming and work. Low Earth Orbit satellite constellations are improving broadband access globally. Starlink and Project Kuiper are leading this expansion with rapid deployment schedules. Military, aviation, and maritime sectors are also adopting satellite-based communication faster. Large investments in satellite technology keep flowing into the industry every year. 5G backhaul integration and IoT ecosystem growth both add new demand layers. Falling launch costs are also making satellite deployment more affordable than ever before.

These trends together point toward steady, sustained market growth. Phased array antenna technology is improving performance for mobile and moving platforms. This makes satellite communication more practical across more applications than before. Defense modernization programs in North America and Asia Pacific add further momentum. As more satellites launch into orbit, ground equipment demand naturally follows. New manufacturing techniques are also reducing antenna production costs across the industry. This creates a self-reinforcing growth cycle across the entire satellite communication value chain.

Restraints: High installation and maintenance costs limiting adoption in developing regions

Installation and maintenance cost is another significant restriction that may be faced during deployment. Modern satellites have complicated and expensive components which may prevent small companies as well as some underdeveloped regions from using them. In addition to this, skilled manpower is required for maintenance and upgrading of satellite communication system which imposes an additional burden on its cost. Small markets usually lack manpower necessary to provide services related to the maintenance of this type of system.

In this regard, satellite communication systems face restrictions while being adopted by cost sensitive organizations and regions because of their price. Several manufacturers have started working on creating less expensive antennas. However, due to their complicated nature, they still cannot be considered cheap. Several financing plans and rental schemes have recently been proposed as possible ways for smaller companies to use modern satellites despite their cost.

Opportunities: LEO satellite growth enabling low-latency applications across IoT, autonomous vehicles, and smart cities

Increasing LEO satellite constellations present many opportunities. This includes having low-latency and fast speed communications for the next wave of innovations. Applications like IoT networks, driverless cars, and intelligent city systems can leverage from these advances. The government's effort to provide internet connection in poorly-served regions is another factor adding to potential opportunities. The manufacturing companies of satellite antennas will see an enormous benefit from the market development. Service providers that operate in rural and remote locations will experience an increased demand in their services.

With more and more industries moving into data-driven and connected business, demand will only rise. Agriculture, marine transport, and vehicle communication systems represent examples of sectors with a huge potential for future development. Antenna companies targeting these developing application fields have an excellent chance of becoming a leading player. The fall in satellite launch cost together with increased demand for data will make the market highly favorable for expansion. Collaboration between antenna producers and satellite organizations will likely increase innovations in products.

Recent Developments:

-

2024: The U.S. Space Force announced plans to field new antennas, upgrading its aging Satellite Control Network by the end of 2025 to address rising demand.

-

2024: C-COM Satellite Systems received Eutelsat Type Approval for its iNetVu Ka-74G antenna system, enabling its use across Eutelsat’s broadband service network.

-

2024: C-COM Satellite Systems suspended its quarterly dividend to prioritize research and development investment, reflecting a strategic shift toward future product innovation.

Satellite Antenna Market Key Players are:

-

Cobham Limited

-

Harris Corporation

-

Viasat Inc.

-

General Dynamics Mission Systems Inc.

-

L3Harris Technologies Inc.

-

Honeywell International Inc.

-

Airbus SE

-

Gilat Satellite Networks Ltd.

-

Hughes Network Systems LLC

-

Ball Aerospace

-

Comtech Telecommunications Corp.

-

Intellian Technologies

-

Kymeta Corporation

-

Maxar Technologies

-

Advantech Wireless

-

ThinKom Solutions Inc.

-

CPI International Inc. (ASC Signal)

-

EchoStar Corporation

-

ND SatCom GmbH

-

Norsat International Inc.

Satellite Antenna Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 7.64 Billion |

| Market Size by 2035 | USD 86.46 Billion |

| CAGR | CAGR of 27.49% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Platform (Land, Space, Maritime, Airborne) • By Technology (SATCOM-On-the-Move (SOTM), SATCOM On the Pause (SOTP)) • By Frequency (L Band, S-band, C-band, X-band, Ku-band, Ka-band, Q band, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Cobham Limited, Harris Corporation, Viasat Inc., General Dynamics Mission Systems Inc., L3Harris Technologies Inc., Honeywell International Inc., Airbus SE, Gilat Satellite Networks Ltd., Hughes Network Systems LLC, Ball Aerospace, Comtech Telecommunications Corp., Intellian Technologies, Kymeta Corporation, Maxar Technologies, Advantech Wireless, ThinKom Solutions Inc., CPI International Inc. (ASC Signal), EchoStar Corporation, ND SatCom GmbH, and Norsat International Inc. |

Frequently Asked Questions

The Satellite Antenna Market is expected to grow at a CAGR of 27.49% from 2026 to 2035.

The Satellite Antenna Market was valued at USD 7.64 Billion in 2025.

Rising LEO satellite deployment, growing high-speed internet demand, and increasing defense modernization spending are the primary growth factors.

The Land segment dominated the Satellite Antenna Market with approximately 28% share in 2025. The Airborne segment is growing fastest, driven by in-flight connectivity demand.

North America dominated the Satellite Antenna Market with approximately 40% revenue share in 2025.

Get in Touch