Self-Driving Car and Trucks Market Report Scope & Overview

Get more information on Self-Driven Cars and Trucks Market - Request Sample Report

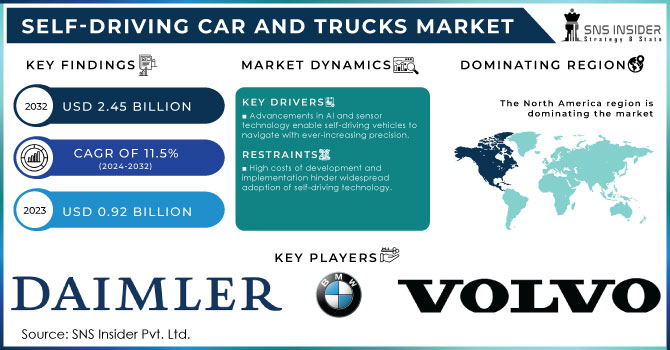

The Self-Driving Car and Trucks Market size was valued at USD 0.92 billion in 2023 and is expected to reach USD 2.45 billion by 2032 and grow at a CAGR of 11.5% over the forecast period 2024-2032.

The self-driving car and truck market are growing extremely fast with the advancements in the areas of artificial intelligence, sensor technology, and computing power. This enables more accurate operations and fewer accidents due to human error. SNS Insider research shows that 94% of all accidents in traffic are caused by human error; self-driving technology promises to make this percentage decrease up to 90%. It has been this emphasis, especially on road safety among businesses and governments aggressively pursuing this objective, that has been the key driver for adoption.

Consumers and businesses alike find themselves more and more drawn to the safety and sustainability benefits of self-driving vehicles. About 58% of consumers are interested in buying autonomous cars, while 63% of logistics companies are considering self-driving trucks as a means to reduce operational cost and achieve a quicker delivery schedule. Sustainability, on the other hand, is also an important factor; autonomous driving systems will optimize routes, reduce fuel consumption, and potentially lower carbon emissions by as much as 20%.

Government policies drove much of the development and deployment of self-driving vehicles. More than 30 countries established regulatory frameworks to facilitate testing and deployment of autonomous vehicles. For instance, 38 states in the United States have passed autonomous vehicle legislation, and a number of incentives for manufacturers and tech companies, which has increased investment in this sector to more than 45% over the last three years. Besides, direct investment is supplemented with partnerships between Original Equipment Manufacturers, technology companies, and venture capitalists. For example, giant automobile companies, such as General Motors, have undertaken joint ventures with technology companies like Waymo, boosting commercial readiness. Also, with a rising tide of familiarity with connected and autonomous technologies in daily applications, the tolerance for self-driving vehicles has grown 12% year-over-year, indicating growing confidence in this transportation revolution.

Self-Driving Car and Trucks Market Dynamics:

Drivers:

-

Advancements in AI and sensor technology enable self-driving vehicles to navigate with ever-increasing precision.

Advances in AI and sensor capabilities have greatly enhanced the ability of self-driving cars to drive in extremely high-precision terms. For instance, through vast volumes of real-time information coming from LiDAR, radar, and cameras, cars can even identify obstacles, detect road signs, and make split-second decisions through AI algorithms. Such technologies thus enable autonomous systems to interpret complex driving environments and adapt accordingly to changing states, such as weather conditions or changes in traffic flow. New LiDAR sensors can create high-definition 3D maps and even achieve an accuracy of up to 95% on object detection, which considerably enhances the reliability and safety of autonomous navigation.

Restrains:

-

High costs of development and implementation hinder widespread adoption of self-driving technology.

The major challenge in the adoption of self-driving technology on large scales is the cost of higher development and implementation. Most investment needed comes in terms of developing advanced sophisticated AI systems, advanced sensors such as LiDAR and radar, and very powerful computing hardware required in developing autonomous vehicles. For instance, the cost of a single LiDAR sensor can range from as low as USD 1,000 to as high as USD 75,000, depending on how much resolution is required and would add significantly to the vehicle's overall cost.

In addition to this, a constant demand for regular testing, software updates, and maintenance with respect to existing standards raises the operational costs. Such high overhead costs and operating costs make it difficult to offer cheap autonomous vehicles, which limits adoption, particularly among price-sensitive consumers and small businesses. While future economies of scale may allow for lower prices, the current high cost reduces the pace of quickened commercialization and acceptance of self-driving technology.

Self-Driving Car and Trucks Market Segmentation Analysis:

By Application:

The Self-Driving Cars and Trucks Market can be classified under personal, commercial, and defense applications each having its own growth dynamics. Under the personal use category, approximately 58% of consumers who are interested in the vehicle for convenience and safety will see mass adoption limited by higher costs and safety concerns. Commercial applications, particularly in logistics, grew more rapidly at 63% in logistics companies at their end to cuts costs and render operations efficient by considering self-driving trucks. These trucks with autonomous capabilities optimize fuel consumption to as much as 15-20% higher efficiency and run non-stop without driver fatigue, hence highly being game-changers in long-haul transportation. On the other hand, the defense sector also invests heavily in research in developing autonomous vehicles for unmanned ground operations that would certainly ensure improved safety and operational efficiency in combat zones. Going forward, governments in countries such as the U.S. and China will have to spend more than 25% of their military budget on autonomous systems. In totality, the diversified applications are driving the growth rate of the autonomous vehicle market.

By Technology:

Basic needs include LiDAR, radar, cameras, and ultrasonic sensors to detect objects and map the environment. The precision for detecting an object may go up to 95% levels directly increasing the safety levels during navigation. Computing power is another critical component as the processing power required by the autonomous vehicles must be vast in order to analyse sensor data in real-time and make decisions in a fraction of a second. The high-performance processors and AI accelerators allow processing thousands of megabytes, while advancement in computing power nearly doubles the decision-making speed in the last couple of years. Lastly, software development pervades the life of the autonomous vehicle, incorporating advanced AI algorithms, machine learning, and real-time mapping technologies which facilitate cars to navigate complex environments. Continuous updates and upgrades in the software form the basis of fine-tuning performance and how there is an expectation that the accelerated improvements in AI would reduce human-error-related accidents to 90%.

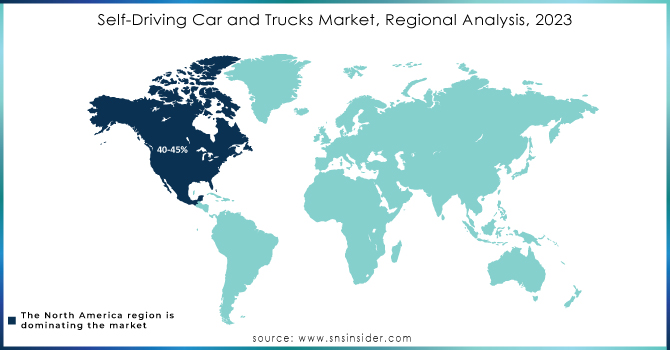

Self-Driving Car and Trucks Regional Analysis:

North America has been at the forefront of the Self-Driving Car and Trucks Market, with an estimated share of approximately 40-45%. This can be primarily attributed to an already developed automotive industry, supported by strong research and development capabilities. These places are well supported in terms of government regulations and a huge consumer population with a keen interest in the application of the newest technologies. In addition, supportive infrastructure like high-quality roads is another factor that makes North America a stalwart leader in the market.

In contrast, the Asia Pacific region presents itself as one of the fast-growing markets, with a growth rate of 20%, led by rapidly expanding economies, growing disposable incomes, and an increased demand for efficient transportation solutions. The region's enormous manufacturing base for traditional vehicles offers a strategic advantage in adopting self-driving technology mainly because it lowers production costs. That means, in addition to economic growth, coming hand-in-hand with technological adoption, positions the Asia Pacific as a critical player in the future of autonomous vehicles.

Get Customized Report as per your Business Requirement - Request For Customized Report

Key Players:

Some of the major Self-Driving Car and Trucks Market key players are:

-

AB Volvo: (Volvo XC90, Volvo VNL)

-

BMW,: (BMW iX, BMW 7 Series)

-

Daimler AG: (Mercedes-Benz EQS, Freightliner Cascadia)

-

Isuzu Motors Limited: (Isuzu D-MAX, Isuzu Giga)

-

Clear Path Robotics: (OTTO 1500, OTTO 100)

-

tesla: (Tesla Model S, Tesla Cybertruck)

-

Toyota Motor Corp: (Toyota Highlander (with advanced driver assistance features), Toyota Mirai (with autonomous tech developments))

-

Volkswagen AG: (Volkswagen ID.4, Volkswagen Transporter (with automation technologies))

-

Ford: (Ford Mustang Mach-E, Ford F-150 Lightning (with advanced driver assist systems))

-

Waymo: (Waymo One (self-driving ride-hailing service), Waymo Via (autonomous delivery service))

-

Nuro: (R2 (autonomous delivery vehicle), R1 (smaller autonomous vehicle for goods delivery))

-

Aurora Innovation: (Aurora Driver (autonomous driving technology for various vehicle types), Partnerships with various OEMs for integrated self-driving solutions)

Self-Driving Car and Trucks Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 0.92 Billion |

| Market Size by 2031 | US$ 2.45 Billion |

| CAGR | CAGR of 11.5% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Vehicle Type (Self-Driving Cars, Sedans, SUVs, Hatchbacks, Self-Driving Trucks, Delivery Trucks, Semi-Trucks, Heavy-Duty Trucks) • By Application (Personal, Commercial, Defence) • By Technology (Sensors, Computing Power, Software) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe [Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | AB Volvo, BMW, Dailmer, AG, Isuzu Motors Limited, Clear Path Robotics, tesla, Toyota Motor Corp, Volkswagen Ag, Ford |

| Key Drivers | • Rising traffic accidents fuel demand for self-driving cars with their superior safety features. • Advancements in AI and sensor technology enable self-driving vehicles to navigate with ever-increasing precision. |

| Restraints | • High costs of development and implementation hinder widespread adoption of self-driving technology. • Public concerns about safety and security of autonomous vehicles create resistance to full integration. |

Frequently Asked Questions

AB Volvo, BMW, Dailmer, AG, Isuzu Motors Limited, Clear Path Robotics, tesla, Toyota Motor Corp, Volkswagen Ag, Ford

Ans: The expected CAGR of the global Self-Driving Car and Trucks Market during the forecast period is 11.5%.

High cost and the new technology adaption

- North America is the fastest growing region

Ans: The Self-Driving Car and Trucks Market was valued at USD 0.92 billion in 2023.

Get in Touch