Self-locking Nuts Market Report Scope & Overview:

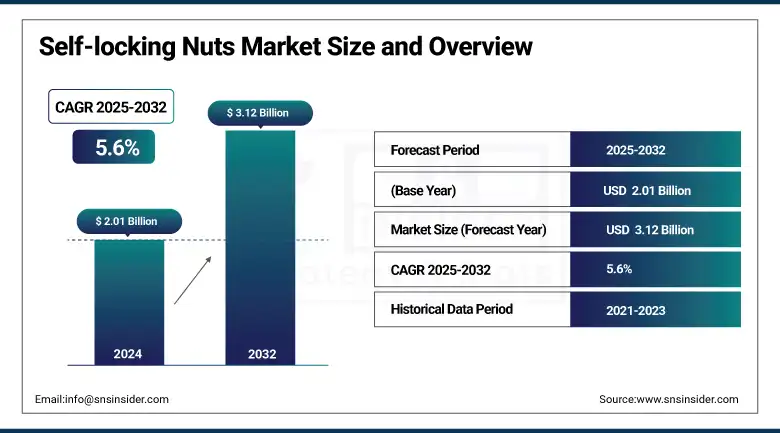

The Self-locking Nuts Market Size was valued at USD 2.01 billion in 2024 and is expected to reach USD 3.12 billion by 2032 and grow at a CAGR of 5.6% over the forecast period 2025-2032.

The market is growing at a steady rate with a rise in demand for vibration-free and secure fastening solutions across major industries, including automotive, aerospace, construction, and oil & gas. These nuts are designed to prevent loosening under vibration and torque without the need for other locking devices, ideal for safety applications. Material innovations such as lightweight alloys and corrosion-resistant coatings are improving product performance and broadening their acceptance in both OEM and aftermarket applications. Increasing industrial automation and infrastructure development, especially in developing countries, are also providing impetus to the market. New distribution channels are emerging as the trend toward direct supply contracts and online industrial platforms accelerates. It is anticipated that the demand for self-locking nuts will continue to grow as safety, product longevity, and operational efficiency become a greater concern for industries looking to increase efficiency and minimize waste in their assembly operations.

To Get more information On Self-locking Nuts Market - Request Free Sample Report

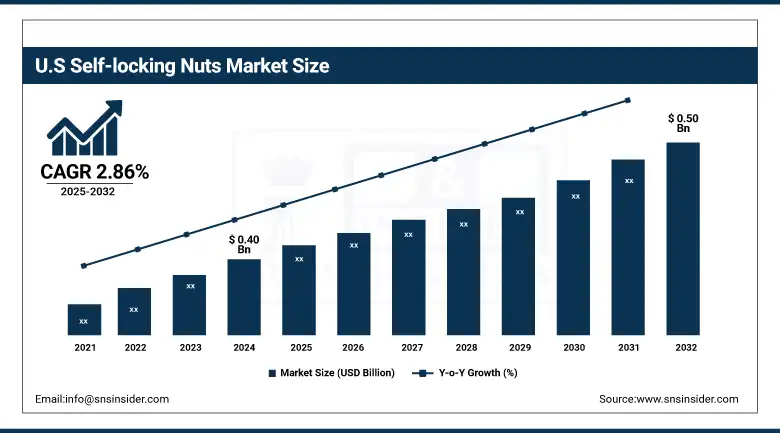

The U.S. Self-locking Nuts Market size was USD 0.40 billion in 2024 and is projected to reach USD 0.50 billion by 2032, growing at a CAGR of 2.86% from 2025 to 2032. In the automotive and aerospace industries, the demand is growing for safety and vibration resistance, which is also in high demand in the largest U.S. market. The U.S. is the biggest consumer in North America as it has a surplus of self-reliant defense industry, both the military and civil aviation, and other major OEMs. Meanwhile, continuous infrastructure developments and stringent quality criteria are driving solids gains in the market for industrial applications.

Market Dynamics

Key Drivers:

-

Rising Aerospace Production and Vibration-Sensitive Applications Drive Growth in the Self-locking Nuts Market

Rising demand for self-locking nuts in the aerospace industry, owing to their long-established use in high-vibration environments, will further boost the metallic nuts market. Aerospace OEMs are referencing fastening technology that provides structural safety and integrity during the most dynamic circumstances. Although commercial aircraft builds and international defense mod programs are leaving, pulling device demand stable in engine, airframe, and landing gear units. These nuts are able to secure other lock mechanisms and offer easy fitting and low maintenance. Relying less on mechanical failure and more on technique and performance, a greater impetus by aerospace engineers to self-locking nuts has become noticeable. This is leading product manufacturers to innovate and develop products that meet stringent industry certifications.

April 2024 HARD LOCK INDUSTRY CO., LTD. unveiled its HARDLOCK nuts in inch sizes for use in aerospace and defense end markets. The expansion was a direct response from the company to increasing requirements for high-performing self-locking fasteners to US and worldwide aviation standards.

Restraints:

-

Volatility in Raw Material Prices and Global Supply Chain Delays Restrain Market Expansion for Self-locking Nuts

The key limitation of the market is the unstable price of raw materials, such as steel and aluminum, and global supply chain issues. These ups and downs hit production costs and profit margins for both suppliers and OEMs. With strong metals like high-grade metal alloys used to create strong, corrosion-resistant locking devices, that industry is particularly sensitive to fluctuations in commodity markets. Moreover, the hangover of global logistics problems caused by post-pandemic port congestion and geopolitical uncertainty has contributed to erratic supply flows, longer lead times, and higher costs of procurement. Sellers often find it difficult to maintain price composure or guarantee on-time delivery to distributors and end customers, limiting operational efficiency and hampering growth prospects. The uncertainty of feedstock accessibility similarly prompts smaller producers to refrain from capacity expansion, missing a sales potential and losing a competitive edge.

Opportunities:

-

Growing Focus on Infrastructure Modernization Presents New Opportunities for Self-locking Nuts

The continued infrastructure development-led projects is continuing to open up of substantial prospects for the self-locking nuts market. Demand from federal and local investments in transportation networks, bridges, power grids, and public utilities is fueling the need for reliable and vibration-resistant fastening products. Self locking nuts are particularly useful in such applications, since they hold the fastening elements tightly together even when such elements are subject to dynamic forces, extreme temperatures and frequent maintenance. Being able to stop from loosening without using other fastening devices, these systems are also perfect for high-stress infrastructure applications. With the focus on long-term durability and structural safety in construction, rising construction activities will continue to fuel uptake of the self-locking nuts. This is driving manufacturers to diversify their product portfolio in line with the changing requirements of infrastructure developers and government contractors.

In April 2025, Huyett announced the launch of an expanded product line featuring over 60,000 industrial fasteners, including a wide range of lock nuts, specifically to meet the growing demands of infrastructure and construction markets. This development highlights how suppliers are responding proactively to capitalize on the infrastructure boom.

Challenges:

-

Standardization Challenges Across Industries Hinder Seamless Adoption of Self-locking Nuts Across Applications

Low standardization in specifications for different industries complicates the design, procurement, and application of self-locking nuts, which is a significant challenge for the market. While some industries, such as aerospace or automotive, have very strict norms, others, such as those in general construction or oil & gas, will refer to non-uniform specifications or local standards. Such a lack of uniformity results in poor interchangeability of fasteners between projects or types of equipment. It also leaves manufacturers dedicated to producing highly bespoke versions, complicating manufacturing and inventory. Additionally, it might be a problem for the end-users to get the right product for their own usage, which is a kind of waste for supply chains. These unstandardized processes play directly into production scale and inhibit market expansion, making penetration difficult, particularly for newcomers and in export-led growth.

Segmentation Analysis:

By Material

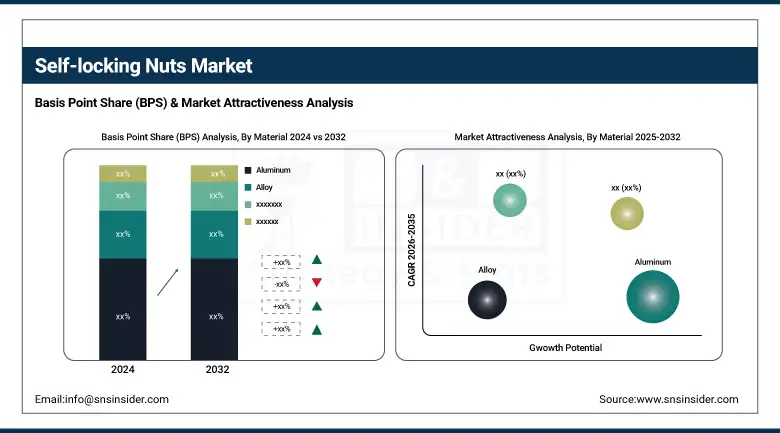

The aluminum segment dominated with over 30% revenue share in 2024, owing to its lightweight properties, corrosion resistance, and high strength-to-weight ratio. These characteristics render aluminum self-locking nuts suitable for use in aerospace, automotive, and electronics, where weight savings are essential. Furthermore, aluminum not only has a low manufacturing cost but is also relatively good at thermal conductivity, which is favorable to its usage in various industrial applications. All of these factors together make aluminum the leading material in self-locking nuts.

The alloy segment is expected to grow at the highest CAGR of 8.07% over the forecast period, on account of the increasing demand for high-performing materials capable of withstanding high loads and vibrations. Alloys provide excellent strength, fatigue resistance, and corrosion durability and are appropriate for heavy-duty applications like construction, oil & gas, and heavy equipment. Their high-stress capabilities are causing customers to become increasingly interested in alloy self-locking nuts for critical industrial applications.

By Distribution Channel

The direct distribution channel generated the highest revenue in 2024 and accounted for 58% of the total revenue due to strong demand from OEMs and large industrial users. Due to direct procurement, buyers can get custom specifications, bulk pricing, and quality assurance without an intermediary. This approach gives us greater control of the supply chain, as well as better technical support and longer-term reliability. That's why direct distribution is the best choice for industries seeking high-performance, application-specific self-locking nuts.

The indirect segment is projected to register a CAGR of 6.55% over the forecast period, owing to a rise in demand for distributors, resellers, and e-commerce sites. This direct sales channel will allow end-users easier access to a greater range of standard fasteners, such as self-locking nuts, particularly in parts of the world where manufacturers are not well represented. It provides an indirect channel to promote MRO business for SMEs and MROs, increases market penetration, and promotes the development of ‘non-direct sales’ business models.

By End-use Industry

In 2024, the automotive segment is dominating in the Self-locking Nuts Market share of around 29% and is also projected to grow at the highest CAGR of 7.86% during the forecast period 2025-2032, fueled by rising global vehicle production and growing emphasis on vehicle safety and reliability. Self-locking nuts are widely used in automotive assemblies, including engine compartments, suspensions, and chassis systems, to prevent loosening under vibration and dynamic loads. As electric vehicles and lightweight designs gain momentum, demand for secure and durable fastening solutions in the automotive industry continues to rise.

Regional Analysis:

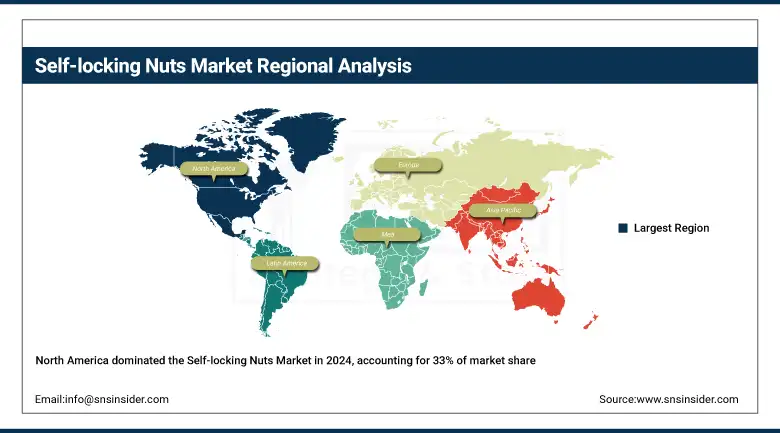

North America is the dominant player in the Self-Locking Nuts market share of around 33% in 2024, due to growing demand from the aerospace and automotive sectors supported by the established manufacturing sector and stringent safety regulations for fastening. United States dominates in North America with a strong aerospace and defense manufacturing capability along with continued investments in automotive technology. The country’s emphasis on critical application, high strength and vibration resistant bolting system will make it a leading player in self-locking nuts market.

Get Customized Report as per Your Business Requirement - Enquiry Now

In 2024, Asia Pacific is the fastest-growing region in Self-Locking Nuts with CAGR 10.14% during the forecast period 2025-2032, due to Rapid industrialization, infrastructure expansion, and increasing automotive production across emerging economies propel demand for self-locking nuts. China is the fastest-growing country in the Asia Pacific region, driven by its booming automotive and construction sectors. China’s extensive manufacturing base, coupled with rising adoption of advanced fastening technologies in rail, aerospace, and industrial equipment, significantly boosts market demand. Government-led infrastructure programs and export-focused production further solidify China’s position as a major contributor to regional market growth.

Europe is a Significant Regional Contributor in 2024. Germany remains the dominant country in Europe’s self-locking nuts market, driven by its world-class automotive and mechanical engineering sectors. Rising demand for durable fastening in electric vehicles, wind turbines, and industrial machinery drives Europe’s adoption of self-locking nuts.

Germany’s focus on high-performance automotive and renewable energy technologies has accelerated demand for advanced fastening components. The country’s precision engineering expertise and export-oriented manufacturing culture contribute to Europe’s steady market growth.

In 2024, the Middle East & Africa and Latin America regions are emerging markets in the self-locking nuts industry, showing moderate yet promising growth. MEA’s expansion is driven by large-scale oil & gas infrastructure and construction projects, particularly in countries like the UAE and Saudi Arabia, where vibration-resistant fastening is critical. In Latin America, Brazil leads with its growing automotive production and industrial manufacturing. Both regions are increasingly adopting durable, corrosion-resistant fastening solutions to improve mechanical reliability. Though still developing, rising industrial investments and infrastructure modernization are expected to support long-term market growth across these regions.

Key Players:

Self-locking Nuts Market Companies are Accu Limited Company, Bossard Group, Chin Hsing Precision Industry Co., Ltd, HARD LOCK INDUSTRY CO., LTD., Huyett, National Bolt & Nut Corp., Nord-Lock International AB, Penn Engineering, STARWDH INDUSTRIAL CO., LTD, Würth Industrie Service GmbH & Co. KG, Others.

Recent Developments:

-

In July 2024, Bossard completed the acquisition of Dejond Fastening NV, a Belgian manufacturer specializing in blind rivet nuts. This strategic move strengthens Bossard's portfolio in locking-device solutions, including self-locking nuts

-

In April 2024, Global Fastener News highlights that HARDLOCK launched its globally unique wedge‑principal two-piece self-locking nuts in inch sizes, demonstrating superior anti-loosening performance under rigorous NAS vibration tests, and emphasizing their reusability thanks to all-metal construction and precision design

| Report Attributes | Details |

| Market Size in 2024 | USD 2.01 Billion |

| Market Size by 2032 | USD 3.12 Billion |

| CAGR | CAGR of 5.6% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material (Steel, Brass, Aluminum, Alloy, Others) • By End-use Industry (Automotive, Aerospace, Construction, Oil & Gas, Others) • By Distribution Channel (Direct, Indirect) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Taiwan, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Accu Limited Company, Bossard Group, Chin Hsing Precision Industry Co., Ltd, HARD LOCK INDUSTRY CO., LTD., Huyett, National Bolt & Nut Corp., Nord-Lock International AB, Penn Engineering, STARWDH INDUSTRIAL CO., LTD, Würth Industrie Service GmbH & Co. KG, Others. |

Frequently Asked Questions

North America dominated the Self-locking Nuts Market in 2024.

The Aluminum segment dominated the Self-locking Nuts Market.

The major growth factor of the Self-locking Nuts Market is the increasing demand for vibration-resistant fastening solutions across automotive, aerospace, and infrastructure sectors.

The Self-locking Nuts Market size was USD 2.01 billion in 2024 and is expected to reach USD 3.12 billion by 2032.

The Self-locking Nuts Market is expected to grow at a CAGR of 5.6% during 2025-2032.

Get in Touch