AI-Based Climate Modelling Market Report Scope & Overview:

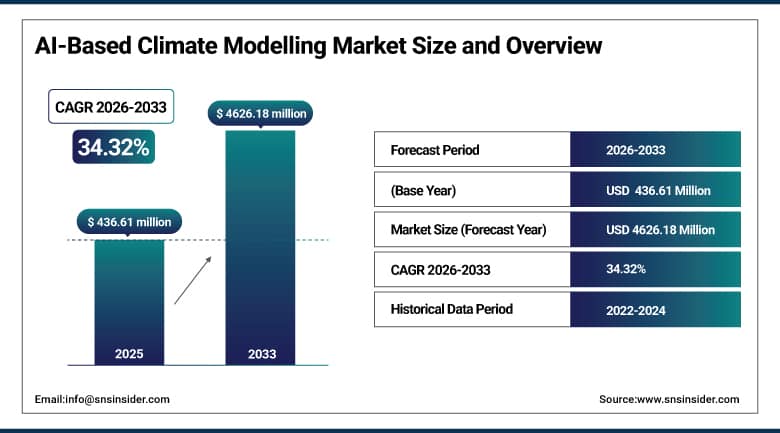

The AI-Based Climate Modelling Market is valued at USD 436.61 Million in 2025E and is expected to reach USD 4626.18 Million by 2033, growing at a CAGR of 34.32% during 2026-2033.

The AI-Based Climate Modelling Market is expanding quickly as there is an urgent need for accurate climate predictions, extreme weather events are happening more often, and governments and businesses around the world are putting more money into climate tech. AI and machine learning improve traditional climate models by analyzing huge amounts of data from satellites, IoT sensors, and historical records. This makes it possible to make more accurate predictions, assess risks better, and monitor the environment in real time. Integration with high-performance computing (HPC) and cloud platforms speeds up the use of this technology in meteorology, agriculture, disaster management, and planning for sustainable policies.

Over 76% of meteorological agencies globally adopted AI-enhanced climate modeling in 2025, improving forecast accuracy by up to 40% and reducing computational costs by 35% through cloud and machine learning optimization.

AI-Based Climate Modelling Market Size and Forecast

-

Market Size in 2025E: USD 436.61 Million

-

Market Size by 2033: USD 4626.18 Million

-

CAGR: 34.32% from 2026 to 2033

-

Base Year: 2025E

-

Forecast Period: 2026–2033

-

Historical Data: 2022–2024

To Get More Information On AI-Based Climate Modelling Market - Request Free Sample Report

AI-Based Climate Modelling Market Trends:

-

Increasing use of machine learning and deep learning to downscale global climate models for hyper-local weather and risk prediction.

-

Growth of cloud-based AI climate platforms enabling scalable, cost-effective modeling for research institutions and governments.

-

Integration of IoT and satellite data with AI models for real-time environmental monitoring and anomaly detection.

-

Rising deployment of AI in climate adaptation and resilience planning for agriculture, urban infrastructure, and insurance.

-

Advancements in hybrid AI-physical models combining numerical simulations with neural networks for improved forecasting accuracy.

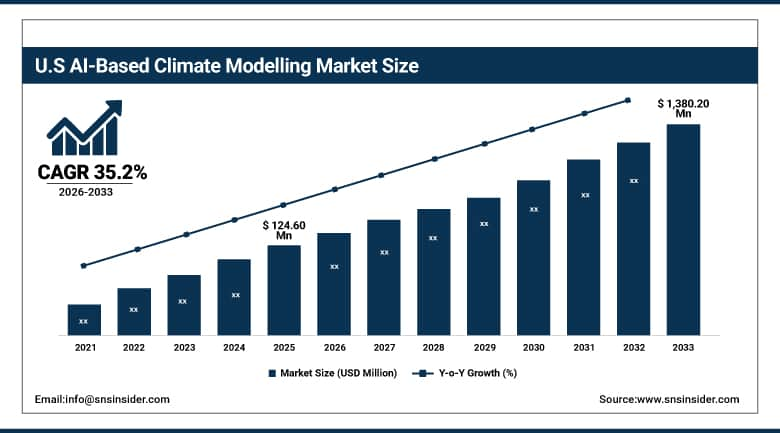

The U.S. AI-Based Climate Modelling Market size is valued at USD 124.60 Million in 2025E and is projected to reach USD 1,380.20 Million by 2033, growing at a CAGR of 35.2% during 2026–2033.

The U.S. dominates the regional market due to robust federal investments led by agencies such as NOAA, NASA, DOE, and NSF, along with the presence of major AI, cloud, and climate analytics providers. Early adoption of AI-driven climate models for extreme weather prediction, disaster resilience, carbon tracking, and climate risk assessment across energy, insurance, agriculture, and defense sectors is accelerating market growth. Strong private-sector funding, hyperscale cloud infrastructure, and public–private research collaborations further reinforce the U.S. leadership in AI-based climate modelling.

AI-Based Climate Modelling Market Growth Drivers:

-

Rising Frequency and Intensity of Climate-related Disasters Drive Demand for AI-enhanced Climate Models Globally

Climate change is making extreme weather events, such as hurricanes, floods, wildfires, and droughts worse, which means there is a growing need more accurate forecast models. AI and machine learning look at several types of data, including satellite images, historical climate data, and real-time sensors, to find trends and make forecasts more accurate. AI models help governments, disaster management agencies, and insurance companies plan for robust infrastructure and reduce economic losses. AI's better processing efficiency and capacity to scale up compared to classic physics-based models further speeds up its use.

In 2025, 71% of disaster response agencies used AI climate models, reducing false alarms by 30% and improving evacuation lead times by up to 48 hours for extreme weather events.

AI-Based Climate Modelling Market Restraints:

-

High Computational Costs, Data Quality Issues, and the “Black-Box” Nature of Complex AI Models Limit Trust and Adoption Among Traditional Climate Scientists and Policymakers

Training advanced AI climate models requires significant processing power, often reliant on expensive HPC or cloud resources. Many regions lack sufficient, high-quality labeled climate data for model training, leading to biases or inaccuracies. Moreover, deep learning models can be opaque, making it difficult to interpret predictions, which is a critical barrier in scientific and policy contexts where explainability is essential. These factors slow integration into operational forecasting and long-term climate planning.

About 62% of climate research institutions cited model interpretability and high cloud-compute costs as key challenges in transitioning from experimental AI models to operational systems in 2025.

AI-Based Climate Modelling Market Opportunities:

-

Expansion Of AI-Powered Climate Services for Agriculture, Renewable Energy, And Water Resource Management Offers High-Growth Verticals for Market Players

AI climate models are used in precision agriculture to predict droughts, pests, and the best times to plant, which makes crops more resistant. Energy businesses use AI to predict how much wind, solar, and hydropower they will make. Water companies use models to predict floods and droughts and manage reservoirs. These application-specific solutions offer recurring revenue potential through SaaS platforms and custom analytics, especially in areas that are vulnerable to climate change.

The Agri-climate AI segment grew by 42% in 2025, with adoption by over 350 large-scale farming cooperatives for yield optimization and risk mitigation.

AI-Based Climate Modelling Market Segment Highlights:

-

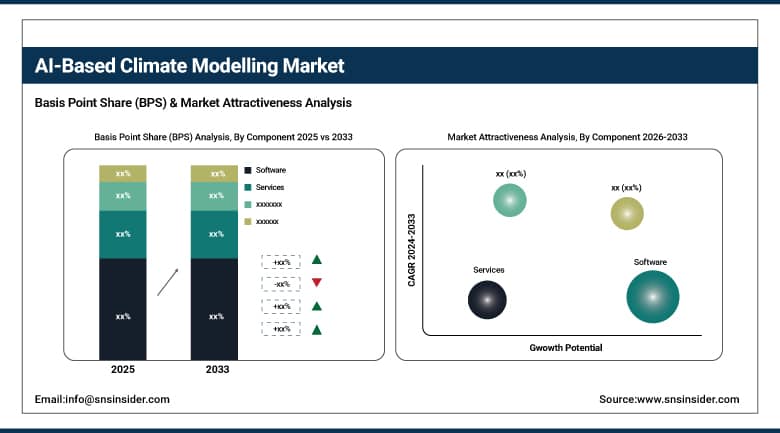

By Component: Software led with 61.4% share, while Services is the fastest-growing segment with a CAGR of 36.8%.

-

By Deployment: Cloud led with 58.9% share, while On-premises is the fastest-growing segment with a CAGR of 32.1%.

-

By Technology: Machine Learning led with 39.7% share, while Deep Learning is the fastest-growing segment with a CAGR of 38.5%.

-

By Application: Weather Forecasting led with 34.2% share, while Disaster Risk Reduction is the fastest-growing segment with a CAGR of 40.3%.

AI-Based Climate Modelling Market Segment Analysis

By Component: Software Led the Market, while Services is the Fastest-growing Segment in the Market

Software dominates the AI-based climate modeling market, as it includes core AI/ML platforms, simulation tools, and data processing frameworks used to build, train, and run climate models. Demand is driven by research institutions, government agencies, and private firms seeking scalable, off-the-shelf AI software to accelerate climate analysis and forecasting workflows without developing in-house solutions from scratch.

Services represent the fastest-growing segment due to the rising need for consulting, system integration, model tuning, and managed AI operations. Many organizations lack the expertise to deploy and maintain complex AI climate models. The segment’s growth is amplified by increasing outsourcing of climate analytics by agriculture, energy, and insurance sectors.

By Deployment: Cloud Segment Dominate the Market, while On-premises is the Fastest-growing Segment

Cloud deployment leads the market owing to its scalability, lower upfront cost, and ease of accessing distributed computing resources needed for AI model training. Cloud platforms (AWS, Google Cloud, Microsoft Azure) offer climate-specific AI services, massive storage for satellite data, and pay-as-you-go pricing, making advanced modeling accessible to smaller organizations and research groups.

On-premises deployment is growing rapidly in sectors with strict data privacy, sovereignty, or latency requirements, such as national defense, secure government climate research, and organizations with existing HPC investments. On-premises solutions provide full control over data and models, essential for sensitive or proprietary climate research.

By Technology: Machine Learning led, while Deep Learning is the fastest-growing segment.

Machine Learning (ML) holds the largest technology share due to its proven effectiveness in tasks, such as pattern recognition, regression analysis, and predictive modeling using historical climate data. Their relative interpretability and lower computational requirements compared to deep learning make them the first choice for many operational climate applications.

Deep Learning is the fastest-growing technology segment, driven by its superior performance in processing unstructured data such as satellite imagery, radar data, and climate simulation outputs. Increased availability of labeled datasets and advancements in transfer learning are accelerating deep learning adoption in cutting-edge climate research.

By Application: Weather Forecasting Led the Market, while Disaster Risk Reduction is the Fastest-growing Segment Globally

Weather Forecasting is the largest application segment, as AI enhances the accuracy and lead time of short-to-medium-range weather predictions. AI models assimilate real-time observational data to correct biases in numerical weather prediction (NWP) outputs, providing crucial updates for aviation, agriculture, and event planning.

Disaster Risk Reduction is the fastest-growing application, fueled by the rising economic and human toll of climate-related disasters. Governments and humanitarian organizations invest heavily in AI tools for disaster preparedness and response, creating a high-growth market for predictive risk analytics and decision-support platforms.

AI-Based Climate Modelling Market Regional Analysis:

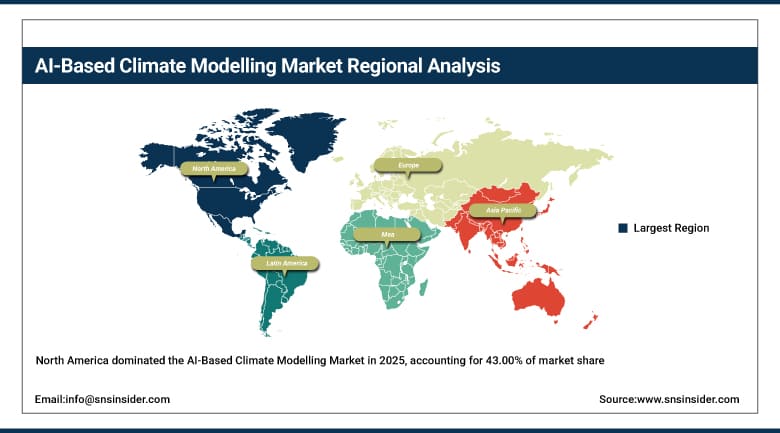

North America AI-Based Climate Modelling Market Insights:

With a 43.00% share in 2025, North America led the market due to the robust public support (NOAA, NASA, DOE), top tech companies (Google, IBM, and Microsoft) in climate AI, and widespread use in weather services, agriculture, and energy. Regional leadership is strengthened by strong venture capital investments in climate tech businesses and collaborations between national labs and AI companies.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe AI-Based Climate Modelling Market Insights:

Europe accounted for a significant share in 2025, supported by the EU’s Green Deal, Horizon Europe funding, and collaborative projects, such as Destination Earth (DestinE). Strong academic research in climate science, combined with strict emissions reporting regulations, drives AI model adoption for climate risk assessment and policy planning across member states.

Asia Pacific AI-Based Climate Modelling Market Insights

Due to its high climate sensitivity, government smart-city programs, and growing investments in artificial intelligence (AI) for disaster management, Asia Pacific is predicted to expand at the quickest CAGR, or roughly 37.20%, between 2026 and 2033. With the help of expanding cloud AI infrastructure, nations like Australia, Japan, and India are implementing AI models for agricultural resilience, flood forecasting, and monsoon prediction.

Middle East & Africa and Latin America AI-Based Climate Modelling Market Insights

In 2025, these regions together demonstrated rapid adoption, propelled by partnerships with international tech providers, international climate finance, and the need for climate adaptation in water-scarce and agricultural sectors. Although market penetration is still lower than in industrialized nations, use cases include drought prediction, desertification monitoring, and early-warning systems for extreme weather.

AI-Based Climate Modelling Market Competitive Landscape:

IBM Corporation

IBM Corporation (founded 1911) is a global technology leader providing AI and hybrid cloud solutions. Its climate modeling portfolio includes IBM Environmental Intelligence Suite, which leverages AI, IoT, and geospatial analytics for climate risk analysis, weather forecasting, and carbon accounting. IBM partners with research institutes and enterprises to deliver scalable climate insights.

-

January 2025, IBM enhanced its AI climate models with generative AI capabilities for automated climate report generation and scenario analysis, integrated within its Watsonx.ai platform.

Google LLC (Alphabet Inc.)

Google LLC (founded 1998) applies its AI expertise to climate science through Google Research and Google Cloud. Key initiatives include weather and flood forecasting models (MetNet), carbon footprint tracking tools, and AI for sustainable agriculture. Google collaborates with governments and NGOs to improve climate resilience using scalable AI.

-

November 2024, Google announced a global expansion of its Flood Hub AI platform, providing flood forecasts up to 7 days in advance across over 80 countries using deep learning models.

Microsoft Corporation

Microsoft Corporation (founded 1975) integrates AI for climate through Microsoft Azure Sustainability Cloud, AI for Earth program, and partnerships with meteorological organizations. Its platform offers AI tools for emissions tracking, climate prediction models, and environmental monitoring, supporting businesses and governments in climate action and reporting.

-

March 2025, Microsoft launched AI-powered “Climate Risk Navigator” on Azure, combining satellite data and machine learning to assess physical climate risks for infrastructure and supply chains.

AI-Based Climate Modelling Market Key Players:

-

IBM Corporation

-

Google LLC (Alphabet Inc.)

-

Microsoft Corporation

-

NVIDIA Corporation

-

Amazon Web Services, Inc.

-

Boulder AI

-

ClimateAI, Inc.

-

Jupiter Intelligence, Inc.

-

Gro Intelligence

-

One Concern, Inc.

-

PrecisionHawk, Inc.

-

Descartes Labs, Inc.

-

Meteomatics AG

-

Atmo, Inc.

-

Climavision

-

Salient Predictions, Inc.

-

Spire Global, Inc.

-

Tomorrow.io

-

Ambienta SGR

-

EcoChain, Inc.

| Report Attributes | Details |

|---|---|

|

Market Size in 2025E |

USD 436.61 Million |

|

Market Size by 2033 |

USD 4626.18 Million |

|

CAGR |

CAGR of 34.32% From 2026 to 2033 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2033 |

|

Historical Data |

2022-2024 |

|

Report Scope & Coverage |

Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

|

Key Segments |

• By Component (Software, Services) |

|

Regional Analysis/Coverage |

North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

|

Company Profiles |

IBM Corporation, Google LLC (Alphabet Inc.), Microsoft Corporation, NVIDIA Corporation, Amazon Web Services, Inc., Boulder AI, ClimateAI, Inc., Jupiter Intelligence, Inc., Gro Intelligence, One Concern, Inc., PrecisionHawk, Inc., Descartes Labs, Inc., Meteomatics AG, Atmo, Inc., Climavision, Salient Predictions, Inc., Spire Global, Inc., Tomorrow.io, Ambienta SGR, EcoChain, Inc. |

Frequently Asked Questions

Ans- AI-based climate models face challenges in trust and adoption due to their complex, "black box" nature, making them hard to interpret and explain.

Ans- The rising frequency of extreme weather events drives the demand for accurate AI-based climate models for better disaster preparedness and response.

Ans- Asia-Pacific is expected to register the fastest CAGR during the forecast period.

Ans- The CAGR of the AI-Based Climate Modelling Market during the forecast period is 34.32% from 2024-2032.

Ans - The AI-Based Climate Modelling Market was valued at USD 242.0 million in 2023 and is expected to reach USD 1715.2 million by 2032

Get in Touch