Semiconductor Foundry Market Report Scope & Overview:

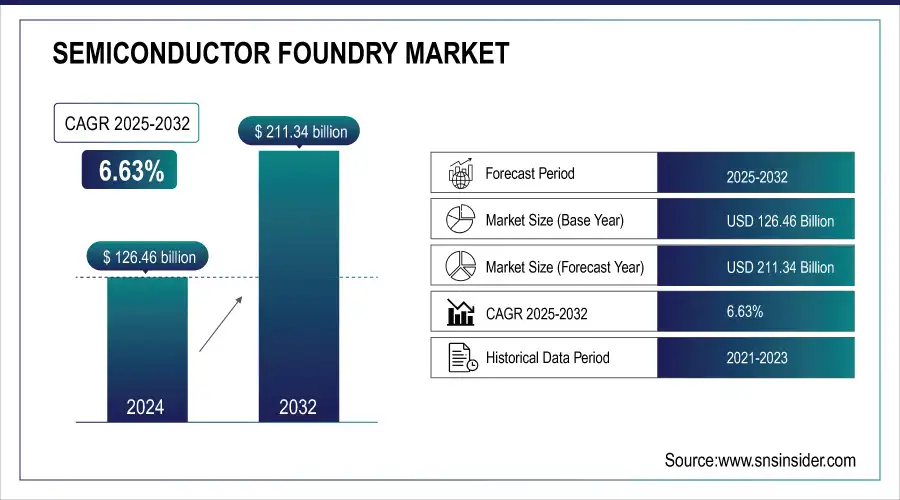

The Semiconductor Foundry Market size is expected to be valued at USD 126.46 Billion in 2024. It is estimated to reach USD 211.34 Billion by 2032 with a CAGR of 6.63% over the forecast period 2025-2032.

The Semiconductor Foundry market is set to experience substantial growth, fueled by the increasing need for cutting-edge electronics, IoT gadgets, and the rise of AI and ML usage. The CHIPS Act of 2022, approved by Congress, is essential for enhancing U.S. semiconductor production. This legislation is aimed at the decline in domestic chip manufacturing, which has decreased from 37% in 1990 to only 12% currently, as a result of other nations making bigger investments in their chip sectors. The CHIPS Act allocates $52 billion in funding for chip manufacturing and research and includes a 25% tax incentive to promote domestic production. These actions are focused on boosting U.S. dominance in semiconductor technology, enhancing supply chains, and increasing national security. The Act helps semiconductor companies by providing incentives to construct, enhance, and extend their operations in the U.S., leading to market expansion and stronger international competition. Semiconductor manufacturing against foreign subsidies. The investments made in the foundry sector have the potential to greatly benefit the market by fostering innovation and expanding capacity, especially in the production of crucial advanced chips for various industries. Shifting attention back to domestic production will strengthen the U.S. supply chain and establish the country as a frontrunner in the global semiconductor market, boosting the growth of the foundry market and securing the nation's leading position in technological progress.

Get more information on Semiconductor Foundry Market - Request Sample Report

One of the main factor behind this growth is the increasing need in different industries such as the thriving artificial intelligence (AI) sector, 5G networks, and the Internet of Things (IoT). Recent sales figures show a clear rebound in the semiconductor market following a difficult 2023, as global semiconductor sales reached USD 51.3 billion in July 2024, showing an 18.7% boost from the prior year and a 2.7% uptick from June 2024. This revival is supported by a decrease in inflation, which has reduced price fluctuations and increased demand again. Generative AI, especially in the AI industry, has played a major role in driving growth and sparking more attention and advancements in semiconductor technologies. It is anticipated that this pattern will persist, with a growing demand for AI chipsets as the technology advances. The semiconductor industry is expected to expand by 16% this year, exceeding previous forecasts, with global sales set to hit USD 611.2 billion, as per the World Semiconductor Trade Statistics (WSTS). It is expected that the Americas will be at the forefront of this growth, with a projected rise of more than 25%. In the future, it is anticipated that worldwide sales will keep increasing, with a projected growth of 12.5% for 2025, reaching USD 687.4 billion. Moreover, the expected reduction in Federal Reserve interest rates could also boost market activity, thereby assisting in the ongoing growth of the semiconductor foundry industry.

Market Size and Forecast:

-

Market Size in 2024 USD 126.46 Billion

-

Market Size by 2032 USD 211.34 Billion

-

CAGR of 6.63% From 2025 to 2032

-

Base Year 2024

-

Forecast Period 2025-2032

-

Historical Data 2021-2023

Semiconductor Foundry Market Trends:

-

Rapid adoption of e-commerce platforms for semiconductor sales, enabling global customer reach and streamlined distribution.

-

Rising demand for customized semiconductor solutions tailored to AI, IoT, and 5G applications.

-

Integration of automation technologies such as goods-to-person systems and AS/RS for efficient order fulfillment.

-

Increasing emphasis on fast delivery, traceability, and operational accuracy in online semiconductor transactions.

-

Expansion of digital platforms driving market penetration and transforming traditional semiconductor supply chains.

Semiconductor Foundry Market Growth Drivers:

-

Advancements in E-Commerce Driving Growth in Semiconductor Foundry Market.

The semiconductor foundry industry is experiencing substantial growth, mainly fueled by the increase in e-commerce solutions. Historically dependent on intricate supply chains and distribution networks, the sector has been revolutionized by the efficiency and accessibility provided by online platforms. E-commerce has made buying, selling, and distributing semiconductor products more efficient, enabling foundries to expand their customer reach and enter new markets worldwide. The growing need for personalized semiconductor solutions for AI, IoT, and 5G has driven the digital transformation. E-commerce platforms allow customers to customize and purchase personalized semiconductor products, fulfilling specific requirements for high-performance, power-saving chips. The semiconductor sector's role in the growth of online sales, which reached USD 4.28 trillion in 2020, highlights the significance of digital platforms in expanding the market. The growth of online platforms enables immediate display of products and direct communication between sellers and consumers, improving market expansion and operational effectiveness. With the evolution of e-commerce affecting industry trends, semiconductor foundries are utilizing automation technologies to manage various order sizes, enhance precision, and increase customer satisfaction. Automated systems like goods-to-person technology and AS/RS are being more commonly utilized in managing e-commerce fulfillment to minimize errors and maximize space efficiency. This advancement supports quick order processing and also meets the increasing need for fast delivery and traceability in online transactions. As a result, e-commerce is crucial in driving growth and technological progress in the semiconductor foundry market.

Semiconductor Foundry Market Restraints:

-

The need for high capital poses an entry barrier in the Semiconductor Foundry Market.

The high costs of setting up and maintaining advanced manufacturing facilities significantly limit the Semiconductor Foundry market. Constructing cutting-edge semiconductor fabs requires massive financial investments, typically reaching several billion dollars. This important investment is motivated by the requirement of advanced machinery and technology, including photolithography machines, etchers, and deposition tools, essential for manufacturing chips with the newest node sizes like 5nm or 3nm. The significant expenses connected with these advanced tools are made worse by the continual costs of upkeep and updates to stay current with quickly changing technology. Moreover, setting up new fabs requires significant infrastructure improvements such as clean rooms, power sources, and cooling systems, which all add to the total cost. The challenging environment for new entrants is due to the high capital barrier that makes it difficult to secure funding. For current foundries, it restricts their ability to quickly increase production in reaction to sudden changes in market demand or to invest in new technologies. The financial pressure also affects their capacity to withstand economic downturns or interruptions in the supply chain, since the fixed costs of factory investments pose a notable risk. As a result, the significant capital demands of semiconductor fabs not only limit new competitors from entering the market but also put current foundries in a delicate situation where they must manage investing in technology while keeping their finances stable. This economic pressure highlights the importance of strategic investment planning and strong financial management in the Semiconductor Foundry market.

Semiconductor Foundry Market Segment Analysis:

By Foundry Type

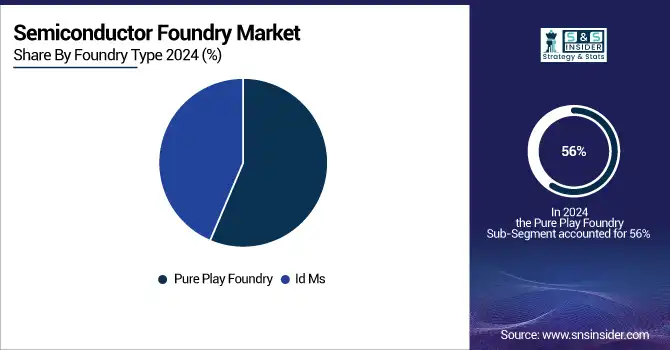

In 2024, Pure Play Foundry secured the highest revenue share in the Semiconductor Foundry market, accounting for 56% of the market share. Their strong market position is primarily due to their specialized business strategies and innovative approaches that address the specific requirements of fabless semiconductor firms. Pure Play Foundries focus only on semiconductor manufacturing, as opposed to Integrated Device Manufacturers (IDMs) that manage design and manufacturing internally. This particular focus allows them to allocate significant resources to advanced manufacturing technologies, guaranteeing their position as industry leaders. A major factor in the success of Pure Play Foundries is their skill in quickly embracing and incorporating cutting-edge process technologies. For example, Taiwan Semiconductor Manufacturing Company (TSMC), a top player in the Pure Play Foundry industry, has been consistently pioneering smaller node technologies like the 5nm and 3nm processes. These advancements are crucial in satisfying the increasing need for high-performance, energy-efficient chips utilized in various Technology ranging from smartphones to artificial intelligence and autonomous vehicles. Pure Play Foundries have taken proactive measures to increase their capacity in order to meet the growing demand for semiconductors.

By Industry

Based on Industry, Consumer Electronics is captured the largest share revenue in Semiconductor Foundry market with 38% of share in 2024. The strong presence is mainly driven by the constant need for high-tech electronic gadgets such as smartphones, tablets, smart wearables, and home automation products. As consumer demand moves towards stronger, more energy-efficient, and feature-packed devices, there has been a significant increase in the demand for advanced semiconductors, which is benefiting the foundry market. Semiconductor foundries are vital in the ecosystem as they enable large-scale production of advanced chips needed for high-demand products. These more compact and efficient chips help manufacturers fit more features into smaller devices and cut down on power usage, a major advantage in the competitive consumer electronics industry. The increased utilization of technologies like 5G, artificial intelligence (AI), and the Internet of Things (IoT) has also heightened the need for high-quality semiconductors. In response to the increased need, top foundries have sped up their manufacturing capabilities and have launched custom chips designed for consumer electronic use.

Semiconductor Foundry Market Regional Analysis:

North America Semiconductor Foundry Market Insights

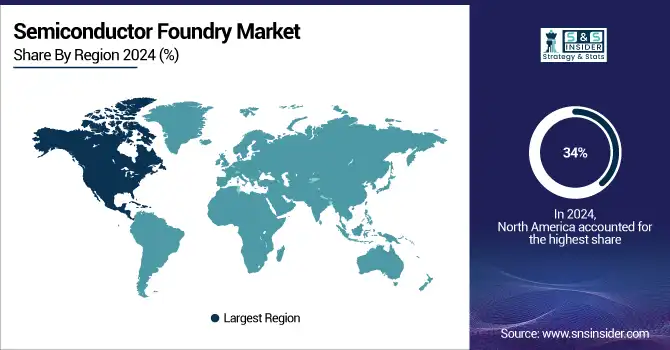

North America dominated the largest share revenue in Semiconductor Foundry Market with 34% of share in 2024. The leadership in this area is supported by the region's solid innovation network, sturdy infrastructure, and substantial funds in semiconductor production. North America is where many leading tech companies and factories are located, leading the way in advancing semiconductor technologies vital to industries like consumer electronics, automotive, and telecommunications. Intel, Global Foundries, and Texas Instruments have played a key role in strengthening North America's position in the Semiconductor Foundry market. For example, Intel has made significant investments in expanding its foundry services through the Intel Foundry Services (IFS) initiative, which aims to offer advanced process technologies and production capacity to outside clients.

Get Customized Report as per your Business Requirement - Request For Customized Report

Asia Pacific Semiconductor Foundry Market Insights

Asia-Pacific holds the second biggest portion of revenue in the Semiconductor Foundry market, accounting for 27% of the share in 2024. The rapid technological advancements, significant investments, and strong manufacturing capabilities in key countries like Taiwan, South Korea, China, and Japan are what drive the prominence of this region. The presence of industry giants in Asia Pacific has propelled the region to become a strong force in semiconductor manufacturing, driving innovation and production capacity. Taiwan is where you can find Taiwan Semiconductor Manufacturing Company (TSMC), the biggest independent Semiconductor Foundry in the world. TSMC has played a crucial role in promoting the growth of the area, always at the forefront of advancements in process technology.

Europe Semiconductor Foundry Market Insights

Europe’s semiconductor foundry market is expanding due to rising demand for automotive electronics, industrial automation, and 5G infrastructure. Governments are supporting domestic manufacturing with funding programs to reduce reliance on Asian supply chains. Increasing adoption of EVs and AI-driven applications further strengthens the region’s growth prospects and strategic importance.

Latin America (LATAM) and Middle East & Africa (MEA) Semiconductor Foundry Market Insights

LATAM and MEA semiconductor foundry markets are gradually growing, driven by rising consumer electronics, telecommunications, and automotive needs. Limited local production capacity encourages investment partnerships and imports. Governments are introducing initiatives to attract semiconductor manufacturing, while digital transformation, 5G adoption, and smart infrastructure projects create new opportunities for regional expansion.

Semiconductor Foundry Market Key Players:

- Taiwan Semiconductor Manufacturing Company

- United Microelectronics Corporation

- Samsung Semiconductor

- Vanguard International Semiconductor Corporation

- Powerchip Semiconductor Manufacturing

- Global Foundries

- Semiconductor Manufacturing International Corporation

- Fujitsu Semiconductor

- Tower Semiconductor

- X-FAB Silicon Foundries

Competitive Landscape for Semiconductor Foundry Market:

Taiwan Semiconductor Manufacturing Company (TSMC) is the world’s largest pure-play semiconductor foundry, dominating the global market with advanced process technologies, including 5nm and 3nm nodes. Serving major clients in AI, 5G, HPC, and automotive sectors, TSMC plays a pivotal role in driving innovation, capacity expansion, and supply chain resilience.

-

On July 28, 2023, TSMC hosted the opening ceremony of its worldwide research and development center in Hsinchu, Taiwan. It united clients, industry and academic research and development collaborators, collaborators in the design community, and high-ranking government officials to commemorate the company's latest center for advancing next-generation semiconductor technology.

Apple Inc. is a global leader in consumer electronics, software, and digital services, widely recognized for its iPhone, iPad, Mac, and wearables. In the semiconductor space, Apple designs its proprietary chips, such as the M-series and A-series, while relying on foundries like TSMC for advanced manufacturing to power its ecosystem.

-

In January 2023, Apple revealed intentions to create new Mac Book Air and iMac models featuring their own Apple M3 processor manufactured using a three-nanometer process. Following these strategies, by December 2022, TSMC initiated large-scale manufacturing of its three-nanometer chip technology intended for upcoming iterations of Macs, iPhones, and other Apple gadgets.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 126.46 Billion |

| Market Size by 2032 | USD 211.34 Billion |

| CAGR | CAGR of 6.63% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments |

• By Offering (Technology,Services) • By Foundry Type(Id Ms, Pure Play Foundry) • By Type (10/7/5 Nm, 16/14 Nm, 20 Nm) • By Industry (Automotive, Aerospace, Consumer Electronics Healthcare, Industrial, Pure Idms) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles |

Taiwan Semiconductor Manufacturing Company, United Microelectronics Corporation, Samsung Semiconductor, Vanguard International Semiconductor Corporation, Powerchip Semiconductor Manufacturing, Global Foundries, Semiconductor Manufacturing International Corporation, Fujitsu Semiconductor, Tower Semiconductor, X-FAB Silicon Foundries & Other Players. |

Frequently Asked Questions

The North America led the Semiconductor Foundry Market.

The Consumer Electronics is leading segment in the market revenue share in 2024.

The Semiconductor Foundry market is currently experiencing rapid growth. This surge is primarily fueled by the heightened adoption of semiconductors in autonomous driving technology, prompting semiconductor foundries to enhance their focus on automotive chip manufacturing, thereby propelling market growth. These advancements are poised to benefit numerous industries, including telecommunications, computing and networking, consumer electronics, and automotive.

The expected CAGR of the global Semiconductor Foundry Market during the forecast period is 6.63%.

The Semiconductor Foundry Market was valued at USD 126.46 Billion in 2024.

Get in Touch